A new survey says consumers find e-commerce sites often fail to meet expectations. Experts say that’s because shoppers have become accustomed to how Amazon gets things done to their liking.

Source link

A new survey says consumers find e-commerce sites often fail to meet expectations. Experts say that’s because shoppers have become accustomed to how Amazon gets things done to their liking.

Source link

Retroactive removal of deduction limits is a giveaway to corporations.

Source link

The Magnificent Seven includes some of the most innovative tech-orientated companies on the market. But what if there was a Magnificent Seven for dividend stocks?

Microsoft (NASDAQ: MSFT), Coca-Cola (NYSE: KO), Procter & Gamble (NYSE: PG), Chevron (NYSE: CVX), Home Depot (NYSE: HD), JPMorgan Chase (NYSE: JPM), and United Parcel Service (NYSE: UPS) represent their industries well and are all top dividend stocks you can count on for decades to come. Here’s why they would make my list for the Magnificent Seven of dividend stocks.

Microsoft is the only Magnificent Seven stock that also deserves to be in the Magnificent Seven of dividend stocks. It is the most valuable company in the world. Microsoft only yields 0.7%, but it pays the most dividends of any U.S.-based company.

Microsoft’s low yield is due to its outperforming stock price, not a lack of commitment to dividend raises. Since fiscal 2019, Microsoft has raised its dividend by 9% to 11% every year like clockwork. The dividend has doubled over the last eight years — a faster growth rate than many of the market’s top dividend stocks.

Microsoft is monetizing artificial intelligence and growing its earnings, paving the way for plenty of future dividend raises. If the stock price languishes, the dividend yield will rise to a much more attractive level. However, Microsoft shareholders would surely prefer outsized gains over a higher dividend yield.

Coke uses its dividend as the primary way to reward faithful shareholders. With a yield of 3.2%, Coke allows investors to collect passive income from a tried and true Dividend King with 62 consecutive annual dividend increases.

Coke is a low-growth business, so investors shouldn’t expect outsized gains from the stock. But this is the Magnificent Seven of dividend stocks, not growth stocks. And when it comes to generating passive income, Coke is as reliable as it gets.

Coke’s consistency is the core reason why Warren Buffett’s Berkshire Hathaway has held the stock for over 30 years.

If it were a decision between Coke and a 10-year Treasury, I’d take Coke all day. The 10-year gives investors another percentage point or so in yield, but with no participation in the market. Of course, no stock is as safe as the risk-free rate, but Coke is close. It’s the ideal investment for risk-averse investors or anyone looking to supplement income in retirement.

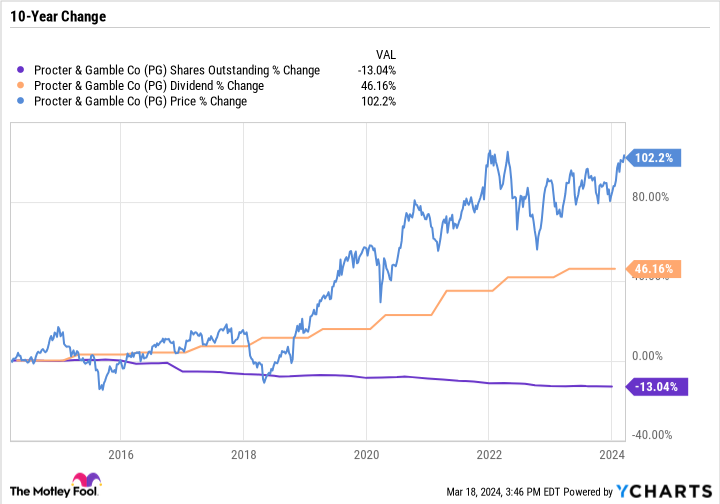

Procter & Gamble has a massive capital return program. It is a great example of a company using dividends and stock repurchases to reward shareholders.

The following chart is one of the prettiest you’ll ever see from a stodgy consumer staple company.

P&G stock has more than doubled over the last decade, the dividend is up over 46%, and P&G has repurchased a considerable amount of stock, reducing its share count by 13%.

P&G may not be the most exciting business, but glitz and glam isn’t the point of this list. When it comes to rewarding shareholders, P&G has done it in many ways and has the business model and brand power needed to continue that streak going forward.

Chevron’s stock buybacks aren’t nearly as consistent as P&G’s. The oil giant tends to buy back more stock during an uptick in the business cycle and pull back on repurchases and capital spending when oil and gas prices fall.

