GameStop’s stock ended Monday’s session up 15.4%, registering its largest daily percentage increase since Dec.13, 2023.

Source link

GameStop’s stock ended Monday’s session up 15.4%, registering its largest daily percentage increase since Dec.13, 2023.

Source link

The Digital World blank-check company has officially changed its name to Trump Media & Technology Group. It begins trading Tuesday with the former president’s initials as its ticker symbol.

Source link

Over the last several decades, retiring and buying a condominium in Florida has been a rite of passage for millions of Americans entering their golden years. Unfortunately, a combination of high insurance rates, high homeowners’ association fees and high interest rates is scaring off buyers and turning Florida’s once highly vaunted condominium market into a disaster zone. This has left condo owners facing a perfect storm that was unimaginable as recently as 10 years ago.

According to a recent Redfin report, Florida’s condominium market is in a state of freefall. Every indicator shows evidence of a market struggling to come to terms with a new reality. First, condo listings have increased by 30% in comparison to the same period one year ago. Another shocking aspect of the report is the extent to which prices in some of Florida’s largest markets are retreating in comparison to condominiums nationwide.

Tampa condominiums are selling for an average of 1% less ($235,000).

Miami condominiums are selling for an average of 2.5% less ($385,000).

Orlando condominiums are selling for an average of 4.8% less ($200,000).

Jacksonville condominiums are selling for an average of 6.5% less ($254,000).

More alarming is the fact that pending sales of condominiums in four of Florda’s largest markets are significantly down, or at best flat, compared to a year ago. That means Florida condos are losing their luster in the eyes of many prospective buyers.

Don’t Miss:

“Condos are sitting on the market much longer than they used to, with less interest from buyers,” Jacksonville agent Heather Kruayai said in the Redfin report.

The culprit for this rapid cooling of the Florida condominium market is a squeeze play that savvy buyers are choosing to steer clear of. First, Florida has the highest homeowner insurance premiums in the country, with the average Floridian paying an estimated three times more than the nationwide average. Second, the only expense rising faster than the insurance premiums are homeowners association (HOA) fees on many Florida condominiums.

Since the collapse of the Surfside Towers in 2021, many Florida condominium communities have been dramatically raising HOA fees to cover both the cost of rising group premiums and assessments for needed maintenance. That’s assuming HOAs can find an insurer willing to write a policy for the community. In many cases, insurers will only cover communities after they make numerous (and costly) repairs or upgrades to existing facilities.

Orlando-based Redfin agent Juan Castro summed up the problem, saying, “Condo costs are shocking. Condos that used to have a $400 monthly maintenance fee may now have a $700 fee. It’s causing buyers to rethink their plans.” Failure to pay HOA fees can lead to foreclosure, which is why buyers are taking a hard look at the numbers and offering less for Florida condominiums. Many are avoiding the Florida condo market entirely.

The most brutal irony of all is that despite Florida condominium prices being down compared to a year ago, they are still higher than they were during the pandemic. Add that to spiraling HOA fees, insurance premiums and interest rates, and you end up with a perfect recipe for buyers collectively hitting the pause button on Florida condominiums. Unfortunately for sellers, the new reality is hitting them in the pocketbook.

Read Next:

Image Credit: Shutterstock

“ACTIVE INVESTORS’ SECRET WEAPON” Supercharge Your Stock Market Game with the #1 “news & everything else” trading tool: Benzinga Pro – Click here to start Your 14-Day Trial Now!

Get the latest stock analysis from Benzinga?

This article Florida’s Condominium Market Is Becoming A Disaster Zone originally appeared on Benzinga.com

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Martinprescott | E+ | Getty Images

Millions of older adults who are behind on their student loans could soon receive a smaller Social Security benefit.

That was the warning from Democratic lawmakers, including Sen. Elizabeth Warren, D-Mass., and Sen. Ron Wyden, D-Ore., in a recent letter to the Biden administration.

“When borrowers are in collections, on average their Social Security benefits are estimated to be reduced by $2,500 annually,” the lawmakers wrote on March 19. “This can be a devastating blow to those who rely on Social Security as their primary source of income.”

The U.S. government has extraordinary collection powers on federal debts and it can seize borrowers’ tax refunds, wages and retirement benefits. Social Security recipients can see up to 15% of their benefit reduced to pay back their defaulted student debt, which “can push beneficiaries closer to — or even into — poverty,” the lawmakers wrote.

After the pandemic-era pause on student loan payments expired in October of last year, the U.S. Department of Education said it wouldn’t resume its collection practices for 12 months.

However, the lawmakers wrote, “we are concerned that borrowers will face the extreme consequences associated with missed payments when protections expire in late 2024.”

They asked the Biden administration to provide a briefing on its efforts to address the issue by April 3.

More from Personal Finance:

FAFSA fiasco may cause drop in college enrollment, experts say

Harvard is back on top as the ultimate ‘dream’ school

More of the nation’s top colleges roll out no-loan policies

The U.S. Department of Education did not immediately respond to a request for comment.

