“We are in our late 60s and in good health, and we have a second home worth $900,000 that is fully paid for.”

Source link

“We are in our late 60s and in good health, and we have a second home worth $900,000 that is fully paid for.”

Source link

Micron Technology (NASDAQ: MU) wowed investors last week with an outstanding set of results for the second quarter of its fiscal 2024, reporting a massive jump in its revenue and a surprise profit, and this sent shares of the memory specialist soaring.

The chipmaker benefited from a jump in demand for memory chipsr. As a result, its revenue increased a massive 58% year over year to $5.8 billion. Micron is anticipating stronger year-over-year growth of 76% in its top line in the current quarter, driven by increased appetite for memory chips from artificial intelligence (AI) servers, smartphones, and personal computers (PCs).

The memory industry has witnessed a significant turnaround of late as demand for consumer electronics is back on track, while AI has created the need for advanced memory chips known as high-bandwidth memory (HBM). Micron management remarked on the latest earnings-conference call that its HBM capacity for 2024 is sold out, while the “overwhelming majority of our 2025 supply has already been allocated.”

This is good news for Lam Research (NASDAQ: LRCX), a semiconductor equipment manufacturer that gets a big chunk of its revenue from selling its goods to memory manufacturers such as Micron. Let’s look at the reasons why Micron’s latest results are an indication that investors would do well to buy Lam Research stock right now.

In the most recent quarter, Lam Research got 48% of its revenue from selling semiconductor manufacturing equipment to memory manufacturers. This explains why the company’s results in recent quarters have been poor. An oversupply in the memory market forced the likes of Micron and others to put a hold on capacity expansion, and so Lam’s top and bottom lines have been heading south.

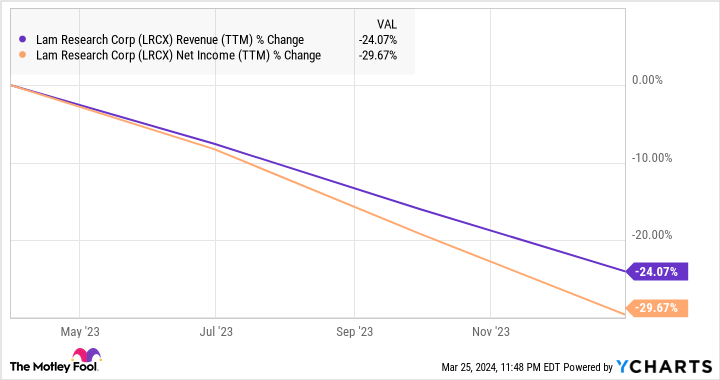

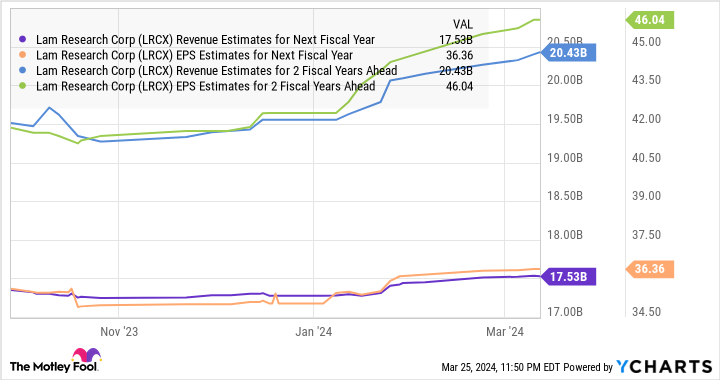

Analysts expect the company to finish the current fiscal year with a 22% decline in revenue to $13.6 billion. Additionally, earnings are expected to drop to $26.76 per share from $34.16. However, as the following chart shows, Lam Research’s revenue and earnings could jump sharply in the next fiscal year, which will begin at the end of June 2024.

Micron’s latest results and management commentary tell us just why Lam’s fortunes are set to turn around. Memory makers will need to increase their supply of HBM to cater to the growing demand from AI servers. The good part is that Lam is already witnessing solid orders for HBM equipment. CEO Tim Archer pointed out on the company’s January conference call with analysts: “In 2024, we expect our HBM-related DRAM and packaging shipments to more than triple year on year… “

It is also worth noting that the overall memory market is set to jump big time in 2024. According to Gartner, the memory industry’s revenue could jump 66% this year following a 39% drop in 2023. More importantly, the growing adoption of AI is set to drive robust long-term memory demand.

According to Micron, AI-enabled PCs are likely to carry 40% to 80% more DRAM (dynamic random access memory) content when compared to traditional PCs. On the other hand, the company expects AI-capable smartphones to “carry 50% to 100% greater DRAM content compared to non-AI flagship phones today.”

Meanwhile, the demand for HBM is forecast to more than double in 2024, generating $14 billion in revenue as compared to $5.5 billion last year. Even better, the HBM market could generate almost $20 billion in revenue next year. All this indicates that memory manufacturers will have to ramp up their production capacities, and a closer look at the industry indicates this is just what’s happening.

Samsung, for example, is expected to increase HBM production by 2.5 times in 2024, followed by a 2x increase next year. Similarly, SK Hynix expects to increase its capital expenditure this year to support increasing HBM demand. As such, the end-market conditions are set to turn favorable for Lam Research.

Lam Research is currently trading at 27 times forward earnings estimates. That’s a small discount to the Nasdaq-100‘s average multiple of 28 (using the index as a proxy for tech stocks). If Lam Research’s earnings hit the $46 estimate, and it were to trade at 28 times earnings, that would put its stock at $1,288, a 33% jump from its current price.

However, don’t be surprised to see the stock delivering stronger gains as the market may reward it with a higher earnings multiple thanks to its AI-fueled growth, which is why investors should consider buying this semiconductor stock before it jumps higher.

Should you invest $1,000 in Lam Research right now?

Before you buy stock in Lam Research, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lam Research wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Lam Research. The Motley Fool recommends Gartner. The Motley Fool has a disclosure policy.

1 Semiconductor Stock to Buy Hand Over Fist After Micron Technology’s Stellar Report was originally published by The Motley Fool

A long-overdue step toward giving investors crucial information to make informed decisions.

Source link

If Tony’s Chocolonely founder Teun van de Keuken had his way, he would’ve ended up behind bars long before he created his popular chocolate company.

The Dutch journalist made an attempt to get himself arrested in 2005, showing up to a police station and declaring himself a criminal. The crime? Fueling slavery by knowingly purchasing a chocolate bar made with illegal child labor.

When his activist stunt failed, van de Keuken came up with a new plan: creating a chocolate bar of his very own that proved the candy could be made without any exploitation of children.

His chocolate company would pay West African cocoa farmers a living income to help combat the scourge of child labor, and its beans would be sourced from land that had been deforested.

Nearly 20 years later Tony’s Chocolonely is not only one of the most popular chocolate brands in van de Keuken’s native Netherlands, it is known around the world.

The brand, whose stated mission is to make “100% slave free the norm in chocolate,” can be found at manor US retailers like Whole Foods, Target and Walmart. Its revenue grew 23% last year to $162 million.

“We’ve demonstrated it’s possible to pay a living income to farmers to address the challenges of child labor,” CEO Douglas Lamont told CNBC Make It in a recent interview. “[We’ve shown] you can be a successful chocolate company doing it the right way, in an ethical way.”

For the full story of how Tony’s Chocolonely went from a stunt to a global brand, check out CNBC Make It’s video.

Want to make extra money outside of your day job? Sign up for CNBC’s new online course How to Earn Passive Income Online to learn about common passive income streams, tips to get started and real-life success stories. Register today and save 50% with discount code EARLYBIRD.

Plus, sign up for CNBC Make It’s newsletter to get tips and tricks for success at work, with money and in life.

When I buy a stock, I try to remind myself that I am buying a small part of a business and that I intend to hold my stocks for the long term. Warren Buffett famously said that his favorite holding period is forever. While that’s aspirational more than anything, it’s an important reminder that success in investing comes from identifying great businesses and then letting them compound over decades.

