Burns, about to play in March Madness’ Sweet Sixteen, says, ‘I’m gonna be honest, I can’t eat what’s in my vending machines’

Source link

Burns, about to play in March Madness’ Sweet Sixteen, says, ‘I’m gonna be honest, I can’t eat what’s in my vending machines’

Source link

With home affordability near its lowest level in over 40 years because of high mortgage rates and home prices, being able to purchase a home for $1 might seem impossible.

However, the city of Baltimore is offering a deal intended to attract new homebuyers. It’s practically giving away houses.

An estimated 13,000 homes in Baltimore are vacant with the city owning about 1,000 of them.

Don’t Miss:

For now, 200 of these properties have been approved to be marketed to Baltimore residents who commit to both living in and fixing up the properties, with city officials saying properties in the program are in the city’s most “stressed” housing markets.

The program was approved despite objections from City Council President Nick Mosby, who said that the new policy left him “deeply concerned.”

“If affordability and affordable home ownership and equity and all of the nice words we like to use are really at the core competency as it relates to property disposition, this is a really bad policy … because it doesn’t protect or prioritize the rights of folks in these communities,” Mosby said.

Other city officials pushed back on the characterization, pointing out that there is a 90-day window that gives Baltimore locals the right to buy before outsiders are allowed to make bids.

Trending: Fortnite’s creator company greenlights partial ownership for investors in the upcoming series.

It’s worth noting that the $1 deal isn’t available to everyone — just individual buyers and community land trusts. Still, developers would only have to pay $3,000, leading to possible opportunities for large profits if home values in the areas increase.

While the chance to get a home for $1 might sound like anyone could participate in the city’s offerings, a prospective buyer needs to be able to afford the costs to make many of these vacant homes safe to live in.

To help contribute to the initiative, the city is also giving out home-repair grants of up to $50,000 to individuals who prequalify for a construction loan.

Resident Maurice Brock warned of the dangers from these properties, telling WJZ-TV in Baltimore, “There are so many risks and hazards associated with these vacant properties … it’s a definite safety risk for citizens, for city employees and firefighters.”

Given that the city of Baltimore regularly ranks in the top five U.S. cities for violent crime, safety concerns are valid, especially as these properties are already in some of the toughest areas of the city.

Prospective homeowners or investors looking to invest in real estate without the headache of owning the actual property can consider purchasing real estate investment trust (REIT) stocks or buying into a fund such as the Vanguard Real Estate Index Fund ETF (NYSE:VNQ), which invests in a diversified basket of REITs.

Read More:

“ACTIVE INVESTORS’ SECRET WEAPON” Supercharge Your Stock Market Game with the #1 “news & everything else” trading tool: Benzinga Pro – Click here to start Your 14-Day Trial Now!

Get the latest stock analysis from Benzinga?

This article This American City Is Offering $1 Homes In Its Crime-Filled Neighborhoods, Sparking Concerns of Gentrification And Violence originally appeared on Benzinga.com

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Why gold-mining stocks look set to outperform physical gold.

