Surging Treasury yields and rising oil prices are calling the tune across markets right now.

Source link

Surging Treasury yields and rising oil prices are calling the tune across markets right now.

Source link

BurnBot RX burns unwanted vegetation without emitting plumes of smoke.

Lora Kolodny for CNBC

Last year’s record heat wave worsened drought and dry conditions across the globe, a particularly calamitous situation for California, which has seen 13 of the state’s 20 most destructive wildfires in history break out since 2017.

In South San Francisco, a small startup is working on a high-tech approach to wildfire prevention.

Anukool Lakhina and Waleed “Lee” Haddad founded BurnBot in 2022 to develop robotics and remote-controlled vehicles that can munch up and burn away invasive plants or other dry vegetation that can fuel fires if left fallow.

BurnBot has just raised a $20 million funding round led by climate-focused ReGen Ventures, for expansion, hiring, and to develop new machines that can traverse steeper hills and get into tighter spaces.

Before BurnBot, firefighters and land owners had to use expensive, time-consuming and more dangerous options like grazing away the vegetation (typically with goats), burning it, applying herbicides or removing vegetation mechanically with a mix of equipment and manual labor.

“The sort of traditional way to do a prescribed burn is with drip torches, and that requires a large number of people,” said Lakhina, BurnBot’s CEO. “A drip torch is like a diesel watering can. You go around, you drop diesel, then ignite it.”

Burnbot’s current model, the RX, is a remote-operated vehicle that looks a cross between an oversized Zamboni and a steel cooking range with a set of fire extinguishers strapped to its back. Like other agricultural and construction equipment, the RX rolls forward on tank-like tracks and wheels, which enable it to maneuver through rough fields.

Within the chambers of the RX are several rows of torches that emit blue flames, and adjust the heat levels precisely to zap away unwanted vegetation or other fuels on the ground below. The chambers of the BurnBot RX also trap and torch away the smoke that comes from burning vegetation, so it doesn’t pollute the air in surrounding communities. When the torching is done, the RX sprays water repeatedly to extinguish any remaining embers.

Inside the chambers of the BurnBot RX torches are lit to do the work of a prescribed burn.

Lora Kolodny for CNBC

Lakhina said BurnBot’s systems can be put to use where traditional controlled burns won’t work. For example, drip torch burns produce a good deal of smoke, which is conductive enough it would interfere with the proper functioning of power lines or high-voltage equipment. BurnBot’s machines can be used even under power lines.

The company is aiming to make every person who works in fire prevention 10 times more effective than they were with old methods, Lakhina said.

Haddad, BurnBot’s chief technology officer, noted that land isn’t always ready to “receive fire” in a prescribed burn. So the company has programmed equipment, which it procures from another supplier, to roll ahead of the RX to crunch up the vegetation in an area of concern before it’s ready for torching.

BurnBot plans to conduct a prescribed burn this Friday in San Diego, a project for CalTrans, the state’s transportation agency. It also plans for another burn for Pacific Gas & Electric, the state’s major utility, in June.

PG&E spends upward of $1 billion on “vegetation management” each year. Kevin Johnson, who leads the company’s Wildfire Resilience Partnerships, said PG&E is always “looking for opportunities to do this work safer, faster, cheaper and to be more environmentally friendly.”

BurnBot has already completed one demonstration of its controlled burn machine underneath PG&E transmission lines.

Brice Muenzer, a battalion chief with CalFire in Monterey, California, said massive fires in the state and throughout the U.S. over the past decade have been partly caused and certainly exacerbated by overzealous elimination of smaller fires, including ritual fires from indigenous communities.

“We removed fire from the ecosystem for the last 150 years and are living through that reality now,” the chief said.

CalFire has worked with BurnBot personnel, machines and additional drones overhead, to create what’s known as a control line in the field in at least one location. Muenzer says the group hopes to do more with the startup.

Creating a control line, or blacklining the land, involves firefighters strategically burning areas when the weather is calm and where flames can be controlled to create scars that will block other fires from jumping in and reaching areas with lots of new material to burn.

BurnBot cofounders (L-R) CTO Waleed “Lee” Haddad and CEO Anukool Lakhina

Lora Kolodny for CNBC

BurnBot aims to eventually expand its operations beyond California, with offices and fleets of its machines wherever vegetation management is needed and wildfire risk is highest.

“There are 50 million acres that the U.S. Forest Service has said need treatment every year and that’s just forest land,” said Lakhina. In the U.S. there are 237 million acres that need treatment overall. And grazing can cost $1,000 an acre.”

Childrens’ health is at stake along with property and healthy forests, Lakhina added. According to the Harvard School of Public Health, wildfire smoke can be more toxic than air pollution from other sources, leading to more emergency room visits, especially for children who are exposed.