The government’s collection practices with student loan borrowers, including the garnishment of wages and Social Security benefits, is an area under review, a source familiar with its plans told CNBC.

Outstanding student debt has been growing among older people. To that point, more than 3.5 million Americans aged 60 and older had student debt in 2023, a sixfold increase from 2004, according to the lawmakers.

Consumer advocates say the government’s collection actions are extreme.

“Many retirees need their Social Security benefits to survive,” said higher education expert Mark Kantrowitz.

Social Security benefits constitute nearly all income for one-third of recipients over the age of 65, the lawmakers said in their letter. The average check for retired workers is $1,907 this year, according to the Social Security Administration.

The garnishments mean older adults are often “forced to choose between skipping meals or rationing medicine,” Kantrowitz said. “It is a morally bankrupt policy.”

I have a million dollars and I want to put it to work for me. Where can I put it to make the most amount of passive income from it? Also, how can I minimize taxes on that to be able to keep more of that money?

– Andrea

While today’s high-interest rate environment has been challenging in many respects, the silver lining is that investors seeking to earn passive income can do so more easily than they could at any point since the global financial crisis of 2007-2009.

Before laying out some options to capitalize on prevailing yields and considering the associated tax consequences, it’s helpful to evaluate your existing financial picture and ask yourself some important questions that will impact where you put the money. (A financial advisor can help you do both and this tool can help you match with one.)

Investing your $1 million dollars with an eye toward generating passive income may very well be the best option for this money. However, rather than viewing your decision in a vacuum, I would recommend looking at the money in the context of your broader financial situation and longer-term goals. In particular, it might be helpful to consider the following questions:

Your total assets: Do you already have a portfolio of investments? Where are those assets located and what are their tax implications (e.g., IRA, Roth IRA, 401(k), brokerage account)?

Your work status: How many more years will you have an income to add to your assets?

Other income: Do you have any other sources of income (Social Security, pension, etc.)?

Purpose for generating passive income: Are you retired and seeking to fund your ongoing expenses? Or is it to provide supplementary income while the rest of your portfolio continues to grow?

Growth vs. income: Are you willing and/or able to sacrifice growth and preservation of purchasing power for the sake of income? If income is the only goal or need, then expectations for growth and your ability to maintain the purchasing power of the assets should remain low.

It is possible that after thinking through these questions you might pursue a different goal for the money. (And if you need more help assessing your financial situation, consider speaking with a financial advisor.)

Given the rise in interest rates since March 2022, income-oriented assets have become more attractive for those looking to earn a reasonable yield from their investments. Building a portfolio that includes a variety of assets capable of generating an aggregate yield is often a sound approach, as opposed to investing in a single product or security. While a financial advisor can help you build a robust portfolio, here are a few options to consider:

While generally considered an alternative to holding cash in a savings account, money market funds have become a popular topic among investors amid rate increases. Prior to the Federal Reserve’s recent series of rate hikes, money market yields were close to 0%, meaning you effectively earned no interest on your investment. Today, however, yields are closer to 5%, making this a much more compelling option for generating low-risk income.

Municipal bonds are another solid option for income-focused investors. As with any investment, you’ll want to consider your goals before investing in municipal bonds since the risk profile and income potential will vary across securities. Evaluating credit ratings and maturities in relation to the yield you expect to earn in exchange for taking on credit and duration risk is a necessary step to take. Because they are typically not subject to federal taxes (or state taxes in the state where they are issued), municipal bonds tend to be a tax-efficient investment.

Like money market funds, certificates of deposit (CDs) have gained popularity as rates have increased. CDs can be particularly attractive if you do not need to liquidate the investment over its intended time horizon since you generally will pay a penalty for early withdrawals. It is therefore important to align a CD’s maturity date with the date at which you expect to need the money back.

If you will need some growth to accompany the passive income your money generates, you may want to consider investing in dividend stocks. The S&P 500 High Dividend Index was paying a dividend yield in excess of 5% as of the end of September, making it competitive with other options listed. Unlike fixed-income products, dividend stocks will typically provide more opportunity for appreciation, which may help you maintain purchasing power over time if that’s a concern.

Of course, there are additional options for generating passive income. These include Treasuries, high-yield bonds, master limited partnerships (MLPs), real estate investment trusts (REITs) and many others. Before committing to each, consider the level of risk you are able and willing to take, the amount of income you will need, and whether some element of growth is necessary. Also, evaluate the tax implications of the investments you choose. (And if you need more help evaluating and selecting investments, consider matching with a financial advisor.)

Each of the options cited above is treated differently for tax purposes. The interest earned by fixed-income securities is taxed at ordinary income tax rates. Taxes on dividends from equity securities depend on how long you own the asset – qualified dividends are taxed at long-term capital gains rates while ordinary dividends are taxed at ordinary income rates. Appreciation from equity securities is taxed at capital gains rates.