Source link

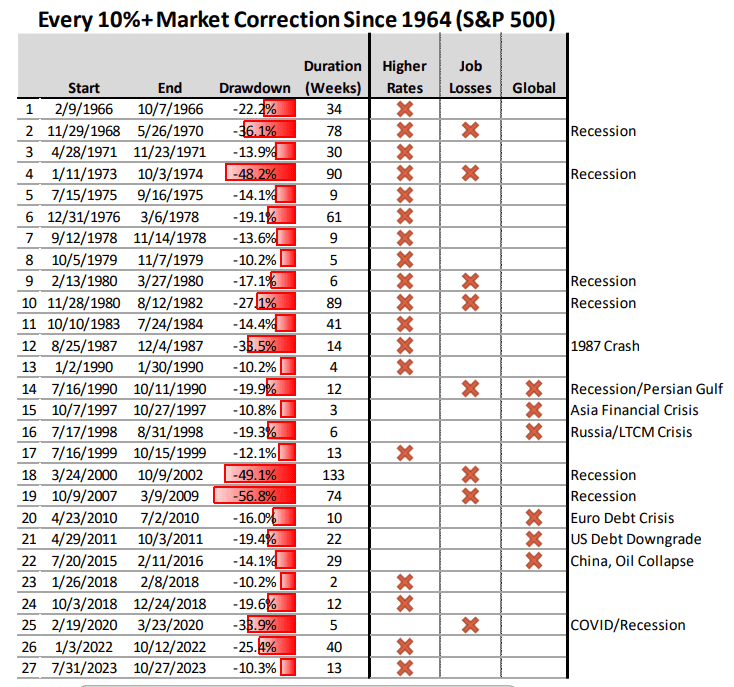

The S&P 500 has marched higher by nearly 30% over the past five months, prompting even bullish market strategists to entertain, or even welcome, the prospect of a “healthy” correction.

But typically market corrections don’t just happen — they need some kind of catalyst to set them in motion. To try and glean some insight into what might trigger the next double-digit pullback, a team of investment strategists led by Piper Sandler’s Michael Kantrowitz examined the 27 corrections of 10% or more for the S&P 500 that have occurred since 1964.

The team found that, without exception, each of these selloffs has been primarily driven by one of three things: rising unemployment, rising bond yields or some kind of global exogenous shock. Sometimes, it has been a combination, as was the case during the two equity-market corrections that occurred during 1980.

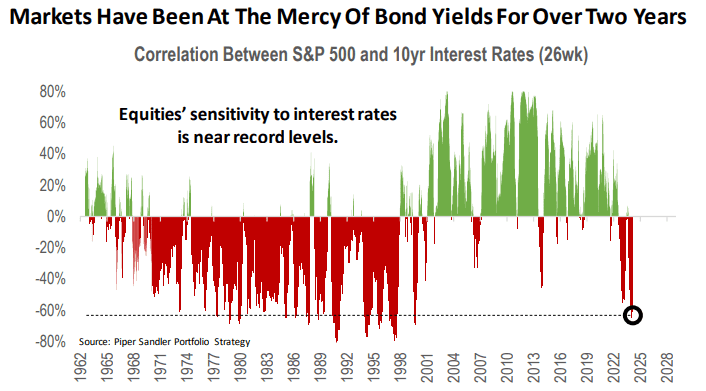

So, which is most likely to trigger the next 10% correction? According to Kantrowitz and his team, rising yields are the biggest threat to tranquil markets. Rising yields also caused the most recent correction, which ended on Oct. 27 with the S&P 500 down 10.3%.

Over the past two years, equities’ sensitivity to higher yields has reached near-record levels last seen near the peak of the dot-com bubble on a rolling 26-week basis. This suggests stocks could still react negatively if long-term bond yields continue to climb, even though equities have been largely immune to the rebound in yields since the start of 2024.

“We’ve written a lot about how rate-sensitive equity markets are today. As such, the biggest risk that we see to equities in 2024 would be a rise in rates,” Kantrowitz and his team wrote.

Because of this, a modest rise in unemployment could actually help keep the rally going by guarding against higher yields. Bond yields, which move inversely to prices, often fall when the economy weakens as demand for defensive assets like bonds increases.

Stocks sold off for three straight months between August and October last year as Treasury yields pushed higher. The nadir of the selloff occurred just a few days after the 10-year Treasury yield peaked north of 5%, a 16-year high, according to FactSet data.

Treasury yields are creeping higher once again during the first quarter. But expectations that still-robust economic growth could help boost corporate earnings have helped to shield stocks, at least so far.

The yield on the 10-year Treasury note BX:TMUBMUSD10Y has gained 39 basis points since the beginning of the year to 4.252%, while the S&P 500 SPX has risen 9.4% since the beginning of the quarter and 26.7% since Oct. 27 to close at 5,218.19 on Monday.

The Nasdaq Composite COMP is up 9.6% since the beginning of the first quarter at 16,452.69 as of Tuesday’s close, while the Dow Jones Industrial Average DJIA has gained 1,670.79 points, or 4.5%, to 39,388.56.

The shipping container is a logistics marvel that can affordably move thousands of items from hundreds of different companies all around the globe.

If there is a slowdown in shipping-container circulation, there could be massive supply chain bottlenecks.

