Shares of Fisker Inc. dropped nearly 40% in the extended session Wednesday after a report said the embattled EV maker is exploring a bankruptcy filing.

Source link

Shares of Fisker Inc. dropped nearly 40% in the extended session Wednesday after a report said the embattled EV maker is exploring a bankruptcy filing.

Source link

Pete Maldonado turned his biggest vice into a multimillion-dollar business.

It all started with a late-night poker game — but this isn’t a story about gambling.

In 2011, Maldonado met his future business partner, Rashid Ali, at a friend’s apartment in Chicago. After a couple of betting rounds, their conversation turned to guilty pleasures.

Maldonado immediately thought of his favorite gas station snack, Slim Jims.

Growing up on New York’s Long Island, Maldonado spent countless afternoons biking up the street to the local 7-Eleven and buying a bundle of beef jerky sticks, as many as he could fit in his basket. “I’d finish all of them before I got home,” Maldonado, 42, recalls.

But after becoming a personal trainer in college, he started cutting Slim Jims — with ingredients that include mechanically separated chicken and corn syrup — out of his diet. Still, Maldonado craved his favorite gas station snack.

He told Ali that he wanted to create a “healthier” meat stick that was high in protein, low in calories and tasted just as good as the snack that defined his childhood.

Ali, who was working as a business operations consultant at the time, thought it was a smart pitch — and just a few weeks later, the pair launched Chomps, a “healthier” beef jerky, as a side hustle from Maldonado’s condo in Chicago.

Since then, Chomps has grown into a nationwide brand attracting more health-conscious consumers to the $17 billion meat snacks market, selling more than 350 million jerky sticks to date. Maldonado and Ali, 43, have stayed on as Chomps’ co-founders and co-CEOs.

Here’s how Maldonado and Ali built up Chomps from a side hustle into a company poised to bring in close to $500 million in sales over the next year.

In 2012, after months of sampling hundreds of jerky sticks in stores across Chicago — and begging friends in other states to mail them their favorite meat snacks — Maldonado and Ali found Chomps’ base recipe at a small corner store six hours away in Greentop, Missouri.

One of their friends in Missouri had mailed them meat sticks made by Kevin Western, a Greentop local who made the snacks for fun and sold them around town.

Maldonado and Ali reached out to Western, who agreed to help them develop Chomps’ initial recipe. He also mentioned that his family ran Western Smokehouse, a local smokehouse operator in Greentop, and could help manufacture the products on a larger scale.

“We wanted to use grass-fed beef and remove a lot of ingredients jerky typically uses, like sugar and nitrates, which can create a lot of manufacturing challenges,” says Ali. “A lot of manufacturers didn’t want to deal with those challenges and do the old way of approaching it. But the Westerns were willing to work with us, and together we came up with a recipe that’s similar to the one we still use today.”

Chomps’ main ingredients include grass-fed beef, water, celery powder, sea salt and red pepper.

“I bought a $99 Photoshop Elements subscription and taught myself how to make packaging,” Maldonado says of Chomps’ original packaging. “It was terrible looking, it had a cowhide print on it.”

Photo courtesy of Chomps

The co-founders pooled about $6,500 of their own money to fund Chomps’ first production run, design packaging, build a website and run ads on Facebook.

“I bought a $99 Photoshop Elements subscription and taught myself how to make packaging,” says Maldonado. “It was terrible looking, it had a cowhide print on it.”

In December 2012, Maldonado and Ali started selling Chomps’ first product — the original beef jerky stick — on its website. At launch, the price point was about $2 a stick (now, the sticks cost about $2.49 each).

Much to their surprise, the company started turning a profit “within a month,” says Maldonado, all of which was reinvested into more product and social media marketing.

At first, Maldonado and Ali had full-time jobs and ran Chomps in their spare time for the first couple of years it was in business.

Maldonado, who moved to Naples, Florida in 2013, worked as a real estate agent throughout his 20s and 30s, while Ali stayed in Chicago and continued consulting.

“We took turns hand-packing and shipping orders,” says Ali. “I remember working anywhere from 60 to 80 hours a week as a consultant, then waking up early in the morning or logging off work at 9 p.m. and immediately switching over to Chomps … looking back, I can’t even believe I was able to do that for as long as I did.”

They didn’t expect Chomps to amount to much more than a side hustle, but, as Maldonado jokes, “Chomps had other plans for us.”

In 2013, Chomps’ first full year in business, the pair sold about $50,000 worth of meat sticks. The following year, their sales doubled to $100,000, and the numbers kept climbing from there.

Chomps closed out 2023 with nearly $245 million in retail sales.

Gene Woo Kim

Maldonado credits Chomps’ early success with the rising popularity of different diets including paleo, Whole30 and keto, all of which encourage eliminating ultra-processed foods and replacing them with whole foods like fresh vegetables, meat and fish.