It’s important to understand the tax treatment of individual assets since that will play a role in determining the type of account that holds these assets. Generally speaking, owning individual stocks and bonds, as well as their passively managed index alternatives, is more tax-efficient than actively managed mutual funds. Therefore, it’s typically advisable to own individual stocks, bonds and index funds in taxable brokerage accounts. Tax-advantaged accounts like IRAs and 401(k)s, and after-tax Roth IRAs, are generally more suitable for your actively managed funds and less tax-efficient securities like high-yield bonds.

Thinking holistically about the assets you own and where to allocate them will ultimately help you mitigate taxes. Of course, it can be helpful to speak with your tax advisor to better understand the impact on your individual situation, given your specific tax brackets. (Consider matching with a financial advisor with tax expertise.)

Positioning your assets for passive income generation is a sound strategy, but only if it aligns with your long-term financial needs and goals. Before committing to this approach, critically assess your personal situation and the rationale behind seeking passive income. From there, you may consider various fixed-income products like bonds and CDs, as well as equity securities like dividend-paying stocks. Each option has its own tax consequences, and the type of account the securities are held in will also have an impact on taxes.

A CD ladder is one way to capitalize on today’s high-interest rate environment while also generating income. The strategy calls for opening multiple CD accounts, each with varying maturity dates. The idea is that you’ll always have a CD reaching its maturity date and paying out interest. Here’s a look at today’s CD rates.

A financial advisor can help you decide which investments are most aligned with your financial goals. Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three vetted financial advisors who serve your area, and you can have a free introductory call with your advisor matches to decide which one you feel is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

Jeremy Suschak, CFP®, is a SmartAsset financial planning columnist who answers reader questions on personal finance topics. Got a question you’d like answered? Email AskAnAdvisor@smartasset.com and your question may be answered in a future column.

Jeremy is a financial advisor and head of business development at DBR & CO. He has been compensated for this article. Additional resources from the author can be found at dbroot.com.

Please note that Jeremy is not a participant in the SmartAdvisor Match platform, and he has been compensated for this article. Some reader-submitted questions are edited for clarity or brevity.

Photo credit: ©iStock.com/Viorel Kurnosov, ©iStock.com/Sam Edwards

The post Ask an Advisor: I Have $1 Million and Want It to Work for Me. How Do I Maximize Passive Income and Minimize Taxes? appeared first on SmartReads by SmartAsset.

New home sales at 662,000 annual rate in February versus 664,000 in the prior month.

Source link

Nissan is targeting an additional 1 million vehicle sales over the next three years and a 30% reduction in electric vehicle production costs by 2030, the Japanese carmaker announced Monday.

In a new medium-term business plan, Nissan also said it would launch 30 new models by fiscal 2026, with 16 of these electrified. It’s aiming for EV and combustion engine costs to reach parity by 2030.

“This plan will enable us to go further and faster in driving value and competitiveness,” Nissan President and CEO Makoto Uchida said in a statement.

“Faced with extreme market volatility, Nissan is taking decisive actions guided by the new plan to ensure sustainable growth and profitability.”

The automaker also said it is targeting an operating profit margin of more than 6% by the end of fiscal 2026, as well as “long-term profitable growth.”

A Nissan Ariya electric car is on display during 2020 Beijing International Automotive Exhibition (Auto China 2020) at China International Exhibition Center on September 27, 2020 in Beijing, China.

Vcg | Visual China Group | Getty Images

To address this, Nissan plans to develop EVs in “families,” integrate powertrains and focus on battery innovations as it looks to cut the cost of its next-generation fleet by 30% when compared with the current model Ariya crossover.

“In order to do that, we have to have a great partnership with our suppliers to work on from the app stream earlier with the scale that we have to provide,” Uchida told CNBC’s “Squawk Box Europe.”

“Otherwise, I think the next five years, there’s a lot of uncertainty that we are facing. The scalability will be most important, and how are we going to make that as a Nissan collaboration with a partnership is going to be one of the key items.”

Under the two-part plan dubbed The Arc, Nissan said it will aim to ensure volume growth through a “tailored regional strategy,” and prepare for an accelerated EV transition by balancing its portfolio between EV and combustion cars, growing volumes in major markets, and financial discipline.

This will be supported by “smart partnerships, enhanced EV competitiveness, differentiated innovations and new revenue streams.”

Nissan said this strategy could yield potential revenues of 2.5 trillion yen ($16 billion) from new business opportunities by fiscal 2030.

A 401(k) is the most common retirement account, but it’s far from the only type of retirement account available. Another common account is an IRA. Unlike a 401(k), an IRA isn’t tied to an employer and must be opened independently, similar to a bank or brokerage account.

There are two main types of IRAs: traditional and Roth. Both have unique benefits and can play a critical role in your retirement savings and investment strategy.