“The skill involved in containerization is moving that container from point A to point B and getting it back to point A as quickly and efficiently as you possibly can,” Simon Heaney, senior manager of container research at Drewry, a maritime research and consulting firm, told CNBC.

Disruptions to global trade can have major impacts on shortages and inflation, causing serious ramifications for American households and businesses.

For example, the Federal Reserve Bank of San Francisco found that supply chain disruptions “contributed on average about 60% of the run-up of U.S. inflation” in the two years following the coronavirus pandemic outbreak.

“People suddenly realized how important that container is to everybody’s standard of living,” John Fossey, senior analyst of container equipment at Drewry, told CNBC.

Indeed, inflation cooled alongside the bounce back of the supply chain, according to a White House analysis of the U.S. economy. The study showed more than 80% of recent progress in lowering inflation can be attributed to the supply chain.

Attacks by Iran-backed Houthi militants on ships traveling through the Red Sea have also led ocean carriers to take longer voyages around the Cape of Good Hope.

“Taking the long way [around] the bottom of Africa, that’s adding about one-third to their voyage distance,” John McCown, nonresident senior fellow at the Center for Maritime Strategy, told CNBC.

Longer voyages result in higher fuel costs for ocean carriers and late arrivals of shipments to their planned destinations, contributing to delays in returning containers to nations like China to be reloaded with exports.

China is a world leader in exports and manufacturing, and accounts for more than 95% of shipping-container production, according to the Federal Maritime Commission.

“Particularly with the Asian countries, [they] long ago recognized that a very key part of [their] economy is exports, and if [they] want to be efficient at exporting products, [they] need to make sure there is a good conveyance system,” McCown said.

Attacks on ships in the Red Sea are the latest shock to the global supply chain after Russia’s invasion of Ukraine and the coronavirus pandemic shook up the logistics industry — including shipping container availability.

“During the pandemic, we had the phenomenon that there were not enough containers because many containers were stuck in rail yards or they were stuck in container ports,” Goetz Alebrand, head of ocean freight for the Americas with DHL Global Forwarding, told CNBC. “There was not the fluidity that we usually had.”

When shipping-container prices skyrocketed in 2020 and 2021, it became more lucrative for shipping companies and leasing firms to send containers back to Asia as fast as possible.

“Because of the need to replenish and reposition containers back to Asia,” Heaney said, “that container will make another sea journey back, but completely empty.”

That trend resulted in a trade imbalance that hit U.S. exports, including agricultural products. In response, some farms dumped milk in fields and plowed crops back into the soil.

“Ideally, you would have the most efficient system,” Heaney said. “The only way to make that happen is to have a completely balanced manufacturing ecosystem, and we don’t have that and we’re unlikely to have that. [It’s] an inefficiency born not of container shipping but just of the nature of the global economy.”

Watch the video above to learn more about how shipping containers enable global trade, why China dominates the shipping industry and what happens after a container shortage.

Investing in fundamentally sound stocks is a smart way to build wealth in the long run. By focusing on companies with robust and scalable business models, healthy financials, sustainable competitive advantages, and reasonable valuations, investors can enjoy significant returns over time.

The S&P 500 and the Nasdaq Composite indexes have gained nearly 32.3% and 38.9%, respectively, in the past 12 months. Despite this, there are still several attractively valued stocks that have the potential to grow rapidly in the coming years.

If you’re on the lookout for such stocks and have $500 that you won’t require for paying bills or for contingencies, then investing those funds in either Baidu (BIDU -1.89%) or Toast (TOST 2.86%) could prove to be a profitable strategy in the long run.

Baidu operates the leading search engine in China, but its shares have been struggling for the past couple of years. The company faces risks such as increasing competition, weakness in the Chinese economy, and U.S. export restrictions that are making it harder for Chinese companies to secure high-end AI GPUs. Yet, there remains much to like in the stock in the long run.

In 2024, the Chinese digital advertising market is expected to grow by 8.9% to $189 billion. Search advertising is the largest part of this market, and is forecast to reach $60.8 billion this year. Given that Baidu controls a nearly 60% share of the Chinese search engine market, it is well positioned to capture a significant portion of this opportunity.