While some stocks in my portfolio have a lot more to prove to stay there forever, there are some that I can’t imagine myself selling. These businesses have long track records and competitive advantages that should pave the way for bright futures. As the saying goes, “Never say never.” Yet with these stocks, I’m as close to never selling as one can be.

Every time I am struggling to find parking or waiting in the long (but efficient) line to check out, I ask myself why I don’t own more Costco Wholesale (COST 0.07%) stock. While most of my fellow shoppers are likely not having the same thought, we’re all there to take advantage of the bulk quantities and low prices. History tells us that this business model has been wildly successful with Costco shares gaining more than 81,000% since its IPO.

Costco ended its fiscal 2024 second quarter (ended February 2024) as the third-largest global retailer and the 12th-largest company in the Fortune 500, with 874 locations worldwide. Its membership model works well. More than 92% of Costco members renew their membership and the company brought in nearly $5 billion in membership fees in the past 12 months.

The low prices keep customers coming in the door, and because Costco sells fewer items than its competitors and turns its inventory over very quickly, it can sometimes even sell items before they need to be paid for. This helps cash flows and reduces expenses.

If there’s a retailer that comes first to mind for me other than Costco, it has to be Amazon (AMZN 0.31%). I don’t think I am alone in finding myself shopping there before almost anywhere else. Over the trailing 12 months, Amazon stock is up 82%. However, during the market slump of 2022, the company fell nearly 50% as it struggled to get its finances back in order following the massive distribution build-out necessitated by the pandemic surge in orders.

Amazon is certainly back on track and ready to reaccelerate its growth. In 2023, Amazon grew revenue by 12% but the more impressive results were further down the income statement. Operating income increased by 202% and net income grew by 1,226%. These results were driven by a recovery in the e-commerce business, which finally turned the corner after its 2022 struggles. It’s also worth remembering that Amazon Web Services (AWS) remains the leader in cloud infrastructure and it grew its revenue by 13% in 2023.

Consumer electronics giant Apple (AAPL -1.06%) has been in the news lately for all the wrong reasons. Finding itself increasingly under the microscope of federal antitrust investigations, the stock has fallen 12% over the past three months. This news is certainly worth watching, but it will take years to play out and the rather modest decline in Apple’s share price suggests the market’s level of concern is less severe than some of the headlines indicate.

Taking a step back, it’s important to remember that Apple is still a ubiquitous brand around the world, and especially within the United States. Known for its iPhone and other consumer electronic devices, Apple is slowly becoming a software company. Apple now has an installed base of more than 2.2 billion devices.

This creates an ecosystem of apps and subscription services that provide a high-margin income stream for the company. In the most recently reported quarter, services revenue (which is where all the subscription products are reported) grew by 11% to $23 billion. This represents 19% of total revenue, up from 18% in the year prior.

Are there scenarios in which I might sell these companies? Sure, anything is possible. However, these three businesses are so competitively advantaged and are still growing so impressively at their large scale, that it’s difficult to envision a scenario where they wouldn’t warrant a spot in my portfolio. Investing can be as simple or as complicated as you want it to be. In my mind, buying and owning these three stocks is about as simple as investing can be.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jeff Santoro has positions in Amazon, Apple, and Costco Wholesale. The Motley Fool has positions in and recommends Amazon, Apple, and Costco Wholesale. The Motley Fool has a disclosure policy.

There was a time when the S&P 500 reaching record highs without any help from Apple Inc. was almost unthinkable. But those days are over, at least for now.

Source link

Lynn Curry, nurse practitioner for Huntsville Reproductive Medicine, P.C., lifts frozen embryos out of IVF cryopreservation dewar, in Madison, Alabama, U.S., March 4, 2024.

Roselle Chen | Reuters

As legal battles over reproductive rights increase across the U.S., one area that could be impacted is egg freezing.

In February, the Alabama state Supreme Court ruled that all embryos created through in vitro fertilization are considered children. This ruling could have far-reaching ramifications of civil and criminal liabilities for fertility clinics and their patients. Over 1 million frozen eggs and embryos are stored in the United States alone, according to biotech fertility company TMRW Life Sciences.

Women who choose to undergo reproductive technology procedures such as egg freezing face a long road riddled with obstacles. Here’s a look into the driving forces behind egg freezing and the financial, social and emotional costs that come with it — based on personal experiences from women across the country.

There’s a notion that most women delaying motherhood are doing so to focus on other aspects of their lives, such as their careers. That’s not so much the case anymore, according to Marcia Inhorn, a professor specializing in medical anthropology at Yale University.

“The majority of women who freeze their eggs are doing it because they have not found a partner. I call that the mating gap — the lack of eligible, educated, equal partners,” Inhorn, who last year authored the book “Motherhood on Ice: The Mating Gap and Why Women Freeze Their Eggs,” told CNBC.

This problem stems from the fact that today, women are receiving higher education at greater rates than men. Inhorn noted that women are outperforming men in higher education in 60% of countries, and that in the United States alone there are 27% more women than men in higher education.

“The result is that, for women who are highly educated in America and of reproductive age — between 20 and 39 — there literally are millions too few college-educated men,” Inhorn added.

Another reason women freeze their eggs is the sense of empowerment the procedure brings them. Fundamentally, Inhorn believes that this freedom that egg freezing allows is what ultimately draws increasingly younger women to the procedure.

“It gives you a little reprieve, a little extra time,” she said.

This statement is one that reproductive endocrinologists and fertility specialists Drs. Nicole Noyes and Aimee Eyvazzadeh agree with.

Noyes, who has worked in the fertility industry since 2004 and is based in New York, has seen a noticeable shift in her patients’ ages and attitudes in the last two decades. In the beginning, her patients tended to be older, in their early 40s and viewed egg freezing as a last-ditch procedure as they hedged the end of their reproductive lives. Now, women as young as their late 20s come in to see Noyes.

Eyvazzadeh, who has also worked in the field for 20 years and lives in California, has noticed a trend towards younger patients who are choosing to freeze their eggs while they’re at their most viable.

This is the case for social media influencer Serena Kerrigan, who just recently turned 30. Despite being in a relationship, egg freezing was a procedure she willingly undertook while focusing on growing her business, she told CNBC.

Kerrigan, who has more than 800,000 followers between her Instagram and TikTok and is based in New York, began sharing her egg freezing journey last year. She wanted to remove some of the stigma around egg freezing and give her followers an inside look at the arduous process.

Kerrigan has paid for all her procedures on her own, she told CNBC, and recently partnered with her clinic, Spring Fertility, to donate a round of egg freezing to one of her followers. Eventually, she hopes egg freezing can be less stigmatized.

“There’s a layer of shame or taboo that I actually don’t understand. To me, this is science, and this is incredible, and this is a huge advancement,” she said. “This is a way of putting the power back into women and having control of their lives.”

While the benefits of egg freezing are certainly enormous, so too are the associated costs.

The average price for a single egg freezing cycle in the U.S. clocks in at $11,000. Many women need multiple egg freezing cycles, especially as they grow older and egg number and quality begin to deteriorate. That’s not to mention additional charges like hormone medication and yearly storage fees, which could respectively clock in at around $5,000 and $2,000.

Nutrition health coach Jenny Hayes Edwards froze her eggs in 2010 at 34 years old and was one of the first women in the U.S. to undergo the procedure. Despite it still being labeled an “experimental” procedure in the U.S., Hayes Edwards was certain she wanted to try. She wasn’t dating anybody at the time and was “working like crazy” while running her restaurant businesses in Colorado.

But high costs were her number one obstacle. Her restaurants had taken a hit after the 2008 financial collapse, when many consumers began foregoing their expensive ski vacations in Colorado.

Hayes Edwards remembers it being a tough decision to make. But her mother eventually helped sway her in favor of the procedure.

“It’s just money, and the opportunity that you might be missing is so much bigger,” Hayes Edwards recalled her mother saying. “I was so grateful that she pushed me over the edge.”

She was able to scrape together the $15,000 needed through maxing out a credit card, selling some jewelry and liquidating a bond in her inheritance.

Hayes Edwards now has a healthy three-year-old daughter, conceived nearly a decade after she froze her eggs, and is still appreciative for the extra time egg freezing bought her to meet her now-husband.

