The 30-year mortgage rate is averaging at 6.74% Freddie Mac said in its latest weekly survey on Thursday.

Source link

The 30-year mortgage rate is averaging at 6.74% Freddie Mac said in its latest weekly survey on Thursday.

Source link

Late in December, Nvidia Corp. topped a list of favorite stocks among analysts working for brokerage firms. But with the stock continuing to soar this year, running the same screen of the S&P 500 produces a different result, with Nvidia no longer even making the top 20.

Back in December, the great majority of analysts polled by FactSet who covered Nvidia NVDA rated the stock a buy or the equivalent. Before the market opened on Dec. 26, their consensus price target for the stock was $668.11, which was 37% higher than the Dec. 22 closing price of $488.30.

Nvidia’s stock closed out 2023 at $495.22, having risen 239% for the year. So far in 2024, the stock has climbed another 83.5% to close at $908.88 on Wednesday. That is slightly above the new consensus 12-month price target of $904.55 for the stock.

Even though 54 out of 60 analysts still rate Nvidia a buy, the stock has gotten ahead of the analysts’ traditional consensus 12-month price target. That combination of favorable ratings and a target below the current price gives some food for thought: A year isn’t a lengthy period for a committed long-term investor.

Last week, we looked at Nvidia’s price-to-earnings valuation, which has come down significantly over the past year.

Beginning with the S&P 500 SPX, we narrowed the list to 74 stocks with at least 75% buy or equivalent ratings among analysts polled by FactSet.

Here are the 20 remaining stocks in the S&P 500 that are buy-rated by at least 75% of analysts and that have the highest 12-month upside potential indicated by the consensus price targets:

|

Company |

Ticker |

March 13 price |

Consensus price target |

Implied 12-month upside potential |

Share buy ratings |

|

United Airlines Holdings Inc. |

UAL |

$43.04 |

$63.46 |

47% |

77% |

|

First Solar Inc. |

FSLR |

$158.04 |

$226.83 |

44% |

82% |

|

Insulet Corp. |

PODD |

$175.54 |

$237.18 |

35% |

83% |

|

Aptiv PLC |

APTV |

$79.72 |

$103.73 |

30% |

80% |

|

Schlumberger Ltd. |

SLB |

$52.57 |

$68.15 |

30% |

94% |

|

Halliburton Co. |

HAL |

$36.53 |

$47.28 |

29% |

88% |

|

Zoetis Inc. Class A |

ZTS |

$176.23 |

$227.20 |

29% |

88% |

|

MGM Resorts International |

MGM |

$42.86 |

$55.24 |

29% |

80% |

|

Baker Hughes Co. Class A |

BKR |

$31.75 |

$40.55 |

28% |

80% |

|

Lamb Weston Holdings Inc. |

LW |

$102.94 |

$129.15 |

25% |

93% |

|

Carnival Corp. |

CCL |

$16.65 |

$20.88 |

25% |

83% |

|

Delta Air Lines Inc. |

DAL |

$43.91 |

$53.89 |

23% |

96% |

|

VICI Properties Inc. |

VICI |

$29.31 |

$35.78 |

22% |

88% |

|

UnitedHealth Group Inc. |

UNH |

$488.00 |

$595.73 |

22% |

88% |

|

Take-Two Interactive Software Inc. |

TTWO |

$144.89 |

$176.11 |

22% |

77% |

|

News Corp Class A |

NWSA |

$26.35 |

$32.02 |

22% |

78% |

|

Las Vegas Sands Corp. |

LVS |

$53.35 |

$63.95 |

20% |

83% |

|

SBA Communications Corp. Class A |

SBAC |

$219.80 |

$262.36 |

19% |

82% |

|

Teledyne Technologies Inc. |

TDY |

$421.24 |

$500.55 |

19% |

90% |

|

NextEra Energy Inc. |

NEE |

$59.54 |

$70.32 |

18% |

77% |

|

Source: FactSet |

|||||

Click on the tickers for more about each company.