It’s natural to want to boost your IRA balance as much as possible to prepare for retirement, and many people set their eyes on the million-dollar mark. And while that’s a great goal, people should keep a few things in mind.

Image source: Getty Images.

IRAs have many great aspects. They’re free, allow you to invest in virtually any stock or exchange-traded fund (ETF) you want, and have flexible early withdrawal rules that can be beneficial for life events like buying a house or paying for higher education expenses.

That said, one downside to an IRA is the relatively low contribution limit. The most you can contribute to an IRA in 2024 (both traditional and Roth combined) is $7,000. If you’re 50 or older, you can add an additional $1,000 catch-up contribution, bringing the limit to $8,000.

IRA contribution limits are far lower than a 401(k), which allows you to contribute $23,000 ($30,500 if you’re 50 or older). This is important to keep in mind when aiming to become an IRA millionaire.

Because of IRAs’ relatively low contribution limits, the key to hitting the million-dollar mark will rely heavily on time. Time is one of the greatest forces in investing, mainly because it fuels compound earnings. Compound earnings occur when the returns you earn from investments begins to generate returns of their own.

For example, imagine you invest $1,000 and earn a 10% return, or $100. If you reinvest the $100 and receive 10% again, you’re now earning a return on $1,100, receiving $110. If you reinvest the $110, the 10% is now on $1,210. It’s a rewarding cycle that can take relatively small investments and turn them into big gains.

For compound earnings to work its magic, though, it needs as much time as possible. The more time, the more the compounding effect grows. Without compound earnings, it’d take someone over 142 years to hit $1 million by saving $7,000 annually and 125 years by saving $8,000 annually.

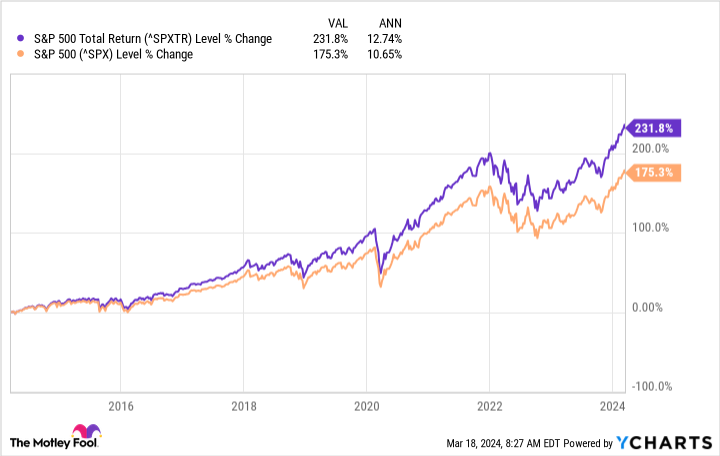

Those aiming to become IRA millionaires should be prepared for the journey to take at least a couple of decades, and that’s on the lower side of things. For perspective, the S&P 500 (^GSPC -0.31%) — which is the stock market’s primary benchmark — has averaged around 10% annual returns since its inception. In the past decade, it has averaged 12.7% total returns, so we’ll round that up to 13% for our example.

Assuming the IRA contribution limit remains at $7,000, and you invest that amount while averaging 13% annual returns, it will take you close to 25 years to cross the million-dollar threshold. If you started at 50 and contributed $8,000 the whole time, it’d still take you close to 24 years.

It’s important to note that past results don’t guarantee future performance, and returns can vary widely — especially over decades. You could average 10% annual returns over those years, or you could average 15%. Nobody can say for certain.

That’s why the main focus should be on starting as early as possible and prioritizing maxing out your IRAs each year. I always recommend that people contribute enough to their 401(k) to get the maximum employer match and then focus on using any additional money to fund their IRAs.

Once your IRA is maxed out for the year, return and add additional contributions to your 401(k) if you choose. That strategy gives you the best of both worlds.

AUSTIN — There is a sort of clubhouse for Austin’s bitcoin believers on the second floor of the Littlefield Building at the corner of Congress Avenue and Sixth Street. The hideaway is at the crossroads of two worlds — the majestic thoroughfare that leads to the Texas State Capitol and the iconic, albeit notorious, stretch of bars, restaurants, and live music that define the capital’s party vibes. It’s an apt metaphor for the space itself.

The Bitcoin Commons is, at once, many things.

By day, it functions as an open plan, fluorescent-lit co-working space for the more corporate-minded bitcoin operators, but at night, it moonlights as a safe space for underground meet-ups of the industry’s rogue actors. Periodically, it plays host to conferences that draw in a mix of attendees ranging from venture capitalists to armed preppers living entirely off the grid. And on some afternoons, once happy hour hits, the kitchen at the back is retrofit with a stowaway bar.

“We also fund developers, and we help them advance their projects,” said Parker Lewis, one of the stewards of the Commons, as well as the author of a new book on bitcoin called “Gradually, Then Suddenly.”

