“She flipped the title on his car, sold all his furniture and told us that our dad didn’t leave me or my sister anything.”

Source link

“She flipped the title on his car, sold all his furniture and told us that our dad didn’t leave me or my sister anything.”

Source link

U.S. Treasury Secretary Janet Yellen testifies during a hearing before the Financial Services and General Government Subcommittee of the House Appropriations Committee at Rayburn House Office Building on Capitol Hill on March 21, 2024 in Washington, DC.

Alex Wong | Getty Images

Treasury Secretary Janet Yellen on Wednesday warned that China is treating the global economy as a dumping ground for its cheaper clean energy products, depressing market prices and squeezing green manufacturing in the U.S.

“I am concerned about global spillovers from the excess capacity that we are seeing in China,” Yellen said during a speech at a Georgia solar company called Suniva. “China’s overcapacity distorts global prices and production patterns and hurts American firms and workers, as well as firms and workers around the world.”

China has a surplus of solar power, electric vehicles and lithium-ion batteries that it can ship out to other countries at cheaper prices. That makes it difficult for the more adolescent green manufacturing industries of the U.S. and elsewhere to compete.

Yellen said she intends to put pressure on Chinese officials about these trade practices during her upcoming visit to China.

“I plan to make it a key issue in discussions during my next trip there,” she said. “I will press my Chinese counterparts to take necessary steps to address this issue.”

The secretary’s concerns come as the White House tries to build a burgeoning clean energy industry domestically with investments from the 2022 Inflation Reduction Act, along with other legislation like the CHIPS and Science Act.

Yellen has regularly touted the gains from these investments, including at another recent speech where she doubled down on the electric vehicle “boom” spurred by the IRA.

But those investments are playing catch-up with China’s government.

“The Biden Administration also recognizes that these investments are new,” Yellen said Wednesday.

Meanwhile, China has been pouring billions into clean energy for years, outpacing the rest of the world in the energy transition.

Yellen added that the more China’s clean energy glut interferes with global market prices, the worse off supply chains for these energy sectors will be.

“President Biden is committed to doing what we can to protect our industries from unfair competition,” Yellen said.

The Chinese Embassy in Washington did not immediately respond to a request for comment.

Yellen’s comments highlight ongoing U.S.-China trade tension even as the two countries try to steady relations.

President Joe Biden met with Chinese President Xi Jinping in November as an olive-branch effort to break the ice after years of tension, marked in part by a tariff war launched by former President Donald Trump.

Trump has floated reinstating significant tariff levels on Chinese products if he wins a second presidential term.

In the time since the Biden-Xi meeting, strengthening U.S.-China relations has proven a precarious effort due to ongoing cybersecurity and trade concerns.

In February, Biden launched an investigation into Chinese smart cars, which he said pose a national security risk because they connect to U.S. infrastructure when they drive on American roads.

“China is determined to dominate the future of the auto market, including by using unfair practices,” Biden said in a February statement. “China’s policies could flood our market with its vehicles, posing risks to our national security. I’m not going to let that happen on my watch.”

Carnival Corp.’s stock dropped Wednesday after the cruise operator reported an narrower-than-expected fiscal first-quarter loss but also provided an estimate for what the collapse of the Francis Scott Key Bridge in Baltimore would cost it this year.

Source link

Social Security offers a vital financial safety net and a cornerstone in the foundation for a secure future for millions of Americans. What happens, though, if your employment history doesn’t support those plans?

If your spouse is eligible to receive retirement benefits, you may qualify for spousal benefits. You’ll need to check the rules and regulations from the Social Security Administration (SSA) to determine if you meet the requirements but can begin your research with the following summary of the major ways you can qualify for spousal benefits.

Image source: Getty Images.

The good news is that you don’t necessarily need your own work history to receive spousal benefits. Ways to qualify include reaching age 62 or caring for a qualified disabled child under age 16. The child also must be eligible for benefits on your spouse’s Social Security record.

You also may be able to make a claim on an ex-spouse’s work record if you’re 62 or older, were married at least 10 years, divorced for at least two, and currently unmarried.