He and Ali started marketing Chomps as a low-carb, sugar-free snack that fit these “healthier” lifestyles, even adding language like “Whole 30 approved” on its packaging.

During its first four years of operation, Chomps sold the snacks directly to consumers through its website, and also to some CrossFit gyms, independent specialty stores and doctor’s offices across the U.S.

Chomps started introducing new flavors in 2013, starting with jalapeno beef. Now, the company offers dozens of spins on the original meat stick, including taco-seasoned beef, pepperoni-seasoned turkey and Italian-seasoned beef.

“A lot of the time, we didn’t even have enough product available on our website because we sold through it so quickly,” says Maldonado. “We’d reach out to people and say, ‘Thank you so much for your purchase. We ran out of product. We’d love to send it to you after if you’ll wait for it. Or we could just refund your money.'”

In 2016, Maldonado and Ali received a phone call that would change their careers — and Chomps’ trajectory.

Trader Joe’s wanted to start selling Chomps’ original beef sticks in all of their stores across the U.S.

“One of the executives’ daughters was doing the Whole 30 diet and discovered Chomps through researching Whole 30 compliant foods,” says Maldonado. “She quickly became a fan of the product and recommended it to the people she knew that were high up at Trader Joe’s, who then reached out to Rashid and me.”

Trader Joe’s placed an initial order for a million meat sticks to stock in over 400 stores. Maldonado and Ali were still running Chomps as a side hustle by themselves at the time, and felt unprepared — but ecstatic — to fulfill such a big order.

“When you grow that quickly, it blows up your entire infrastructure,” says Ali. “You have to think about the business completely differently, and it forced us to do that.”

Maldonado and Ali say their first big order from Trader Joe’s, which requested a million sticks to stock in their stores across the U.S., changed the trajectory of Chomps’ business.

Photo courtesy of Chomps

Up to that point, Maldonado says Chomps produced up to 10,000 pounds of meat each month “at most” to fulfill customer orders. But the Trader Joe’s order alone required at least 120,000 pounds of meat to be produced within weeks. To help them fulfill that massive order, Maldonado says he and Ali ended up renting additional storage space in Chicago and hiring temp workers to hand inspect the products before shipping them to Trader Joe’s.

Chomps started selling meat sticks in Trader Joe’s, its first national retailer, in July 2016. Maldonado quit his real-estate career soon after to work on scaling Chomps from Naples full time, while Ali waited until 2018, when Chomps opened an office in Chicago and hired its first employee, to leave consulting for good.

“I had people saying, ‘You really want to sell meat snacks for a living?'” Maldonado recalls. “We were passionate about it, though, and we had the conviction that this was going to work.”

Once Chomps started selling its sticks in Trader Joe’s, other stores quickly followed, including Whole Foods, Target and Walmart.

Getting into those retailers has given the business a massive boost: In 2020, Chomps’ retail sales hovered around $45 million, but in 2023, it closed out with nearly $250 million in retail sales.

As Maldonado and Ali will tell it, Chomps’ success can be largely attributed to its commitment to attracting a consumer niche that might feel shut out by its competitors: women.

“The meat snacks market is very heavily male-dominated, and other companies are hitting younger male customers,” says Maldonado. “But we did a brand study in 2018 and found that over 70% of our customer base is female, which is not something Rashid and I were ready for, or expecting, by any means.”

Chomps’ strongest demographic, he adds, is women ages 25 to 45, who “really respond” to the snack’s low sugar content and diet certifications.

Chomps re-designed its packaging to appeal more to a female consumer: bright colors, “zero sugar” in large, bold text and an eye-catching slogan in the center (“All stick without the ick”).

Photo: Clint Boland for CNBC Make It

To strengthen that customer relationship, Chomps re-designed its packaging to appeal more to a female consumer: bright colors, “zero sugar” in large, bold text and an eye-catching slogan in the center (“All stick without the ick”).

In 2021, after bootstrapping the company for a decade, Chomps secured their first funding round — an $80 million minority investment — from private equity firm Stride Consumer Partners, which has also helped the business expand.

Chomps now has two offices, one in Naples and one in Chicago, and 78 employees.

Even though Chomps has been in business for more than 10 years, Ali and Maldonado still think of it as a startup, and say they aren’t taking its recent success for granted.

“Pete and I still run the business like it’s a $100,000 business,” Ali says. That means being careful not to overhire, or overexpand production too quickly. Right now, Chomps is available in the U.S. and Canada.

“Running a snack business is a challenge … I describe it as a house of cards,” says Ali. “Like, anything could happen at any point, you could plateau or you could start losing market share. So we have a healthy amount of stress to make sure that we can continue the pressure on moving forward.”

