These 7 steps can give Boeing a path to recovery.

Source link

These 7 steps can give Boeing a path to recovery.

Source link

In a new development, VeChain (VET) has announced the introduction of its latest No-Code Tokenized Asset Marketplace-as-a-Service platform (MaaS), fueling optimism within the community of an impendent price uptick.

The announcement also featured the collaboration of the MotoGP racing team Gresini Racing as its first enterprise client. By collaborating with Gresini Racing, an enormous fan base will be offered digital collectibles through the MaaS platform.

With the launch of its No-Code Tokenized Asset Marketplace (MaaS) platform, VeChain has made tremendous progress toward increasing mass adoption of blockchain technology. VeChain’s continuous goal to promote widespread blockchain technology adoption by removing technological hurdles is consistent with this user-friendly strategy.

Since its founding, VeChain has created several use cases powered by blockchain applications. These include product authentification, creating new digital communication channels, provenance and sustainability traceability, and others. This demonstrates its understanding of the tremendous potential that its technologies have for Web 3.

Given the rise in demand for tokenizing Real-World assets (RWAs) solutions, the introduction of MaaS seems appropriate. Furthermore, NFC functionality and support for “Phygitals,” or real-world physical assets with NFT/digital counterparts, will be added later in the platform.

Specifically, this innovation was created to significantly influence the digital asset market. It aims to provide enterprise and individual builders with an “easy-to-use white-label NFT platform for digital asset sales” and transfers that require little to no programming.

MaaS applications are diverse and address the increasing need for platforms that enable asset tokenization. Blackrock‘s latest application for a Real World Asset (RWA) tokenization fund highlighted this path. So far, the No-Code Tokenized Asset Marketplace-as-a-Service platform (MaaS) is expected to be fully operational later this year.

Despite the launch of MaaS, VeChain (VET) is witnessing a daily downtrend of nearly 2%. However, in the weekly timeframe, the crypto asset has increased by over 5%, suggesting an upward move.

As of the time of writing, VET was trading at $0.0440, with its market cap dropping by 2.78% in the past day. Meanwhile, its trading volume is down by about 24% in the last 24 hours.

In August 2018, during a downside trend in the cryptocurrency market, VET made its market debut. However, following the 2021 bull run, VET rose to the top, peaking at $0.281 before the cycle ended.

Featured image from Shutterstock, chart from Tradingview.com

Disclaimer: The article is provided for educational purposes only. It does not represent the opinions of NewsBTC on whether to buy, sell or hold any investments and naturally investing carries risks. You are advised to conduct your own research before making any investment decisions. Use information provided on this website entirely at your own risk.