There are a few additional factors to keep in mind. First, if you remarry after you become eligible for divorced spousal benefits, you’ll lose those benefits. (But you can reapply if you later become single again.) In any case, the amount of your spousal benefit will depend on your spouse’s earnings history and when you start collecting benefits.

Generally, you can receive up to 50% of your spouse’s full retirement benefit. However, if you start receiving benefits before your full retirement age, your benefit will be permanently reduced. The SSA offers an online tool for estimating your potential spousal benefit.

Knowing these eligibility requirements can help you and your spouse plan your retirement strategy. If you’re the lower earner in the marriage, you may want to delay taking your own retirement benefits until you reach your full retirement age to maximize your potential spousal benefit.

You can estimate your retirement benefit and investigate various claiming situations, including spousal benefits, using the SSA’s online benefits planner. The planner also is a good aid for understanding some of the complexities involved in making educated decisions about your retirement income.

Spousal benefits can be a significant source of income for retirees. By understanding the eligibility requirements and how different claiming strategies can affect your benefit amount, you and your spouse can work together to maximize your retirement income. The same goes for your ex-spouse.

For more detailed information on spousal benefits and claiming strategies, visit the Social Security Administration’s website. Consulting with a financial planning advisor who understands both Social Security and how your benefits will fit in with the eggs already in your nest is also a good idea.

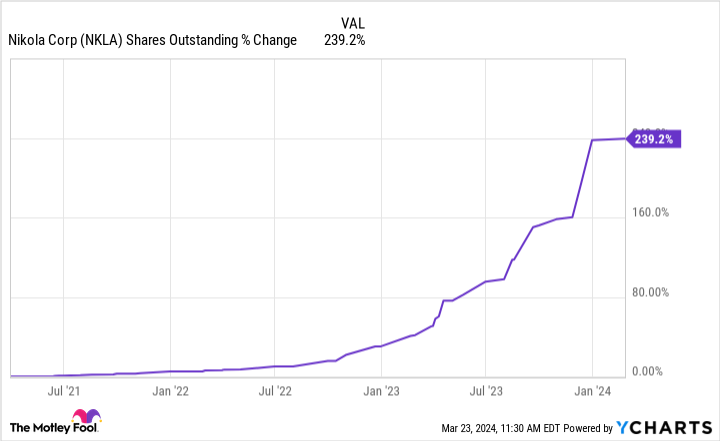

Driving almost 24% lower since the start of the year, Nikola (NASDAQ: NKLA) has failed to keep pace with the S&P 500, which has risen almost 10%. Enthusiasm for the battery truck manufacturer has powered down considerably from where it was several years ago when the stock made its debut on the public markets.

The company encountered several bumps in the road, and the market has punished the stock recently, but that doesn’t mean the shares can’t reverse the trend and head higher. Many optimists believe now’s a great time to add the electric-vehicle (EV) stock to their portfolios.

Let’s take a closer look at both arguments to get a better sense of whether picking up shares now is a smart move.

For pessimists, the company’s flagging financial health is at the core of their concern. In 2023, Nikola reported revenue of $35.8 million, a 28% year-over-year decline. Towards the bottom of the income statement, Nikola reported earnings before interest, taxes, depreciation, and amortization (EBITDA) of negative $752.7 million, a steeper loss than the negative EBITDA of $698 million reported in 2022.

Critics will be quick to point out that Nikola’s financials pale in comparison to the company’s projection of where it would be at this time. In a 2020 investor presentation, Nikola forecast 2023 revenue and EBITDA of $1.4 billion and negative $66 million, respectively.

Further powering the bears’ concerns is the prospect of shareholder dilution. Incurring steep losses over the past few years, Nikola has resorted to raising capital through the issuance of equity to help keep the lights on.

Besides the financials, bears are pumping the brakes on Nikola stock as competition continues to ramp up. While the company has floundered in achieving the growth it had imagined over the past few years, electric-trucking peers show no signs of slowing down.

Tesla represents a familiar and formidable foe with its Semi battery-electric truck. In Nevada, Tesla is developing a Gigafactory, which the company recognizes as its “first high-volume Semi factory.”