Maldonado has a bit of a sunnier perspective on the future of Chomps. “This whole thing has become so much bigger than we ever imagined … it’s given us a newfound passion for the business,” he says. “Especially after Rashid and I have gotten older, we’re both married now with kids, we’re even more driven now to make a difference in snacking for families like ours … that’s what we’re here to do.”

DON’T MISS: Want to be smarter and more successful with your money, work & life? Sign up for our new newsletter!

Many people worry about their finances, stressing over whether they’re saving enough, spending too much or heading toward a debt crisis.

But several often-overlooked signs may indicate that you’re in better financial shape than you realize. While having a significant nest egg or being debt-free are obvious indicators of financial wellness, there are more subtle clues that your money-management skills are on point.

Don’t Miss:

Are you rich? Here’s what Americans think you need to be considered wealthy.

The average American couple has saved this much money for retirement — How do you compare?

One way to gauge whether you’re in better financial shape than you realize is by looking at your savings account balance relative to national averages. The Motley Fool Ascent survey found that 71% of Americans have $5,000 or less in savings, with 41% having $500 or less set aside.

Specifically, the survey revealed:

11% have $0 in savings

30% have between $1-$500

8% have $500-$1,000

22% have $1,001-$5,000

So if your savings exceed $5,000, you are already outpacing most American households in terms of having a financial cushion. And if your balance tops $10,000, you find yourself in the minority of only 21% of people who have managed to amass a five-figure safety net.

Looking at net worth, which is the total of all assets (retirement accounts, home equity, investments, etc.) minus total debts, can provide perspective. If your net worth exceeds the median level for your age group, it signals you have accumulated more wealth than the typical household in your cohort.

For example, according to the Federal Reserve’s Survey Of Consumer Finances published in October 2023, the median net worth for ages 35-44 is $135,600. For ages 45-54 it’s $247,200. Having a net worth higher than these medians suggests you are ahead of the curve in building up a financial backbone.

Trending: Breaking records, mortgage loans generated $12.25 trillion of household debt nationwide – What are the other major categories of debt?

With a mortgage being most families’ largest debt, having paid down more principal than what remains outstanding is an encouraging sign. Once you owe the bank less than your home’s value, you are positioned with some protective equity.

Nationally, the average mortgage debt is around $241,815, according to Bankrate. If your remaining balance is comfortably below this level, it implies you’ve made serious headway in reducing your housing debt burden.

Experts advise keeping consumer debt payments (student loans, auto loans, credit cards, etc.) below 15% of your gross monthly income. If you meet this threshold, it means you likely have affordable, manageable debt loads that don’t risk putting you in an overly strained cash flow situation.

For the average U.S. household income of around $70,000 per year, 15% would equate to debt payments of less than $875 per month. Lower debt obligations give you more financial breathing room.

A general personal finance rule of thumb is to have enough readily accessible cash savings to cover approximately three to six months’ worth of basic living expenses in case of job loss or income disruption. If your liquid cash reserves allow you to meet at least the lower three-month benchmark, it demonstrates an ability to weather short-term financial hardships.

Based on the average monthly expenditure of $6,081, three months’ worth of expenses would require cash savings of $18,243 to meet the lower benchmark of the three- to six-month rule of thumb for financial preparedness.

Regular contributions to retirement accounts such as a 401(k), individual retirement account (IRA) or another pension plan are indicative of forward-thinking financial planning. Starting early and contributing consistently to your retirement savings can leverage the power of compound interest, significantly impacting your financial security in later years.

A professional advisor can analyze your current savings levels, projected retirement expenses and risk tolerance to determine whether you’re on track to reach your retirement goals or if you need to make adjustments. They can also ensure your investment portfolio is properly allocated and diversified based on your age and retirement timeline.

Making the effort to consult an adviser every few years demonstrates a commitment to objectively assessing your retirement readiness. Small course corrections now can have a significant positive impact down the road versus leaving your retirement planning on autopilot indefinitely.

Read Next:

*This information is not financial advice, and personalized guidance from a financial adviser is recommended for making well-informed decisions.

Jeannine Mancini has written about personal finance and investment for the past 13 years in a variety of publications including Zacks, The Nest and eHow. She is not a licensed financial adviser, and the content herein is for information purposes only and is not, and does not constitute or intend to constitute, investment advice or any investment service. While Mancini believes the information contained herein is reliable and derived from reliable sources, there is no representation, warranty or undertaking, stated or implied, as to the accuracy or completeness of the information.

“ACTIVE INVESTORS’ SECRET WEAPON” Supercharge Your Stock Market Game with the #1 “news & everything else” trading tool: Benzinga Pro – Click here to start Your 14-Day Trial Now!

Get the latest stock analysis from Benzinga?