News Corp NWSA is the corporate parent of MarketWatch publisher Dow Jones.

Don’t miss: Alphabet is the bargain stock among the ‘Magnificent Seven’

Also read: Why Japan’s stock market could keep soaring — plus three stock picks there

Packages move along a conveyor at an Amazon fulfillment center on Cyber Monday in Robbinsville, New Jersey, on Nov. 29, 2021.

Michael Nagle | Bloomberg | Getty Images

Amazon will host a spring sale next week with discounts on seasonal items, and this one is not restricted to Prime members.

Amazon said Thursday that the event, which it’s calling the “Big Spring Sale,” will run for six days starting March 20, in North America. Unlike the Prime Day discount bonanza typically held in the summer, next week’s event will be open to shoppers who don’t pay for a Prime membership. The subscription program costs $139 per year, or $14.99 a month, in the U.S., and perks include free, speedy shipping; video streaming; and access to exclusive Prime Day deals.

Spring fashion, fitness products, outdoor furniture, Amazon-branded devices and other “warm weather essentials” are among the categories that will be discounted, Amazon said. It’s the first time Amazon has held such an event in the first quarter.

In recent years, Amazon has added shopping events, including a “Prime Big Deal Days” in the fall, a 48-hour “Pet Day” and a beauty-focused sale ahead of the holiday shopping season.

The company is launching its spring event as shoppers, grappling with high inflation, remain hungry for discounts. Inflation has receded from its 40-year highs in mid-2022, but it remains above the Federal Reserve’s 2% goal. Consumer prices rose more than expected last month, increasing 3.2% in February from a year earlier, the U.S. Department of Labor said Tuesday.

Amazon also faces rising competition from low-cost retailers Temu and Shein, which have been on an ad-spending blitz to attract American shoppers. Shein mostly offers deeply discounted apparel and accessories. Temu is akin to an online flea market and has seen its popularity boom due to its rock-bottom prices and a gamified shopping experience.

Fool.com contributor Parkev Tatevosian discusses why he places this growth stock on his list of top stocks to buy.

*Stock prices used were the afternoon prices of March 11, 2024. The video was published on March 13, 2024.

Parkev Tatevosian, CFA has positions in PayPal. The Motley Fool has positions in and recommends PayPal. The Motley Fool recommends the following options: short March 2024 $67.50 calls on PayPal. The Motley Fool has a disclosure policy.

Parkev Tatevosian is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through his link, he will earn some extra money that supports his channel. His opinions remain his own and are unaffected by The Motley Fool.

He may be the world’s best stock picker. But that doesn’t mean every single one of Warren Buffett’s picks held by Berkshire Hathaway dishes out gains each and every year. And that’s OK — the Oracle of Omaha is in it for the long haul. He likely understands you’re going to take some short-term lumps while waiting for a company’s long-term performance to be reflected in its stock’s price.

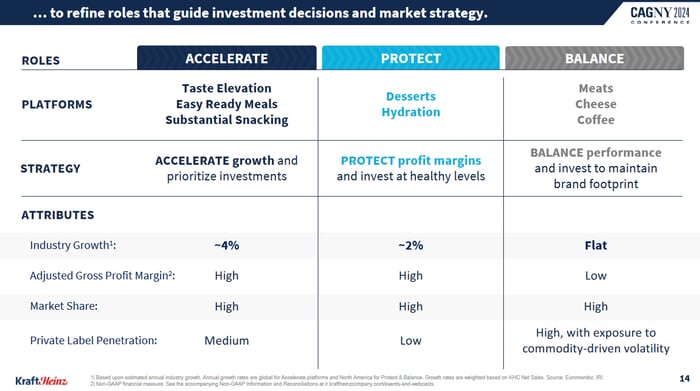

That said, every now and then the proverbial planets align for one of Berkshire’s holdings, setting the stage for a parabolic move. The fund’s position in The Kraft Heinz Company (KHC -0.61%) could be on the cusp of such a move now. Here’s why.