“We help advance bitcoin through education and actually developing the monetary network, the code base, and the applications,” said Lewis, who is widely considered to be one of Texas’ de facto bitcoin ambassadors.

Francisco Chavarria was born in Mexico City and spent time in Salt Lake City, but three years ago, he made the move to Austin to be a part of a community of like-minded thinkers. His company, Yopaki, which is a neobank for bitcoin focused on the Latin American market, just won first place in a hackathon put on at the Commons.

“If you talk to other builders in the competition, a lot happens here,” said Chavarria. “There definitely is a sense of, ‘I don’t need for others to lose for me to win.’ There really is a relationship and a collaboration for bitcoin to succeed.”

“Right now it feels like we’re all winning because of the price, but those of us who have been building in the bear market, we know,” Chavarria added.

Austin’s “Bitcoin Commons” hosts regular meetups and conferences for the city’s bitcoiners.

CNBC

Bear or bull market, bitcoiners have flocked to Austin because of a combination of pro-crypto policies, abundant, renewable energy, and an ever-growing network of some of the brightest developers and miners on the planet. And even in the price doldrums, they typically bring the same level of enthusiasm to the conversation — though bitcoin’s recent stretch of record-breaking price moves has gone a long way toward boosting morale.

In March, bitcoin hit multiple, fresh all-time highs, as trader enthusiasm for the digital asset sector soared. A lot of that price run-up has to do with the record flows into the newly-launched spot bitcoin exchange-traded funds in the U.S., led by the world’s largest asset manager Blackrock and its $15.5 billion iShares Bitcoin Trust, which have helped to solidify bitcoin’s place as an asset class that’s here to stay.

Collectively, these spot ETFs have brought in around $60 billion, and in some cases, they have been breaking records for ETF flows altogether.

“The biggest driver is certainly the ETF flows, which have surpassed the expectations of all but the most bullish pundits,” said Castle Island Venture’s Nic Carter of bitcoin’s record price moves this month. “And these blockbuster flows have materialized before the major wirehouses, asset managers, and RIAs have actually approved the ETF for their clients.”

Carter added that there is also new liquidity coming into bitcoin from Asian markets via two main pathways: bitcoin’s version of non-fungible tokens known as ordinals, as well as bitcoin-issued coins called BRC20 tokens.

In the last 20 years, Austin has matured into one of the country’s leading tech centers, a trend accelerated by the Covid pandemic, which saw industry leaders migrate en masse from California.

“Bitcoin was founded in 2009. A lot has happened post-financial crisis. Austin was already emerging as a tech center, and you know, enter bitcoin, and it just became the logical home,” said Lewis, who runs business development at Zaprite, a bitcoin-native financial services firm.

It helps that Texas is a libertarian-friendly state that actively supports free market policies. It has proven to be a big draw for a group of people who think of bitcoin as a way of life — that is, a monetary network that is decentralized, borderless, and doesn’t answer to central banks or governments.

Austin’s “Bitcoin Commons” draws in an eclectic mix of people, including venture capitalists, bitcoin miners, and coders.

CNBC

Many hardcore bitcoiners ironically embrace the term maximalist or maxi as a way to self describe. In Texas, though maxis exist along a professional spectrum from venture capitalists, to miners, coders, company executives, and generalist techies, the eclectic tribe have a few things in common. Many are family-oriented, patriotic carnivores with an aversion to the overreach of government and a strong belief in the right to bear arms, among multiple other personal, individual liberties.

Bitcoin’s eponymous Austin lair, which is adorned with the Texas state flag and bitcoin memorabilia, has adopted Chatham House rules for many of its events to protect the identities of those conversing within its walls. One such meetup is the monthly BitDevs (short for bitcoin developers) gathering, where bitcoin builders, investors, and the bitcoin curious are all welcomed, so long as no pictures or videos are taken.

At these meetings, topics run the gamut, from detailed discussions about code to concerns that the Microsoft-maintained GitHub may pose a greater existential threat to the bitcoin network since much of the development work and conversations among coders happen on that platform. At one such gathering, the moderator of the two-hour session asked the room who ran a bitcoin node. More than half of the people in attendance raised their hands.

After attending multiple Austin BitDev meetups over the last three years, a few common conversation themes have emerged, including the focus on identifying threat vectors to the network and brainstorming workarounds. Beyond software, there are also concerns over hardware vulnerabilities, given that the ASIC chip used in bitcoin mining rigs are manufactured out of China, a country which has proven hostile to the crypto sector in recent years.

The “Bitcoin Commons” functions as a sort of clubhouse for the city’s bitcoin believers. It puts on a mix of programming, including conferences and hackathons, as well as hosts a co-working space by day.

CNBC

The Commons hosted a hackathon, BitDevs, and a one-day conference dubbed the Bitcoin Takeover on the sidelines of the annual South by Southwest tech festival, which put on virtually no crypto programming this year.