In recent years, egg freezing, fertility and family planning services have increasingly popped up as employer benefits, especially among technology companies. A 2021 study from Mercer showed 42% of large companies — those with at least 20,000 employees — covered in vitro fertilization services in 2020, up from 36% in 2015. Nineteen-percent of these companies had egg freezing benefits, more than triple the 6% offering these benefits in 2015.

Michelle Parsons decided to freeze her eggs since the procedure was offered through her job. The various tech companies Parsons has worked for have offered anywhere between $10,000 to $75,000 in fertility benefits.

Parsons, who is a lesbian, had always known that she wanted to freeze her eggs — and undertook the procedure while working at Match Group as chief product officer of dating app Hinge. At the time, neither she nor her ex-partner were ready to have children, but it was one financial incentive Parsons didn’t want to miss out on.

Besides eggs, Parsons also chose to freeze her successfully fertilized embryos as another backup. Frozen embryos have a much higher likelihood of viable thawing. In fact, Parsons’ search for a sperm donor sparked one of the most-used features on the Hinge app — voice prompts.

“When we started to listen to all of these voice recordings of potential sperm donors, the lightbulb went off in my head and I was like, wow, this is what’s missing from dating right now,” Parsons told CNBC. “Because voice gives you so much nuance into personality, humor, vibe … we ended up building that feature called voice prompts on Hinge and it was a huge, wild success that led to rapid growth for Hinge and it became viral on TikTok.”

Still, Parsons noticed egg freezing taking a toll on her professional and personal life in other ways.

“You have to inject yourself with hormones for two weeks. You have to eat differently. You don’t really want to be in social settings. You can’t drink. There are all these other ramifications around just going through that process, even though we know it’ll be for this one month and then it’ll be over,” she said.

The process also doesn’t guarantee success.

Evelyn Gosnell underwent her first egg retrieval when she was 32, following by two additional cycles at 36 and 38 years old. By the time she was ready to have children with her now-partner, the New York-based behavioral scientist had many frozen eggs ready. But, she received no viable and normal embryos after her eggs had been thawed and fertilized.

The S&P 500 is up a whopping 31.4% over the last year. But many stable, dividend-paying companies have largely missed out on the growth-fueled rally.

United Parcel Service (NYSE: UPS) and Chevron (NYSE: CVX) have lost value over that time, while Kinder Morgan (NYSE: KMI) is up less than 8%. The rationale for investing in these dividend stocks is to generate stable passive income no matter what the market is doing, not trying to outperform the S&P 500 over a short period of time.

Here’s why these Motley Fool contributors think all three dividend stocks have what it takes to continue raising their payouts and rewarding shareholders.

Scott Levine (UPS): Providing the market with 2026 financial targets, UPS suggested to investors this week that it sees growth over the next three years — a period during which the company expects to “drive higher productivity and efficiency,” according to its CEO, Carol Tome. However, investors didn’t take kindly to the news as Tome also stated that UPS is battling near-term headwinds.

However, this shouldn’t preclude forward-looking investors from picking up shares. Although they should rightly be mindful of how the company handles the current challenges, UPS is a leading supply chain company that has overcome challenges before, making it — and its forward-yielding 4.5% dividend — a smart pick right now.

One of the ways that UPS will achieve productivity and efficiency increases is through its embracing of artificial intelligence. In 2023, for example, UPS opened a new facility where AI and machine learning have taken center stage. Dubbed UPS Velocity, the Kentucky-based warehouse has more than 700 mobile robots in operation, and UPS expects to increase this to 3,000 by the end of the year. Powered by AI and machine learning, the mobile robots and human employees currently move more than 350,000 packages through the 900,000 square-foot facility.

It’s not only in warehouses where UPS is leveraging the power of AI. The company has relied on AI since 2012 for optimizing delivery routes. According to UPS, Orion “recalculates individual package delivery routes throughout the day as traffic conditions, pickup commitments, and delivery orders change.” By optimizing routes based on changing conditions, UPS can reduce both the number of miles that drivers travel and the amount of fuel that the vehicles must use — two factors that help the company to reduce costs. From 2012 through 2020, UPS estimated that Orion had helped the company to achieve annual savings of approximately 100 million miles and 10 million gallons of fuel.

Lee Samaha (Chevron): Warren Buffett bought Chevron stock this year even though the stock price was disappointing. The stock is slightly down over the last year, compared to the S&P 500’s 31% rise, and the price of oil is still above $80 a barrel.

One reason, which also explains why it’s underperformed peers like ExxonMobil, ConocoPhillips, and Occidental Petroleum so far this year, is the uncertainty around its intended $60 billion acquisition of Hess. Oil majors have been looking to acquire energy assets as they generate bundles of cash from a relatively high price of oil. Meanwhile, the sector continues to fall out of favor among investors due to concerns about investing in fossil fuels as the world transitions to clean energy solutions.

That said, there’s still a hugely important role for oil in the global economy, and there’s upward pressure on the price given OPEC and OPEC+ production cuts. Whoever wins the next election is going to have to replenish the massive drawdown in the U.S. Strategic Petroleum Reserve carried out by the current administration in an attempt to lower gasoline prices.

In addition, the International Energy Agency (IEA) has already raised its oil-demand estimate four times since November.

If the oil bulls and Warren Buffett are correct, then Chevron, with or without Hess, is likely to generate bundles of cash flow in the future, and that’s excellent news for income-seeking investors.

Daniel Foelber (Kinder Morgan): When the market is roaring higher, it’s easy to overlook quality pipeline and energy-infrastructure stocks like Kinder Morgan. After all, the growth prospects are limited.

Existing infrastructure could lose value if oil and natural gas demand falls over the next few decades. But that’s not the case right now. In fact, the world needs more energy.

Kinder Morgan is investing in infrastructure to support the export of liquefied natural gas (LNG). LNG is natural gas that has been cooled and condensed into liquid form for easier transport overseas.

Kinder Morgan’s projects require high up-front costs but produce stable cash flows thanks to long-term contracts. Kinder Morgan’s business is ideally suited as a low-growth company that returns cash to shareholders.

After cutting its dividend to $0.125 a share after the 2015 oil and gas crash, Kinder Morgan has since raised its dividend back up to $0.2825 — presenting a yield of 6.3%. Kinder Morgan has consistently raised its dividend every year since 2018, and there will probably be another moderate raise in the next quarter or two.

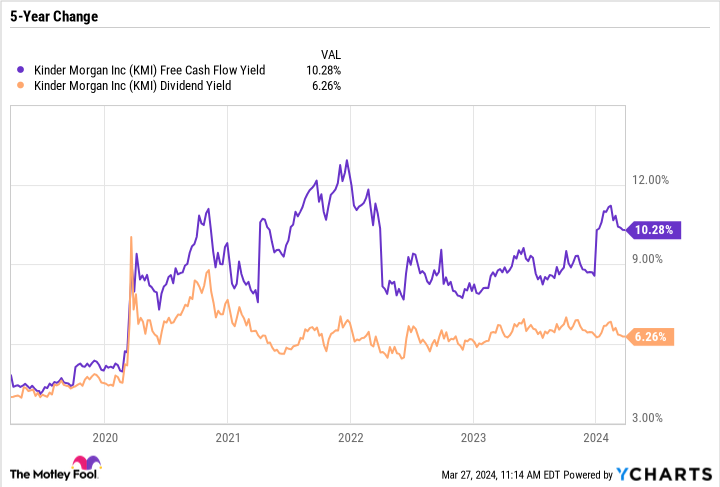

Kinder Morgan has done an impressive job restoring order to its balance sheet by paying down debt. To sustain a healthy balance sheet, Kinder Morgan must support the dividend with free cash flow so it doesn’t have to deplete its cash position or take on debt. Two useful metrics to compare are its FCF yield and its dividend yield.

As you can see in the chart, Kinder Morgan’s FCF yield is higher than its dividend yield. FCF yield is just FCF per share divided by the share price. But more importantly, it tells us how much the dividend could be if Kinder Morgan paid out all of its FCF. The four percentage point or so difference between the FCF yield and the dividend yield gives Kinder Morgan a nice margin for error. It indicates its dividend is affordable and there is room to raise the dividend in the future.