To further strengthen its position in search advertising, Baidu has leveraged generative AI technologies and advanced natural language capabilities to develop “Ernie,” a generative AI model and chatbot. This technology has been playing a pivotal role in generating incremental revenues with improved ad targeting and bidding. Ernie is also helping advertisers articulate their requirements through a conversational interface, to optimize search and feed personalized content to ad campaigns. These initiatives have led to Baidu witnessing an increase in the number of advertisers on its platform, and also growth in their ad budget allocations.

Baidu’s cloud business is another key catalyst for the company. It expects its overall cloud business revenues to accelerate in 2024. Management has expressed confidence in its ability to improve the gross margins of its legacy enterprise cloud business and maintain the profitability of the AI cloud business in 2024. The integration of generative AI and foundational models into the cloud business has enabled Baidu to win customers and projects in the internet, technology, and education sectors.

Despite these growth drivers, Baidu is currently trading at only 2 times trailing 12-month sales, even lower than its five-year average price-to-sales ratio of 3.07. The market currently has a pessimistic view of the stock that does not seem justified.

Hence, considering the multiple secular tailwinds driving the business and its cheap valuation, there is a high possibility that the stock will make a solid comeback in the coming years.

Toast offers a comprehensive cloud-based software-as-a-service platform to help restaurants streamline activities including online ordering, logistics management for food delivery, accounting, marketing, and loyalty programs — thereby enhancing their operations and boosting their growth potential.

Toast’s offerings are being rapidly adopted in the restaurant industry thanks to its competitive advantages, including an all-in-one platform, localized go-to-market strategy, and the consistently solid performances of its sales and marketing teams. The company added a net 6,500 restaurant locations in the fourth quarter and ended 2023 with approximately 106,000 locations, up 34% on a year-over-year basis.

Currently, there are 860,000 restaurant locations in the U.S. and 22 million locations in the world. Toast has estimated its U.S. target addressable market to be $55 billion, and the global target addressable market to be $110 billion. Given that its annual recurring revenue is just $1.2 billion, there is still a massive runway of possible growth ahead for the company. While high-value full-service restaurants have been the foundation of Toast’s success, the company is also seeing significant traction in other areas such as small and medium-sized businesses (SMBs), mid-market enterprise and international segments, and restaurant retail.

Toast has also been successful in efficiently acquiring new SMB customers through referrals and inbound leads in markets where it already has a higher penetration rate (over 20% SMB market share in that area). It describes those areas as “flywheel markets.” In 2023, Toast almost doubled the number of its flywheel markets, and nearly 30% of the company’s markets are now in that category. These flywheel markets should continue to help boost the company’s revenues and margins.

Toast is not yet profitable on a GAAP basis. However, it is moving in the right direction. In 2023, it reported a net loss of $36 million, a significant improvement from its $99 million loss in 2022. The company also delivered a free cash flow of $93 million in 2023.

Analysts expect Toast’s revenues to grow 25% to $4.8 billion in 2024. Despite this, the company is trading at only 3.3 times trailing 12-month sales, even lower than its 3-year average price-to-sales ratio of 4.9.

Considering all these points, Toast could soar in the coming years.

Every long-term investor should have some financial stocks in their portfolio. Why? Managing money is a multi-trillion-dollar industry.

There is something for every investor in finance. Want to invest in high-growth emerging markets? Check. Want some blue-chip stocks that will pay you dividends? No problem. No matter how you slice it, there is a path to building wealth that can help you retire a millionaire.

Here are five stocks to dig deeper into that I’ve picked for their strong fundamentals and long-term potential.

More than 660 million people live in Latin America, and many still lack access to essential banking services. Nu Holdings (NU 0.49%) is helping change that. It’s a digital bank, which means it doesn’t have physical branches. As long as you have internet access, you can bank with Nu. The company operates primarily in Brazil, Mexico, and Colombia, with 95 million members today.

Members are increasing, and the company’s cross-selling of different banking, insurance, and investment products is fueling strong profit growth. The company’s net income was $361 million in Q4, up from just $58 million a year prior. With profitable growth and expansion, Nu Holdings could add a spark to any long-term portfolio over the coming decades.