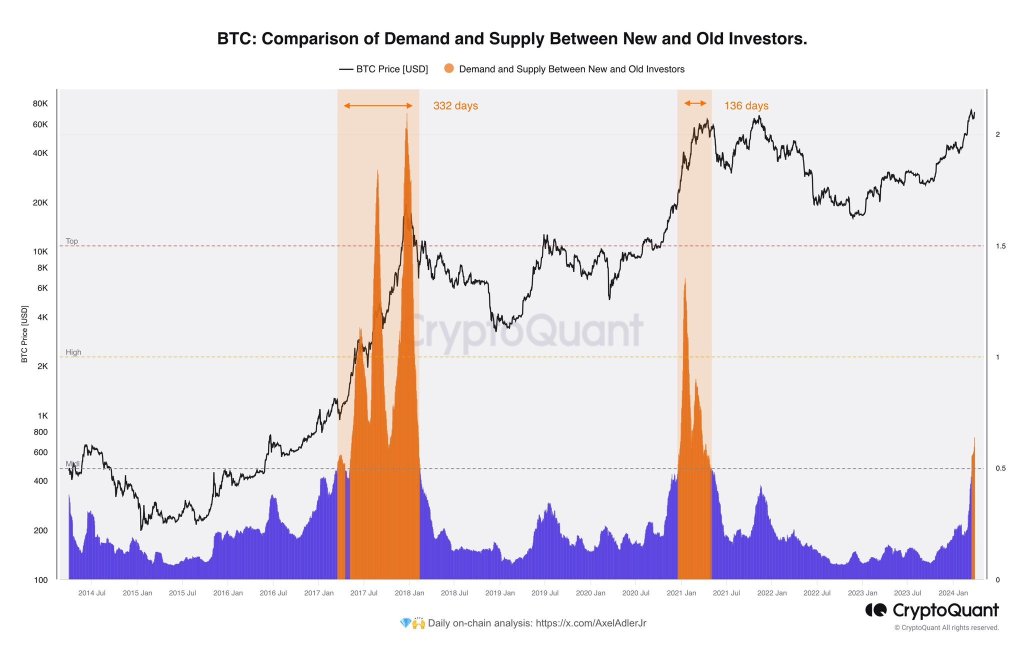

Ki Young Ju, the founder of CryptoQuant, a blockchain analytics firm, has noticed a curious trend. In a post on X, the founder shared a snapshot suggesting that Bitcoin “old whales” might be shifting their holdings to “new whales,” mainly traditional finance heavyweights like Fidelity and BlackRock.

The United States Securities and Exchange Commission (SEC) recently approved these new whales to list spot Bitcoin exchange-traded funds (ETFs) for all investors.

While a definitive sell-off isn’t confirmed, commentators replying to the founder’s post believe these “old whales” could be mitigating risk. In their assessment, moving their Bitcoin stash from self-custody to a regulated investment vehicle like spot Bitcoin ETFs is a better measure of covering unexpected eventualities.

If this is the approach, then it could prove strategic. Bitcoin holders can transact without depending on a third party. Notably, this development coincides with a significant drop in BTC inventory on major exchanges like Coinbase and Binance, as well as at GBTC.

The decline has accelerated since the introduction of spot Bitcoin ETFs, hinting at a potential departure from exchanges. Meanwhile, the operators of GBTC are unwinding the product and converting it to a spot Bitcoin ETF following a court decision.

Even so, that “old whales” are moving their coins to centralized products like ETFs contradicts the core philosophy of BTC as a tool for financial self-sovereignty. Whether more users, mainly retailers, will choose to own spot Bitcoin ETF shares rather than the underlying coins directly remains to be seen.

Institutions might be obliged by law to use a regulated product if they need to be exposed to BTC. However, retailers can choose to buy directly from exchanges or mine. This freedom might lead to more retailers opting to buy BTC.

This trend emerges ahead of the highly anticipated Bitcoin halving. This event is set for mid-April 2024 and will further reduce BTC’s circulating supply, potentially driving higher prices. Before then, BTC prices are firm, steady above $70,000 at the time of writing.

Feature image from DALLE, chart from TradingView

Disclaimer: The article is provided for educational purposes only. It does not represent the opinions of NewsBTC on whether to buy, sell or hold any investments and naturally investing carries risks. You are advised to conduct your own research before making any investment decisions. Use information provided on this website entirely at your own risk.

Sam Bankman-Fried, the former CEO of FTX, was sentenced to 25 years in jail today in a packed courtroom, marking a significant moment in the legal scrutiny of the crypto industry. He will be 57 years old when he is released. The sentencing, as detailed by Inner City Press, comes after a series of legal proceedings that shed light on the complexities and potential vulnerabilities within the digital asset space.

Bankman-Fried, dressed in a light brown jail uniform from MDC-Brooklyn, faced the judgment of Judge Lewis A. Kaplan, who, after considering the pre-sentence report and the guidelines disputes, delivered a sentence that reflects the gravity of the crimes committed. The courtroom, filled with prosecutors, defense lawyers, and an FBI agent, bore witness to the culmination of a case that has been closely followed by both the crypto community and the general public.

The legal proceedings highlighted the extensive financial losses incurred by investors, lenders, and customers, with Judge Kaplan rejecting the defense’s argument about the loss amount. The court found that investors lost $1.7 billion, lenders lost $1.3 billion, and customers faced an $8 billion shortfall. These figures underscore the scale of the fraud and the impact on the victims involved.

The defense had previously sought leniency, citing Bankman-Fried’s autism diagnosis and arguing for a reduced sentence of 63 to 78 months. However, the prosecution argued for a substantial prison term of 50 years.