All told, Kinder Morgan is worth considering if you’re looking for an investment centered around passive income rather than potential capital gains.

Should you invest $1,000 in United Parcel Service right now?

Before you buy stock in United Parcel Service, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and United Parcel Service wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Daniel Foelber has no position in any of the stocks mentioned. Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chevron and Kinder Morgan. The Motley Fool recommends Occidental Petroleum and United Parcel Service. The Motley Fool has a disclosure policy.

Buying These 3 Beaten-Down High-Yield, Dividend Stocks Could Be a Genius Move to Boost Your Passive Income was originally published by The Motley Fool

In this podcast, Motley Fool host Dylan Lewis and analysts Emily Flippen and Jason Moser discuss:

Motley Fool contributor Brian Feroldi breaks down Reddit’s S-1 and the major risks facing the self-proclaimed “front page of the internet.”

To catch full episodes of all The Motley Fool’s free podcasts, check out our podcast center. To get started investing, check out our quick-start guide to investing in stocks. A full transcript follows the video.

This video was recorded on March 22, 2024.

Dylan Lewis: Regulators keep cranking the heat on Big Tech Motley Fool Money starts now.

It’s the Motley Fool Money radio show. I’m Dylan Lewis joining me in studio Motley Fool senior analysts, Emily Flippen and Jason Moser. Fools great to have you both here.

Jason Moser: Hey.

Emily Flippen: Good to be here.

Dylan Lewis: We’ve got a mini-dive on a splashy IPO, a story of a struggling ice cream brand and of course, stocks on our radar. Up first though, regulators continue to focus on big tech. Jason Apple is in the cross-hairs of regulators. The FTC filing suit this week aimed at Apple’s iPhone and it’s accompanying suite of services. The FTC alleges that Apple undermines apps, products, and services that would otherwise make users less reliant on the iPhone, promote interoperability and lower costs for consumers and developers. This seems to really boil down, Jason, to the walled garden that Apple has been able to maintain with it’s software and hardware.

Jason Moser: I was going to say, the walled garden really is the phrase that stands out here. This is something that could have some teeth. We’ll have to wait and see there. I’m certainly no antitrust expert nor am I litigator, but I think one thing for sure, this isn’t good in that it’s not going to be resolved anytime soon. We have an idea that this is going to take several years to play out. I think that is probably the biggest near-term risk for Apple in that it’s going to more than likely take their attention away from where they really need to be focused, that’s on innovation.

You look at Apple today, it still really is a phone company meaning at the end of the day, that’s where they make most of their money. Now, that’s slowly starting to change. They are bringing more in regard to services, revenue, and whatnot. But for a company like Apple, I would argue that Apple saved the Vision Pro and I am not a believer that the Vision Pro is going to be accepted by the masses, by any stretch. Fascinating technology, but Apple, has been stuck in this iteration as opposed to innovation cycle.

They’re just not innovating as much as I think people would like to see and that comes at a cost. That starts to bring growth into question. They’re going to have to deal with this for a while and then it takes away from whatever they may be working on. If it takes away from that innovation, that obviously is a near-term risk. Now, this probably ends up as something were Apple has to use money to make the problem go away and that’s not a bad problem for a company like Apple. I did think it’s interesting to note that our balance sheet, we always talk about how much cash Apple has more than most countries.

Apple’s now in a net debt position, which I think is just fascinating to see now, that’s a fine position for them because that debt is stretched out over long periods of time, very low interest debt, and it’s the cash machine. Ninety-five billion dollars of free cash flow after accounting for stock-based compensation. That’s not a problem for them at all, but it is something that is going to take their eye off the ball for a while.

Dylan Lewis: Emily, Apple has very long argued that a lot of the decisions they make within their ecosystem are in the interest of their users, privacy, security, trying to make sure there’s not malicious apps or things like that that are getting out there. We will see where this winds up landing for the company. But I look at this, especially given the series of interventions we’ve been seeing from the FTC and say, regulators are not shying away from Big Tech anytime soon.

Emily Flippen: I’ve been historically dismissive of regulations against a business like Apple because for the most part they’ve been without teeth. That was up until very recently when Apple actually lost a series of judgments in the EU against the use of its App Store. They’ve prevented third-party apps from being able to come in, in-part because they want to maintain that walled garden for their costs.

I said, hey, look, we’ve seen these cases come up in United States, but lower courts have continuously sided, for the most part, with Apple. So to see this come out, especially from the Department of Justice and FTC, it’s clear that this is a bigger overreaching judgment that’s looking at the core of Apple’s business instead of one particular issue, which is really interesting because it’s penalizing Big Tech for being Big Tech.

Being the dismissive person I am, I’d be easy for me to say, hey, look, we’re heading into an election year, the Department of Justice tends to be very politically connected so we don’t really know what’s going to happen in terms of a potential change in administration, whether or not that will change anything for the future. So I wouldn’t be surprised to see nothing come of this, but my dismissiveness in the past has not paid off well so maybe I’ll be a little bit more cognizant moving forward.

Dylan Lewis: Sticking with the Big stories, a huge stock split announced for Chipotle this week. In release, Emily, the company announced a 50-for-1 stock split. I had to double-check that one. I wasn’t even sure that was accurate. I have never seen a stock split of that size.

Emily Flippen: I guess it’s not just Chipotle serving sizes that are getting smaller. [laughs] I say that very tongue in cheek. So stock splits can sometimes raise a lot of investor interest. In this case, a 50-for-1 stock split, which basically means, if you owned one share of Chipotle prior to a split, you are now going to own to 50 shares of Chipotle. They will decrease in price by 50 folds, but you will in turn own 50 more. It’s essentially like cutting up a pizza.

You can have a giant pizza and you can cut it into eight different slices, or you can cut it into 500 different slices, isn’t changed the size of the pizza it just changes the size of the slice, but in this case, it actually can increase accessibility for some investors who don’t have access to fractional share trading, increased accessibility for those who may trade options, as well as for Chipotle to issue its own stock back to employees and internal use. It’s an interesting development, but not one that if you’re a shareholder of Chipotle changes anything in terms of the business performance.

Dylan Lewis: Jason, I think the academic argument was laid out very well right there by Emily’s saying this is how you cut up the pie. I do think when we look at stock splits, very rarely is it a sign that a company is doing something poorly. When we see a stock split of this magnitude, and I think it is just a testament to the incredible run that Chipotle has gone on over the last 15 years.

Jason Moser: It’s been a very incredible run, particularly when you consider the lows that this company hit in regard to the food safety issues from several years back, real recovery there now, it required a leadership change, but you got to do what you got to do. This company has a much better spot today as a shareholder, as a consumer of the product. I love everything that they’re are doing. I’m glad you mentioned issuing stock to employees because I think that’s another thing to point out in the release and like they use this word here, to commemorate this special event

There commemorating this special event, first stock split in history. But they announced a special one-time equity grant for all restaurant General Managers and crew members with more than 20 years of service. We also saw something like this with Amazon. You see it with all of these companies when their share price gets to the point where you’re talking about thousands of dollars, it just becomes very difficult to use equity as a form of compensation. This is going to allow them to do that. I’m not saying that’s the reason why they did it, but it’s certainly a benefit that comes from it.

Dylan Lewis: Before we go to break, we’ve got a new name on the New York Stock Exchange, shares of Reddit hit the market this week. Emily, judging by the reaction, the market excited to see some new names in the IPO market. Shares currently up 50% from where they listed.

Emily Flippen: Shares are fluctuating pretty greatly here, which is not surprising. Also not surprising to see it up so significantly because the IPO was oversubscribed, one of the things that Reddit did. This is a platform, social media platform of sorts, who has offered some of its most loyal and engaged users the opportunity to buy in at their IPO, and contrast, the IPO gives an opportunity for some of their long-term investors and private equity venture capitalists to actually be able to sell out of the company as well. It does test the market’s appetite for IPOs, which I can understand, because it’s the first big tech related IPO we’ve had in a while. But at the same time, given they’re really unique nature of Reddit’s business, the unique nature of this solicitation for the IPO, I think it’s too early to say that this shows that investors are ready again for IPOs.