Because BurnBot offers greater precision than grazing, herbicides and mechanical removal, its systems should prove ecologically more beneficial as well, Haddad said. The BurnBot RX is able to help prevent the spread of seeds from invasive species, for example, without causing any of those species to develop resistance to an herbicide.

ReGen was joined in BurnBot’s funding round by investors including AmFam Ventures, which is the venture arm of an insurance company, Toyota Ventures, and earlier backers including robotics fund Pathbreaker, Convective Capital and Chris Sacca’s Lowercarbon Capital.

WATCH: Revisiting Maui six months after devastating wildfires

In Florida, homeowners are grappling with insurance rates that are nearly three times the national average, a situation that has prompted concerns at both the state and federal levels.

The average cost of home insurance in the Sunshine State has soared to approximately $6,000 annually, significantly outpacing the national average of about $1,700. This surge in premiums is attributed to a 102% increase over the past three years, according to the Insurance Information Institute.

Gov. Ron DeSantis has been particularly vocal about the challenges plaguing Florida’s insurance market, highlighting the state’s reliance on Citizens Property Insurance Corp. as a key issue. Established by the Florida legislature as a not-for-profit insurer of last resort, Citizens has come under scrutiny for its financial solvency. DeSantis’s assertion that the corporation is “not solvent” raises alarms over its capacity to manage claims after major storms, potentially necessitating a government bailout.

The insurance crisis is multidimensional, with Florida’s vulnerability to hurricanes and severe weather playing a significant role. Regulatory and financial hurdles within the state’s insurance industry exacerbate the problem, leaving homeowners facing exorbitant premiums and, in some cases, the inability to secure insurance coverage. The situation has caught the attention of U.S. Sen. Sheldon Whitehouse, who has sought detailed financial information from Citizens in light of DeSantis’s remarks. Whitehouse’s concerns underscore the potential implications for federal resources and the national economy.

Efforts to mitigate the crisis have included legislative attempts to reform the insurance market. These efforts aim to stabilize premiums and ensure the solvency of insurers like Citizens. However, the impact of these measures remains uncertain as homeowners continue to confront the challenges of affordability and availability of insurance coverage.

Citizens CEO Tim Cerio has countered claims of financial instability, asserting the corporation’s strong financial condition. He clarified that, should Citizens deplete its resources, Florida law mandates levying a special surcharge on Floridians rather than seeking federal financial assistance. This approach, however, means that a hurricane impacting one part of Florida could lead to increased insurance costs for homeowners throughout the state, according to Jake Holehouse, president of HH Insurance.

Adding to the concern, AccuWeather’s forecast for an “explosive 2024 hurricane season” intensifies the urgency to address Florida’s insurance market challenges. With predictions of an extremely active season, fueled by factors such as the potential development of La Niña and record-warm sea surface temperatures, the stability and preparedness of Florida’s insurance indiustry are more critical than ever.

As Florida faces the prospect of an unprecedented hurricane season, the dialogue between state officials, insurance industry leaders and federal representatives underscores the complex interplay of environmental, financial and regulatory factors driving the state’s insurance crisis. The path forward requires a concerted effort to devise sustainable solutions that protect homeowners while ensuring the financial health of insurers like Citizens Property Insurance Corp.

“ACTIVE INVESTORS’ SECRET WEAPON” Supercharge Your Stock Market Game with the #1 “news & everything else” trading tool: Benzinga Pro – Click here to start Your 14-Day Trial Now!

Get the latest stock analysis from Benzinga?

This article Florida Governor Ron Desantis’ Raises Alarm By Calling Citizens Insurance ‘Not-Solvent’ As An ‘Explosive’ Hurricane Season Is Predicted originally appeared on Benzinga.com

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Several different strategies will get the job done, but there’s one common element among all these approaches.

Got a decent amount of money right now that you’d like to turn into a seven-figure stash by the time you retire? Well, good news… it’s probably possible. The key to doing so is just a combination of how much time you’ve got and what you do with that money in the meantime. If you’ve got enough of both, it’s possible for you to turn $100,000 into $1 million. Here are a few ways you can make it happen.

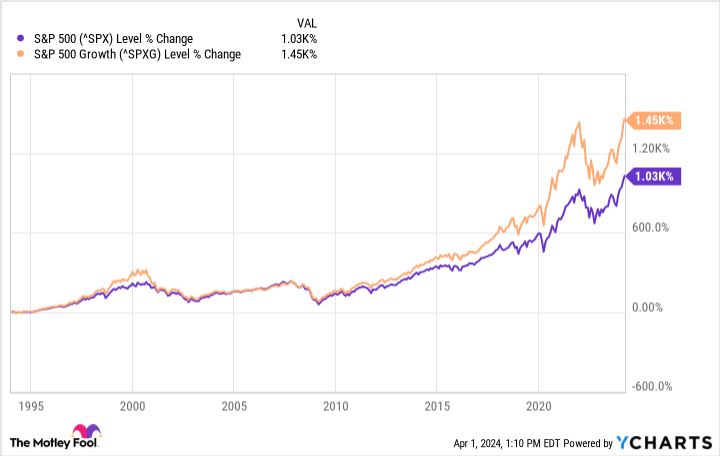

Many new investors start their journeys by buying some of the market’s most popular growth stocks. And understandably so. These tickers (by definition) are expected to continue growing in value.