Judge Kaplan’s decision to vary downward from the Guidelines range while still acknowledging the significant number of victims and the use of sophisticated means emphasizes the complexity of sentencing in cases involving emerging technologies and financial structures. The finding of obstruction of justice, including attempted witness tampering and perjury, further emphasized the deliberate actions taken by Bankman-Fried to mislead and defraud.

During the sentencing hearing, a poignant moment unfolded as victims were given the opportunity to address the court. One such victim, Sunil Kavuri, who traveled from London specifically for this purpose, shared his experiences and the impact of the FTX collapse on him and others. Kavuri highlighted the ongoing struggles faced by victims, challenging the narrative that the loss was zero and criticizing the handling of the bankruptcy estate. He pointed out the significant discrepancies in the valuation and sale of assets, including a token that significantly appreciated in value after being sold at a discount and the sale of Solana tokens at a 70% discount.

Kavuri’s testimony underscored the real and continuing harm suffered by those affected, including the tragic note that at least three individuals had committed suicide as a result of the fraud. Judge Kaplan acknowledged Kavuri’s points, reinforcing the gravity of the situation and the inaccuracies in claims that customers would be made whole. This victim’s statement added a deeply personal dimension to the proceedings, emphasizing the human cost of financial crimes and the need for accountability beyond the sentencing of Bankman-Fried.

In a heartfelt defense of his client, Sam Bankman-Fried’s attorney, Mark Mukasey, presented a contrasting image of the former FTX CEO to the court. Mukasey argued that Bankman-Fried’s actions, while resulting in significant financial fallout, were not driven by the same malice or predatory intent that characterized other high-profile financial criminals, such as those who stole from Holocaust survivors. He emphasized that Bankman-Fried was not a “ruthless financial serial killer” but rather someone who made decisions based on mathematical calculations, not with the intention to cause personal pain.

Mukasey also relayed personal insights from Bankman-Fried’s mother, who described her son as misunderstood and not fitting the mold of a “greedy swindler.” According to Mukasey, Bankman-Fried did not abscond with funds but remained engaged until the end, with a genuine desire to see people repaid. This narrative was allowed to be presented in court partly due to Judge Kaplan’s decision to depart from the usual practice of enumerating the papers considered for sentencing, acknowledging the overwhelming volume of last-minute submissions from both the defense and the prosecution.

The defense’s portrayal of Bankman-Fried aimed to humanize him and differentiate his case from other financial frauds, suggesting that while the consequences of his actions were severe, his motivations were not inherently malicious. Mukasey’s statement also served as an acknowledgment of the victims’ suffering, expressing an understanding of their pain and a commitment to appeal, while maintaining respect for the jury’s verdict.

In a plea to the court, speaking directly Bankman-Fried admitted,

“I made a lot of mistakes. But that’s not how the story ended. Customers weren’t paid back. FTX didn’t survive that. Yeah, customers have been given conflicting claims. That’s caused a lot of damage. They could have been paid back.”

In a moment of candor, Sam Bankman-Fried expressed a somber reflection on his future, acknowledging the likelihood that his ability to contribute meaningfully to society may be irreparably diminished. He admitted to the court that his capacity to make an impact is severely limited by incarceration and that the length of his sentence, whether it be 5 or 40 years, is beyond his control. He stated,

“My useful life is probably over. I’ve long since given what I had to give. I can’t do it from prison.”

Bankman-Fried also addressed the perception of his actions, recognizing the stark contrast between his alleged intentions and how prosecutors, the court, and the media interpreted them. He also said he now expects customers to be repaid. He commented, “I think I failed at that. I’m not sure why, but I do think I did.” He also referred to a specific instance involving a text to the general counsel, which he claimed was an attempt to assist, though it was not viewed as such by others. Even on the day of his sentencing, Bankman-Fried continues to assert that he did not steal user funds maliciously.

However, in his judgment, Judge Kaplan asserted that he believed much of Bankman-Fried’s public rhetoric “was an act” designed to obtain power and influence.

According to Inner City Press, before the sentence was issued, the government argued,

“The defendant is not a monster but he committed gravely serious crimes that harmed many people – and he would consider doing it again. So, 40 to 50 years.”