It’s been an uncharacteristically poor performer since Buffett helped orchestrate the merger of food giants Kraft and Heinz back in 2015. Shares have been more than halved since the post-merger stock began trading, in fact, with most of that setback taking shape before the COVID-19 pandemic.

What gives? As it turns out, the anticipated cost savings and competitive edges weren’t so easy to achieve. Supply chain disruptions stemming from the pandemic followed by soaring inflation have held the stock down in the meantime. It’s been so long since the company’s made a truly healthy fiscal showing, in fact, that many investors and analysts may be throwing in the towel now, presuming Kraft Heinz is beyond repair.

But that could be a big mistake. This year could mark the beginning of a long overdue turnaround.

To be clear, there’s still much work to be done. The analyst community is essentially calling for no sales growth this year, with per-share earnings only projected to grow from last year’s $2.98 to $3.04 per share. That’s anything but thrilling.

There are some initiatives that relatively new CEO Carlos Abrams-Rivera is leading, however, that will take time to measurably matter. One of these is a rethinking of the company’s innovation priorities. It’s ramping up its reach into the easy-ready meals and what it refers to as “substantial snacking” categories, for instance, as well as doubling down on taste elevation.

One such development is the creation of a boxed kit allowing consumers to recreate Taco Bell’s Crunchwrap Supreme and Chipotle Chicken Quesadilla at home. The company is also repositioning its popular brands of macaroni and cheese into being meals themselves. These are higher-growth opportunities that Kraft Heinz says could one day account for three-fourths of its revenue, versus less than two-thirds of its sales right now.

The Kraft Heinz Company also understands it must still look beyond food itself to be better. It’s got to spend more efficiently as well. That’s why it’s now using artificial intelligence (AI) to plan its promotional calendar. It’s also getting a better handle on demand forecasting. These efforts are paying off. The company says it’s still on track to realize this year’s target of $2.5 billion worth of new spending efficiencies.

To be fair, at first blush much of what Abrams-Rivera appears to be doing now doesn’t look all that different than what his predecessor, Miguel Patricio, appeared to be doing then. All food companies strive to innovate in order to remain competitive. All companies look for ways to cut costs.

Dig deeper though. Kraft Heinz is emerging from a years-long period of disappointing management followed by an inflation-spurring pandemic. It’s stronger now than it was then, and is certainly more in tune with what consumers as well as its institutional customers actually want.

This includes (among other things) more plant-based eating options like plant-based Oscar Mayer hot dogs in addition to making comfort foods like mac and cheese even more accessible. This is actually the most holistic strategic thinking the company’s demonstrated in quite some time.

Image source: The Kraft Heinz Company’s CAGNY 2024 presentation.

That’s also why analysts expect Kraft Heinz’s top- and bottom-line growth to start showing some measurable acceleration beginning next year.

Do Buffett and Berkshire’s other managers fully understand the turnaround The Kraft Heinz Company is finally piecing together for itself? Maybe. Maybe not. But he certainly sees enough to stick with all 326 million shares of the company Berkshire’s been holding since 2015, when Kraft and Heinz merged. That speaks volumes.

Maybe the dividend has something to do with it. The stock is yielding 4.6% right now, based on a dividend that’s been paid every quarter — even if it hasn’t grown — since the beginning of 2020. Earnings have more than adequately funded the dividend, too. In fact, although the company’s management has made no mention of it, analysts’ projected earnings growth along with Kraft Heinz’s recent cash-flow growth could be setting the stage for a dividend bump in the foreseeable future.

KHC Cash from Operations (Quarterly) data by YCharts

Even if that’s not in the near-term cards, forward progress is. The hard part is the waiting. But there’s still reason to take a shot sooner rather than later. Kraft and Heinz are both iconic brand names the market wants to support. Once enough investors and analysts start seeing a glimmer of hope on the horizon, don’t be surprised to see some real movement in the stock.