Dylan Lewis: I think it’s at least a decent sign that we saw a company like Cava come public earlier in the last 12 months and now we have Reddit as well. Jason, when you look out at the Reddit IPO, any thoughts?

Jason Moser: I’m just between this common Chipotle talk now I’m starting to think about Reddit. I’m not a Reddit user, I have been linked to Reddit before, when doing a Google search or something like that. To me, I think this is one where I would absolutely just play, wait and see. It seems to me, at least, that this rhymes a lot with Twitter back in the day. Probably a limit as to how they can really grow that overall user base. It’s a little bit of a different platform to use. Some might say it’s a little bit complicated, a little bit difficult to use. A lot of similarities in what we saw when Twitter first became public, similar concerns. It’s not to say it can’t be successful, but for me, I would absolutely just play wait and see, and let’s see if these guys can really generate some meaningful cash.

Dylan Lewis: If you want more on the Reddit IPO, stay tuned, we’ve got to mini dive coming on the back half of the show, but coming up next, we’ve got Earnings that give a glimpse into two big names and apparel and why they’re struggling. Stay right here. You’re listening to Motley Fool Money. Welcome back to Motley Fool Money. I’m Dylan Lewis, joined here in studio by Emily Flippen and Jason Moser. It’s the tail end of earnings season but we still have some big names reporting this week. Emily, speaking of the tail end, we have an update from pet supplier, Chewy, shares down after reporting, what’s going on with pets bar?

Emily Flippen: If I’m CEO Sumit saying, I’m looking at the market and saying what do you want? [laughs] But actually tell me because what the market was saying for Chewy at this point last year was effectively, hey look, we like your platform. It’s great you’re seeing all this engagement, but you need to have profits. What has Chewy done over the course of the past year? Well, expand profits and that’s exactly what we saw this quarter. Financially, the company’s results were really solid. Sales grew again by their non-discretionary spend. This is things like pet food, cat food, dog food, those repeat purchases, but margins are incredibly strong.

They continue to expand. The company, expanded its free cash flow by nearly three times and management actually said that they think they’ve reached an inflection point for the expansion of their cash flow generation moving forward as well. We have sales growth, margin expansion, cash flow expansion. It begs the question of why is Chewy down? Why do investors not like the stock? Unfortunately for Chewy, that comes back to the pet industry right now.

There has been a slower amount of growth, which is to say negative growth and pet household formation, which is basically the number of people who are buying pets domestically in the United States and that’s been on a pretty consistent decrease since the pandemic, when a lot of pet households were formed in the first place. Now, despite the fact that these pet households that were formed are consuming Chewy and engaging with the product, the same rate that the previous non-pandemic pet households are, that growth has still lead the market to believe, maybe that top-line growth moving forward is just not going to be high enough to justify Chewy’s valuation for which I still believe the company is massively undervalued in relationship to the size of its long-term market.

Dylan Lewis: You are still believer and you feel like the market is underestimating what Chewy’s doing?

Emily Flippen: Yes. In terms of their core E-commerce business. Where I do get a little bit hung up is that, some of their new initiatives. These have been great so far. This is the push into pet pharmacy, pet healthcare, those you call it teledog to steal a word from Jason. All of that is great because it integrates directly onto Chewy’s platform. If you’re an Autoship customer, you get access to a lot of this stuff for free. But one of their newest initiatives is opening up actual physical vet care clinics. They’re starting in Florida where Chewy is headquartered and plan to use that as a gauge for expansion across the rest of United States. Now, they’re smart and slow about how they expand and I appreciate that because again, they don’t want to negatively impact that cash flow. But there is a little bit of potential like a hubris, I guess, that is in building physical stores, that is a massive deviation from their previous strategy so as a Chewy shareholder, that’s probably the thing I’m watching most closely.

Dylan Lewis: Over to apparel, we have earnings from Nike and Lulu. Lemon this week, let’s start out with the goddess of victory, Jason, shares of Nike down 8% after reporting fiscal Q3 results. It seems like Nike is a bit of a company at a pivot or inflection point.

Jason Moser: I think that’s fair to say. I think the result or the market’s reaction is probably a result of guidance, which I’ll get to in a minute. But I don’t think anyone will question how strong a business or brand this ultimately is. But they’ve definitely hit some headwinds recently and in part of that, it was discussed in the call, they had this deliberate strategy, they refer to as the Consumer Direct Acceleration strategy. They wanted to be more of a direct-to-consumer business via digital and their Nike stores. That worked out OK over the last few years because everything was thrown into chaos with, with the pandemic.

But we’re seeing this great reset back to normalcy and Nike is recognizing that this focus on direct came at the cost of all of the success they’ve witnessed through the years, through their wholesale channels. What that resulted in was essentially flat top-line growth for the quarter and ultimately, when I refer to guidance, this was for the third quarter. But when you look out to fiscal 25, they’re actually guiding, at least for the first half of the year, low to mid single digit sales declines. It is something where you’ve got this business, they’re a little bit of a restructuring mode.

It wasn’t a bad quarter and honestly, when you look at where the business, the fundamentals are still good, gross margin was up 150 basis points, inventories standing at 7.7 billion. Now, that was down 13% so it’s nice to see they were able to get those inventories down while pushing those gross margins up. Cash and equivalents that still in very good shape here in cash and short-term investments, $10.6 billion. You look globally, China performed well up 6% versus North America’s 3%.

I think really now it’s just a matter of getting back to that wholesale opportunity. They recognize the opportunity in direct, but maybe they placed a few, too many eggs in that direct basket. It’ll take a little investment in product, a little investment in marketing, and I think we can expect that to flow down to the bottom line, not in a good way. That’s a near-term issue. They’ll figure that out. I think you’ve got to be looking at sell-offs like this with a company like this, and asking yourself if you don’t want to own a few of these shares.

Dylan Lewis: Emily, Lululemon also in the dumps post-earnings shares down 17%. It seemed like a big part of the reason why it was the company’s outlook.

Emily Flippen: Outlook and maybe tonality, I’ll add in there because CEO Calvin McDonald was immediately defensive on Lululemon’s earnings call. Some of the first words out of his mouth were “As you’ve heard from others in our industry, there’s been a shift in US consumer behavior” which nobody wants to hear. But that did distract from what is otherwise a really strong quarter for the company, it had a really strong holiday season, updated their guidance in January as a result, and then exceeded that guidance again in this most recent quarter.

But they did choose to focus a lot on how the behavior of North American consumers has changed recently, in part because it seems like the economic outlook which is impacting, as Jason just mentioned, numerous industries across the United States, but also because they didn’t do a great job of managing their own inventory, which is to say, McDonald accounted for some of the loss to not having the right colors or the right sizes in stock.

In their defense, their inventory has continued to decrease. It’s not like the company is over here buying a bunch of products, stocking them in stores and then throwing their hands up and saying nobody wants it. You have to give management the benefit of the doubt, but there is certainly a bigger story here just to say, we’ve been waiting a long time for the economy to slow down in the United States, for consumer behavior to shift, are these the first canaries in the coal mines that consumer spending is about to be in the dumps over the course of 2024?

Dylan Lewis: I look at Nike, and I also look at Lululemon, and we’ve seen a lot of discussion of consumers trading down as a major story to be watching, looking for more discount options as well, let’s get a little bit tighter. Do you feel like this is something that’s affecting the results here?

Emily Flippen: It’s possible, I will want to see the results from other discount retailers. I’m thinking about like the T.J.Maxxs of the world to see if they’re picking up some of the slump here from Lululemon. But I do think that regardless of what’s driving it, I’m not sure if it really matters from Lululemon’s perspective because they don’t play that game. They don’t mark down and that’s a conscious effort on their part.

Jason Moser: I think that’s important to note too, we’re talking about this for Tay be like Tiffany, in that they understand the value in that brand. They need to protect it by not discounting. When you start putting that stuff on fire sale, all of a sudden, you associate that brand a little bit differently. I think we saw Under Armour for many years trying to play that. Let’s just get this stuff out to as many people as we just sell as much stuff as we can. They lost some brand credibility. That really does play out on those, not only the financials in the near-term, but it creates some long-term headwinds. It’s really difficult to bounce back from that.

