Berkshire Hathaway’s Class A stock is trading at a wider-than-usual 2.5% premium to the company’s Class B stock after moving more than a half percentage point Monday.

Continue reading this article with a Barron’s subscription.

Berkshire Hathaway’s Class A stock is trading at a wider-than-usual 2.5% premium to the company’s Class B stock after moving more than a half percentage point Monday.

Continue reading this article with a Barron’s subscription.

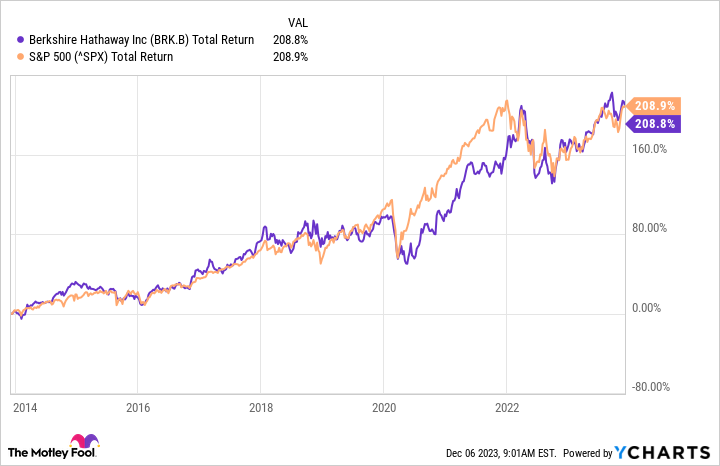

Berkshire Hathaway CEO (BRK.A -0.18%) (BRK.B -0.33%) Warren Buffett has a well-earned reputation as one of the world’s best business pickers. From 1965 to 2022, Buffett’s business acumen helped Berkshire’s shares deliver an astounding compound annual return of 19.8%.

If you bought a fund tracking the benchmark S&P 500 and reinvested the dividends over this period, you’d still only end up with an average compound annual return of 9.9%. That’s a testament to Buffett’s uncanny skill as an investor.

Nonetheless, the Oracle of Omaha himself has often said that most investors should simply buy a low-cost index fund that tracks the S&P 500 and call it a day. In Berkshire’s 2013 annual letter, for instance, he specifically recommended the Vanguard 500 Index Fund (VOO 0.47%) for its low fees and nearly identical performance to its benchmark index.

Image Source: Getty Images.

Should investors heed Buffett’s advice or is Berkshire stock still a better growth vehicle than this popular indexed exchange-traded fund (ETF)? Let’s dig deeper to find out.

Berkshire is a diversified conglomerate that has investments in various sectors, such as insurance and energy, technology, and consumer goods, as well as large holdings of U.S. treasuries, U.S. and foreign equities, and a lot of cash. Its stock is designed to withstand both unforeseen economic shocks and normal economic downturns that occur in business cycles.

However, Berkshire does face some unique challenges due to its girth. The company has struggled to find attractive opportunities that can move the needle for its massive portfolio since the turn of the century. As a result, its stock has lagged behind the market at times over this period.

Buffett and analysts alike have acknowledged this reality and pointed to the company’s size as a limiting factor. This is a key reason Apple has become the dominant position in Berkshire’s stock portfolio in recent years, as it’s one of the few growth companies that can match its scale.

Over the last 10 years, Berkshire stock hasn’t been able to produce higher returns on capital than the S&P 500 because of its size problem and its lack of a dividend. Dividend payments allow investors to amplify capital gains over time through the power of compounding. Buffett’s holding company has also underperformed the VOO over the past five years by nearly 15%, and most analysts expect this trend to continue for the foreseeable future.

BRK.B Total Return Level data by YCharts.

At this stage in its history, Berkshire is more of a defensive play against market volatility, rather than a top-notch capital-appreciation vehicle. During short periods, the conglomerate’s shares will likely do better than the broader markets because of its safety factor. It should also consistently generate positive net returns over the long term, which isn’t an easy thing to do.

However, most investors would be smart to follow Buffett’s advice and go with the VOO as a low-cost and tax-efficient way to grow capital over long periods. Still, Berkshire’s stock could play an important role in a well-diversified portfolio as a hedge against economic and geopolitical risks, as well as other black-swan-type events.

