“We were told that the attorney had attempted to call Mary’s family but that none of the numbers worked.”

Source link

“We were told that the attorney had attempted to call Mary’s family but that none of the numbers worked.”

Source link

The actress, director and author reflected on why she hired her former lawyer, who is now serving a 14-year prison sentence for wire and tax fraud.

Source link

At age 60, you’re not too far from retirement. In fact, the average retirement age is 61, although there are plenty of Americans who continue working into their late 60s and beyond.

It’s always important to know whether you’re on track with your retirement savings. That’s especially true as you reach your 60s, since you’re getting close to the end of your career. If you’re trying to figure out where you stand, you’ll find data on the average 401(k) balance below, plus some tips on what to do if you need to save more.

Bonus offer: unlock best-in-class perks with this brokerage account

Read more: best online stock brokers for beginners

The average 60-year-old has $70,000 to $210,000 in their 401(k). Why such a wide range? There are two recent sources with a fairly large difference:

Vanguard reported that Americans ages 55 to 64 have a median 401(k) balance of $70,620 and an average balance of $232,710 in How America Saves 2023.

A 2024 Empower article reported that Americans in their 60s have a median 401(k) balance of $209,382 and an average balance of $555,621.

The median balances are likely a more accurate representation of the overall average. When there’s a big difference between a median and an average, it’s because outliers are having an outsized impact on the average. In this case, people with very high 401(k) balances bring up the average quite a bit.

A popular guideline on retirement savings is to save eight times your salary by age 60 and 10 times your salary by 67. Many 60-year-olds are likely well behind that guideline, based on the recent data. To be fair, some Americans also have other forms of retirement savings, such as individual retirement accounts (IRAs).

Even at 60, there’s still time to make significant contributions to your retirement savings. If you feel like you won’t have enough money to retire, here’s what you can do.

The 401(k) contribution limit is $23,000 in 2024. But one of the advantages of being 50 or older is that you can also make additional catch-up contributions of up to $7,500, for a combined limit of $30,500. If you can’t contribute that much, try to at least put in enough to max out any 401(k) match your employer offers.

Just like 401(k) plans, IRAs allow you to save for retirement while saving on taxes. The contribution limit is $7,000 in 2024. When you’re 50 or older, you can make additional catch-up contributions of up to $1,000, for a combined limit of $8,000.

There are several financial benefits to delaying your retirement. By working longer, you’ll be able to save more. You’ll start withdrawing from your retirement savings later, and you can also delay taking Social Security. If you wait until age 70, you’ll receive your maximum Social Security benefits.

Another way to make up the gap in your retirement savings is to reduce your cost of living. You could start looking into areas with a lower cost of living for after you retire — some people even choose to retire abroad. If you want to stay in your current city, you could move to a smaller, more affordable home.

If you can max out your 401(k) and IRA, that’s $38,500 in retirement savings per year, and potentially more if contribution limits increase. After five years, you’ll have added $192,500 to your retirement. That money could also grow if you invest in stocks and bonds.

Most people can’t max out all their retirement accounts, so don’t feel bad if you aren’t contributing that much. Just put in as much as you can. If you do that, combined with potentially working longer and cutting costs, you can still retire with financial security.

This credit card is not just good – it’s so exceptional that our experts use it personally. It features a lengthy 0% intro APR period, a cash back rate of up to 5%, and all somehow for no annual fee!

Click here to read our full review for free and apply in just 2 minutes.

We’re firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.The Motley Fool has a disclosure policy.