They’ve also got a collective track record to justify this interest. Over the course of the past 30 years the S&P 500 Growth index has outgrown the S&P 500 (^GSPC -0.72%) by nearly half as much more than the market’s most-used benchmark gained during that period.

Sticking with growth stocks for the entirety of this span wouldn’t have been easy for investors, however.

See, while the S&P 500 feels volatile, it’s not nearly as volatile as the S&P 500 Growth Index and its underlying stocks are. They’re so volatile, in fact, that at times it would have been tough to stick with many of these names. And if you can’t stay in stocks when things get ugly, you risk missing out on most of their upside. That’s because stocks’ biggest gains often come immediately after their biggest sell-offs, and right at the very beginning of new bull markets… when many investors still don’t believe the bear market is over, and are therefore on the sidelines. Big mistake.

Growth stocks aren’t the only way of producing big investment gains, however. Boring old dividend stocks can do the same.

This may seem counterintuitive on the surface. Dividend stocks tend to be shares of slower-moving, lower-growth companies, after all.

But, don’t dismiss the upside of slow and steady value-creation in the form of cash — particularly when the companies in question are in the proven habit of raising their dividend payouts. These quality stocks ultimately tend to outperform their non-dividend-paying peers. Mutual fund company Hartford did some data-mining on the matter, determining that in the 40-year span from 1973 to 2023, the more willing and able a company was to pay a dividend, the better its stock performed. These stocks also tend to be less volatile (lower beta), making them even easier to hang onto when things become turbulent for the market.

| Dividend Profile | Average Annual Returns | Beta |

|---|---|---|

| Dividend growers/initiators | 10.2% | 0.89 |

| Dividend payers | 9.2% | 0.94 |

| No change in dividends | 6.7% | 1.02 |

| Dividend cutters/eliminators | (0.6%) | 1.22 |

| Dividend non-payers | 4.3% | 1.18 |

| Equal-weight S&P 500 index | 7.7% | 1.00 |

Data source: Hartford Funds and Ned Davis Research

For reference, reinvesting the dividends paid by the highest-quality dividend stocks returning (net) on the order of an average of 9% to 10% per year would grow $100,000 into $1 million in roughly 25 years, a result that’s in line with growth stocks’ historic long-term returns.

The only catch is, you really do have to reinvest those dividends into more shares of those dividend-paying names to produce these kinds of results. Hartford adds that over the past several decades, dividends accounted for around one-third of the S&P 500’s net gains, and since 1960, reinvested dividends drove about 85% of the index’s cumulative returns. Just know that most of these net gains will come closer to the end of any time frame than to the beginning of it.

But what if you think a dividend-oriented strategy is too far to the other extreme? There’s a hybrid approach that’s both simpler and zero-maintenance. Why not just own the market as a whole through an index-based instrument like the SPDR S&P 500 ETF Trust (SPY -0.64%), which merely mirrors the S&P 500’s performance (for better and for worse)?

Boring? Sure… a little. This approach, however, avoids many of the inherent problems of being an investor these days.

Chief among these sidestepped problems is that if you buy and hold an index fund, you don’t experience the risky temptation of trying to perfectly time a trade’s entry or exit. The idea is to simply plug you into the overall market’s long-term performance, which is an average gain of about 10% per year.

Yes, some years are better while others are worse. In that you know you can’t know when these near-term ebbs and flows are going to take shape though, you don’t even bother trying. You simply let time work its magic over the course of two to three decades, smoothing out all the market’s highs and lows that surface in the interim en route to growing $100,000 into $1 million.

Another upside: This strategy also allows you to avoid making constant check-ins on your stocks or the market’s current condition. Such check-ins often spur impromptu buying and selling you may not really want to do, but feel like you have to at the time just because you’re already looking.

There’s a fourth option, of course. That is, utilize all three strategies. Start with a foundational index fund, then add dividend stocks (don’t forget to turn on the DRIPs), and then pick up some growth stocks you have good reason to believe will still be thriving 10, 20, and even 30 years down the road. This approach provides you with balanced exposure to the key upsides of all three strategies. You’ll also find that this blended approach leaves your entire portfolio’s value relatively steady from one month and even one year to the next.

Just notice the common thread in all three strategies. That’s time — in all three scenarios above, the path to turning a small six-figure sum into a $1 million retirement nest egg took 25 to 30 years, depending on the market environment at the beginning and then at the end of the time frame. Giving yourself enough time to achieve the goal is far more important than whatever stock-picking strategy you use. Conversely, not giving yourself enough time to meet your investment goal is the biggest investment risk you can take.