Meanwhile, Daimler Truck also is challenging Nikola’s progress. In 2023, it reported electric-truck deliveries of 3,443. Nikola, on the other hand, shipped 114 trucks to customers.

Rather than dwell on Nikola’s challenges, optimists are firm in their beliefs that the road ahead for the company is a lot smoother than its recent path. Bulls believe that the gap between the company’s estimate of where it’d be now versus where it actually is now stems from the deceit of the company’s founder, Trevor Milton, who was convicted of securities fraud in December.

Now at the helm is Steven Girsky, who had served in several leadership positions for General Motors, including vice chairman and president of GM Europe. Optimists have more faith that Girsky will be more adept at steering the company in the right direction.

Bulls are also enthusiastic about Nikola’s projections for 2024. While the company’s financial performance in 2023 left much to be desired, management’s outlook for this year is encouraging.

At the top of the income statement, management estimates that truck sales will deliver revenue of $150 million to $170 million (significantly higher than in 2023). When it comes to profitability, management thinks the company’s gross margin will narrow considerably, from negative 597% in 2023 to negative 100% to negative 80% in 2024.

Already, the company is off to some success in 2024, fueling the hopes of Nikola enthusiasts. In February, it announced the opening of its first hydrogen refueling station in Southern California. Nikola has high aspirations for these Hyla-branded refueling stations that will meet the demands of both its hydrogen fuel cell electric trucks, as well as drivers of other Class 8 hydrogen trucks.

By the end of 2024, Nikola hopes to have 14 refueling stations of this sort in operation.

Both bulls and bears make valid arguments regarding the buy case for Nikola. Ultimately, investors will have to decide for themselves whether it’s the right time to park Nikola stock in their portfolios. However, it’s critical that prospective buyers know the considerable risks of an investment.

There’s no guarantee that the company will achieve its 2024 projections. If it does, there’s no assurance it will extend further growth in 2025. For the majority of investors, therefore, the most prudent course of action is to watch this story continue to evolve from the side of the road for the time being.

Should you invest $1,000 in Nikola right now?

Before you buy stock in Nikola, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nikola wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Tesla. The Motley Fool recommends General Motors and recommends the following options: long January 2025 $25 calls on General Motors. The Motley Fool has a disclosure policy.

Is Nikola Stock a Buy? was originally published by The Motley Fool

Mortgage applications dipped 0.7% in the last week, the Mortgage Bankers Association said. The average rate for a 30-year mortgage is 6.93%.

Source link

2024 Ford Mustang

Source: Ford

DETROIT — Ford Motor sees opportunity to grow Mustang sales as it becomes the last American muscle car with a traditional V8 engine, playing to generations of gearheads who’ve been drawn to the performance vehicles.

The optimism comes after Mustang’s closest American competitors ended production of their muscle cars in December. General Motors stopped producing the Chevrolet Camaro, and Stellantis ended production of its Dodge Challenger V8 ahead of a new all-electric muscle car later this year, followed by gas-powered models with twin-turbo, inline-six engines that are expected in 2025.

Their exodus (and that of others in the muscle car market) is the result of changing consumer demand away from two-door cars, as well as tightening fuel economy standards and the emergence of all-electric vehicles capable of unrivaled acceleration.

Jeff Marentic, general manager of Ford Blue products, which includes the Mustang, said the pony car remains good business for the automaker both domestically and internationally. Mustang marks its 60th anniversary on April 17.

“We’re excited to continue to offer Mustang. It’s sad to see competition leaving but that’s beneficial to us,” Marentic told CNBC. “For people who are looking for a true American sports car, it’s available to them. … We’re looking and talking about the future of Mustang, and how far we can grow it.”

Ford Chair Bill Ford and President and CEO Jim Farley converse in front of newly revealed Mustang Dark Horse at The Stampede in downtown Detroit on Sept. 14, 2022.

Ford

Marentic declined to discuss specific sales expectations for the vehicle but noted the company has added a new V8 model for the seventh-generation vehicle called the Dark Horse — a not so subtle reference to Ford’s ambitions for the V8-powered car.