Here’s How Much the Average 60-Year-Old Has in Their 401(k) was originally published by The Motley Fool

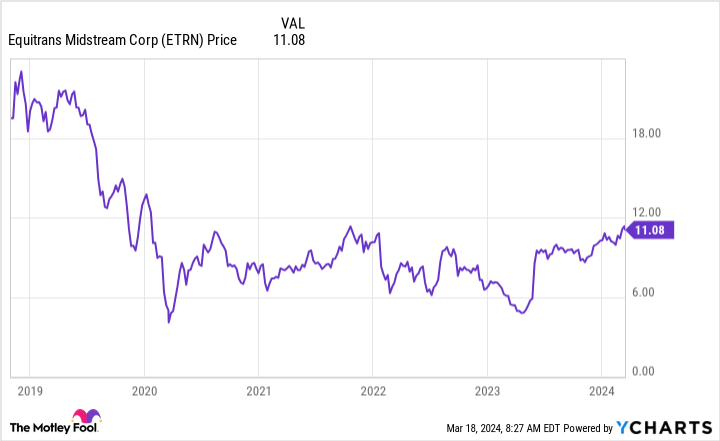

NextEra Energy Partners (NEP 1.29%) is showing up on high-yield screens today thanks to its huge 12%+ distribution yield. This wasn’t always the situation, noting that the yield was closer to 4% at the end of 2022. The steep unit price decline that pushed the yield higher is worth examining, but the potential fallout from that decline is also worth considering. To get an idea of why the latter consideration is important, just look at what’s happening with Equitrans Midstream (ETRN 1.31%) today.

NextEra Energy Partners was created by NextEra Energy (NEE 0.68%), one of the largest utilities in the United States. In addition to being a large regulated utility, NextEra Energy is also one of the largest producers of solar and wind power in the world. To take advantage of Wall Street’s once hot demand for anything related to clean energy, NextEra Energy created a master limited partnership (MLP) to own clean energy assets.

Image source: Getty Images.

NextEra Energy Partners is basically a funding vehicle for its parent, NextEra Energy. The parent sells clean energy assets, or “drops them down,” in industry lingo, to the MLP. The MLP buys the assets by issuing units and taking on debt. NextEra Energy uses the cash from the asset sales to fund future investments. NextEra Energy Partners uses the cash flow from the assets it buys to pay distributions to unitholders.

But investors have soured on the clean energy space, leading to a notable decline in the price of NextEra Energy Partners. That makes it more expensive to sell units. Making matters worse, rising interest rates increased the cost of debt capital, too. At this point, it isn’t nearly as attractive for NextEra Energy to sell assets to NextEra Energy Partners. And, as you might expect, NextEra Energy has announced plans to pull back on drop downs. That, in turn, will lead to slower growth at NextEra Energy Partners.

The big story for Equitrans Midstream is that EQT Corp. (EQT), the company that created the MLP, is buying it back. This isn’t the first time that a parent company of an MLP has bought back the MLP it created. The list includes utilities like Dominion Energy and pipeline operator Kinder Morgan, among others.

As you might expect, EQT is pitching its purchase of Equitrans Midstream as a positive. In fact it called the transaction “transformative,” even though it is, in many ways, just recreating the company as it was before Equitrans Midstream was spun off. The real story is that Equitrans Midstream is being bought back at a price that is far below the price at which it was spun off.

Now think back to NextEra Energy Partners. The purpose of that MLP is to be a funding vehicle for NextEra Energy, but it just isn’t as valuable as it once was on that front. With the unit price dramatically lower than it was, there’s a very real possibility that NextEra Energy simply buys the MLP back on the cheap.

To be fair, the runway for growth in the clean energy sector is more attractive than the growth opportunity in the pipeline sector. That suggests that NextEra Energy might want to wait longer to see what happens with NextEra Energy Partners before doing anything rash. But there are multiple examples of MLP spinoffs being bought back once they have outlived their usefulness. If you own NextEra Energy Partners you should keep the Equitrans Midstream situation in the back of your mind.

The real concern here, however, should be for investors who are considering adding NextEra Energy Partners to their portfolio because of its hefty 12%+ distribution yield. While that yield is backed, to some degree, by a strong parent, NextEra Energy could just as easily decide to buy the MLP, effectively making what was an attractive yield quickly go away. Equitrans Midstream, among others, shows that this is, in fact, a very real possibility and a risk dividend investors shouldn’t ignore.

Reuben Gregg Brewer has positions in Dominion Energy. The Motley Fool has positions in and recommends EQT, Kinder Morgan, and NextEra Energy. The Motley Fool recommends Dominion Energy. The Motley Fool has a disclosure policy.