A close-second risk: Not doing anything constructive with your money once you’ve worked so hard to save up a meaningful amount of it to put to work for your future.

An index tracking the strength of the U.S. dollar against a basket of rivals touched its highest level since mid-November on Tuesday, adding to the headwinds facing U.S. stocks.

Source link

The market is full of top-tier stocks to buy.

Although the market continues to hit all-time highs, plenty of stocks are worth buying right now. While some may be overpriced, plenty look like good deals.

If you’ve got $3,000 lying around, buying this trio is a wise idea.

Meta Platforms (META 1.23%) is probably known better by its previous name, Facebook. Meta changed its name to signal a shift to focus on the metaverse, but this also included augmented and virtual reality products that are starting to generate some interest thanks to the rise of artificial intelligence (AI). For example, Meta is working on its Ego AI product, which, through the use of glasses, can teach users activities like cooking or playing tennis.

But this is just a product that’s still years away. Fortunately, Meta’s primary business is doing great.

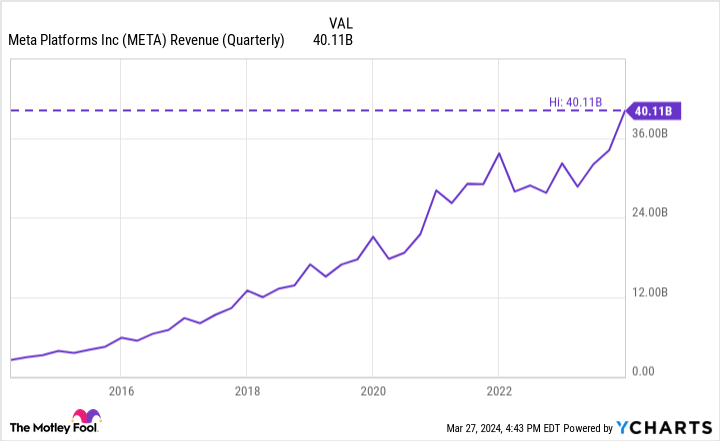

Most of Meta’s revenue and profits come from advertising on its social media platforms. While this industry wasn’t successful in late 2022 and early 2023, it came roaring back, and Meta is doing as well as ever. In Q4, revenue was up 25% to $40.1 billion, a new all-time high. Its profits also skyrocketed, up 20% to $14 billion.

META Revenue (Quarterly) data by YCharts

Management also gave bullish commentary for 2024, which should excite investors because it shows Meta isn’t done growing. With Meta’s stock priced around 25 times forward earnings, it’s a stock that investors should be willing to buy now.

Adobe (ADBE -0.57%) is the industry leader in digital media creation software. However, with the rise of AI-generated images, many questioned if Adobe’s products were necessary. This came to a focus during Adobe’s first quarter of 2024 (ending March 1), as Adobe’s Firefly product has to compete with many free programs.

However, Adobe saw strong demand, with companies like Accenture, Starbucks, and IBM adopting the software add-on. Still, investors were worried about Q2 growth projections, as they only indicated 9.4% growth at the midpoint. This caused investors to panic, and the stock is down over 11% since the company reported earnings.

This seems like an overreaction and allows investors to scoop up Adobe shares much cheaper than they previously could. Wall Street is certainly convinced that Adobe is undervalued, as the average analyst has a one-year price target of $620 on the stock — a 24% increase from its current levels. With Adobe trading for 28 times forward earnings, it seems like another no-brainer buy.

UiPath (PATH -2.79%) is a leader in robotic process automation (RPA). Its software helps clients automate repetitive tasks, freeing up employees to do work that requires original thinking. It also utilizes the power of AI to help increase the number of tasks it can automate, a key factor in today’s environment.

Unlike most stocks, UiPath has had a down 2024, losing around 25% of its value. This has nothing to do with its business, as its fourth quarter of fiscal year 2024 (ending Jan. 31) was quite positive. Its annual recurring revenue (ARR) rose 22% to $1.46 billion and it posted an operating profit of 4%.

It also wasn’t overvalued, as it trades around 10.5 times sales — pretty cheap compared to its peers with similar growth.

As a result, I think UiPath is a great stock to buy right now, as its stock hasn’t benefited from the AI trend that many others have. This means it’s only a matter of time before UiPath gets the recognition it deserves and becomes a more highly valued stock.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Adobe, Meta Platforms, and UiPath. The Motley Fool has positions in and recommends Accenture Plc, Adobe, Meta Platforms, Starbucks, and UiPath. The Motley Fool recommends International Business Machines and recommends the following options: long January 2025 $290 calls on Accenture Plc and short January 2025 $310 calls on Accenture Plc. The Motley Fool has a disclosure policy.

Every day the streaming landscape is looking more and more like the beast it sought to slay — cable.