This article Are You Secretly Doing Better With Your Money Than You Think? Here Are Some Signs You’re Financially Healthy originally appeared on Benzinga.com

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

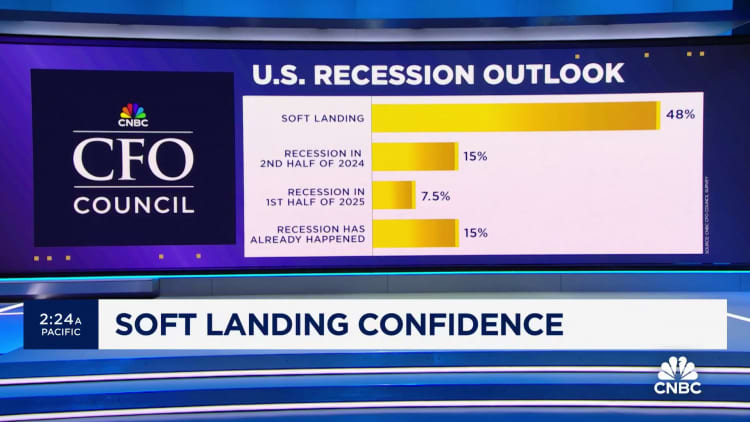

Chief financial officers at large companies see a U.S. economy and equities market that can continue to grow, even as fears about sticky inflation and a potentially overextended, and concentrated, bull run in stocks weigh on investors.

That’s according to the CNBC CFO Council Survey for the first quarter of 2024, which shows a dramatic year-over-year change in the view from CFOs about the Federal Reserve’s inflation battle. The percentage of CFOs who think the Fed will be able to achieve a soft landing has reached a five-quarter high, at 48%. It’s a marked change from where CFOs were a year ago in Q1 2023, with expectations of a soft landing tripling since the first quarter of last year.

For the first time in five quarters, not a single CFO rated the Fed’s efforts to bring inflation down as “poor,” while those who described the central bank’s policy as “good” edged higher again quarter over quarter to 55%.

The latest forecast of long-term inflation expectations came in higher than expected this week, but the market reacted positively to Tuesday’s CPI reading, and stocks closed at a new record after some days of selling. This bullishness despite continued jitters on inflation lines up with the view from CFOs on the council.

CFOs have been consistent across our surveying in their view that inflation will not return to 2% any time soon, and that’s the case again in the Q1 survey, with nearly 80% of CFOs saying inflation won’t hit the Fed’s 2% target before 2025 at the earliest.

This view of inflation remaining above the Fed’s target for considerably longer plays into a CFO outlook that the Fed will not move as quickly as the market thinks to cut interest rates. In recent months, the market has gotten the Fed’s message that March is out of the picture for the start of rate cuts, but CFOs remain more cautious on the Fed. According to the Q1 survey, the largest percentage of CFO respondents (44%) do not expect a rate cut until September. The CME FedWatch tool shows a majority of traders still betting on June as a likely target. In the Q1 CFO survey, equal groups of just under 25% of CFO respondents think the cuts will begin in June or July.

Despite CFOs expecting a slower moving Fed than traders, the latest quarterly view represents an increase in dovish expectations. The greatest swing in the survey’s interest rate outlook comes from CFOs who in the previous quarterly survey had not expected rate cuts to begin before November 2024 at the earliest.

Jerome Powell, chairman of the U.S. Federal Reserve, smiles during a press conference following the Federal Open Market Committee (FOMC) meeting in Washington, D.C., U.S. on Wednesday, May 1, 2019.

Anna Moneymaker | Bloomberg | Getty Images

CFOs don’t see rate anxiety as being a major short-term hurdle for stocks. Over 80% of CFOs believe the Dow Jones Industrial Average is more likely to continue its run up to the 40,000-point mark, with technology continuing to lead the way among sectors, than slip into a bear market.

CFO Council members, as a group, have expressed consistent concerns since the Fed began raising interest rates almost exactly two years ago, in March 2022, in keeping with a typically cautious mindset among chief financial officers and referencing recent economic history and expectations it would be repeated — restrictive monetary policy ultimately leads to a large drop in consumer credit quality and demand that damages the economy and, even if in the short-term the labor market remains solid, ultimately layoffs spiral across sectors before the Fed can reverse course and avoid a recession. Even if unemployment and consumer debt are up, and consumer demand is down, the severity of the damage that CFOs were expecting has obviously not come to pass.

The quarterly CFO survey is a snapshot of views from a select number of chief financial officers at large companies comprising the 100 member-plus council, with 27 members providing responses in Q1.