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway. The Motley Fool recommends Kraft Heinz. The Motley Fool has a disclosure policy.

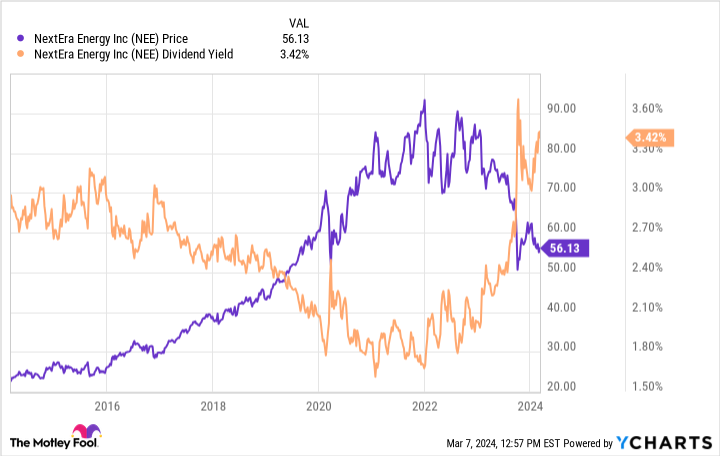

Utilities are conservative income stocks with a reputation for being safe enough to be appropriate for widows and orphans. That’s true for some utilities, but NextEra Energy (NEE 0.55%) bucks the trend (in a good way). While NextEra operates a boring utility, it also owns a rapidly growing renewable power business.

For both growth and income and dividend growth investors, it’s a great stock to consider. And now is a unique opportunity to buy it. Here’s what you need to know.

NextEra Energy’s dividend yield is around 3.5%. That’s basically in line with the utility average, using Vanguard Utilities Index ETF as an industry proxy. While income-focused investors might see NextEra’s yield as modest, it’s important to note that the 3.5% yield is near the highest levels of the past decade. So in this way, the stock looks historically cheap right now.

That said, management expects to increase the dividend by roughly 10% in 2024, which is both attractive on an absolute level and extremely high for a utility. But that’s right in line with the rate of dividend growth over the past decade. The dividend has been increased annually for 29 years, so an increase in 2024 would bring that record up to a cool three decades. NextEra Energy is a dividend growth machine, and there’s no reason to think that the growth is going to come to a halt anytime soon.

Notably, management projects earnings growth of between 6% and 8% a year through 2026. There’s a chance that dividend growth will slow down and simply track along with earnings growth, but even that would suggest an attractive dividend growth rate. This is particularly true of a utility stock.

That’s notable because dividend growth investors and growth and income investors looking to create a diversified portfolio will probably find it hard to add utility exposure. Most stocks in the sector are simply slow-growing on the earnings and dividend fronts. NextEra Energy’s historically high yield and robust growth outlook make the stock an ideal diversification pick for investors looking for something with a little more growth.

The really big reason for NextEra’s high yield is that interest rates have risen. There are two issues for investors to consider here. First, other income options are now more competitive, like certificates of deposit. Second, and more importantly, higher interest rates will make it more expensive for NextEra to grow its business. The utility sector is capital-intensive and makes heavy use of leverage. Don’t get too worried about this.

There are two distinct businesses here to consider. First, NextEra owns Florida Power & Light, which is the largest regulated utility in Florida and about 70% of the utility’s business. The Sunshine State has benefited from population growth for years. More customers mean more revenue and more opportunity to invest in regulated assets. This is a very stable and reliable business, because NextEra has been granted a monopoly in exchange for accepting government oversight of the rates it charges and its capital investment plans. Regulators generally adjust so that utilities can earn a reliable return. Thus, it’s highly likely that the rates NextEra can charge will eventually be updated to account for higher interest rates.