George Budwell has positions in Apple and Vanguard S&P 500 ETF. The Motley Fool has positions in and recommends Apple, Berkshire Hathaway, and Vanguard S&P 500 ETF. The Motley Fool has a disclosure policy.

A web3 membership designed to empower you with cutting-edge insights and knowledge. Learn more ›

Welcome! 👋 You are connected to CryptoSlate Alpha. To manage your wallet connection, click the button below.

If you don’t have enough, buy ACS on the following exchanges:

Access Protocol is a web3 monetization paywall. When users stake ACS, they can access paywalled content. Learn more ›

Disclaimer: By choosing to lock your ACS tokens with CryptoSlate, you accept and recognize that you will be bound by the terms and conditions of your third-party digital wallet provider, as well as any applicable terms and conditions of the Access Foundation. CryptoSlate shall have no responsibility or liability with regard to the provision, access, use, locking, security, integrity, value, or legal status of your ACS Tokens or your digital wallet, including any losses associated with your ACS tokens. It is solely your responsibility to assume the risks associated with locking your ACS tokens with CryptoSlate. For more information, visit our terms page.

Bitcoin has become one of the top 10 assets in the world by market cap. This places it higher than Tesla, Visa, and Berkshire Hathaway stock.

Crypto watchers might remember that a few years ago, Bitcoin was declared the top-performing asset of the 2010s, even beating out competitors like gold and stocks like Apple Inc (NASDAQ: AAPL). Now, it seems history is repeating itself, according to Infinite Market Cap, a platform that tracks the market capitalization of thousands of assets.

As per Infinite Market Cap, Bitcoin has overtaken the likes of Tesla Inc (NASDAQ: TSLA) and Berkshire Hathaway Inc (NYSE: BRK.B) to enter the top 10 assets in the world by market cap. This puts it in the same league as Amazon.com Inc (NASDAQ: AMZN) stock and even gold.

Bitcoin, like most of the crypto industry, is currently recovering from a harsh crypto winter. In April of last year, the price of Bitcoin dipped below $40,000 per token and even below $20,000 at several points. This could be put down to general market swings, as well as several high-profile industry collapses of last year, including Terra and FTX. These created an air of tension in the industry and as the prices of cryptos fell across the board, many companies were forced to lay off staff and scrap upcoming projects.

Now, Bitcoin has risen above the $41,000 mark and some experts are eyeing the $100,000 point by sometime next year. This optimism has been triggered by the incoming Bitcoin halving, which historically signals a spike in the token price. There is also the Bitcoin ETF application that has been pursued by the industry for years but seems to be on the brink of approval.

As of this article, Bitcoin has a market cap of $818.3 billion, which is just under Meta’s market cap of $834.76 billion. Its closest competitor is Berkshire Hathaway stock, which has a market cap of $777.3 billion.

It is quite telling that Bitcoin has been able to recover from a winter that lasted for several months. Every time that the price of Bitcoin has dipped, critics rush to declare cryptocurrency dead as a whole. But once again, Bitcoin has come out of its winter and seems to be on a path to even surpassing its previous all-time high. This shows the resilience of the token and should boost investor confidence.

It is also very telling that Bitcoin’s market capitalization has risen so high that is in the same category as gold, silver, and Amazon stock only a decade into its existence.

If this current trajectory continues, we can expect that not only will Bitcoin end this decade as one of the highest-performing assets as it did last time but this success should also trickle down to other tokens in the industry.

next

Bitcoin (BTC), the original cryptocurrency, is gaining momentum versus global large-cap stocks, overtaking the market value of American conglomerate Berkshire Hathaway. Its market cap breached $800 billion on Dec. 4 after nudging past billionaire investor Warren Buffet’s company on Dec. 3.

As Bitcoin surged past $40,000 over the weekend, its market cap rose to above $780 billion, just beating out Berkshire Hathaway’s $779 billion market cap it closed the market with on Dec. 1 (based on its class A stock, BRK.A).