Some of the C-suite economic confidence may be playing into plans for corporate cash. Buybacks are booming again in 2024 and could reach $1 trillion next year, but there is also evidence of more appetite for deal making to start the year, despite the significant regulatory headwinds and antitrust stance of the Biden administration. Nearly one-third of CFO respondents say strategic M&A will be the top capital spending priority this year, which was the most popular response among CFOs for 2024 capex planning.

The Q1 CFO survey doesn’t come without warning signs for an economy and market that have proven more resilient than many, including CFOs, expected throughout the last year. But the biggest risk cited by CFOs this quarter is also a perennial one for major corporations. Throughout the history of CFO Council polling, consumer demand has most consistently ranked as the No. 1 external risk to business, and it is back at the top of the list now (37%), and at its highest level among risk factors in five quarters.

The U.S. House of Representatives voted Wednesday in favor of a bill that would ban TikTok nationwide if the popular app continues to be controlled by a Chinese parent company.

Source link

There’s no crying in baseball—and no crying in the boardroom either, according to JPMorgan Chase CEO Jamie Dimon.

In his 18 years at the helm of the world’s biggest bank, the Wall Street titan has cemented his reputation as an outspoken thought leader on finance and CEOship—and occasionally, the “pet rock” that is Bitcoin.

When it comes to management, Dimon believes leaders should be willing to dismiss employees who aren’t a good fit—and even he was once on the receiving end of the firing gun.

At a 2017 event at the Stanford Graduate School of Business, a Ph.D. student asked Dimon how he addresses bureaucratization within his bank. Dimon, who turned 68 today, shared what he thought was one of the toughest aspects of management: “You have to get rid of the bad people.”

Sometimes “bad” means a poor culture fit, and other times, it’s as simple as “they’re not good enough” at their job, Dimon said. Many managers are unwilling to get rid of the “bad people,” Dimon continued, and instead opt to reward their loyalty.

In order to achieve a true meritocracy staffed by top performers, Dimon says managers should think more like sports coaches. “In sports, if you’re not batting 250, you’re not going to be playing second base,” the bank chief said. “And it’s very easy, you take out a pitcher that’s not doing a good job.”

“In business, they are left in those jobs for a long time,” said Dimon, whose net worth is $2.1 billion according to Forbes.

“Loyalty is such a misnamed thing sometimes,” Dimon continued at the Stanford event.

As a young CEO, Dimon was asked why he demoted “Joe,” an employee who had been with the company for a long time and trained many other workers.

“How can we be loyal to you when you weren’t loyal to Joe?” an employee asked Dimon. “I couldn’t answer the question,” Dimon said at the Stanford event, so he slept on it and then called the employee the following day.

“If I was loyal to Joe and kept him in the job, and most people thought he just wasn’t doing a good job anymore, who am I being disloyal to?” Dimon recalls saying. “Everybody else and the customer.”

The billionaire was once on the receiving end of a high-profile firing himself—at the hands of a former mentor. While Dimon was an undergraduate at Tufts University, banker and family friend Sandy Weill hired him to spend the summer working at the investment bank Shearson—where Dimon’s father and grandfather both worked as stockbrokers.

After his graduation from Harvard Business School, Dimon followed Weill to American Express—turning down offers from Goldman Sachs, Morgan Stanley, and Lehman Brothers to do so. A few years later, Dimon followed Weill to Commercial Credit. By 1998, a 33-year-old Dimon was president and chief operating officer of Travelers, an insurance company.

“Then we merged with [Citigroup],” he said on the Coffee with the Greats podcast in 2020. Dimon was named Citi’s president following the merger—but a few months later, Weill, who had mentored him for 15 years at this point, asked him to resign during an executive weekend retreat.

“The problem was in 1999 he wanted to be CEO and I didn’t want to retire,” Weill told the New York Times in 2010. “I regret that it came to that. I don’t know what else could have been done except for him to be more patient.”

Though he was surprised by the firing, Dimon said he was “fine.” “It was my net worth, not my self-worth, that was involved,” he said on the podcast.

While out of a job, Dimon took up boxing and read biographies of leaders who had “truly suffered,” the Harvard Business Review reported in 2007. He interviewed for jobs at Amazon and Home Depot, according to CNBC, and became CEO of Chicago-based Bank One in 2000.

JPMorgan Chase acquired Bank One in 2004, and Dimon was named CEO of the bank in 2005—proving patience does pay off, eventually.

Dimon has practiced what he preaches. In 2009, he abruptly ousted Bill Winters, the former co-head of investment banking at JPMorgan. Winters was considered a potential successor to the CEO role—he was even dubbed a member of Dimon’s “SWAT team” in a 2008 Fortune article about the bank’s response to the financial crisis.

The Wall Street Journal reported that Winters became the Dimon to Dimon’s…well, Weill, because he never believed in the universal banking model of combining an investment bank with a traditional lender.