The rest of NextEra is NextEra Energy Resources, one of the largest renewable power generators in the world. This is a fast-growing business with a very long runway for growth as carbon-heavy power sources get replaced by renewable sources like solar and wind. NextEra currently operates around 34 gigawatts of clean energy. It has plans to add as much as 41.8 gigawatts to that total by 2026. This side of the business is not regulated, so higher interest rates will have to be dealt with on a contract-by-contract basis. Market forces are likely to ensure NextEra can profitably grow this side of its business even if there’s some near-term disruption to deal with.

In all, higher interest rates are a headwind. But they’re highly unlikely to change the long-term growth trajectory of NextEra and its dividend.

There’s no such thing as a perfect investment, but the current concerns about NextEra’s growth seem likely to be temporary and, perhaps, a little overblown. That’s an opportunity for investors that think in decades. Growth-and-income and dividend growth-focused investors have the chance to add a reliable utility stock to their portfolios with a historically attractive yield. That’s not something you should pass up without giving NextEra a deep dive.

Fool.com contributor Parkev Tatevosian highlights one stock in Warren Buffett’s Berkshire Hathaway portfolio that investors can buy now and hold for the long run.

*Stock prices used were the afternoon prices of March 11, 2024. The video was published on March 13, 2024.

Should you invest $1,000 in Paramount Global right now?

Before you buy stock in Paramount Global, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Paramount Global wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 11, 2024

Parkev Tatevosian, CFA has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Parkev Tatevosian is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through his link, he will earn some extra money that supports his channel. His opinions remain his own and are unaffected by The Motley Fool.

1 Ridiculously Cheap Warren Buffett Stock Down 89% to Buy Now and Hold Forever was originally published by The Motley Fool

Wall Street offers investors a multitude of pathways to grow their wealth. Among these countless strategies, few have delivered more robust long-term returns than buying and holding dividend stocks.

Last year, researchers at Hartford Funds released a lengthy report that examined the power and potential that dividend stocks bring to the table for long-term-minded investors. In particular, a collaboration with Ned Davis Research revealed a stark disparity in average annual returns between non-payers and companies that regularly pay a dividend.

According to the report (“The Power of Dividends: Past, Present, and Future”), non-payers were 18% more volatile than the benchmark S&P 500 and produced an average annual return of just 3.95% over a half-century (1973-2022). By comparison, companies that paid a dividend were 6% less volatile than the S&P 500 and more than doubled the average annual return (9.18%) of non-payers over the same timeline.

In other words, it’s not a matter of if investors should add dividend stocks to their portfolio, but rather a debate over which income stocks they should buy.

While certainly not everyone’s cup of tea, vice stocks (also known as “sin stocks”) have historically been exceptional dividend payers. Vice companies operate in industries that some investors may view as immoral or undesirable, such as the tobacco or fossil fuel industry. Despite the negative emotions sin stocks can evoke from some investors, they can make those willing to look past their faults considerably richer.

If you’re wanting to generate $600 in super safe annual dividend income, simply invest $5,925 (split equally, three ways) in the following three ultra-high-yield vice stocks, which sport an average yield of 10.15%!

The first high-octane vice stock that can help you bring home $600 in annual dividend income from an initial investment of $5,925 split across three sin stocks is tobacco company Altria Group (NYSE: MO). Altria has raised its dividend 58 times over the last 54 years.

The obvious challenge for tobacco companies is that, over time, consumers have become increasingly aware of the potential dangers of long-term tobacco use. Altria operates in the United States and has seen the percentage of adults smoking cigarettes plummet from 42% in the mid-1960s to just 11.5%, as of 2021. Although a dramatically shrinking pool of customers would normally be a red flag from which no company comes back from, Altria has shown that it has a few tricks up its sleeve.