In announcing the sentence, Judge Kaplan proclaimed that Bankman-Fried was nothing short of a “performer.”

“When not lying, he was evasive, hair splitting, trying to get the prosecutors to rephrase questions for him. I’ve been doing this job for close for 30 years. I’ve never seen a performance like that.”

His sentencing was reported by Inner City Press as follows,

“It is the judgment of the court that you are sentenced to 240 months then consecutive 60 [etc] for a total of 300 months [25 years].”

The implications of today’s sentencing extend beyond the immediate legal consequences for Bankman-Fried. They touch on broader questions about the regulation of digital assets, the protection of investors, and the future of digital asset markets. As the industry grapples with these challenges, the outcome of this case will likely influence discussions and decisions on how best to navigate the complex intersection of technology, finance, and law.

This article will be updated with additional details as they become available.

Home Depot on Thursday said it is acquiring SRS Distribution in an $18.25 billion deal, the latest and largest sign of its ambitions to drive sales by winning more business from contractors, roofers and other home professionals.

The home improvement retailer expects the acquisition to close this fiscal year, which ends in late January. It said it will finance the deal through cash on hand and debt.

Home Depot already draws half of its business from pros, while the other half comes from do-it-yourself customers. With the deal, the Atlanta-based company is making yet another push to gain the customers who tackle complex and lucrative construction jobs, particularly as homeowners pull back on DIY projects. That was one of the priorities that Home Depot leaders laid out for this year. It’s also why the company has been opening a growing network of distribution centers that can stock large quantities of items that pros need, such as lumber or shingles, and deliver them directly to a job site.

The acquisition is the largest in Home Depot’s history.

In an interview with CNBC, CEO Ted Decker described the deal as “a complementary accelerator” to its efforts to attract more pros. He said the deal increases Home Depot’s total addressable market by $50 billion.

SRS Distribution sells supplies to professionals in the landscaping, pool and roofing businesses. It’s owned by two private equity firms, Leonard Green & Partners and Berkshire Partners.

The McKinney, Texas-based company has approximately 11,000 employees and 760 branches across 47 states. It also has a fleet of 4,000 delivery trucks and a dedicated salesforce that caters to the home pros, Decker said.

The acquisition adds to other recent deals that the retailer has made in the pro space. They include the approximately $8 billion acquisition of HD Supply, a national distributor of maintenance, repair and operations products in the multifamily and hospitality markets, in 2020. Last year, it also made two other acquisitions for undisclosed amounts: International Designs Group, which owns Construction Resources, a distributor of surfaces, appliances and other products that sells to home pros; and Temco, an appliance delivery and installation company.

Decker said he’s confident the deal will get approved by federal regulators, even as they increase scrutiny of mergers and acquisitions.

“With the separate customer base, different channels, different purchase occasions, we feel good that this will go through,” he said.

The acquisition is expected to be dilutive to Home Depot’s earnings per share due to amortization, but accretive in terms of cash earnings per share in the first year after the deal closes.

Home Depot has leaned into the pro business as its growth stagnates. The retailer, a major beneficiary of pandemic trends, has dealt with moderating sales as consumers take on fewer home projects and spend more on grocery bills and experiences. Over the past few quarters, customers have bought fewer big-ticket items and tackled smaller, less pricey projects.

Decker said last month on an earnings call that Home Depot would focus on opening new stores, attracting more pro sales and trying to make customers’ shopping experience more seamless.

Home Depot plans to open a dozen new stores during the fiscal year. It recently announced it will open four distribution centers that help support sales to pros.

The acquisition comes after the home improvement retailer said last month that it expects slower sales trends to continue. It said it anticipates total sales for the full year will grow about 1%, including an additional week in the fiscal year. Yet it expects comparable sales, which take out the effect of store openings and closures and do not include the additional week, to drop by about 1%.

Home Depot had a total of 2,335 stores across the U.S., Mexico and Canada as of the end of the fiscal year in late January. It has about 465,000 employees.

As of Wednesday’s close, shares of Home Depot are up about 11% this year. That’s slightly ahead of the 10% gains of the S&P 500. Home Depot’s stock closed at $385.89 on Wednesday, bringing its market value to about $382 billion.