Looming talks of platform bundles come as major streamers push ad-supported plans, limit password sharing and lean into live sports coverage. The goal of exponential subscriber growth, fueled by pandemic lockdowns, has shifted. Wall Street wants profits.

The key to that may be depth, not breadth.

Last year many streaming services began shrinking their once-robust content libraries in order to pay smaller licensing fees. (Streamers must pay to license even their own film and TV shows, like when NBC forked over $500 million to buy back the rights to “The Office,” an NBC show, in 2019.)

In the face of profit pressures and growing competition for viewers, streamers have taken to removing content to avoid the residual payments and licensing fees. That dynamic has split the major streaming companies into two camps: buyers and sellers.

On one side is Netflix, Amazon and Apple — companies that agnostically license content from other studios to bolster their streaming libraries. Then there’s Disney, Universal, Warner Bros. Discovery and Paramount, which rely on decades worth of legacy content to build out their own services and also generate capital by auctioning it off to the highest bidder.

“The brands that are acquiring those titles are thinking about how to operate more cost effectively by not creating things but by buying licenses,” said Stephanie Fried, chief marketing officer at Fandom, the world’s largest platform for entertainment fans.

The sellers get cash, while the buyers get content that has a track record of reliability and consumer value. That’s especially important for Netflix, which is a newer entrant in Hollywood, and as a result has fewer long-running, binge-able series. Just look at how NBC’s “Suits” took off on the service last year.

Notably, Netflix is already profitable. Amazon and Apple have said they see streaming as additive to their overall businesses, not core to them. The rest of the major streaming players are still working toward profitability.

Narrowing content libraries naturally means a need for differentiation.

The initial bloom of new platforms over the last 15 years saw most entrants take an “everything to everyone” approach, attempting to become the only streaming service you’d need. That meant, besides the user interface, most streaming services began to look alike over time.

Fried said this lack of distinction could ultimately be a negative as the landscape gets stretched thin. She suggested streamers look at the type of content their subscribers are consuming and pick up complementary shows and films that have not yet been licensed.

That model has worked well for smaller streaming services like BritBox, which has a wide swath of British dramas, mysteries and period pieces; and Shudder, which centers on the horror genre.

Netflix, for example, which has seen success from nostalgic sitcoms like “Friends” and “The Office,” could add on similar shows like Nickelodeon and Paramount’s “Fairly Odd Parents” and “Hey Arnold,” Disney’s “Boy Meets World” and “American Dad” as well as the NBC-owned “Saved by the Bell,” according to data from Fandom.

Fandom, which hosts more than 50 million wiki pages on entertainment properties across television, film, gaming, comics and more, has a “really good sense of the overlap between all of these walled gardens,” Fried said.

Original shows on Apple TV+ like “Severance,” “Defending Jacob,” “Home Before Dark” and “Servant” have enthralled and spooked viewers. That type of dark investigative thriller centered on character-driven narrative would pair well with the likes of Warner Bros. Discovery’s “The Leftovers,” Netflix’s “Haunting of Hill House” and the Disney-owned early seasons of “Twin Peaks,” Fried said.

Over at Amazon Prime Video, subscribers have opted for action-packed shows like “The Boys,” “Jack Ryan,” “Reacher” and “Invincible” as well as high fantasy series “The Rings of Power” and “Wheel of Time.” Fandom’s data suggests shows like Netflix’s “Jupiter’s Legacy,” Warner Bros. Discovery’s “My Adventures with Superman,” Paramount’s “Mayor of Kingstown” and Disney’s “The Americans” would further engage the streamer’s audience.

Similarly, Fandom’s data could tell streamers what types of shows they should invest in when looking to create new product.

On Disney+, family entertainment is everything. Fried noted that Disney’s best opportunity to differentiate itself is to double down on being the leader in kids and family-friendly content. Disney-owned Hulu, meanwhile, has seen success with “feel good” 30-minute sitcoms and prestige dramas, Fandom’s data shows. NBC’s “Parks and Recreation” and the ’90s version of “Fresh Prince of Bel-Air” alongside Paramount’s “The Nanny” could serve Hulu audiences well, according to Fandom, along with Netflix’s “Queen’s Gambit” and “Black Mirror” and the BBC show “Orphan Black.”

Universal’s Peacock is all about crime dramas and medical series, and Paramount+ is the place for viewers to get their sci-fi fix. At Warner Bros.’ Max, high-quality prestige shows have long been the bread and butter of HBO, and high fantasy entrants like “Game of Thrones” and “The Last of Us” have enticed younger audiences.

Doing well and doubling down in certain segments means keeping your viewers for longer, Fried said: “When they’re thinking about cutting your service it’s like, ‘I can’t, because they have all of my X type shows.”

Disclosure: Peacock is the streaming service of NBCUniversal, the parent company of CNBC.