Across those multiple gatherings, there was a newfound interest in talking about the burgeoning ecosystem of projects building on top of bitcoin’s blockchain, which began to heat up with the introduction of ordinals in Jan. 2023 — bitcoin’s version of non-fungible tokens.

One underrated driver of bitcoin’s recent rally is new programming innovations that may allow it to reach technological parity with ethereum. These advancements involve beefing up the bitcoin ecosystem with tools like smart contracts, which are programmable pieces of code that help to eliminate middlemen like banks and lawyers from transactions. That makes it easier for developers to create products and applications for consumers.

BitVM, for example, has a promising plan to do just that. It is ultimately trying to bring smart contracts to the bitcoin network, which has helped spur this renaissance of interest in layer two technology — that is, the startups being built on top of bitcoin’s base chain.

“I’ve never seen deal pacing move this aggressively in the bitcoin space in my entire career,” Carter tells CNBC.

Indeed, the VC appetite for these layer two bitcoin projects has been picking up in the last few months.

PitchBook says that the fourth quarter of 2023 was the first time in almost two years that deal value in the crypto sector had increased, reaching $1.9 billion — up 2.5% from the previous quarter. While still well off the 2021 high of $31 billion, funds are building back interest, and trust, in the space.

Grant Gilliam spent 15 years working in private equity in New York before pivoting to run a bitcoin VC fund called Ten31. This investment platform, which is focused exclusively on bitcoin, has invested $125 million of equity in aggregate since launching five years ago. More than $100 million was deployed in the last two years during the bear market.

“We invest across the bitcoin ecosystem across every major theme,” Gilliam told CNBC. “Anything that is relevant to bitcoin infrastructure, we like to say the picks and shovels of companies building products and services for holders of bitcoin.”

Gilliam, who spent a few years commuting from New York to Austin every month for the BitDevs meetup, said that some of the layer two bitcoin investments are more hype than substance, but he’s still bullish overall on the deal space.

“There’s been a lot of L2 hype lately, mainly driven by the ordinals, and inscriptions, developments or innovations, if you want to call it that,” Gilliam said. “There’s a lot of activity in that right now, but we haven’t been as focused on that. It’s our firm view that the ordinals will prove to be a passing fad.”

Gilliam says that Ten31 is focused on basic building blocks of the ecosystem, such as companies that are providing financial services, which could be custody trading and lending, or projects that are working to scale the lightning network.

Lightning, with is the layer two payment technology meant to realize bitcoin’s original vision of being peer-to-peer cash continues to struggle with the issue of reaching scale. Developers tell CNBC that a lot of engineering work remains to close that gap.

“Number go up” is a big mantra among bitcoiners, but as the community evolves, so too does the thinking about the price of the coin.

“Price is really an output of many inputs of human beings, building tools to make bitcoin both more secure and a greater utility,” Lewis said. “Price is the best indicator of more people coming to the conclusion that bitcoin is money, and it’s a better store of value, so it is very relevant.”

Every four years, bitcoin undergoes a market making event known as the halving. It cuts the production of new bitcoin in half, and it has typically come before a major run-up in the price of bitcoin.

Miners from around the world flocked to Texas when China banned the practice in 2021, attracted by the abundant renewable energy and a grid that’s friendly to flexible buyers of power — both ideal conditions for miners.

In April, however, the profits for these bitcoin miners will be cut in half.

For some, it may prove an Armageddon-level event. Others have braced for impact by swapping out their fleet of machines for more efficient rigs. The price run-up in bitcoin has also helped to give some of these companies a buffer in their profit margins.

West Texas miner Jamie McAvity has 60 megawatts at his mining site. It runs on a part of the grid that is 90% powered by a mix of solar and wind power.

“If you’ve been in for more than one cycle, you have situated yourself in a place where you can resist the halving to the best of your ability,” McAvity told CNBC at Austin’s Bitcoin Commons.

McAvity, who previously worked for ten years as a trader on the floor of the New York Mercantile Exchange, added that ETF flows have helped to change the pricing dynamics for the world’s largest coin.

“The spot ETF inflows are so massive that reducing the available supply of newly mined bitcoins from 900 to 450, is probably going to be immaterial relative to that,” he said.

“But who knows, the ETFs could cool off for a while, and it’s hard for someone to credibly say that a reduction in supply is not going to change the market price equilibrium, because that’s a fundamental principle of market economics,” he added.

A cotton candy machine was part of the catering at the Boys Club’s crypto conference on the sidelines of South by Southwest.

CNBC

A ten minute walk west from the Bitcoin Commons is the Austin Proper Hotel, a five-star establishment where the lighting is intentionally dim to strike a certain mood. Here, the Boys Club, a popular and buzzy, female-led organization which self-describes as a “social collective bringing new voices to the new internet” put on its own crypto conference on the sidelines of South by Southwest.