Both the 2024 Dark Horse and Mustang GT are powered by a 5.0-liter V8 engine, with the new model generating up to 500 horsepower and 418 foot-pounds of torque. Ford also has announced a 2025 Mustang GTD with a supercharged 5.2-liter V8 engine that’s expected to arrive as early as later this year with more than 800 horsepower.

Ford has been able to continue to sell Mustang V8 models in part because it has invested in making the vehicles more efficient and it was early to adopt smaller, turbocharged four-cylinder engines that now make up about 48% of Mustang sales in the U.S.

Ford also offers an all-electric Mustang Mach-E crossover that features similar design cues and badging to the two-door coupe, but it shares little to no other characteristics other than the name.

“I can understand the green movement, but we’re so proud of our V8s,” Marentic said, adding the model accounts for a majority of Mustang sales in Europe. “It helps define who Ford is outside of the United States.”

The Ford Mustang Mach-E is presented at the New York International Auto Show, Manhattan, New York, April 5, 2023.

David Dee Delgado | Reuters

The seventh-generation Mustang, which Ford revealed in September, recently started shipping outside of North America. It will eventually be sold in 85 markets on every continent aside from Antarctica, according to Ford.

Non-U.S. sales have assisted in keeping the Mustang, which is exclusively produced at a plant in metropolitan Detroit, in production amid declining domestic demand for two-door sports cars.

U.S. sales of the Mustang have declined from a recent peak of more than 122,000 units in 2015 to fewer than 49,000 last year.

Internationally, Ford reports there have been more than 235,000 Mustangs registered since 2015. That’s when the automaker began producing right-hand drive models for countries such as the United Kingdom, Australia and Japan.

The top markets for Mustang outside of the U.S. are Canada, Australia and Europe, according to Ford.

“People relate extremely strongly to Mustang,” Marentic said. “The pull is amazing.”

Marentic declined to discuss future product plans for the Ford Mustang, including a hybrid that was reportedly canceled for the seventh-generation car or the potential for an all-electric version of the two-door vehicle.

Many people find that during their working years, housing is their largest monthly expense. But come retirement, healthcare might take the place of housing as the single expense you spend the most amount of money on.

As such, it’s in your best interest to do what you can to make your healthcare costs more manageable. Here’s how.

Image source: Getty Images.

When it comes to enrolling in Medicare, you get a choice. You could stick to original Medicare, which is Parts A, B, and D. Or as an alternative, you could sign up for a Medicare Advantage plan.

Medicare Advantage plans often cover more services (such as dental care and eye exams) than original Medicare. But that doesn’t necessarily make them a more cost-effective choice for you. You’ll have to really research your options carefully to determine which is best for you.

Also, within the realm of Medicare Advantage, there may be a large number of plans to choose from in your area. Take the time to review what those different plans cost and cover. And also, look at plan ratings to get a sense of how satisfied enrollees tend to be with them.

If you decide to stick to original Medicare, consider Medigap coverage, or supplemental insurance. This could limit the amount you’re forced to spend on expenses like coinsurance and deductibles.

Letting health issues escalate could not only put your wellbeing at risk, but also, cost you more money. As such, it’s a good idea to keep up with doctor visits and make sure you’re scheduling diagnostic tests as per your providers’ recommendations.

If you’ll be signing up for Medicare, you should also try to take advantage of the program’s free health services. Enrollees are generally entitled to a wellness visit every year. And certain diagnostic tests are available at no cost as well.

You could always tap your 401(k) or IRA in retirement if you need money to pay for healthcare expenses. But when you’re also trying to pay for housing, groceries, transportation, and at least some entertainment, dipping into your limited cash reserves for medical bills could become stressful.

That’s why it’s a great idea to have separate, dedicated savings for healthcare spending in retirement. So if you have access to an HSA, or health savings account, during your working years, do your best to fund it.

However, what you’ll also want to do is leave your HSA balance alone while you’re still working. HSAs don’t require you to spend down your plan balance every year. Quite the contrary — savers are encouraged to invest unused funds and grow their balances. So if you follow that path, you may end up with a large sum of money in retirement that’s earmarked for healthcare spending. That could take a lot of the pressure off.