For well over a century, no asset class has come close to rivaling the annualized returns stocks have delivered for investors. With thousands of tradable securities, including exchange-traded funds (ETFs), Wall Street offers investors of all walks and risk tolerances a path to grow their wealth.

But among these seemingly countless pathways to riches is one that’s undeniably toward the top of the pack: buying and holding high-quality dividend stocks.

Last year, Hartford Funds released a lengthy report (“The Power of Dividends: Past, Present, and Future”) that examined the multiple ways dividend stocks have outperformed non-payers over extended periods.

Image source: Getty Images.

In a collaboration with Ned Davis Research, Hartford Funds noted that dividend-paying companies produced an average annual return of 9.18% spanning 50 years (1973-2022), and did so while being 6% less volatile than the benchmark S&P 500. By comparison, the average annual return from non-payers was less than half that of dividend stocks (3.95%) over a half-century, and the non-payers were 18% more volatile than the broad-based S&P 500.

Companies that pay a consistent dividend to their shareholders are usually profitable on a recurring basis and time-tested. In short, they’re just the type of businesses we’d expect to increase their valuations over the long term.

However, income seekers don’t have to settle for paltry yields when seeking out dividend stocks to buy. Although studies have shown that yield and risk have a tendency to go hand-in-hand — i.e., high-yield stocks come with added risks — proper vetting can reveal some high-octane income gems.

As we leap into April, three magnificent ultra-high-yield stocks, with an average yield of 9.02%, stand out as screaming buys.

The first amazing dividend stock with a premium yield that you can confidently add to your portfolio in April is none other than pharmaceutical juggernaut Pfizer (PFE -0.59%).

Pfizer stock recently hit a decade-low, with the overhang from the COVID-19 pandemic acting as a cement weight around its proverbial ankles. As one of the few companies to successfully develop a COVID-19 vaccine (Comirnaty), as well as an oral tablet designed to lessen the severity of COVID-19 (Paxlovid), Pfizer’s sales soared during the early stages of the pandemic. But with the worst now behind us, combined sales of these drugs have tumbled from over $56 billion in 2022 to an estimated $8 billion this year.

While this seesaw in sales has crimped the necks of Wall Street analysts, some investors have clearly lost sight that Pfizer is far better off now, from a financial standpoint, than it was prior to the pandemic. Not only is it generating an extra $8 billion in annual sales from its core COVID-19 lineup, but the company’s vast non-COVID portfolio of therapeutics has continued to grow on an organic basis.

For example, if sales for Comirnaty and Paxlovid are stripped out, operating revenue for all of Pfizer’s other novel drugs rose by 7% in 2023. The company’s guidance calls for another 3% to 5% operating sales growth, sans Comirnaty and Paxlovid, in 2024.

Something else to note is that Pfizer’s bottom line will take an approximate $0.40-per-share hit this year following the acquisition of cancer-drug developer Seagen. This is a temporary speed bump that will give way to cost-savings and a vastly superior cancer-drug pipeline and product portfolio beginning in 2025.

The highly defensive nature of the healthcare sector is another reason income investors can trust Pfizer. No matter what’s happening with the stock market or U.S. economy, people still need prescription medicines. This tends to lead to highly predictable operating cash flow in any economic climate.

Shares of Pfizer can be scooped up right now for just 11 times forward-year earnings, which is an attractive valuation for a company that’ll pay you more than 6% annually to be patient.

A second magnificent ultra-high-yield dividend stock that’s begging to be bought in April is cannabis-focused real estate investment trust (REIT) Innovative Industrial Properties (IIPR -2.40%). “IIP,” as the company is more commonly known, has increased its quarterly payout by 1,113% since issuing its first distribution in July 2017.

IIP has contended with two very clear headwinds. First, marijuana stocks lost their buzz in early 2021 after it became clear that the Biden administration and a Democrat-led Congress wouldn’t be passing much in the way of cannabis-reform measures.

The other issue is that a small number of IIP’s tenants became delinquent on their rent early in 2023. All REITs eventually deal with delinquencies, and it’s how they respond to these challenges that dictates their outlook. IIP’s management team was able to rework some of its master-lease agreements, as well as sell a couple of properties, to move its rent collection rate back to 100% by February 2024.

One of the factors that makes Innovative Industrial Properties such a smart buy for REIT investors is that a vast majority (95.8%) of its asset portfolio of more than 100 properties is triple-net leased. A triple-net lease requires the tenant to cover all expenses pertaining to the property, including utilities, maintenance, property taxes, and insurance premiums. While rental rates are lower for triple-net leases, it also absolves IIP from dealing with surprise expenses.

Interestingly enough, IIP is one of the few companies that’s actually benefiting from the congressional stalemate on cannabis reform. Since most multi-state operators (MSOs) have limited access to basic financial services, IIP has leaned on sale-leaseback agreements as a solution. IIP purchases medical marijuana cultivation and/or processing assets from MSOs using cash and immediately leases the property back to the seller. This nets IIP a long-term tenant and yields highly predictable cash flow.