Carnival (CCL -4.95%) and Coupang (CPNG 1.02%) may not seem out of favor, but zoom out. Both of these one-time highfliers are now trading more than 70% below their all-time highs.

If you have $1,000 to invest, you may want to consider one of these stocks. They’re on sale right now, at least compared to their historical peaks. Let’s take a closer look so you can decide if you want to go shopping.

The cruise line industry’s recovery is complete. Carnival posted encouraging financial results this week. Revenue rose 22% to $5.4 billion for the fiscal first quarter that ended on Feb. 29. The world’s largest cruise line operator posted an operating profit, reversing an operating deficit from the prior year. Interest expense would turn the profit into a loss on the bottom line, but the red ink was less than what it was targeting three months earlier.

Analysts also figured that Carnival’s profit would be worse than what it ultimately reported. This isn’t a surprise anymore. Carnival has been consistently exceeding bottom-line expectations lately, and the last three quarters have put up double-digit percentage beats.

| Quarter | EPS Estimate | Actual | Surprise |

|---|---|---|---|

| Q4 2022 | ($0.87) | ($0.85) | 2% |

| Q1 2023 | ($0.60) | ($0.55) | 8% |

| Q2 2023 | ($0.34) | ($0.31) | 9% |

| Q3 2023 | $0.75 | $0.86 | 15% |

| Q4 2023 | ($0.13) | ($0.07) | 46% |

| Q1 2024 | ($0.18) | ($0.14) | 22% |

Data source: Yahoo! Finance. EPS = earnings per share.

Carnival is posting record revenue results, and the future is even more exciting. Demand and what folks are willing to pay for a bon voyage have never been stronger. Its booked position for the final three quarters of fiscal 2024 is its best on record, with pricing and occupancy well ahead of where they were last year at this point.

Net yields — an industry metric that basically tracks revenue per available passenger cruise day without the more variable expenses including air transportation and travel agent commissions — is expected to approach 10% this fiscal year. Carnival and its rivals have overcome the prolonged pandemic-related shutdown, but the shares have not.

Image source: Getty Images.

Carnival stock has more than doubled since the start of last year, but it’s still trading 76% below the all-time high it reached in early 2018. Yes, cruise line operators had to do some pretty desperate things to stay afloat when they were largely unable to take on passengers for more than a year in the wake of the COVID-19 crisis. Carnival bloated its share count and its debt levels. However, the company is now turning the corner on profitability.

It expects to generate an adjusted profit of $1.28 billion, or $0.98 a share, pricing the stock at a reasonable 17.5 times forward earnings. Carnival now has the means to pay down its debt or repurchase shares without sacrificing growing its fleet. The future is bright for cruise line stocks, and Carnival is leading the way.

Let’s sail all the way to South Korea for our next stock on sale. Coupang is that country’s e-commerce leader, and it isn’t even close. With more than 100 distribution centers promising overnight delivery for orders placed before midnight, Coupang is within a 10-minute drive of 70% of South Korea’s shoppers.

Its latest report featured an encouraging trend. After a steady run of decelerating revenue growth since going public at $35 three years ago, revenue has now accelerated for four consecutive quarters.

| Period | Revenue Growth (YOY) |

|---|---|

| Q1 2021 | 74% |

| Q2 2021 | 71% |

| Q3 2021 | 48% |

| Q4 2021 | 34% |

| Q1 2022 | 22% |

| Q2 2022 | 12% |

| Q3 2023 | 10% |

| Q4 2023 | 5% |

| Q1 2024 | 13% |

| Q2 2024 | 16% |

| Q3 2024 | 21% |

| Q4 2024 | 23% |

Data source: Coupang. YOY = year over year.

Investors should be all over Coupang, but it continues to be a broken IPO. The stock is currently trading 74% below the $69 price point it hit when it peaked on its first day of trading in early 2021. Coupang was growing faster when it made its public debut, but it was oozing a lot of red ink at the time. It’s profitable now, armed with a cash-rich balance sheet to expand outside of its home turf and even make strategic acquisitions.