Today, Winters is doing quite well for himself—he was named CEO of British bank Standard Chartered in 2015. In February, the bank reported statutory pretax profit of $5.09 billion and rewarded shareholders with a $1 billion share buyback.

And though Dimon has long joked “five more years” when asked if he plans to step down, it appears JPMorgan is laying the groundwork for what comes after. The bank announced a reshuffle of top executives in January, in order to “position the firm for the future” and “further develop the company’s most senior leaders.”

The front-runners to replace Dimon are widely reported to be Jennifer Piepszak, co-CEO of JPMorgan’s commercial and investment bank; and Marianne Lake, CEO of consumer and community banking. But it remains to be seen whether they’ll have the same baseball coach mentality as Dimon.

This story was originally featured on Fortune.com

Fool.com contributor Parkev Tatevosian evaluates SkyWater Technologies (SKYT -4.69%) stock and lets you know whether investors should buy.

*Stock prices used were the afternoon prices of March 10, 2024. The video was published on March 12, 2024.

Parkev Tatevosian, CFA has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. Parkev Tatevosian is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through his link, he will earn some extra money that supports his channel. His opinions remain his own and are unaffected by The Motley Fool.

Less than three months into 2024, the usual suspects are lifting the stock market higher. The so-called “Magnificent Seven” (Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta Platforms, and Tesla) remain some of the hottest stocks on Wall Street.

But investors want to know which of these stocks, if any, remain screaming buys. Here are the two that I believe still have plenty of gas left in the tank.

Image source: Getty Images.

Topping my list is Amazon. Shares of the e-commerce leader are up 88% over the last 12 months, helping founder Jeff Bezos climb back atop the list of richest Americans.

But what puts Amazon at the top of my list isn’t its recent performance — it’s the company’s long-term prospects.

As the world’s top cloud services provider, Amazon Web Services (AWS) stands to reap enormous benefits from the artificial intelligence (AI) revolution. That’s because developers will look to AWS for support, guidance, and infrastructure to scale their AI-powered applications.

Simply put, hyperscalers like Amazon, Microsoft, Alphabet, and Meta Platforms own a significant portion of data centers globally, with some estimates putting the figure at 40% of overall capacity.

Financially, the effects of the AI revolution are already evident. In Amazon’s most recent quarter (the three months ending on Dec. 31, 2023), the company reported AWS revenue of $24.2 billion, which was up 13% from a year earlier.

Amazon’s new generative AI assistants like Q (a chatbot for businesses) and Rufus (an online shopping assistant) represent opportunities for Amazon to have its own ChatGPT moment. And, with 500 million Alexa-enabled devices already sold, Amazon already has a hardware foothold in many households. It simply needs the software buzz to truly capture the moment.

In any event, Amazon’s combination of fantastic leadership, outstanding financials, and leading market share in cloud services make it a screaming buy in my book.

Yes, Nvidia is still a screaming buy, too. I know that might be hard to believe, with shares recently up an astounding 600% in only 18 months.

However, just like how the result of one coin flip doesn’t impact the outcome of the following one, Nvidia’s unbelievable last 18 months say nothing about where the stock is headed. In a nutshell, past performance doesn’t imply future returns.

There is, however, one interesting trend that potential investors should keep in mind: That’s the company’s valuation. And contrary to what you might think, Nvidia’s shares keep getting cheaper — not more expensive.

In fact, as you can see in the chart below, Nvidia’s forward price-to-earnings (P/E) ratio has decreased by more than 50% over the last three years.

NVDA PE ratio (forward) data by YCharts.

And P/E ratios are volatile because they’re based on either trailing earnings or future earnings estimates — meaning they often soar or collapse around earnings announcements, as you can see in the chart above.

At any rate, Nvidia’s forward P/E ratio has significantly dropped because analysts expect the company to score from rising sales of its graphics processing units (GPUs), which are used to power many of today’s cutting-edge AI applications.

In summary, investors shouldn’t shy away from Nvidia just because its stock has been on a tear. To the contrary, Nvidia’s future looks bright thanks to the skyrocketing demand for AI chips. Granted, its not a stock for every investor. But for those who are willing to buy and hold, Nvidia could still be a screaming buy right now.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Jake Lerch has positions in Alphabet, Amazon, Nvidia, and Tesla. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The “Magnificent Seven” is a group of the world’s largest technology stocks. They delivered an average return of 112% last year, led by Nvidia, which gained a whopping 239%.

Nvidia continues to lead the group higher in 2024, but shares of electric vehicle (EV) giant Tesla (NASDAQ: TSLA) are heading in the opposite direction:

Tesla stock is now trading 57% below its all-time high. The company is suffering from a slowdown in electric vehicle sales — where it generates most of its revenue — which is forcing investors to adjust their growth expectations for the future.