But Chevron’s dividends are as consistent as they come. Chevron has raised its dividend for 37 consecutive years. That means it didn’t cut it during the COVID-19-induced crash, the 2014 and 2015 downturn, or any oil and gas downturn since the late 1980s.

Chevron has the balance sheet, cost profile, and portfolio to continue rewarding shareholders. Its dividend yield of 4.2% makes it one of the higher-yielding reliable stocks out there.

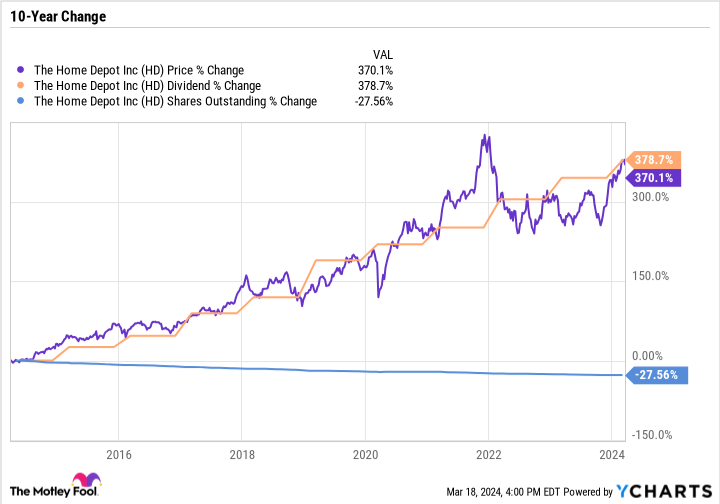

Home Depot has been a perfect dividend stock over the last decade. It has crushed the broader market, and somehow, the dividend has grown at an ever faster rate.

Home Depot has also reduced its share count by over a fourth while expanding the business.

Investors shouldn’t expect this level of growth over the next 10 years, but Home Depot is still a good investment. The company is vulnerable to external factors, such as broader economic cycles, the housing market, the construction industry, and consumer spending. But it is well positioned, and one of the best cyclical dividend stocks to own long term.

Since Nov. 1, JPMorgan is up over 38% — a massive move for such a large, diversified bank. JPMorgan is now worth more than Bank of America, Wells Fargo, and half of Citigroup combined. The Big Four banks have really turned into JPMorgan and the other three.

Banking is a cyclical industry that tends to ebb and flow to the tune of the broader economy. Right now, JPMorgan’s profits are soaring.

Still, what makes the company a good long-term investment, and a worthy addition to the Magnificent Seven of dividend stocks, is that it regularly returns value to its shareholders. Over the last decade, the dividend is up 176%, while the share count is down nearly a fourth.

JPMorgan slashed most of its dividend in 2009 during the fallout of the financial crisis. But since then, it has raised its dividend every year. Today, the dividend is nearly triple what it was pre-cut, and JPMorgan has turned into a quality passive income play.

The recent run-up in the stock price has pushed JPMorgan’s yield down to 2.2%. But the company is at the top of its game and is a good representative of the financials sector in the Magnificent Seven of dividend stocks.

UPS has raised its dividend every year for the last 21 years, except for in 2009, when it kept its dividend flat. The company isn’t the most reliable dividend payer on this list, but it has increasingly used dividends as a key way to reward shareholders.

In 2022, UPS raised its dividend by 49%, a significant increase for its size. Today, UPS yields 4.3%, which is high for an industry-leading industrial company.

UPS is a cyclical business that depends on the strength of the broader economy. Package delivery volumes to businesses are higher during an economic expansion. Similarly, deliveries to consumers are higher when discretionary spending is strong.

Although UPS offers investors a compelling yield, it’s doubtful the company will make as large of raises to its dividend going forward. Still, its current level is quite high, as UPS stock would have to rally about 45% for the yield to fall below 3%.

Microsoft, Coca-Cola, Procter & Gamble, Chevron, Home Depot, JPMorgan Chase, and UPS have track records of dividend raises, solid underlying businesses, future growth prospects, and industry leadership. Many of these companies also reward shareholders with stock repurchases, as well as long-term capital gains for patient investors.

These companies may not always have the highest yields, but they do have earnings growth, which sets the stage for future raises.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for two decades, Motley Fool Stock Advisor, has more than tripled the market.*

They just revealed what they believe are the 10 best stocks for investors to buy right now… and Microsoft made the list — but there are 9 other stocks you may be overlooking.