Many assume Latin American e-commerce giant MercadoLibre (MELI -0.81%) is a one-trick pony, but that couldn’t be further from the truth. MercadoLibre’s fintech unit, Mercado Pago, could be the company’s crown jewel. In Q4, it had 53 million unique fintech users, up 22% year-over-year. Users can bank, borrow, and invest with Mercado Pago.

Investors may like that MercadoLibre is much more than a fintech company. Its e-commerce, logistics, and advertising units give the business a diverse revenue base. Total revenue grew 37% in 2023, so there’s still a lot of potential investment upside if the company can maintain its torrid pace.

Legendary investor and billionaire Warren Buffett can’t invest your money for you, but buying stock in his holding company Berkshire Hathaway (BRK.A 0.47%) (BRK.B 0.40%) is the next closest thing. His company holds a variety of private and publicly traded businesses, spanning insurance, energy, railroads, and more. Collectively, Berkshire is a financial fortress. The company’s many businesses provide stable and diverse revenue streams, and the company is sitting on a whopping $167 billion in cash.

That means investors can rest easy knowing the company is built to last. Its $370 billion investment portfolio is flush with blue-chip stocks that continue to grow and pay dividends that pile up on Berkshire Hathaway’s balance sheet. It’s not just safety investors get with this stock; the shares have also trounced the broader market over time. There’s a lot to like here.

Mega-bank Bank of America (BAC 0.62%) is among the most significant holdings in Buffett’s portfolio at Berkshire Hathaway. Buffett bought shares in 2007, then sold them, but bought them back in 2017. Banks like Bank of America are arguably too big to fail if the 2008-2009 financial crisis proved anything to investors. In other words, their failure would cause catastrophic damage to the financial system, and so the government provides them with a backstop.

Buffett has Bank of America as Berkshire’s second-largest position today. The company grows with the U.S. economy and pays investors a solid dividend that yields 2.6% today. There’s always the risk of another economic catastrophe, which threatens all banks. But ultimately, it’s hard to deny Bank of America as a banking blue-chip investors can confidently buy and hold.

Real estate is one of the world’s oldest wealth-builders. Real estate investment trusts (REITs) like Public Storage (PSA -0.18%) enable investors to benefit from real estate without owning buildings. REITs must pay at least 90% of their taxable income, making them great dividend stocks. Public Storage yields 4.3% at its current share price. The company owns more than 3,000 properties across the U.S.

What’s excellent about Public Storage is that it can raise rent on units over time, which builds revenue growth into its business model. The industry is projected to grow by more than 7.5% annually through 2027, which bodes well for the company. Investors can buy and hold this blue chip, as real estate never goes out of style for long.

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bank of America, Berkshire Hathaway, and MercadoLibre. The Motley Fool recommends Nu. The Motley Fool has a disclosure policy.

Nvidia (NVDA -0.17%) has been one of the market’s hottest chip stocks. The chipmaker was originally known for making gaming GPUs, but the rapid expansion of the artificial intelligence (AI) market over the past few years drove more companies to purchase its high-end data center GPUs to process complex AI tasks.

Nvidia’s rally of more than 2,000% over the past five years boosted its market cap to $2.4 trillion and minted a lot of millionaires. But it’s also driving more investors to search for the next big chipmaker that could follow Nvidia’s footsteps.

Image source: Micron.

Could that chipmaker be Micron (MU 2.32%), one of the world’s top producers of DRAM and NAND memory chips? Let’s review the key differences between Micron and Nvidia to see if Micron has a shot at replicating Nvidia’s gains.

Micron designs its memory chips and manufactures them at its own foundries. That makes it different from Nvidia, which designs its chips but outsources its production to third-party foundries like Samsung and Taiwan Semiconductor Manufacturing Company. Micron operates that capital-intensive model at much lower margins than Nvidia.

Data source: YCharts

Micron’s memory chips also cost a lot less than Nvidia’s GPUs, and it doesn’t dominate its core markets in the same way as Nvidia. Micron is the world’s third-largest supplier of DRAM chips and the fifth-largest supplier of NAND chips, but Nvidia is the leading producer of discrete GPUs by a wide margin. According to JPR, Nvidia controlled 80% of the market at the end of 2023, while AMD only held a 19% share.