Coupang shares may not be cheap at just under 30 times next year’s projected earnings. Being an undisputed leader in an emerging industry in a country whose economy is on the rise deserves a premium. With momentum back on its side, the e-commerce company is on sale.

Rick Munarriz has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Coupang. The Motley Fool recommends Carnival Corp. The Motley Fool has a disclosure policy.

Baltimore City Fire Boat 2 floats past the Dali container vessel after it struck the Francis Scott Key Bridge that collapsed into the Patapsco River in Baltimore, Maryland, U.S., on Tuesday, March 26, 2024.

Bloomberg | Bloomberg | Getty Images

The collapse of a major Baltimore bridge and its knock-on effects could result in the biggest-ever marine insurance payout, the chair of insurance giant Lloyd’s of London said on Thursday.

Analysts have forecast that insured losses from the disaster would amount to a figure in the single-digit billions, after a huge cargo ship crashed into the Francis Scott Key Bridge on Tuesday. Six people were presumed dead.

“We’re beginning to deploy resources in anticipation of this being a very substantial claim for the industry. And for the Lloyd’s market, it’s going to take some time for for the complexity of the situation to unravel,” Bruce Carnegie-Brown told CNBC’s “Squawk Box Europe.”

“So, [it’s] very early days to call a number. I don’t at this point anticipate that it’s outside our realistic disaster scenario planning. It feels like a a very substantial loss, potentially the largest-ever marine insured loss, but not outside parameters that we plan for.”

Carnegie-Brown added that, while there would clearly be claims for the ship, cargo and the bridge, it is “second-order impacts” that would become “substantial.”

“A lot of business is going to be interrupted, supply chains are going to be interrupted by ships that are both trapped inside the port and of course, ships that were trying to gain access to the port that no longer can, and those second order effects will take some time to work through,” he said.

Baltimore is the 11th biggest port in the U.S. and the country’s busiest for the import and export of autos and light trucks. Supply chain operators are scrambling to minimize the impact on trade.

Morningstar DBRS analysts said in a Wednesday note that insured losses could total between $2 billion and $4 billion, depending on the length of time that the port is blocked. Such a figure would surpass the current highest amount, which was paid out from the capsizing of the Costa Concordia cruise ship in 2012.

Various insurance policies are likely to be triggered across marine liability and hull, property, cargo and business interruption.

“Despite the hefty insured losses, we expect they will remain manageable for the insurance industry as they will involve a large and diversified pool of well capitalized insurers and reinsurers,” Morningstar said.

Barclays puts the potential insurance claims between $1 billion and $3 billion.

The Singapore-flagged container vessel was chartered by Danish shipping giant Maersk and was carrying its customers’ cargo, but it was operated by charter vessel company Synergy Group. Early reports suggest the ship lost power before hitting the bridge.

Investigations will be carried out by authorities in both Singapore and the U.S. to establish legal liability, as part of a complex process that could take months or years.

Maersk will have had liability cover as the charterer, rather than as the operator of the vessel, David Osler, shipping and commodities principal analyst at Lloyd’s List Intelligence, told CNBC earlier this week.

Barclays analysts said in a Wednesday note that German autos manufacturers BMW, Mercedes and Volkswagen are most exposed, as European imports accounted for 40% to 50% of U.S. sales in recent years.

BMW told CNBC that the incident would not impact material supplies for its U.S. plant, and that the company was in contact with its logistics partner regarding imports. Volkswagen said its port operations were located on the seaboard side of the bridge and would not be impacted, but noted that it may face trucking delays. Mercedes noted that other entry ports, such as Brunswick, Georgia, would help ease import pressures.

“While there will be near term disruptions in auto imports and exports, I’m confident that Customs and Border Protection, regional ports, and terminal operators will work closely with the auto industry to identify optimal shipping alternatives until the Port of Baltimore resumes vessel operations,” Mitch Merriam, vice president of borders and maritime security at K2 Security Screening, told CNBC by email.

“The Port of Baltimore is going to suffer in the short term, but plans are already underway to divert and accommodate the additional traffic at other east coast ports, including Philadelphia, Norfolk, Savannah and Charleston. All of them can handle cars and light trucks.”