But the head of Ark Investment Management, Cathie Wood, thinks Tesla is more than an EV company. She says it’s the biggest opportunity in the artificial intelligence (AI) space thanks to its industry-leading autonomous self-driving software, and it could propel the company to an astronomical valuation in the future.

Ark’s price target for Tesla stock implies a 1,140% upside over the next three years, but is that realistic?

Tesla delivered a record 1.8 million EVs in 2023, and its Model Y became the best-selling car in the world. However, with consumers struggling under the pressure of elevated inflation and rising interest rates, the company slashed the price of its EVs by an average of 25.1% throughout last year to spur demand.

Given the uncertain economic climate, Tesla chose not to issue a sales forecast for 2024. Investors don’t like uncertainty, and the lack of guidance is a key reason Tesla stock is down in the early stages of 2024. Some analysts believe the company will deliver around 2.2 million cars this year, representing 22% growth compared to 2023. That’s less than half the long-term annual growth target of 50% consistently forecasted by CEO Elon Musk.

There is some concern that demand for EVs is fading across the industry. Late last year, Ford postponed $12 billion worth of investments in its EV operations, citing weak demand. General Motors scrapped a $5 billion deal with Honda to produce an affordable EV model, and the company abandoned its long-standing production forecast for 2024. EV start-up Rivian Automotive issued a very weak production forecast for 2024 while announcing plans to cut 10% of its workforce in February.

In its conference call with investors for the fourth quarter of 2023, Tesla offered investors some details about an affordable EV model it plans to produce starting in 2025. It will feature an entry-level price point of around $25,000 to entice consumers at the lower end of the income spectrum, who would otherwise choose a gas-powered car. It could be an important growth driver for Tesla, but it won’t solve the company’s short-term woes.

Tesla’s revenue came in at a record-high $96.7 billion in 2023, which marked an increase of 19% compared to 2022. Revenue grew much slower than Tesla’s vehicle deliveries, largely because of the price cuts I mentioned.

But those price cuts had an even greater impact on the company’s profitability. Taking in less revenue per EV sale led Tesla’s gross profit margin to decline to 18.2% in 2023, from 25.6% in 2022. As a result, its non-GAAP (generally accepted accounting principles) earnings per share fell 23% to $3.12.

That has serious implications for the valuation investors apply to Tesla stock.

Ark believes Tesla stock could jump to $2,000 per share by 2027, not only because of its EV sales, but also because of its autonomous self-driving software. In 2023, EV sales accounted for 85% of the company’s total revenue, but Ark believes that will shrink to 47% by 2027, with 44% of its revenue coming from that new technology.

Tesla’s self-driving software remains in beta mode, but it completed more than 500 million miles of real-world testing with participating customers. It could eventually transform the company’s economics in a number of ways.

First, Tesla will earn a subscription fee from each customer who buys the self-driving software. Second, Musk says Tesla might consider licensing it to other carmakers. Software typically carries a high gross profit margin of up to 80%, so those two revenue sources could send the company’s earnings skyward once it achieves scale.

Finally, Musk wants to build a self-driving ride-hailing network so Tesla customers can monetize their cars when they aren’t using them. It would operate similarly to Uber, with Tesla earning a split of the revenue in exchange for maintaining the network.

Interestingly, Ark’s forecast doesn’t factor in a revenue contribution from Tesla’s new humanoid robot, Optimus. Sales could begin in 2027, and Musk intends to eventually ship millions of units at $20,000 each, so it could be an enormous opportunity. Optimus could, theoretically, replace many human jobs in industries like manufacturing to enable plants to operate around the clock.

Let’s circle back to Tesla’s $3.12 in earnings per share for a moment. Based on that figure and its current stock price, Tesla trades at a price-to-earnings (P/E) ratio of 56.2.

Therefore, despite the 57% plunge in its stock price since late 2021, Tesla is still nearly twice as expensive as its peers in the tech sector, represented by the Nasdaq-100 index, which trades at a P/E ratio of 32.9.

Ark’s prediction that Tesla stock will jump to $2,000 by 2027 hinges on the company generating $1 trillion in annual revenue by then. In other words, the company’s revenue will have to grow more than tenfold from here, or by 80.2% compounded annually.

Remember, Musk himself is only targeting a 50% annual increase in EV deliveries going forward, and the company will likely fall significantly short of that in 2024. Plus, even though self-driving software could eventually transform Tesla’s economics for the better, it’s still in beta mode, with no firm release date. It’s unlikely mainstream adoption will occur at scale by 2027.

The probability that Tesla stock soars 1,140% to reach $2,000 by 2027 appears low. However, it might still be a great long-term investment on the back of its autonomous driving software, its Optimus robot, and its affordable EV — just not yet.