‘When I married my husband, he sold his house, which was valued at about $100,000 more than mine, but he had no equity in it.’

Source link

U.S. President Joe Biden and Vice President Kamala Harris meet with (L-R) Senate Minority Leader Mitch McConnell (R-KY), House Speaker Mike Johnson (R-LA), Senate Majority Leader Chuck Schumer (D-NY), House Minority Leader Hakeem Jeffries (D-NY), on February 27, 2024 at the White House in Washington, DC.

Roberto Schmidt | Getty Images

President Joe Biden on Saturday signed Congress’ $1.2 trillion spending package, finalizing the remaining batch of bills in a long-awaited budget to keep the government funded until Oct. 1.

Almost halfway into the fiscal year, the president’s signature ends a months-long saga of Congress struggling to secure a permanent budget resolution and instead passing stopgap measures, nearly averting government shutdowns.

“The bipartisan funding bill I just signed keeps the government open, invests in the American people, and strengthens our economy and national security,” Biden said in a Saturday statement. “This agreement represents a compromise, which means neither side got everything it wanted.”

The weekend budget deal slid in just under the wire before the Friday midnight funding deadline, as has been typical this fiscal year with eleventh-hour disagreements derailing near-complete deals.

The Senate passed the budget in a 74-24 vote at roughly 2 a.m. ET Saturday morning, technically two hours after the deadline due to last-minute disagreements. However, the White House said that it would not begin official shutdown operations since a deal had ultimately been secured and only procedural actions remained.

The House passed its own vote Friday morning after a week of scrambling to reconcile a lingering sticking point: funding for the Department of Homeland Security, which the White House took issue with last weekend. The White House’s qualms delayed the negotiation process further, just as lawmakers were preparing to release the legislative text of the budget proposal.

This trillion-dollar tranche of six appropriation bills will fund agencies related to defense, financial services, homeland security, health and human services and more. Congress approved $459 billion for the first six appropriations bills earlier in March, which related to agencies that were less partisan and easier to negotiate.

With the government finally funded for the rest of the fiscal year, House Speaker Mike Johnson, R-La., has cleared his plate of at least one looming issue.

But in so doing, he may have created another.

Hours before the House passed the spending package Friday morning, hardline House Republicans held a press conference to lambast the bill. Moments after the House narrowly passed the bill, far-right Georgia Republican Rep. Marjorie Taylor Greene filed a motion to oust Johnson.

If ousting a House speaker for budget disagreements feels like a familiar story, that’s because it is.

In October, after former Speaker Kevin McCarthy struck a deal with Democrats to avert a government shutdown, the House voted to remove him, making him the first Speaker in history to be removed from that position. Johnson has been trying to appease the hardline Republican wing of the House, called the Freedom Caucus, to avoid meeting a similar fate.

A new survey says consumers find e-commerce sites often fail to meet expectations. Experts say that’s because shoppers have become accustomed to how Amazon gets things done to their liking.

Source link

Retroactive removal of deduction limits is a giveaway to corporations.

Source link

The Magnificent Seven includes some of the most innovative tech-orientated companies on the market. But what if there was a Magnificent Seven for dividend stocks?

Microsoft (NASDAQ: MSFT), Coca-Cola (NYSE: KO), Procter & Gamble (NYSE: PG), Chevron (NYSE: CVX), Home Depot (NYSE: HD), JPMorgan Chase (NYSE: JPM), and United Parcel Service (NYSE: UPS) represent their industries well and are all top dividend stocks you can count on for decades to come. Here’s why they would make my list for the Magnificent Seven of dividend stocks.

Microsoft is the only Magnificent Seven stock that also deserves to be in the Magnificent Seven of dividend stocks. It is the most valuable company in the world. Microsoft only yields 0.7%, but it pays the most dividends of any U.S.-based company.

Microsoft’s low yield is due to its outperforming stock price, not a lack of commitment to dividend raises. Since fiscal 2019, Microsoft has raised its dividend by 9% to 11% every year like clockwork. The dividend has doubled over the last eight years — a faster growth rate than many of the market’s top dividend stocks.