The core advantage that all tobacco companies enjoy is strong pricing power. Tobacco contains nicotine, which is an addictive chemical. Despite some people quitting tobacco products altogether, those users who continue to smoke cigarettes have demonstrated a willingness to absorb hefty price increases. Even with cigarette shipments declining over time, Altria has been able to modestly move its revenue and profit needle higher by simply raising its prices.

To add to this point, Altria is the company behind the most-popular premium cigarette brand in the United States. Altria closed out 2023 with a nearly 47% share of the entire U.S. cigarette market, including all brands, with Marlboro alone comprising 42.1% of the U.S. market. Being the dominant choice for a lot of smokers makes it easier for Altria to raise its prices.

Altria has also made the move into smokeless products to enhance its long-term growth prospects. After swinging and missing with a sizable investment in electronic-vapor company Juul, Altria looks to have hit a home run with its $2.75 billion acquisition of NJOY Holdings, which closed this past June.

What differentiates NJOY from a veritable sea of e-vapor companies is that it’s received a half-dozen marketing granted orders (MGOs) from the U.S. Food and Drug Administration. Whereas almost all e-vapor products lack MGOs and could, in theory, be pulled from retail shelves at any time, NJOY’s products will remain on retail shelves. This acquisition positions Altria’s growth rate to pick up in the latter-half of the decade.

A second ultra-high-yield sin stock that can help you generate $600 in super safe annual dividend income from a starting investment of $5,925 (split equally) is coal company Alliance Resource Partners (NASDAQ: ARLP). Alliance Resource is currently yielding a jaw-dropping 14.3%!

Entering this decade, most investors had written off coal stocks for dead. It was widely believed that historically low interest rates and the desire for developed countries to reduce their carbon footprints would (pardon the pun) fuel demand for solar and wind projects, among other clean-energy solutions. However, the COVID-19 pandemic changed everything.

For three years during the pandemic, global energy companies dramatically reduced their capital expenditures. We’ve also witnessed a rapid rise in interest rates over the last two years, which had spurred clean-energy projects. The end result has been a slower shift to clean-energy solutions and tight global oil supply. It’s been coal companies like Alliance Resource Partners that have stepped up to meet growing global energy demand.

What’s interesting about Alliance Resource Partners is that it’s not just benefiting from a historically favorable coal price. Management deserves a lot of credit for consistently locking in volume and price commitments up to four years in advance. When the company issued its full-year outlook in late January, it had 93% of its production at the midpoint of its forecast for 2024 priced and committed, along with roughly 45% of its output in 2025. Locking these commitments in ahead of time helps to generate highly predictable operating cash flow year after year.

It’s also worth pointing out that management hasn’t overextended the company’s balance sheet trying to expand production. Alliance Resource Partners has traditionally slow-stepped its expansion efforts to ensure that its outstanding debt remains manageable. This has been critical to sustaining a robust quarterly payout.

Furthermore, Alliance Resource Partners has been diversifying its operations beyond coal and into oil and natural gas royalties. Though royalties are a smaller part of its current operations, it can serve as a smart hedge in the event that coal prices retreat.

The third ultra-high-yield vice stock that can produce $600 in super safe annual dividend income from a beginning investment of $5,925 split equally among three stocks is oil and gas company Enterprise Products Partners (NYSE: EPD). Enterprise has raised its distribution in each of the past 25 years.

For some investors, the memory of the demand cliff for oil companies during the COVID-19 pandemic is still fresh. Drillers were absolutely clobbered by domestic and global lockdowns, which briefly sent crude oil futures contracts into the negative by more than $40 per barrel. Thankfully, Enterprise Products Partners was largely shielded from this historic volatility.

Enterprise’s secret to success is that it’s a midstream company. It’s an energy middleman that oversees more than 50,000 miles of transmission pipeline and can store in excess of 260 million barrels of liquids and refined product.

Whereas upstream drillers tend to be highly dependent on the spot price of crude oil, Enterprise Products Partners relies heavily on long-term, fixed-fee contracts with drilling companies. Fixed-fee contracts remove the impact of inflation and spot-price changes from the equation and make Enterprise’s operating cash flow highly predictable.