The Boys Club caters to a more blockchain agnostic crowd, where the focus is less on exclusivity to one coin or chain — and more about borrowing the best features from across the ecosystem to solve problems in the real world.

CNBC caught up with Micha Benoliel at the one-day summit. Benoliel built Nodle, a decentralized wireless network that’s now getting into the business of using the blockchain to battle AI-powered deepfakes.

“Blockchain is the only way to make a record that is immutable, and is going to prove the time at which this photo has been taken, or video, and also to help you prove the location and other elements that are going to reinforce that proof, so it creates a real immutable proof of authenticity,” he said.

The Boys Club put on its own Austin summit on the sidelines of SXSW with programming on the new internet, crypto, and digital culture.

CNBC

The one-day popup event gathered together more of a web3 crowd to talk about everything from the latest trends in tokenization to the resurgence of on-chain meme culture.

Similar to other bull runs in the price of bitcoin, some altcoins have seen a meteoric rise alongside blue chip names in crypto, because they’re seen as a comparatively cheaper buy.

Dogecoin, a meme-coin that was started as a joke, now has a market cap of nearly $25 billion, placing it in the top ten most valuable cryptocurrencies on the planet. Boden, a coin named after President Joe Biden, saw a run-up of more than 800% in a six-hour window after Super Tuesday, and the newly popular DogWifHat is collectively worth more than $2 billion.

Typically, this is the bellwether of a peak bubble moment, but analysts say that despite frothy conditions, this bull run is different to past cycles.

The price of bitcoin is cyclical, and it sees price run-ups roughly every four years. Each time, the price floor is higher. What’s also a departure this time around is the fact that institutional money is here in a way that it hasn’t been during past bull runs.

Fundamentals in the crypto market are playing a big role, as well.

In a note from JPMorgan on Mar. 15, analysts credit ether, the world’s second-biggest crypto token by market cap, for being a significant driver of crypto’s recent gains, including Coinbase‘s stock price rise. Ether has rallied nearly 50% so far this year, recently breaching the $4,000 price level and outpacing bitcoin’s returns, before paring back some gains.

“While the focus of the cryptocurrency marketplace has been the net new money going into U.S. spot Bitcoin ETFs and the positive impact on Bitcoin token prices (here, the spot Bitcoin ETF and its ultimate launch in January has driven the cryptoecosystem over the past several months), we see impact of ETH appreciation also as particularly meaningful,” JPMorgan wrote.

Regulators in the U.S. remain a universal concern for the crypto sector, especially amid reports of the Securities and Exchange Commission probing crypto companies building on the ethereum network.

Still, many in the space, including coders and investors remain optimistic.

Ethereum, the blockchain that underpins ether, underwent a major upgrade on Mar. 13 dubbed Dencun. Developers told CNBC it was expected to slash transaction fees by up to 90%. That is game-changing not just for the end-users, but also for the coders building apps on top of ethereum.

Base, crypto exchange Coinbase’s self-built layer two network, is ethereum-based and allows developers to more easily build decentralized apps. Coinbase’s Base lead, Jesse Pollak, anticipates this will open the door to applications in both the gaming and decentralized social media arena now that it is no longer nearly as cost prohibitive to build these types of programs.

“The thing that is happening with Dencun is we’re going to create a whole new kind of storage on ethereum that’s purpose built for Layer 2s like Base,” Pollak told CNBC.

“That means that right now we pay a ton to ethereum, and we’re going to pay a lot less, which is going to lower the fees for everyone. Because ethereum is basically going to build a product purpose built for us,” continued Pollak.

Chris Dixon, crypto chief at venture firm a16z, echoed that sentiment, noting that part of their portfolio is focused on these startups.

“The core idea is that if you build a social network, or a game or a financial service, on top of the blockchain, it has all sorts of benefits where the money and control flow out to the users and the creators that access the network, as opposed to the companies that control it,” said Dixon. “In the same way that steel was a better way to build bridges and buildings than wood was in the Industrial Revolution, blockchains are a building material.”

It’s been a tough past couple of years for fintech stocks. Rising interest set the stage for economic lethargy, while an inverted yield curve threatened an outright recession. Such a backdrop makes owning already risky financial technology names even riskier.

A funny thing happened on the road to inevitable doom, however — the global economy didn’t implode. Most regions’ economies are doing reasonably well. The World Economic Forum is calling for a worldwide economic growth rate of 3.1% this year, in fact, before accelerating to a pace of 3.2% next year. The yield curve continues its trek back toward being un-inverted too; each day it makes this progress raises the odds of a so-called soft landing rather than a full-blown meltdown. That’s bullish for most stocks, but it’s particularly bullish for economically sensitive fintech names.

Here’s a closer look at three fintech stocks that could lead the group’s bullish charge all the way through 2030. That’s how long recently rekindled economic growth could last, presuming the world’s banking and political leaders don’t stand in the way.