Healthcare is an unavoidable expense — in retirement and in general. But if you make these moves, you may find that covering your healthcare costs isn’t as difficult once your career comes to an end.

Stocks have surged over the past few months. That rally has pushed most major stock market indexes toward their all-time highs. A big driver has been an expansion of valuation multiples. The S&P 500 currently trades at 23.5 times earnings, while the Nasdaq 100 is above 31. So bargains are few and far between.

However, several high-yield dividend stocks trade at compelling discounts right now, including Agree Realty (ADC 1.66%), Iron Mountain (IRM 2.81%), and Ryman Hospitality Properties (RHP 2.83%). Here’s why value investors should take a closer look at these income stocks.

Agree Realty is a real estate investment trust (REIT) focused on free-standing retail properties. Last year, it generated $3.95 per share of adjusted funds from operations (FFO). With shares recently trading around $56 apiece, it sells for about 14 times FFO. That’s quite a discount compared to the broader market indexes.

That lower valuation is a big reason the REIT offers such a high dividend yield. It’s at 5.3%, compared with 1.4% for the S&P 500. While REITs have higher dividend payout ratios than most other stocks, Agree Realty’s was 74% last year, which is relatively low.

One factor weighing on the REIT is its relatively slower growth rate. While it grew its adjusted FFO by 24.2% overall last year to $378 million, it was only up 3.1% on a per-share basis. That’s due to issuing stock to fund new investments; it spent $1.3 billion to expand its portfolio last year. It sees adjusted FFO per share growing by another 3% this year. While that’s lower than many investors would prefer, Agree Realty still has compelling total return potential when adding in its high-yielding dividend and multiple expansion upside as interest rates fall in the coming years.

Iron Mountain is another REIT. It focuses on secure information storage, which includes operating data centers. Those facilities are seeing surging demand, powered in part by artificial intelligence. That’s driving up the valuations of most data center REITs.

However, Iron Mountain currently trades at a discount to other REITs that operate data centers. The company expects to generate about $4.45 per share of FFO this year. With the REIT recently trading around $78.50 per share, it sells at about 17.5 times FFO. That also puts it at a nice discount compared to the broader market. Its lower valuation is a big reason its dividend yield is more than double the S&P 500’s at 3.3%.

That’s an enticing value for a company that expects to deliver accelerated growth in 2024. The company foresees its revenue growing by 10% to 12% this year, up from a 7% increase last year. Meanwhile, adjusted FFO should rise by 8% this year, an increase from 4% growth in 2023. Given the strong and growing demand for data centers, Iron Mountain could continue growing at an accelerated rate.

Ryman Hospitality Properties produced $8.09 per share of adjusted FFO last year. The hospitality REIT recently traded at less than $115 a share, putting its valuation at around 14 times its adjusted FFO. That cheap price is a big driver of its 3.8% dividend yield.

On one hand, it will probably become a bit more expensive this year, given its adjusted FFO guidance range of $7.60 to $8.20 per share, or $7.90 at the midpoint. However, a big driver of the potentially lower adjusted FFO is the near-term negative impact of capital investments. The company plans to spend $360 million to $440 million to upgrade its hotels in 2024, which will cause some disruption and impact same-store RevPAR growth.

However, those investments should pay bigger dividends in the future. It’s spending money to drive growth at its properties, including new food and beverage options, more rooms, and exciting amenities. These upgrades should enable it to generate more revenue and cash flow in the future, which it can use to pay dividends.

Despite a surging stock market, there are some interesting bargains these days. REITs Agree Realty, Iron Mountain, and Ryman Hospitality Properties trade at noticeable discounts to the broader market indexes. That’s a big reason they offer such high dividend yields. Those payouts enable investors to get paid well while they wait for the market to start valuing these REITs higher.

Matt DiLallo has positions in Iron Mountain and Ryman Hospitality Properties. The Motley Fool has positions in and recommends Iron Mountain. The Motley Fool recommends Ryman Hospitality Properties. The Motley Fool has a disclosure policy.

Krispy Kreme’s stock soared Tuesday, after the doughnut seller said its doughnuts will start becoming available at all of the fast-food giant’s U.S. restaurants.

Source link