Compared to Nvidia, Micron operates in a more commoditized market, has less pricing power against its competitors, and is more exposed to cyclical downturns as the memory chip market goes through its boom-and-bust cycles. However, Micron still produces denser and more power-efficient DRAM and NAND chips than its two largest competitors, Samsung and SK Hynix. That technological edge helps Micron lock in producers of higher-end PCs, mobile devices, and servers.

Micron endured a rough slowdown over the past two years as personal computer (PC) shipments declined in a post-pandemic market, the 5G upgrade cycle ended, and the macro headwinds curbed its chip sales to the enterprise and industrial markets. The Chinese government also barred its key infrastructure providers from buying Micron’s memory chips. All of those challenges offset its stronger growth in the automotive and AI markets.

Micron’s revenue grew 29% in fiscal 2021 (which ended in September 2020), but only rose 11% in fiscal 2022 and tumbled 49% in fiscal 2023. However, analysts expect its revenue to rise 56% in fiscal 2024 and 43% in fiscal 2025 as three tailwinds kick in. First, the PC and smartphone markets should gradually stabilize. Second, it should sell more chips to the enterprise, industrial, and automotive markets as the macro environment warms up again.

Lastly, the explosive growth of the generative AI market will drive more data centers to upgrade their memory chips alongside Nvidia’s GPUs. During Micron’s latest conference call, CEO Sanjay Mehrotra said the memory chip market was still in “the very early innings of a multiyear growth phase driven by AI” and that those technologies would transform “every aspect of business and society.” As an example, Mehrotra predicted that AI-enabled phones would “carry 50% to 100% greater DRAM content compared to non-AI flagship phones today.”

That’s a bright outlook, but Micron’s new growth cycle will still likely end in a few years. That’s because companies drive up memory prices by buying a lot of chips when a certain market — like smartphones, cloud data centers, and AI — runs hot.

In response, Micron and its peers usually ramp up their production of new chips to satisfy that demand. But once the hot market cools, the chip shortage quickly turns into a supply glut as companies are left with an excess inventory of chips. That’s why Micron’s chip sales fell in 2019 and 2022 — and why they’ll likely drop again once the AI market matures.

This next growth cycle could last a lot longer than previous ones, but it will eventually end in a downturn. Nvidia will also face a similar slowdown, but its cyclical declines have been much milder than Micron’s over the past decade. That’s because Nvidia’s dominance of the discrete GPU market grants it more pricing power during market downturns — while Micron remains heavily exposed to the price cuts at its larger competitors.

Micron’s stock trades at less than 4 times next year’s sales, and it could run higher as its next growth cycle begins. If its valuations hold steady and it grows its revenue at a CAGR of 30% over the next five years, its stock could nearly quadruple. That would be an impressive gain, but it could end in a cyclical downturn and won’t come close to replicating Nvidia’s gains over the past five years. Simply put, Micron is still a promising semiconductor play — but it’s probably not the next Nvidia.

Leo Sun has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

(Bloomberg) — BlackRock Inc. Chief Executive Officer Larry Fink said the US public debt situation “is more urgent than I can ever remember” and that the country needs to adopt policies to spur economic growth.

Most Read from Bloomberg

The nation can’t rely on taxes and spending cuts to get the problem under control, Fink wrote in his annual letter Tuesday. He raised the prospect of a “bad scenario” akin to Japan’s economy in the late 1990s and early 2000s, which led to a period of austerity and stagnation.

“A high-debt America would also be one where it’s much harder to fight inflation since monetary policymakers could not raise rates without dramatically adding to an already unsustainable debt-servicing bill,” said Fink, 71.

The cost of servicing the debt has already ballooned, and the 3 percentage points in extra interest payments the US government now must pay on 10-year Treasuries compared with three years ago is “very dangerous,” he wrote.

“More leaders should pay attention to America’s snowballing debt,” Fink wrote, saying the US can’t take for granted that investors will continue to want to buy as much US debt. Foreign countries are building their own capital markets and are likely to invest domestically, he said.