Given the long-term growth potential of legalized cannabis in the U.S., Innovative Industrial Properties’ forward price-to-earnings (P/E) ratio of less than 18, and its 7% yield, are both enticing.

Image source: Getty Images.

The third magnificent ultra-high-yield dividend stock that makes for a screaming buy in April is coal company Alliance Resource Partners (ARLP 0.35%). Yes, you did read that correctly — I said, “coal company.”

Entering the decade, coal stocks were left for dead. Historically low interest rates and a strong U.S. economy were expected to fuel global investment in wind and solar solutions. However, the arrival of the COVID-19 pandemic changed those plans.

During the pandemic, global energy companies were forced to significantly reduce their capital spending due to a historic demand cliff for energy commodities. In the wake of the pandemic, domestic interest rates have soared and global crude oil supply has remained tight. It’s coal companies like Alliance Resource Partners that have stepped up to fill the energy-demand void.

Although Alliance Resource Partners has enjoyed selling its coal at a historically high per-ton price, much of the company’s success can be attributed to its management team. In particular, Alliance Resource has historically booked production up to four years in advance. Locking in volume and price commitments years in advance provides the transparency to cash flow needed to make confidently make acquisitions, expand production, and pay a hefty distribution without adversely impacting profits.

To add to the above, Alliance Resource Partners’ management team has always slow-stepped its production expansion. Doing so has ensured that the company’s debt level remains manageable, which hasn’t always been the case for its peers.

Lastly, the company has diversified its revenue channel by acquiring 67,700 acres’ worth of royalty oil and gas interests. If the spot price of energy commodities remains high, earnings before interest, taxes, depreciation, and amortization (EBITDA) should push higher from this royalty segment.

A forward P/E ratio of around 5, coupled with a 14% yield, makes Alliance Resource Partners one of the cheapest supercharged dividend stocks on the planet.

Over the last 30 years, no next-big-thing trend or innovation has come close to rivaling the advent of the internet. However, artificial intelligence (AI) has the potential to do for businesses in this generation what the internet did for corporate America three decades ago.

By the turn of the decade, analysts at PwC foresee AI, which relies on software and systems in place of human oversight, increasing global gross domestic product by $15.7 trillion. No company has more directly benefited from the AI revolution than semiconductor stock Nvidia (NASDAQ: NVDA).

Over the span of 15 months, Nvidia’s valuation has soared by $1.9 trillion to $2.26 trillion, which ranks behind only Microsoft and Apple among publicly traded companies in the U.S.

Nvidia’s outperformance is a reflection of the overwhelming demand for its high-powered A100 and H100 graphics processing units (GPUs). Some analysts believe Nvidia’s top-tier chips could account for more than 90% of the GPUs deployed in AI-accelerated data centers this year. The early stage scarcity associated with these chips has afforded Nvidia exceptional pricing power.

But there are also plenty of reasons to believe Nvidia is in a bubble.

For example, every next-big-thing trend and innovation over the last three decades has worked its way through an early stage bubble. Investors have a habit of overestimating the adoption of new technology, and I don’t anticipate AI being the exception.

Nvidia is also likely to see its pricing power wane in the quarters to come as new competitors enter the space and the company’s own production reduces the scarcity of AI-GPUs. The bulk of Nvidia’s 217% data-center sales growth in fiscal 2024 (ended Jan. 28, 2024) can be traced to its pricing power.

The chief concern might just be that its top four customers, which are “Magnificent Seven” constituents and comprise roughly 40% of its sales, are all developing in-house AI chips for their data centers. One way or another, Nvidia’s orders from its top customers are liable to taper off in the quarters to come.

If history rhymes, once more, and the AI bubble bursts, Nvidia’s market cap could crater (in context to where it is now) and allow other companies to leapfrog it.

Here are five companies — not including Microsoft and Apple, which are already ahead of Nvidia — which have the tools and intangibles to be worth more than Nvidia three years from now.

The first industry titan that shouldn’t have any trouble surpassing Nvidia’s market cap over the coming three years is Alphabet (NASDAQ: GOOGL)(NASDAQ: GOOG), the parent company of internet search engine Google, streaming platform YouTube, and autonomous-driving company Waymo, among other ventures.

The reason Alphabet would hold up substantially better than Nvidia if the AI bubble bursts is because it’s a veritable monopoly in internet search. In March, Google accounted for more than 91% of worldwide internet search share. Looking back through nine years of monthly data from GlobalStats, Google hasn’t ceded more than 10% of global internet search share to all other companies, combined. It’s the clear-and-obvious choice for advertisers looking to get their message in front of users, and it’s going to benefit immensely from long periods of domestic and international growth.