There’s no denying the original fintech name’s very-highest-growth days are in the past. But PayPal (PYPL 1.90%) is hardly a has-been.

PayPal is of course an online payment and mobile wallet platform. It arguably created and defined what a digital payment service should be, in fact, and then became the name in this space to beat.

The thing is, rivals did eventually start creeping onto this company’s turf, and they never really stopped. That’s why PayPal shares performed so poorly beginning in late 2021 after a heroic run-up from their early 2020 low. Not only was the e-commerce boom stemming from the COVID-19 pandemic starting to cool off, but it was also a time when cryptocurrency-based payment platforms began capturing consumers’ as well as investors’ attention. Many investors feared the worst for PayPal.

It’s now clear those fears were mostly unmerited. Last quarter’s revenue was up 8% year over year, capping off full-year top-line growth of 8%. Although the total number of active PayPal users didn’t grow, the number of times these users utilized PayPal’s service to make a payment improved 14% on a year-over-year basis. The analyst community is calling for comparable sales growth this year and next, with earnings growth expected to roll in at around the same pace.

That’s nowhere near the sort of growth PayPal was experiencing in its heyday. The entire online payment and mobile wallet market has matured, making growth tougher to come by.

What this company may lack in future growth potential, however, it more than makes up for in dominance of a market that’s set to expand due to a combination of population growth, the increasing proliferation of web connectivity, and a growing willingness to use purely digital payment options (as opposed to payment cards). Capital One estimates PayPal still controls on the order of a market-leading 45% of the electronic payments market.

Consumers’ growing interest in digital financial services isn’t just a boon for PayPal, however. It’s impacting the entirety of the banking industry. Bank of America reports three-fourths of its customers now routinely use at least one of its digital banking tools, for instance, while roughly half of any product and service sales made to consumer banking customers last quarter happened online. In this same vein, the American Bankers Association says the most common way U.S. consumers now check their bank account balance is with a mobile app. Indeed, data gathered by JP Morgan Chase‘s Chase Bank indicates that 62% of consumers feel they couldn’t live without their banking app, while nearly 80% of these people use their banking app at least once per week.

As was the case with shopping, the world’s moving more and more of its banking business online.

Enter SoFi Technologies (SOFI 2.06%). Not only is it an online bank, it’s only online — there are no branches. This hasn’t limited its offerings, though. Customers enjoy access to every option a consumer would expect to find available at a brick-and-mortar bank, including checking and savings accounts, loans, investments, credit cards, and even insurance.

And people are responding to this relatively new kind of banking. SoFi now boasts a little over 7.5 million customers, more than doubling its count from just a couple of years back. Indeed, the company’s expanded its customer base in every single quarter going all the way back to the first quarter of 2020.

SoFi’s not yet reliably profitable, but analysts expect it to report its first full-year profit in 2024 after swinging to its first quarterly profit in the final quarter of last year. That could prove catalytic for this stock that’s been lethargic for the past couple of years.

Last but not least, add MercadoLibre (MELI -1.39%) to your list of fintech stocks that could outperform most of its peers between now and 2030.

Don’t worry if you’ve never heard of it — if you live in North America, you’ve no reason to. That’s because the company strictly serves the Latin American market with its suite of fintech solutions. It’s often called the Amazon of Latin America, in fact, although that description doesn’t do it justice. MercadoLibre is just as akin to the aforementioned PayPal as well as to the online auction site eBay.

Although the internet and mobile phones have existed in South America for about as long as they have anywhere else, neither were as common there as they may have been in other parts of the world until recently. For perspective, Americas Market Intelligence says Latin America’s e-commerce market expanded 36% in 2021 before accelerating to a growth pace of 39% in 2022, as infrastructure growth finally caught up with demand.

The thing is, there’s still lots of room for more of this growth. Americas Market Intelligence is looking for 24% growth in Latin America’s e-commerce market this year, with another 21% growth in the cards for next year.

Helping drive this acceleration is the past and present development of the region’s mobile connectivity. Only 60% of the continent’s residents owned a mobile device capable of connecting to the web as of 2020, according to research outfit GSMA. Even with the ongoing availability and adoption of mobile phones, though, only 67% of Latin America’s population is expected to have regular access to mobile internet by the end of next year.

This of course bodes well for MercadoLibre’s long-term potential … not that investors will have to wait until 2030 for their patience to start paying off. Last year’s revenue was up an impressive 37%, supporting even more earnings growth. This year’s and next year’s projected sales and profit growth are similarly impressive numbers, reflecting the maturation of the region’s digital consumerism.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. Bank of America is an advertising partner of The Ascent, a Motley Fool company. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Bank of America, JPMorgan Chase, MercadoLibre, and PayPal. The Motley Fool recommends eBay and recommends the following options: short July 2024 $52.50 calls on eBay and short March 2024 $67.50 calls on PayPal. The Motley Fool has a disclosure policy.