“Is a debt crisis inevitable? No,” he wrote, calling for capital markets to help grow the economy through infrastructure investments, especially in the energy industry.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Sure, Nvidia is on fire. Its stock is up an eye-popping 1,980% over the last 5 years — meaning a $10,000 investment in 2019 would be worth a staggering $208,000 today.

But as the saying goes, past performance is no guarantee of future results. So let’s consider some alternatives to the king of AI stocks. Here are three names that I think AI-focused investors would be wise to consider.

First up is Advanced Micro Devices (NASDAQ: AMD). Granted, AMD may not have captured the same level of AI buzz as its competitor Nvidia, but the company is similarly benefiting from the AI revolution. Indeed, shares of AMD have soared 179% since January 2023.

Like Nvidia, AMD designs advanced semiconductors that can be used to train large language models. Its latest AI-focused offering is the MI300X chip, unveiled in December 2023. So far, Microsoft, OpenAI, and Meta Platforms have all expressed interest in using the chip, which offers an alternative to the current AI workhouse, Nvidia’s H100 chip.

The MI300X could help AMD secure a key foothold in the AI accelerator market, particularly considering its cost. It sells for around $10,000 to $15,000, well below the H100’s price of $40,000.

With the first deliveries of the MI300X happening right now, it will take some time to see what the demand for the chip looks like. However, AMD Chief Executive Officer (CEO) Lisa Su has expressed optimism, both for the MI300X and the overall AI market. Back in December she predicted that the market for AI chips would hit $400 billion by 2027, up from around $40 billion in 2023. If her prediction is anywhere near accurate, AMD investors will have lots to smile about in the coming years.

Next up is Oracle (NYSE: ORCL), an under-the-radar AI stock if ever there was one.

The company is probably best known for being one of the classic “tech bubble” stocks of the early 2000s. The database software giant’s stock skyrocketed during the first wave of internet adoption in the late 1990s before crashing 84% in the bear market of 2001-2003.

Nevertheless, Oracle is now back and riding high thanks to its data center business. In its most recent earnings report (for the three months ending on Feb. 29, 2024), Oracle beat expectations, highlighted by:

$13.3 billion in total revenue, up 7% year-over-year

$5.1 billion in cloud revenue, up 25% from a year ago

$2.4 billion in net income, an increase of 27% from a year earlier.

Moreover, the company raised forward guidance. Indeed, Chief Financial Officer (CFO) Safra Catz sounded a very optimistic note, saying that the company is likely to surpass its goal of $65 billion in annual revenue by 2026. Moreover, Chairman Larry Ellison highlighted that soaring spending from hyperscalers like Microsoft is moving Oracle’s needle.

In short, the AI wave is helping Oracle find its mojo once again — and investors should take note.

Last is Palantir Technologies (NYSE: PLTR), the company at the forefront of AI-driven big data analysis.

Some investors might find Palantir’s business model difficult to understand. In a nutshell, Palantir helps organizations run their operations more efficiently. The company does this through multiple AI-powered software platforms that analyze enormous data sets, recognize patterns, and offer solutions.

Financially, it’s clear Palantir is racking up wins. Its customer count, revenue, net income, and free cash flow are all growing. Moreover, the company is starting to execute a pivot toward the private sector after getting much of its early-stage revenue from government contracts.

Even now, Palantir generates more revenue from governmental entities ($1.2 billion in 2023) than from commercial customers ($1.0 billion in 2023).

However, that’s likely to change. Palantir’s commercial revenue is growing at around 20% year over year, while government revenue is growing at 14%. If that trend holds, Palantir’s commercial revenue will surpass its government revenue by 2027.

At any rate, investors shouldn’t sleep on Palantir. The company’s rapid growth means that it could become the next big name in the AI investing space.

Should you invest $1,000 in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Jake Lerch has positions in Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Meta Platforms, Microsoft, Nvidia, Oracle, and Palantir Technologies. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Forget Nvidia: Here Are 3 Other Artificial Intelligence (AI) Stocks to Buy Instead was originally published by The Motley Fool