Dylan Lewis: We’re going to wrap the earnings takes with a look at Accenture, shares down 12% after earnings. Jason, we’re also seeing results from the company dragging down some of the other companies in the consulting space this way?

Jason Moser: We were talking about Nike being a little bit more company created headwinds. Really Accenture, this is less a company thing, this is more a macro thing. You look at the call there. They said in the call, they see clients continuing to prioritize spending in large-scale transformations, things like AI for example and that converts to revenue more slowly, but then they also see continued delays in decision-making and a slower pace of spending.

That’s really something that is completely out of their control and they just have to deal with it. But the good news is that once that spending does start picking back up, Accenture is one of the first places that should see the benefits there. Now, they did guide down, revenue growth somewhere in the neighborhood of 5%, they guided that down to 3%, pulling earnings back considerably as well. They solve financial services, take a good hit, that’s about 20% of their revenue. The good news is they’re making a lot of investments in AI, they do continue to see the tailwinds there. It’s a macro stretch that they’re going to have to get through.

Dylan Lewis: Emily Flippen, Jason Moser, Fools, we’re going to see you guys a little bit later in the show. Up next, we’ve got a 15-minute Dive Into fresh IPO, Reddit, some of the major risks, some of the major opportunities, and what you need to know for this newly listed company. Stay right here. You’re listening to Motley Fool Money.

Welcome back to Motley Fool Money. I’m Dylan Lewis. This week, a familiar name went public, Reddit, the home of WallStreetBets and the epicenter of the meme stock movement listed its shares on the New York Stock Exchange. As a longtime Redditor, I was excited to dig into the S1 and look at the company’s books. Motley Fool contributor Brian Feroldi, joined me for a mini dive into the site bet, is the self-proclaimed front page of the Internet. Shares of Reddit hit the public markets this week under the ticker RDDT. Joining me to do a mini dive on these social media slash news slash community company is Motley Fool contributor Brian Feroldi. Brian, thanks for jumping on.

Brian Feroldi: Thank you for having me, Dylan. I’ve had my eyes on this company for a while, so I’m glad we finally have numbers to put to the name.

Dylan Lewis: I know we actually checked in on this business back in the beginning of 2022 when it seemed like an IPO was on the horizon. We’ve been waiting for that IPO for a little over two years now, but no more speculation. The shares are listed. Let’s dig into the business. Paint us a little bit of a picture with what you see with Reddit.

Brian Feroldi: For those that are unfamiliar, Reddit describes itself as a quote on quote, “Community of communities.” It’s a social networking slash blog site that brings millions of users together from all over the world to share news, information, recommendations, and what makes reading a little bit unique is that you can do so using an anonymous name or your real name. To put some scale behind this, this is a website that is one of the 10 most popular websites in the world. 73 million daily active users, 267 million weekly average users, over 100,000 active communities on the platform. This was an interesting tidbit considering that 98% of this company’s revenue comes from advertising, 75% of Redditors, that’s what they call their users, believed that it is a trustworthy place to inform them to make a purchasing decision. That could be a major plus in the bookcase for this company.

Dylan Lewis: That’s a key thing that advertisers are paying attention to. I’m someone who has used Reddit since college, and what’s interesting is, I think it shows the duality of the business here because they have about half of their users as logged-in users, but they also have about half of their monthly and daily active users coming in through an unlogged in experience.

We see a lot of that coming in through Google search, people finding information on the internet and then coming to the site, i have found it to be an excellent source of information, particularly for incredibly niche topics. You mentioned the community orientation and I think what’s so great about the platform is you can go really deep with people who are fanatics about something and really find your online community. It can be very useful, and trying to find information there. When you do use it just to help people who understand it, who maybe aren’t as familiar, any specific communities or topics they interact with?

Brian Feroldi: There are a few subreddits that I look at on occasion, there’s one like DataIsBeautiful, that’s subreddit has beautiful graphs and illustrations. There are some wonderful geography subreddits, and if you’re into the financial independence movement like, I am, there’s a wonderful subreddit called fatFIRE, which is all about how people are trying to retire early and live a luxurious lifestyle while doing so.

Dylan Lewis: You mentioned that this is an ad-based business. It’s also one of those high-growth type businesses and the financials really reflect a company that has been private for a while during a period of venture funding. It’s still losing money. It’s posting some decent growth. It’s moderated a little bit but what jumps out to you looking at the numbers, Brian?

Brian Feroldi: Well, first when you said high growth, depends on your definition of high growth. This company is growing at a decent rate. I wouldn’t classify it as a high-growth company. but in the last year ending 2023, we saw revenue grew 21%-$804 million. Probably the most impressive number on the income statement to me was this company’s gross margin at 86% last year, and that was up from 84% in the year-ago period so very high gross margin business.

As you teed up, that’s where the good news stops, on the income statement. This company is spending heavily on operating expenses, particularly research and development, so it’s because of that this company is losing money, $91 million net loss in 2023. Free cash flow losses was $84 million last year. The good news for investors is this company is going to have an absolute war chest of cash to continue funding those losses. Depending on what the IPO price is at, this company estimates that post IPO, it will have $1.5 billion in cash and zero debt.

Dylan Lewis: That’s nice. We like to see that safety and we’d like to see that security. I do wonder a little bit about that R&D spend. I’m curious. I mean, I think you could make a strong case for any tech platform, and you have to look at them as a platform company in a way, making those types of futuristic investments. I do wonder a little bit because it’s coming at the expense of profitability. One of the things I’ve been trying to wrap my head around Brian, looking at this company is, for folks that aren’t familiar. it is an incredibly user-generated content-type business. You have people who are posting and actually, the people who are moderating that content are also generally members of the community. You would think that it would give them a very favorable cost profile but we don’t really see that play out. Do you feel like there’s an actual path to profitability here?

Brian Feroldi: There definitely could be. I mean, the company could, of course, grow its way to profitability, but when I saw the amount of money this company is spending on research and development, I did do a double take to be like, where is that money going? I mean I’m an occasional Reddit user and the site looks pretty much the same to me now as it did a year ago, two years, and three years ago. So one would think, given that they knew that they were about to come public, that they’re using that capital to really build out the advertising tools that will make their platform even more attractive to advertisers, which does take some investment but I have a feeling this company’s path to profitability is through growth and not through cost-cutting.

Dylan Lewis: Speaking of growth, we’re seeing some interesting numbers when it comes to their user trends. I mentioned the logged-in and logged-out breakdown they have for their users. In recent quarters, there has been a pretty decent spike in year-over-year growth and they hit about 27% but this is not a platform that is on the scale of a lot of the other social media businesses out there. I think they have about 70 million daily actives at this point. Can this break out from the very tech-literate, very future-forward audience that it tends to have and get into more of a mainstream spot? Because I know that this is one of those businesses and one of those user sites where, if you’ll love it, you’ll love it, and otherwise you maybe not even have heard of it.

Brian Feroldi: If you haven’t heard of it, you certainly don’t use it. I think that that could really provide some cap on the upside potential of this business. A big part of the thesis here, especially at the valuations they’re coming public at, it hinges on this company significantly, improving its revenue and profitability metrics over time. It is going to be awfully hard to do so if they don’t attract new users to the platform so that certainly could be a challenge. That’s one thing that we saw as a big challenge for Pinterest, the last social media network that we saw that come public, I think in 2019 or so, they really struggled to grow outside of their core user base, and I could see Reddit having the same issue.

Dylan Lewis: If we see user growth as an opportunity, what else is out there in terms of opportunities for this business to grow and hit the scale that I think it probably needs to in order to be profitable?

Brian Feroldi: This company calls out a handful of ways that it could continue to meaningfully grow. One thing that surprised me about the platform is even though it’s nearly 20 years old, 90% of the content on this platform is in English, so there is a huge opportunity for them to penetrate international markets simply by making their platform more friendly to people whose native tongue is not English. Another thing they called out is video.