Google Cloud can also thrive if Nvidia stumbles. Enterprise cloud spending is still in its early innings, and Google Cloud has gobbled up a 10% share of worldwide cloud infrastructure service share, as of September 2023. Since cloud margins are traditionally juicier than advertising margins, Alphabet’s cash flow growth may accelerate in the latter-half of the decade.

Like Alphabet, e-commerce juggernaut Amazon (NASDAQ: AMZN) can jump back ahead of Nvidia at some point over the next three years if the AI bubble deflates.

Most people are familiar with Amazon because of its world-leading online marketplace. In 2023, an estimated 38% of online retail spending in the U.S. was traced to its e-commerce site. But the real benefit of having more than 2 billion people visit Amazon’s website each month is the advertising revenue it can generate, and the subscription revenue brought in via Prime. Amazon topped 200 million Prime users in April 2021, and has almost certainly added to this figure since becoming the exclusive streaming partner of Thursday Night Football.

However, Amazon’s premier cash flow driver is its cloud infrastructure service platform. Despite accounting for a sixth of the company’s net sales, Amazon Web Services (AWS) consistently generates 50% to 100% of Amazon’s operating income. AWS is the world’s top cloud infrastructure service platform by spend, per Canalys.

Even though social media company Meta Platforms (NASDAQ: META) is betting on a future fueled by AI and augmented/virtual reality, the company’s core operations should sustain double-digit earnings growth and help lift its valuation well past Nvidia come 2027.

Meta’s “secret sauce” is no secret at all. Despite its metaverse ambitions and big spending at Reality Labs, the company’s bread-and-butter continues to be its social media empire. It’s the parent of the most-visited social site on the planet (Facebook), and collectively attracted just shy of 4 billion monthly active users during the December-ended quarter with its family of apps. Just as advertisers willingly pay a premium to Alphabet’s Google because of its dominance in internet search, Meta’s ad-pricing power tends to be superior in most economic climates.

The other reason Meta can shine and completely close the roughly $1 trillion valuation gap between it and Nvidia over the coming three years is its balance sheet. Meta is a cash-flow machine. It generated more than $71 billion in net cash from operations last year and closed out 2023 with $65.4 billion in cash, cash equivalents, and marketable securities. Not only does this cash provide a buffer to the downside, but it affords Meta the luxury of taking chances that few other companies can match.

A fourth company that can surpass AI stock Nvidia’s market cap over the course of the next three years is conglomerate Berkshire Hathaway (NYSE: BRK.A)(NYSE: BRK.B). Since Warren Buffett took the reins at Berkshire Hathaway in the mid-1960s, he’s overseen an annualized average return on his company’s Class A shares that’s approaching 20%!

One of the primary reasons Berkshire Hathaway has been such a moneymaker for investors is the “Oracle of Omaha’s” love of dividend stocks. Berkshire is on track to collect in the neighborhood of $6 billion in payouts this year, with just five core holdings accounting for almost $4.4 billion in aggregate dividend income. Since dividend-paying companies are often profitable on a recurring basis and time-tested, they’re just the type of businesses we’d expect to grow in lockstep with the U.S. economy over long periods.

Warren Buffett and his investment team also gravitate to brand-name businesses with trusted management teams. For instance, the $155 billion invested in Apple adds up to almost 42% of Berkshire Hathaway’s invested assets. Apple is one of the world’s most-valuable brands, and CEO Tim Cook has done a masterful job of leading ongoing physical product innovation while also pivoting the company to a subscription services-driven future.

The fifth stock that’ll be worth more than artificial intelligence stock Nvidia three years from now is payment-processing behemoth Visa (NYSE: V). As things stand now, Visa will have to close a nearly $1.7 trillion valuation gap. But if the AI bubble pops and Visa keeps doing what it’s been doing for decades, it can happen.

What makes Visa tick is the company’s long runway of opportunity. It’s the undisputed market share leader in credit card network purchase volume in the U.S. (the largest market for consumption globally), and has a multidecade opportunity to organically or acquisitively push its payment infrastructure into underbanked regions, such as the Middle East, Africa, and Southeastern Asia. Visa should be able to sustain a double-digit earnings growth rate throughout the remainder of the decade, if not well beyond.

Visa’s other source of success is its relatively conservative management team. Although it would probably be wildly successful as a lender, its leaders have chosen to keep the company solely focused on payment facilitation. The advantage of this approach is that Visa doesn’t have to set aside capital to cover loan losses during economic downturns since it’s not a lender. The result is a profit margin that’s consistently hovered at or above 50%!

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 1, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Sean Williams has positions in Alphabet, Amazon, Meta Platforms, and Visa. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Berkshire Hathaway, Meta Platforms, Microsoft, Nvidia, and Visa. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Prediction: 5 Stocks That’ll Be Worth More Than Artificial Intelligence (AI) Stock Nvidia 3 Years From Now was originally published by The Motley Fool

Forecasts lacked realistic representations of price and wage setting.

Source link