*Stock Advisor returns as of March 21, 2024

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Wells Fargo is an advertising partner of The Ascent, a Motley Fool company. JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. Citigroup is an advertising partner of The Ascent, a Motley Fool company. Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bank of America, Berkshire Hathaway, Chevron, Home Depot, JPMorgan Chase, and Microsoft. The Motley Fool recommends United Parcel Service and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

If There Was a “Magnificent Seven” for Dividend Stocks, These Would Be My Top Picks was originally published by The Motley Fool

There are still a number of companies in the private market that are potential IPOs — but underwriters will likely take a cautious approach this year.

Source link

This week’s non-fungible token (NFT) sales have taken another nosedive, intensifying the downtrend that began with a 16.55% decline from March 9 to March 16, 2024. The last seven days have witnessed an even steeper drop, with NFT sales plummeting by 18.57%. Cryptopunk #7,804 Shines in a Week of Falling NFT Sales In line with […]

This week’s non-fungible token (NFT) sales have taken another nosedive, intensifying the downtrend that began with a 16.55% decline from March 9 to March 16, 2024. The last seven days have witnessed an even steeper drop, with NFT sales plummeting by 18.57%. Cryptopunk #7,804 Shines in a Week of Falling NFT Sales In line with […]

Source link

As of March 22, the bitcoin holdings of Grayscale’s Bitcoin Trust (GBTC) have diminished by 27,917.37 compared to its status three days prior, now amounting to 350,252 bitcoin valued at approximately $22.2 billion. Since evolving into an exchange-traded fund (ETF) listed on public exchanges, GBTC has shed billions in bitcoin over the preceding 71 days. […]

As of March 22, the bitcoin holdings of Grayscale’s Bitcoin Trust (GBTC) have diminished by 27,917.37 compared to its status three days prior, now amounting to 350,252 bitcoin valued at approximately $22.2 billion. Since evolving into an exchange-traded fund (ETF) listed on public exchanges, GBTC has shed billions in bitcoin over the preceding 71 days. […]

Source link

A London resident reportedly caught with bitcoins worth over $4.3 billion has been convicted for entering into a money laundering arrangement. The woman specialized in converting digital assets into physical assets, such as multimillion-dollar houses and jewelry. Converting Bitcoin to Physical Assets A British woman, found in possession of bitcoins currently valued at over $4.3 […]

A London resident reportedly caught with bitcoins worth over $4.3 billion has been convicted for entering into a money laundering arrangement. The woman specialized in converting digital assets into physical assets, such as multimillion-dollar houses and jewelry. Converting Bitcoin to Physical Assets A British woman, found in possession of bitcoins currently valued at over $4.3 […]

Source link

You should expect to need savings on top of Social Security once your retirement kicks off. But you have options when it comes to choosing a home for your nest egg. Those might include a traditional IRA, a Roth IRA, or a traditional 401(k) plan offered by your employer.

These days, though, a growing number of 401(k) plans are including a Roth savings feature. And that’s an option you may be tempted to take advantage of — especially this year because Roth 401(k)s are no longer forcing savers to take required minimum distributions.

Image source: Getty Images.

While a Roth 401(k) might seem like a great home for your retirement savings, there are certain pitfalls you might encounter if you choose one of these accounts. Here are three reasons you may not want a Roth 401(k) to serve as your nest egg’s home.

The nice thing about saving for retirement in an IRA is that you get a world of investment options to choose from. Want to load up on individual stocks you research yourself? Go for it.

With a 401(k), you’re generally limited to several different funds. Within that realm, some funds may come with lower expense ratios than others. Either way, you’ll still be limited as to how you invest your retirement savings, so an IRA may be a better bet.

If you want the benefit of tax-free investment gains and withdrawals, you can always choose the Roth version of an IRA. Even if your income is too high for a Roth, there’s always the conversion option.

The investments you choose for your 401(k) could leave you paying a lot of money in fees. But even if you opt for low-cost investments, like index funds, you might still get hit with fees associated with administering your 401(k).

Those fees, like investment-specific fees, could eat away at your returns over time. With an IRA, your fees may be lower.

Contributing to a 401(k) plan makes sense when there are employer-matching dollars to take advantage of. Data from Vanguard finds that within its platform, 95% of retirement plans come with some type of matching contribution on the part of a sponsoring employer.