We’ve seen this as a trend among all the social media platforms where they’re trying to compete against TikTok, and one way they’d do that is really promoting users to share video on their platform as opposed to being just text-based. An interesting category that they called out is that they believe that data licensing and AI training could become a massive opportunity for this company. We’ve seen an explosion in interest, in all things related to AI, and Reddit certainly has a treasure trove of data for AIs to scrape through and build models around.

Now that is a nascent part of the business today, but management believes that it could be a big contributor over time. Finally, they are interested in growing a contributor program and building up a marketplace to allow their users to sell products and services to each other. On the contributor front, they might even get into the fact of paying their users to post, as we’ve seen on X slash Twitter recently, and YouTube and Instagram have been doing so. If they get into that, if there’s a way to make money for, that could attract new users to the platform.

Dylan Lewis: We’ve talked a little bit about where they fit into the overall social landscape. I think one of the big questions for me and one of the big risks for me looking at its business is, is it more in the lane of a Twitter or X? Or is it more in the lane of a Meta? Is it a business that can find users outside of its core group? Also, is it a business that can effectively monetize in a way that doesn’t bother its core users? I don’t have a good answer to that. Other than to say, I have my doubts. I think generally what we tend to see when companies come public is an increased focus on monetization and increased focus on extracting more value from the time that people spend online. Brian, I think one of the big risks I look at what this business is are the moves that they’re going to make to become more profitable, going to make the experience materially worse for an audience that’s very vocal, very tech forward, and very willing to hop to other platforms at times?

Brian Feroldi: That to me is also the key question and the key risk for investors to think about. To your point, when a company goes from being private to being public, the culture of that business changes. For the first time, the management team has a number over their head that they have to hit every 90 days, and that pressure changes the culture up and down the organization. They may have to start stuffing more ads down users’ throats, and it’s going to be interesting to see if the users, accept that, or if they rebel. I think you bring up an excellent point. Anecdotally, the people I know that our Reddit users tend to be young, extremely tech savvy, and also have ad blockers up on their systems. So I could see this company having a hard time monetizing its user base.

Dylan Lewis: I think one of the other things that comes to mind for me as a risk with this business is the pecking order in digital ad spend. We have seen broadly when ad budgets start to tighten up, the major players, the YouTubes, the Facebooks, and the Metas feel a pinch, but the budget stays with them. I think right now Reddit lives in the same lane as Snap, probably Twitter or X and places like Pinterest, where it’s nice to have for a lot of ad budgets but they still need to be convinced that the dollars are going to come back to them. It’s probably one of the first places that people are willing to cut when times get tough.

Brian Feroldi: You just hit the nail on the head. When you’re an advertiser, you are going to try and put your dollars behind the place that had the highest return on your investment. Meta and [Alphabet‘s] Google are two fabulous platforms for advertisers to earn a very strong return on their investment. Reddit has the opportunity to offer a differentiated user base. If they can build out the tools, it’s possible that they could continuously peel out that away. Also, the advertising market is just massive, it’s a trillion dollar market. Even if this company only gets to a few percent market share, that could still be a big opportunity. Of course, it’s also been around for almost 20 years now and it hasn’t even come close to hitting that 1% market share. Perhaps that shows the core business itself is going to have a hard time doing so.

Dylan Lewis: All right, Brian, putting all this together, we have worked our way out of the IPO winter, so to speak. We’ve had some big names come public like Cava. But the market is always hungry for new names, always looking for new businesses. As this one comes public, is this one that you’re interested in.

Brian Feroldi: You have to channel my inner Jim Gillies here. I would be interested in this company at the right price. I never buy IPOs, and I was burned a couple of years ago by being super interested in bullish on Pinterest when it came public, and that company has really struggled on the public market. If the numbers that we see are to be believed, this company’s becoming public at a valuation of about 8X sales or 10 times gross profit. That’s not extreme, but we don’t know what the first-day pop is going to be for this business. At the right price, I might be interested, but I never buy IPOs. I give them at least a year to see how they actually perform. But if this company outperforms expectation and comes on the right price, I could see myself taking a position.

Dylan Lewis: Since you mentioned Pinterest, I do want to walk through what the cautionary tale there looks like. What was the thesis and what went wrong, and what can we learn there as we look at Reddit here?

Brian Feroldi: Pinterest was my wife’s favorite company. She used it all the time and it was a social media platform that had a lot of positives to it. A core, a user base, a very friendly platform. It was a natural place to go from being a core lurker to someone that would make a purchase. That was very much what the platform was about. What they struggled with was growing the user base and then increasing their average revenue per user. A big part of the thesis was, there were like one-tenth of the rate that Facebook was, and if they can just get to a third of the rate of Facebook, that would lead to tremendous upside growth. They’ve made some progress on that front, but it hasn’t been as easy as I assumed it was going to be. I could very much see Reddit having that same promise, but also having that same struggle.

Dylan Lewis: Brian Feroldi, thanks so much for joining me today and talk me through this prospectus.

Brian Feroldi: Always a pleasure to be here Dylan.

Dylan Lewis: Listeners, if you’ve got a company you want us to do a 15-minute Dive Into, let us know. Write in at [email protected]. Coming up next, Emily Flippen and Jason Moser return with a couple of stocks on their radar. Stay right here. You’re listening to Motley Fool Money. As always, people on the program may have interest in the stocks they talk about and the Motley Fool may have formal recommendations for or against. Don’t buy or sell anything based solely on what you hear.

I’m Dylan Lewis, joined again by Emily Flippen and Jason Moser. We’ve got stocks on our radar coming up in a minute. But first, pour some melted ice cream out for Unilever. The consumer giant announced plans to cut 7,500 jobs and it will also be spinning out its ice cream unit, which is the home of Ben and Jerry’s. Jason, are you surprised to see Unilever moving away from ice cream and such a big brand like Ben and Jerry’s.

Jason Moser: The timing seems a little odd, hadn’t these guys heard a little thing called. Now, apparently you just take some of them, eat all the ice cream you want. I did find it interesting when you look at the ice cream space, just in regard to US market share, actually private-label is the biggest shareholder. But Ben and Jerry’s, it’s a close second, so it’s not an irrelevant business, but like he said, growth has slowed down, perhaps doesn’t fit well with the rest of Unilever’s business, so it seems like it’s on the chopping block.

Dylan Lewis: Emily, I know when I’m looking for a treat Ben and Jerry’s is where I go. I’m usually a Jerry Garcia guy. What about you?

Emily Flippen: Well, first of all, chunky monkey girl of course banana ice cream, you can’t beat it. I am concerned though, because part of the reason they’re making this spin-off is just because consumer trends have abbed away from ice cream. Whether that’d be for health reasons or otherwise, whatever was driving people to buy lots of Ben and Jerry’s is no longer driving that same growth, and I can appreciate that from a leverage perspective, but from a consumer perspective, I’m going to lose it if I don’t have access to Ben and Jerry’s. Not that I eat it, I get I’m part of the problem. I look at the calories on the pint and I can’t justify making that purchase, but on the rare occasion that I do, I want the junkie monkey and I think there’ll be a big hole in people’s hearts if this for some reason loses distribution as a result of its spin-off.

Brian Feroldi: [laughs] Let’s get over to stocks on our radar. Our man behind-the-glass, Rick Engdahl, is going to hit you with a question. Jason, you’re up first. What are you looking at this week?

Jason Moser: Interesting week for Topgolf Callaway Brands ticker is MODG. Earlier in the week a rumor started spreading there. Maybe some acquisition of the company. South Korean news outlet reported that there was interest in perhaps spinning off the top golf side of the business and selling the Callaway side of the business. The company [inaudible] hot over that, didn’t really commit one way or the other, but it’s an interesting thing to think about. The major shareholders apparently have selected a lead manager to explore possible deals. There’s even a rumor out there floating that PIF, the public investment fund that controls live golf, they might be interested in buying this Callaway brand business. Phil Mickelson is clearly on board with it, said, “I pray this happens. ” Rick, a question about Topgolf Callaway.

Rick Engdahl: The top golf people worried about competition from the ax throwing people because given the conflicts, I got to go with the ax throwers, although top golfers have the range, I don’t know. What do you think?

Jason Moser: Ax throwing seems like it would be a lot more fun and this is coming from a lifelong golfer Rick. Emily, what’s on your radar this week?