The port handles a wide range of goods including sugar and gypsum and is used by retailers such as Home Depot, Ikea and Amazon.

— CNBC’s Ganesh Rao and Lori Ann LaRocco contributed to this story.

Leading the downturn today, Fantom (FTM) contributes to the 2% drop in the crypto market after weeks of growth.

Fantom is one of those altcoins that followed the broader momentum of the market. The latest market data shows that the token is down 10% in the past 24 hours, but is still on the green in the bi-weekly timeframe at 14%. However, Fantom has a trick up its sleeve to curb this brewing bearishness potentially.

Sonic is the brand-new technology that the Fantom has been developing in the past 2 years. According to their latest blog post, Sonic was able to surpass the network’s 200 transactions per second metric. Although 200 TPS was already impressive compared to Ethereum’s 12 TPS, the network was quickly congested, and user experience deteriorated.

Kong said in the blog post:

“Sonic will be used to create a new best-in-class shared sequencer for L1 and L2 chains, capable of processing over 180 million daily transactions with real, sub-second confirmation times, and serve as the foundation to relaunch Fantom as an entirely new community-centric brand.”

This brand-new tech will cover all parts of the Fantom network, from bridging to a stablecoin launch, Sonic has it all.

Sonic Labs will also gain a slice of the pie as the foundation ultimately adds grant programs alongside the network upgrades.

Bitcoin is now trading at $70.396. Chart: TradingView

“We will continue to significantly scale and accelerate our Sonic Labs grant program for developers who build unique and valuable applications and public goods in categories including gaming, DeFi, social media, streaming, and now distributed AI,” Kong added.

This will significantly increase the size of Fantom’s user base, boosting investor confidence, and giving more room for developers to innovate.

Furthermore, the advancements brought forth by Sonic Labs in covering all aspects of the Fantom network, from bridging to the launch of a stablecoin, are poised to have a notable impact on Fantom’s market dynamics.

By streamlining processes, enhancing interoperability, and introducing new functionalities, these developments are likely to enhance the network’s attractiveness to investors and users alike.

We are thrilled to announce the first of many angel investors that have joined our round!

Sam Kazemian (@samkazemian ) is the founder of @FraxFinance ✦, one of the largest DeFi protocols with over $1.6bn in assets such as sfrxETH and the FRAX stablecoin.

🌐 Frax is committed… pic.twitter.com/zSL1XFNHYR

— Fantom Foundation (@FantomFDN) March 27, 2024

The Fantom Foundation X account announced today that Frax Finance Founder Sam Kazemain is the first angel investor for Sonic, stating that Frax will deploy natively issued assets on Sonic on its eventual launch.

Meanwhile, the bears have completely taken over the FTM market in the short to medium term. Investors in FTM could only hope that the broader market downturn will reverse in the coming weeks.

Featured image from Pexels, chart from TradingView

Disclaimer: The article is provided for educational purposes only. It does not represent the opinions of NewsBTC on whether to buy, sell or hold any investments and naturally investing carries risks. You are advised to conduct your own research before making any investment decisions. Use information provided on this website entirely at your own risk.

If you’re taking a required minimum distribution from an IRA, 401(k) or other tax-deferred account and don’t need the money to cover living expenses, where should you stash that unneeded cash?

Investors now need to start taking RMDs at age 73 or, if they were born after 1960, at age 75. Depending on the balances of your accounts, that distribution can be a sizable amount of money, perhaps more than you need to live on. One option is to reinvest that money, and a Roth IRA would seem to be a perfect choice: withdrawals from Roth accounts are tax-free – including all gains on your investments – and you’ll never need to take any of those pesky RMDs during your lifetime.

There’s just one catch: You can’t directly convert your RMDs to a Roth. But for some people, there is a potential workaround. For 2024, you can contribute up to $7,000 plus another $1,000 if you’re at least 50 years old – if you have enough earned income.

Get matched with a financial advisor to discuss your own retirement strategy.