But if you’re in that unlucky 5%, it may not be worth it to contribute to a Roth 401(k) if the above circumstances apply to you. If there’s no workplace match, you may want to max out an IRA first. Then, if you wish to contribute beyond that point, you can divert extra funds to a Roth 401(k).

You may also want to keep some of your retirement savings outside a tax-advantaged account. That way, your money will be completely unrestricted.

Roth 401(k)s give you many of the benefits of Roth IRAs but with higher contribution limits. As you can see, however, there are drawbacks to making a Roth 401(k) the home for your retirement savings, so you may want to consider a different solution.

The U.S. dollar has strengthened its grip on the global financial system since Russia invaded Ukraine two years ago, defying expectations of “de-dollarization.”

Source link

Bitcoin (BTC 1.68%) has stolen the cryptocurrency spotlight. Its price has soared 125% over the past year due in large part to enthusiasm surrounding spot Bitcoin exchange-traded funds (ETFs). However, Ethereum (ETH 1.51%) returned about 80% over the same period, and at least one Wall Street analyst sees bigger gains on the horizon.

Geoff Kendrick, head of digital assets research at Standard Chartered Bank, believes smart contract technology and spot Ethereum ETFs (if approved) could send the cryptocurrency to $14,000 by 2025. That implies about 310% upside from its current price of $3,400, an enticing figure given the short timeline.

Is Ethereum worth buying?

The Ethereum blockchain is programmable, meaning that developers can build self-executing programs called smart contracts on the platform. That technology is the foundation of tokenization and other decentralized finance (DeFi) applications, and the many utilities of smart contracts could increase demand for Ethereum in the coming years.

To elaborate, tokenization is the process whereby ownership rights to digital and physical assets are represented as tokens on a blockchain, which itself serves as a digital ledger. Benefits include improved audit transparency because details are automatically and immutably recorded on the blockchain when tokens are transacted. Tokenization could also improve asset liquidity by enabling fractional ownership of assets like real estate, artwork, and other collectibles.

More broadly, DeFi platforms could expand access to financial services and reduce the underlying costs by allowing users to borrow, invest, and earn interest on money without intermediaries like banks. That would be particularly valuable in underbanked regions of the world.

Ethereum is the blockchain best positioned to benefit if and when smart contract technology sees greater adoption. I say that because users clearly have a preference for Ethereum. It accounts for 56% of the funds held in DeFi applications, meaning it holds more market share than all the other blockchains combined, according to DeFi Llama. Consequently, demand for the cryptocurrency could soar if DeFi goes mainstream, simply because users must pay transaction fees to interact with products on the blockchain.

Spot Ethereum ETFs are investment products that (if approved) would provide direct exposure to Ethereum while eliminating the hassle of cryptocurrency exchanges and blockchain wallets. Those funds would greatly reduce friction for individual and institutional investors, which could boost demand for the cryptocurrency and send its price higher.

Indeed, recently approved spot Bitcoin ETFs illustrate how much demand such investment products could unlock. Specifically, the spot Bitcoin ETFs issued by BlackRock and Fidelity saw greater cash inflows during their first month on the market than any other ETFs launched in the past 30 years, according to Bloomberg Intelligence.

With that in mind, seven issuers have submitted applications for spot Ethereum ETFs, including BlackRock and Fidelity. The Securities and Exchange Commission (SEC) must reach a decision by May 23, but investors should not take approval for granted. In fact, James Seyffart at Bloomberg expects the SEC to deny the applications this time around. His assessment is based on the fact that regulators have not engaged with potential issuers to the same degree that they did with spot Bitcoin ETF applicants before approval.

Smart contract technology is intriguing, and the potential benefits of tokenization and other DeFi use cases are undeniable. However, widespread adoption of Ethereum-based smart contracts is probably a ways off, even in the best-case scenario.

Additionally, I doubt spot Ethereum ETFs will win regulatory approval in May. Fortune recently reported that the SEC is investigating the Ethereum Foundation, which oversees the crypto, as part of its push to classify many cryptocurrencies as securities. The outcome could shake the market in unpredictable ways, and it would be unlikely that the SEC would approve spot Ethereum ETFs while the investigation is ongoing.

For those reasons, I would avoid Ethereum right now. That does not mean the cryptocurrency will lose value. In fact, Geoff Kendrick may be spot-on with his target of $14,000. However, I see more compelling investment opportunities in Bitcoin and the stock market.

Trevor Jennewine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bitcoin and Ethereum. The Motley Fool has a disclosure policy.