It can’t be overstated how important cash-flow predictability is to a midstream juggernaut like Enterprise Products Partners. Being able to accurately forecast its cash flow one or more years in advance is what’s historically given management the confidence the make regular bolt-on acquisitions, as well as put close to $7 billion to work in major infrastructure projects, many of which are aimed at bolstering its natural gas liquids operations.

Enterprise is also benefiting from global crude oil supply constraints. Russia’s ongoing war with Ukraine, coupled with years of global underinvestment from energy majors, is liable to buoy the spot price of crude oil and encourage domestic drillers to increase their production. That’s music to the ears of one of America’s top midstream energy companies.

Should you invest $1,000 in Altria Group right now?

Before you buy stock in Altria Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Altria Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 11, 2024

Sean Williams has no position in any of the stocks mentioned. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

Want $600 in Super Safe Annual Dividend Income? Invest $5,925 Into the Following 3 Ultra-High-Yield “Vice” Stocks. was originally published by The Motley Fool

Shares of fashion brand Fossil Group Inc. jumped 8.5% in after-hours trading Wednesday after Kosta Kartsotis stepped down as chief executive and the company announced a strategic review amid pressure from an activist investor.

Source link

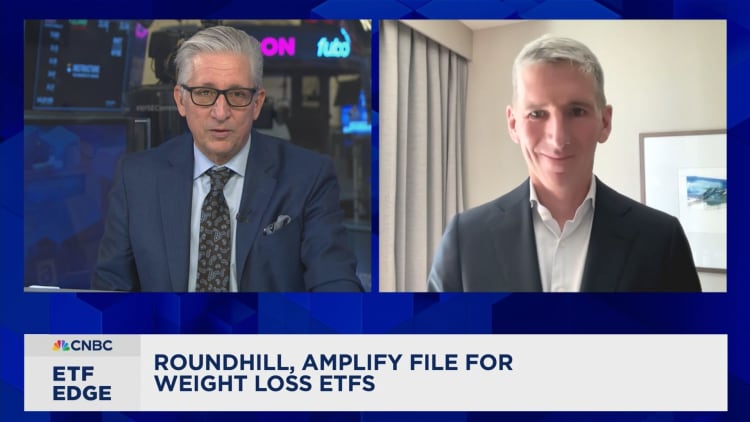

There may be a stronger case to invest in single stocks over exchange-traded funds in the weight loss space.

Amplify ETFs and Roundhill Investments each filed a prospectus last week to launch funds focused on weight loss companies, a move that Strategas ETF and technical strategist Todd Sohn believes hinges on the performance of two dominant stocks: Novo Nordisk (NVO) and Eli Lilly (LLY).

“The main holdings are going to be Lilly and Novo Nordisk, and probably one or two other big names … along with some of the manufacturers down the supply chain,” he told CNBC’s “ETF Edge” this week. “Ultimately, it’s up to those big behemoths that are playing those drugs.”

With just two players currently at the forefront of the U.S. obesity drug market, ProShares’ Simeon Hyman questions the relevance of weight loss ETFs for investors looking to buy into the industry.

“I think that’s one of the challenges whenever you see an innovation like this,” the firm’s global investment strategist said in the same interview. “If the benefits are going to incumbents, then maybe there isn’t a theme per se that needs to be exploited.”

Strategas’ Sohn also suggested that ETFs based on themes, rather than sectors or indices, might be falling out of favor with investors.

“I think thematics are a little bit on the backburner right now, especially the way they performed the last couple of years. I think there’s room for them, but more than one, it’s gonna be tough,” he said.

So far in 2024, Novo Nordisk has gained 29% and Eli Lilly is up 30%, as of Wednesday’s close. The broader Health Care Select Sector SPDR (XLV) is 7% higher during the same period.

Disclaimer