Microsoft is monetizing artificial intelligence and growing its earnings, paving the way for plenty of future dividend raises. If the stock price languishes, the dividend yield will rise to a much more attractive level. However, Microsoft shareholders would surely prefer outsized gains over a higher dividend yield.

Coke uses its dividend as the primary way to reward faithful shareholders. With a yield of 3.2%, Coke allows investors to collect passive income from a tried and true Dividend King with 62 consecutive annual dividend increases.

Coke is a low-growth business, so investors shouldn’t expect outsized gains from the stock. But this is the Magnificent Seven of dividend stocks, not growth stocks. And when it comes to generating passive income, Coke is as reliable as it gets.

Coke’s consistency is the core reason why Warren Buffett’s Berkshire Hathaway has held the stock for over 30 years.

If it were a decision between Coke and a 10-year Treasury, I’d take Coke all day. The 10-year gives investors another percentage point or so in yield, but with no participation in the market. Of course, no stock is as safe as the risk-free rate, but Coke is close. It’s the ideal investment for risk-averse investors or anyone looking to supplement income in retirement.

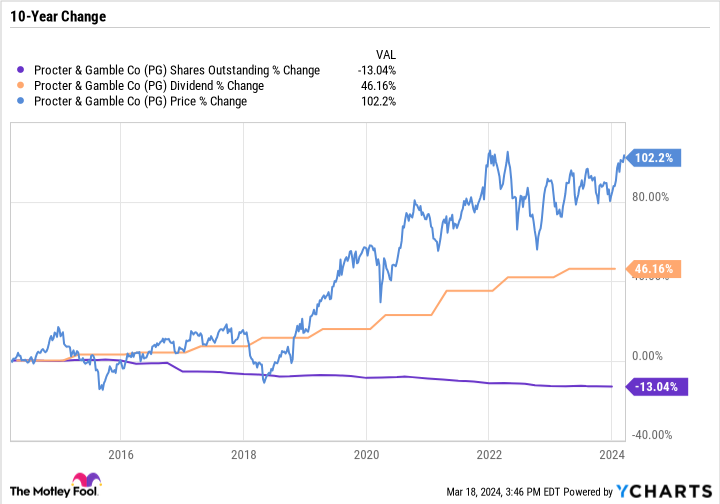

Procter & Gamble has a massive capital return program. It is a great example of a company using dividends and stock repurchases to reward shareholders.

The following chart is one of the prettiest you’ll ever see from a stodgy consumer staple company.

P&G stock has more than doubled over the last decade, the dividend is up over 46%, and P&G has repurchased a considerable amount of stock, reducing its share count by 13%.

P&G may not be the most exciting business, but glitz and glam isn’t the point of this list. When it comes to rewarding shareholders, P&G has done it in many ways and has the business model and brand power needed to continue that streak going forward.

Chevron’s stock buybacks aren’t nearly as consistent as P&G’s. The oil giant tends to buy back more stock during an uptick in the business cycle and pull back on repurchases and capital spending when oil and gas prices fall.

But Chevron’s dividends are as consistent as they come. Chevron has raised its dividend for 37 consecutive years. That means it didn’t cut it during the COVID-19-induced crash, the 2014 and 2015 downturn, or any oil and gas downturn since the late 1980s.

Chevron has the balance sheet, cost profile, and portfolio to continue rewarding shareholders. Its dividend yield of 4.2% makes it one of the higher-yielding reliable stocks out there.