BRK.A has seen a slight decline recently, slipping around 1.3% over the past five days. Despite the recent drop, Berkshire Hathaway is still up 4.7% over the past 30 days and 14.7% year to date (YTD).

The volatility of BRK.A is nowhere near that of Bitcoin, which has surged 20% over the past month and almost 150% YTD, according to data from CoinGecko. The cryptocurrency has been steadily hitting multimonth highs recently, surpassing $41,000 on Dec. 4 for the first time since April 2022.

At the time of writing, Bitcoin’s market cap amounts to $811 billion, or 4% higher than the market value of Berkshire Hathaway. Founded in 1839, Berkshire Hathaway is a multinational holding firm headquartered in Omaha, Nebraska, in the United States. Berkshire’s main business is insurance, from which it invests in a big portfolio of companies, including Bank of America and Apple.

Cryptocurrency lawyer John Deaton took to X (formerly Twitter) to comment on the news. “That’s a pretty damn big bottle of rat poison,” Deaton wrote, referring to the words of Berkshire Hathaway CEO Buffett, who famously called Bitcoin “rat poison squared” in 2018.

Related: Bitcoin tops $40K for first time in 19 months, Matrixport tips $125K in 2024

According to data from CompaniesMarketCap, Bitcoin is now the 10th-biggest asset by market cap, following Meta Platforms (formerly Facebook) and Nvidia, whose market value currently stands at $834 billion and $1.2 trillion, respectively.

With Bitcoin’s market cap surging past $800 billion, the cryptocurrency is now 38% short of its all-time high $69,000 price posted in November 2021.

The current bullish action could wind up marking the second time in the history of Bitcoin that its market capitalization reaches $1 trillion. Bitcoin previously broke the $1 trillion market cap in February 2021 at $53,700.

Magazine: Bitcoin ETF race has a new player, Binance ends support for BUSD, and more: Hodler’s Digest: Nov. 26 – Dec. 2

Charlie Munger’s death will likely put pressure on Berkshire Hathaway Inc. Chairman Warren Buffett to provide more detail about the investing activity of two key understudies.

“You begin a pivot to Todd Combs and Ted Weschler,” Bill Smead, chief investment officer at Smead Capital Management, a longtime Berkshire shareholder, said in a phone interview. Combs and Weschler together run about 10% of Berkshire’s $350 billion investment portfolio.

While Berkshire remains the 93-year-old Buffett’s show, a lack of detail around the performance and approach of Combs and Weschler has been a frustration, Smead said. That will likely change as Munger’s absence leaves a huge “void.”

“They will become Buffett’s alter ego rather than Munger,” he said.

See: Charlie Munger’s death ends partnership with Warren Buffett that built Berkshire Hathaway

Smead said that could mean a role for the pair at Berkshire’s annual meeting in Omaha, where Buffett and Munger famously held court each May in hourslong question-and-answer sessions that informed and delighted shareholders and, in recent years, a worldwide audience.

Buffett and Munger “were generous and open” about their investing process, Smead said. While Combs and Weschler appear to be excellent stock pickers who share their mentors’ mindset, they remain something of a mystery, he said.

A Berkshire Hathaway representative said it was too soon to say what changes may be in store for the annual meeting.

Munger, 99, died Tuesday at a California hospital, Berkshire Hathaway announced Tuesday afternoon. Buffett and Munger were known to talk by phone for hours a day. Buffett, 93, often described Munger as his “right-hand man,” who helped shape Berkshire’s investing approach.

Berkshire shares were little changed Wednesday. Class A shares

BRK.A,

were up 0.1% on Wednesday, while Class B shares

BRK.B,

rose 0.2%. Berkshire shares are up nearly 17% so far in 2023, versus a gain of more than 18% for the S&P 500

SPX.

Munger’s death didn’t take Berkshire Hathaway shareholders by surprise, but the end of perhaps the most significant partnership in the history of modern investing inevitably raises important questions for investors.

“My feeling is that Berkshire is not going to be able to replace Charlie Munger and nor do I anticipate they’re going to try,” said Cathy Seifert, an analyst at CFRA Research, who has a buy rating on Berkshire Hathaway.