The IRS defines earned income as money you get for working, such as wages, commissions, bonuses, tips and honorariums for speaking, writing or taking part in a conference or convention. Income generated by self-employment also counts. Income that doesn’t qualify includes taxable pension payments, interest income, dividends, rental income, alimony and withdrawals from Roth IRAs or other nontaxable retirement accounts, along with annuities, welfare benefits, unemployment compensation, worker’s compensation payments and your Social Security income.

Another restriction on Roth contributions is the income limit. Once your modified adjusted gross income (MAGI) hits $146,000 for a single filer or $230,000 for joint filers, your maximum Roth contribution starts phasing out up to $161,000 (single filers) or $240,000 (joint filers). After that, you’re no longer eligible to contribute.

You also need to remember that you need to wait five tax years after your first contribution to any Roth account before you can make withdrawals. Heirs who inherit your Roth will need to withdraw the entire balance within 10 years.

Consider speaking with a financial advisor to develop a tax-efficient retirement strategy.

If you don’t qualify to make a Roth contribution, you still have options to eliminate, reduce or delay your RMDs.

Roth conversion: You can convert your IRA to a Roth account, once you’ve taken your RMD for the year. You’ll pay taxes on the amount you convert, so one tactic is to convert the maximum amount available without pushing yourself into a higher tax bracket. Each Roth conversion carries its own five-year rule.

Charitable contribution: You can use a Qualified Charitable Distribution to donate some or all of your RMD to a charity recognized by the IRS and you won’t be taxed on the donated amount. To qualify, the money must be transferred directly from your IRA to the charity.

Keep working: Your 401(k) account with your current employer isn’t subject to RMDs if you’re still on the payroll. One tactic is to roll 401(k)s from previous employers into your current plan so that they won’t be subject to RMDs. Once you stop working, however, RMDs are required.

Be careful: The punishment for failing to take an RMD during the required time period is a hefty one – up to 50% of the missed RMD amount.

A financial advisor can help you navigate the particular risks and tradeoffs in your situation.

Structuring your retirement withdrawals to reduce your tax bite means looking at all your sources of income, including retirement accounts, RMDs, Social Security benefits, pensions and taxable investment income. For some people, withdrawing money from an IRA early in retirement can reduce the size of their eventual RMDs. If they also delay collecting their Social Security benefits, their benefit amount to increase by 8% each year until they reach 70 years old. Also, be sure to coordinate taxes, withdrawals and RMDs between spouses, and remember that a younger spouse’s RMDs won’t need to be taken until they reach age 73 or 75.

Other common retirement tax moves include investing in tax-free bonds, moving to a state with no income tax or estate tax, harvesting tax losses in taxable investment accounts and holding any taxable assets long enough to qualify for lower long-term capital gains tax rates.

To learn more about retirement planning and how to work toward your goals, talk to a financial advisor for free.

How to manage your RMDs – and all the other many tax questions that can arise in retirement – can be complicated. Take the time to estimate your retirement taxes before you start collecting pensions, Social Security and taking withdrawals from retirement accounts.

Balancing taxes and retirement income – and figuring out how to minimize taxes in retirement – is a crucial issue. A knowledgeable financial advisor can help you decide how to structure and coordinate these payments over the span of your retirement.

Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three vetted financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you.

Make sure you’re protecting your cash reserves from inflation by securing them in an account that generates a competitive interest rate. Leaving cash in a checking account or low-yield savings account can stifle your purchasing power over time.

Photo credit: ©iStock.com/skynesher

The post Can I Use My RMDs to Transfer Money Into My Roth IRA? appeared first on SmartReads by SmartAsset.

Bitcoin miner Bitdeer is reportedly in discussions with private credit firms to secure $100 million in funding to expand its mining capacity. It is believed that the cryptocurrency miner has engaged a financial adviser to assist with the negotiations. Negotiations Between Bitdeer and Lenders Continue The cryptocurrency mining firm Bitdeer Technologies Group is reportedly seeking […]

Bitcoin miner Bitdeer is reportedly in discussions with private credit firms to secure $100 million in funding to expand its mining capacity. It is believed that the cryptocurrency miner has engaged a financial adviser to assist with the negotiations. Negotiations Between Bitdeer and Lenders Continue The cryptocurrency mining firm Bitdeer Technologies Group is reportedly seeking […]

Source link