Investors might do well to buy Tesla stock upon further updates on those fronts — perhaps near the end of this year or in 2025, depending on the company’s progress.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for two decades, Motley Fool Stock Advisor, has more than tripled the market.*

They just revealed what they believe are the 10 best stocks for investors to buy right now… and Tesla made the list — but there are 9 other stocks you may be overlooking.

*Stock Advisor returns as of March 11, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, Tesla, and Uber Technologies. The Motley Fool recommends General Motors and recommends the following options: long January 2025 $25 calls on General Motors, long January 2026 $395 calls on Microsoft, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The Biggest Loser in the “Magnificent Seven” Could Soar 1,140%, According to Cathie Wood’s Ark Invest was originally published by The Motley Fool

The U.S. stock market performed well over the past year. The broad-based S&P 500 advanced 28%, the blue chip Dow Jones Industrial Average gained 18%, and the technology-heavy Nasdaq Composite soared 39%. But patient investors can still find buying opportunities on a budget.

For instance, Cloudflare (NET -0.32%) and Shopify (SHOP 1.85%) trade at reasonable valuations given their future growth prospects, and both stocks were priced at less than $100 per share at the time of writing.

Here’s what makes these businesses worthwhile investments.

Cloud computing specialist Cloudflare provides a broad range of application, network, and security services that accelerate and protect corporate infrastructure and applications across private data centers and public clouds. It also offers compute and storage services through its Workers development platform that empower businesses to build and run applications on its network.

Cloudflare has achieved a strong presence in several relevant verticals due to unparalleled speed and immense scale. It operates the fastest cloud network on the market, and it handles about 20% of all web traffic. That last fact creates an important network effect. The machine learning models that power its platform are continuously fine-tuned using vast amounts of data gleaned from across the internet, improving their ability to route traffic and block threats.

Cloudflare reported excellent financial results in the fourth quarter. Customers rose 17% to 189,791 and the average client spent 15% more. In turn, revenue increased 32% to $362 million and non-GAAP net income jumped 148% to $53 million. Management said close rates and average deal size improved markedly compared to the previous quarter, meaning the company is making progress on improving sales force productivity.

Going forward, Cloudflare has particularly compelling opportunities in developer services and network security services. Forrester Research has called the company a leader in edge development platforms, and International Data Corp. has recognized its leadership in zero-trust network access, citing threat-detection capabilities as a key strength.

With that in mind, the edge computing market is expected to compound by 37% annually through 2030, and the zero-trust security market is forecast to grow by 17% per year during the same period. Meanwhile, Wall Street expects the company to increase sales by 25% annually over the next five years.

That forecast makes Cloudflare’s recent valuation of 25 times sales appear tolerable. Patient investors should consider buying a small position in this growth stock today, with the understanding that shares could be volatile in the near term.

Shopify offers software and services that help merchants manage their businesses across physical and digital storefronts. Its software integrates with e-commerce marketplaces like Amazon and social media like TikTok, as well as direct-to-consumer websites and mobile apps. Ancillary services include financial solutions, fulfillment support, and tools for cross-border commerce and wholesale.

Shopify reported strong financial results in the fourth quarter, beating estimates on the top and bottom lines. Sales increased 24% to $2.1 billion due to strong growth in subscription and merchant services revenue. Meanwhile, non-GAAP net income more than quadrupled to reach $441 million due to cost-control efforts, including head count reductions and the sale of its capital-intensive logistics business.

Shopify shares fell following the fourth-quarter report as a result of light guidance, but investors should view the pullback as a buying opportunity. Shopify is the market leader in e-commerce and omnichannel commerce software, and the second-largest e-commerce company in the U.S. That tells me Shopify is ideally positioned to benefit as consumers spend more online. Indeed, the company ranked no. 16 on the Fortune Future 50 List for 2023, an annual evaluation of the world’s largest companies based on their long-term growth prospects.

Beyond retail, Shopify has added wholesale e-commerce tools to its enterprise-grade platform, Shopify Plus. That significantly expands its addressable market because wholesale e-commerce sales exceed retail e-commerce sales by a factor of three. While it’s too soon to make any firm judgments, Shopify reported strong momentum in wholesale last year, with gross merchandise volume climbing nearly 150% in the fourth quarter.

Going forward, Grand View Research expects retail e-commerce sales to grow by 11% annually through 2030, while wholesale e-commerce sales are forecast to increase by 18% per year during the same period. But Wall Street expects Shopify to expand more quickly. The consensus among analysts calls for annual revenue growth of 22% over the next five years. In that context, its current valuation of 14 times sales seems quite reasonable. Patient investors should feel comfortable buying a small position in this growth stock today.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Trevor Jennewine has positions in Amazon and Shopify. The Motley Fool has positions in and recommends Amazon, Cloudflare, and Shopify. The Motley Fool has a disclosure policy.