But the long-serving vice chairman was such a crucial element to the success of Berkshire Hathaway that investors in the near-term will likely be looking for any sign the loss is having an impact on Buffett, she said in a phone interview.

Seifert, in a client note late Tuesday, said that Munger’s passing “could test (to a degree) transition plans Berkshire established several years ago, though we do not expect any significant issues to arise.”

Berkshire in 2021 confirmed that Greg Abel, who oversees Berkshire’s noninsurance operations, will be Berkshire’s post-Buffett CEO. Aijit Jain is expected to continue running the insurance businesses after Buffett leaves the scene, while Combs and Weschler are expected to head up investment operations, according to Barron’s.

Investors should also pay attention to appointments to Berkshire’s board after a number of recent departures, Seifert said. She expects there to be pressure to add more diverse members to the board.

Opinion: Who will say no to Warren Buffett now that Charlie Munger is gone?

In Q3, Berkshire Hathaway (BRK.A -0.00%) (BRK.B 0.24%) sold $7 billion worth of public equity holdings, including its entire stake in United Parcel Service (UPS 0.85%).

Let’s look at how meaningful the sale was to Berkshire, its exposure to the transportation industry, and whether you should follow Berkshire’s lead and sell the dividend stock too.

Image source: Getty Images.

UPS has always been one of the most peculiar Berkshire holdings because of the position sizing.

In Q2, Berkshire held just 59,400 shares of UPS. At the time of the filing, the position was worth $10.6 million, just 0.03% of Berkshire’s public equity portfolio and the smallest holding of 48 securities. UPS has long been a Buffett stock on a technicality rather than a meaningful position.

In his 2020 annual letter to Berkshire shareholders, Buffett called Berkshire’s 100% ownership of BNSF Railway one of the company’s “Big Four” assets, along with its then 91% ownership (now 92% ownership) of Berkshire Hathaway Energy, its then-5.4% ownership of Apple, and most importantly, its property/casualty insurance business.

BNSF Railway made Berkshire $5.9 billion in profit last year. Slapping a conservative 15 multiple on the business would make it worth $88.5 billion. A 22 multiple would make it worth around as much as UPS, which has a market cap of $127.4 billion.

Berkshire has a lot of exposure to the transportation industry through BNSF — not the package delivery industry per se, but certainly the transportation of goods and the vulnerabilities that come with an industry so closely tied to the ebbs and flows of the economy.

This exposure may partially explain why UPS may never amount to a meaningful position in Berkshire’s portfolio. On top of that, Berkshire probably thought that other companies were a better deal than UPS. After all, UPS had a higher price-to-earnings ratio than Apple when Buffett began buying it in 2016. And in 2021 and 2022, Berkshire went on an oil and gas buying spree, namely through Chevron and Occidental Petroleum.

All told, it makes sense why Buffett and his team decided to seek other opportunities.

UPS has been hit hard by slowing package delivery volume, paired with labor negotiations that resulted in $500 million in up-front expenses, among other costs.

The company is used to going through economic cycles. And it’s worth noting that UPS is coming out of its biggest boom in company history, a boom that saw all-time high operating margins paired with a blistering top- and bottom-line growth rate.

Zoom out, and UPS has been doing well, with the stock up over 50% in the last five years, trailing-12-month revenue up 29.5%, and normalized diluted earnings per share up 38.1%. And that’s even after this year’s slowdown in the business.

UPS Revenue (TTM) data by YCharts

UPS continues to make major investments in expanding routes, improving its logistics, and increasing the efficiency of its operations through technology. It also gets a larger share of revenue from healthcare and small and medium-sized businesses than ever before, which is making its business more diversified and resilient to a downturn.

The company’s ability to invest even during a downturn, while also turning a healthy profit, shows that UPS doesn’t go through the epic booms and crushing busts of other cyclical stocks, but rather can benefit from an economic expansion while also putting up decent results during a contraction.

In addition to investing through a downturn, UPS also has the free cash flow and balance sheet capable of supporting its sizable dividend. UPS paid $4.08 per share in dividends in 2021 before implementing a whopping 49% raise in 2022 and then raising the dividend by another $0.10 per share per quarter in 2023 — putting the quarterly dividend at $1.62 per share. The sizable raises places UPS in an elite category of high-quality, high-yield dividend stocks, as the stock currently yields 4.4%.