Emily Flippen: PDD holdings. That’s the ticker, PDD, also known as Pinduoduo, the Chinese e-commerce giant, up massively after their quarter. Temu, which is their ex China facing e-commerce app just continues to blow results out of the water. I am a shareholder of Pinduoduo, I forgot about that until I looked at my accounts recently and realize I’ve apparently made a lot of money on it, even though the mandate of the company has changed.

Dylan Lewis: All right, Rick, a question about Pinduoduo.

Rick Engdahl: First of all, I didn’t think it was real company until I had to looked it up. I had never heard of Temu before, until my daughter brought it up in a rant about fast-fashion and labor practices or something. Is there any concern about the upcoming young generation of conscious consumers out there or is this just a myth?

Emily Flippen: Certainly a lot of concern, not a business that’d be willing to recommend today, even though I have all the [inaudible] and that I do own it in my account.

Dylan Lewis: Rick, you’ve got two very different businesses here this week. Which one’s going on your watchlist?

Rick Engdahl: I think I want to see that battle between the golfers and the ax throwers. It’s going to be prime TV.

Dylan Lewis: You and me both, I’d love that. Emily Flippen and Jason Moser, thanks for being here. Rick, thanks for weighing in on our radar stocks. That’s going to do it for this week’s Motley Fool Money radio show. Show was mixed by Rick Engdahl. I’m your host, Dylan Lewis. Thanks for listening. We’ll see you next time.

In this podcast, Motley Fool host Dylan Lewis and analysts Andy Cross and Matt Argersinger discuss:

Motley Fool host Ricky Mulvey catches up with Bloomberg entertainment reporter Lucas Shaw for a look into the business of streaming, the power of incentives, and corporate infighting at Paramount.

To catch full episodes of all The Motley Fool’s free podcasts, check out our podcast center. To get started investing, check out our quick-start guide to investing in stocks. A full transcript follows the video.

This video was recorded on March 15, 2024.

Dylan Lewis: We’re entering a new era in real estate. Motley Fool money starts now.

It’s the Motley Fool Money radio show. I’m Dylan Lewis, joining me in the studio. Motley Fool Senior Analysts, Matt Argersinger, and Andy Cross. Gentlemen, great to have you both here.

Matt Argersinger: Hey, Dylan.

Andy Cross: Hey, Dylan.

Dylan Lewis: We’ve got a run-down on retail, the state of things at Paramount and of course, stocks on our radar. But we’re kicking off with real estate news, Matt, after several years and lawsuits related to excessive fees and antitrust activity, we might be looking at a new real estate market.

Matt Argersinger: We might be, Dylan, if you ever sold a home. It’s always been confounding well, at least for me, that in addition to paying a commission to your agent, in that case, the seller’s agent or the listing agent, you’d also have to pay a 2.5, 3% commission to the buyer’s agent. And this was essentially, for decades, a mandate of the National Association of Realtors, NAR, of which the vast majority of agents in the US are members of. It’s why commissions on transacting home haven’t traditionally been set in this 5-6% range, split evenly, usually by the seller’s agent and the buyer’s agent.

So instantaneously on every transaction, in addition to other closing costs, repair expenses, 5-6% of your homes’ equity would instantly, that had been built up maybe for over many years, and worth tens of thousands of dollars would instantly go away for these commissions. It always seemed like one of the final areas of the market that had yet to be disrupted. Because if you think about what’s happened to travel agents, what’s happened to brokerage commissions, certainly transacting and almost everything in the country has gotten cheaper overtime except transacting a house.

If you look at the median price of a home in the US, right around $400,000, that’s 20,000 or more in commissions just to sell a house. But here we are. The NAR has essentially settled, which means they are not contesting any more of these lawsuits, the civil action suits against them, they’re paying a fee and the idea is that they’re going to lose their monopoly position on the marketplace. Now, agents won’t be required to be members of the NAR.

They won’t be forced, for example, to subscribe to MLS listings already get paid and essentially makes real estate agents, free agents that can set their own commissions. And if you’re a home seller, or a homebuyer, gives you far more negotiating power. You can pay a commission to a buyer that you want to pay, and it’s no longer causing a mandate to pay a commission to the other side of the transaction.

Dylan Lewis: Matt, and looking at this news, I was trying to process both the news itself and then the follow-on impact that it would have. And I feel like for buyers and sellers, we’re probably looking at lower fees and a little bit more flexibility. Beyond that in the business landscape of real estate, I feel like it’s really hard to nail down what it means for companies like Zillow, Redfin, and other operators.

Matt Argersinger: I think clearly for the publicly traded agencies, this is not going to be great news. I mean, those fees are coming down, their margins have to come down. The business is going to change. There’s going to be less agents in the marketplace. For companies like Redfin and Zillow, it is a little cloudy for me, because for one, Redfin who has already trying to disrupt the whole transaction fee of this marketplace anyway and with Zillow, Zillow really depends on the vast majority of its revenue still comes from agents who pays a low for leads on their marketplace.

They need agents, and they depend on the traditional model. So for Zillow, it’s also could be disruptive, although a little confusing. I would just say this, good real estate agents do deserve to get paid. I don’t want to make it seem like these commissions were being paid out the door for nothing. I mean, many work really hard. I’ve worked with agents that had been great. They spent a lot of time working with buyers or sellers, and they deal with a lot of paperwork. There’s a lot of value to what they do. So I feel like it’s still, in a way, it makes the marketplace better for them because I think good agents will thrive. Good agents will still get paid. A lot of agents who were just living off these richly undeserved agent commissions will not thrive.

Dylan Lewis: This week we’ve also got updates in AI sending tech companies in two different directions. We’re going to kick off looking at Adobe here, Andy. Company reported earlier this week, results were good, but it seems like the guidance and the general outlook on how AI might be affecting the business has the market concerned.

Andy Cross: Yeah. Dylan, it’s like that Damocles hanging over Adobe. AI is just waiting for that string to catch, to end up doing some serious damage to this company. This is a company that’s been in investing in AI for a long time. Their Firefly solution, since its launch, now has more than 6.5 billion images created. They’re investing in this space, and they talk a lot about this. However, even though that quarter was really quite good, revenues up 11%, adjusted earnings per share up 18%. They didn’t have to pay a billion-dollar fee for the Figma transaction getting canceled. Their digital media revenue was up 12%.

Their ending annual recurring revenue, which is very important when you think about this business, up 14%. The Document Cloud business, which is part of their solutions and part of this package, was up 23%. So that’s really impressive. Their digital experience revenue, that’s their new marketing business they’ve been growing. That was up 10% with remaining performance obligations up 16%. So the quarter was all really positive, very good. However, it was all in the conversation about the guide in their future revenues, thinking about the bookings and how artificial intelligence is or is not impacting their business.

Especially it’s things like OpenAI Sora, which is their text to video creating device and how much that’s impacting, not just creating videos and imaging, but also giving clients the ability to edit those. Lots of conversations around what that means for their business. They didn’t come out very enthusiastic about the guide going forward. Lots of conversations around with the analysts about what this means after minutia at the timings at this quarter, next quarter, a lot of concerns that so much of the growth of the year is going to be back-ended into the second half.

Clearly you see the stock reacting, more down 13% as we’re going into tape this. The market clearly having some discussions and some hesitations about Adobe, which is the leader in this space. By the way, the stock has done very well over the last year. So I think the most pullback maybe a little ahead of itself and this is some of the pullback we’re seeing.

Dylan Lewis: A different story with AI over at Oracle. This is a company that is catching the tailwinds of AI. Matt shares up 10% this week following the company’s fiscal Q3 report. Thanks in large part to demand for the company’s Cloud offerings.

Matt Argersinger: Absolutely. I mean, if you look at the headlines, revenue up 7%, adjusted EPS up 16%, both better-than-expected, but the two likely reasons, and you hit one of them, the stock has been up so much. First Oracle’s remaining performance obligation, RPO, Andy mentioned this for Adobe as well. This is basically sales that Oracle is contractually obligated to fulfill, but hasn’t yet quite recognize as revenue or if you’re a simple investor like me, it’s called backlog.