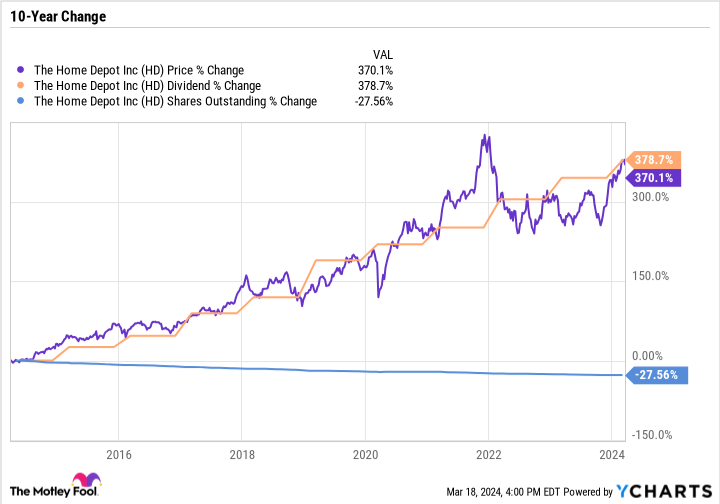

Home Depot has been a perfect dividend stock over the last decade. It has crushed the broader market, and somehow, the dividend has grown at an ever faster rate.

Home Depot has also reduced its share count by over a fourth while expanding the business.

Investors shouldn’t expect this level of growth over the next 10 years, but Home Depot is still a good investment. The company is vulnerable to external factors, such as broader economic cycles, the housing market, the construction industry, and consumer spending. But it is well positioned, and one of the best cyclical dividend stocks to own long term.

Since Nov. 1, JPMorgan is up over 38% — a massive move for such a large, diversified bank. JPMorgan is now worth more than Bank of America, Wells Fargo, and half of Citigroup combined. The Big Four banks have really turned into JPMorgan and the other three.

Banking is a cyclical industry that tends to ebb and flow to the tune of the broader economy. Right now, JPMorgan’s profits are soaring.

Still, what makes the company a good long-term investment, and a worthy addition to the Magnificent Seven of dividend stocks, is that it regularly returns value to its shareholders. Over the last decade, the dividend is up 176%, while the share count is down nearly a fourth.

JPMorgan slashed most of its dividend in 2009 during the fallout of the financial crisis. But since then, it has raised its dividend every year. Today, the dividend is nearly triple what it was pre-cut, and JPMorgan has turned into a quality passive income play.

The recent run-up in the stock price has pushed JPMorgan’s yield down to 2.2%. But the company is at the top of its game and is a good representative of the financials sector in the Magnificent Seven of dividend stocks.

UPS has raised its dividend every year for the last 21 years, except for in 2009, when it kept its dividend flat. The company isn’t the most reliable dividend payer on this list, but it has increasingly used dividends as a key way to reward shareholders.

In 2022, UPS raised its dividend by 49%, a significant increase for its size. Today, UPS yields 4.3%, which is high for an industry-leading industrial company.

UPS is a cyclical business that depends on the strength of the broader economy. Package delivery volumes to businesses are higher during an economic expansion. Similarly, deliveries to consumers are higher when discretionary spending is strong.

Although UPS offers investors a compelling yield, it’s doubtful the company will make as large of raises to its dividend going forward. Still, its current level is quite high, as UPS stock would have to rally about 45% for the yield to fall below 3%.

Microsoft, Coca-Cola, Procter & Gamble, Chevron, Home Depot, JPMorgan Chase, and UPS have track records of dividend raises, solid underlying businesses, future growth prospects, and industry leadership. Many of these companies also reward shareholders with stock repurchases, as well as long-term capital gains for patient investors.

These companies may not always have the highest yields, but they do have earnings growth, which sets the stage for future raises.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for two decades, Motley Fool Stock Advisor, has more than tripled the market.*

They just revealed what they believe are the 10 best stocks for investors to buy right now… and Microsoft made the list — but there are 9 other stocks you may be overlooking.

*Stock Advisor returns as of March 21, 2024

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Wells Fargo is an advertising partner of The Ascent, a Motley Fool company. JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. Citigroup is an advertising partner of The Ascent, a Motley Fool company. Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bank of America, Berkshire Hathaway, Chevron, Home Depot, JPMorgan Chase, and Microsoft. The Motley Fool recommends United Parcel Service and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

If There Was a “Magnificent Seven” for Dividend Stocks, These Would Be My Top Picks was originally published by The Motley Fool

There are still a number of companies in the private market that are potential IPOs — but underwriters will likely take a cautious approach this year.

Source link