UPS made the dividend raises, largely as a result of its incredible performance during the worst of the pandemic. Investors shouldn’t expect huge raises in the years to come. But even if UPS just maintains its dividend for a while, it still sports a yield around three times the S&P 500. UPS’s dividend yield is also coincidently the same as the 10-year Treasury rate of 4.4%.

UPS is a good choice for investors who want the passive income available from a risk-free asset like the 10-year Treasury but who are also comfortable with the risks and potential reward that comes from investing in the stock market.

UPS may be in for some near-term challenges. But the business has laid a foundation that is built to last. And its dividend provides a sizable incentive to hold the stock through periods of volatility.

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple and Berkshire Hathaway. The Motley Fool recommends Chevron, Occidental Petroleum, and United Parcel Service. The Motley Fool has a disclosure policy.

ProPublica reported Thursday that Warren Buffett may have violated Berkshire Hathaway’s ethics policies.

Leaked IRS data seen by ProPublica showed that Buffett sold shares in stocks that Berkshire was trading.

Buffett has previously said that trading the same stocks as Berkshire would pose a conflict of interest.

Legendary investor Warren Buffett may have violated Berkshire Hathaway’s ethics policies — which he himself wrote — by personally trading the same stocks as the conglomerate, according to a ProPublica report on Thursday.

While changes in Berkshire’s stock portfolio are closely watched by investors, Buffett has largely been quiet about his personal holdings.

But leaked IRS data obtained by ProPublica show that in the last two decades he made trades in his personal portfolio on the same companies that Berkshire bought or sold during the same quarter or the quarter before.

The company did not immediately respond to Insider’s request for comment. Buffett also didn’t respond to ProPublica’s request for comment.

Berkshire’s ethics policies say “all actual and anticipated securities transactions of Berkshire” have to be publicly disclosed before company employees can personally trade those stocks.

And Buffett himself has said previously that he “can’t be buying what Berkshire is buying,” and that doing so would present a conflict of interest.

Yet ProPublica reported that Buffett made at least $466 million in personal stock sales between 2000 and 2019, though the records it viewed didn’t include securities he bought and held.

Here are the three stock sales ProPublica uncovered:

On April 24, 2009, Buffett sold $20 million worth of Wells Fargo shares in his personal account. ProPublica didn’t specify a particular transaction Berkshire made in the stock but noted the company was already a large shareholder.

In August 2009, Buffett personally sold $25 million in Walmart stock. It’s not clear which came first, but that same quarter, Berkshire roughly doubled its stake in the retailer.

In October 2012, Buffett privately sold $35 million of Johnson & Johnson shares, which Berkshire also sold. A filing at the end of the quarter did not specify a date. The conglomerate later sold millions more shares in the subsequent two quarters.

Read the original article on Business Insider

(Bloomberg) — Occidental Petroleum Corp. bought back $522 million of Berkshire Hathaway Inc.’s preferred stock in the second quarter, demonstrating its willingness to repay Warren Buffett even as commodity prices drop.

Most Read from Bloomberg

The purchase brings Occidental’s redemptions this year to 12% of Berkshire’s initial $10 billion investment, which was used to fund the producer’s acquisition of Anadarko Petroleum Corp. in 2019. Berkshire’s preferred stock carries an 8% annual dividend, making it an expensive part of Occidental’s capital structure.

Separately, Berkshire owns 25% of Occidental’s common stock and is the company’s largest shareholder, according to data compiled by Bloomberg. Berkshire is willing to buy more Occidental common stock, Buffett said at its shareholder meeting in Omaha earlier this year. However, he ruled out buying the oil producer in its entirety.

Occidental shares dropped as much as 2.7% in after-market trading as the company missed analysts’ earnings estimates because of weaker realized prices for its gas production. The company raised its 2023 production guidance 1.3%, but also reported higher capital spending than expected.

Most Read from Bloomberg Businessweek

©2023 Bloomberg L.P.