Oil prices probably won’t spike, but buy the yen if they do.

Source link

Oil prices probably won’t spike, but buy the yen if they do.

Source link

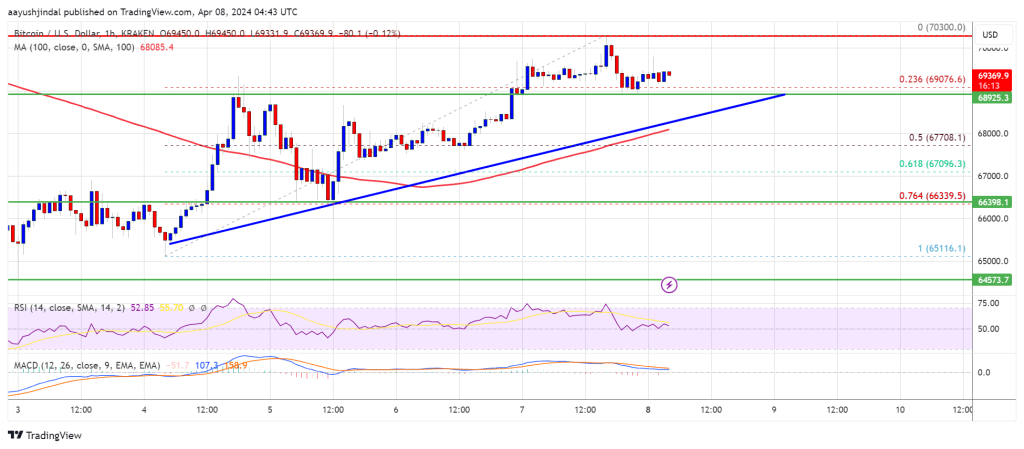

Bitcoin price is showing a few positive signs above the $68,500 resistance. BTC must settle above the $70,000 resistance to continue higher in the near term.

Bitcoin price started a decent increase above the $67,500 resistance zone. BTC cleared the $68,500 and $68,800 resistance levels to move into a positive zone.

The price even spiked above the $70,000 resistance zone. A high was formed near the $70,300 level and the price is now correcting gains. There was a move below the $70,000 level. There was a move below the 23.6% Fib retracement level of the upward move from the $65,116 swing low to the $70,300 high.

Bitcoin is now trading above $68,000 and the 100 hourly Simple moving average. Immediate resistance is near the $69,800 level. The first major resistance could be $70,000.

Source: BTCUSD on TradingView.com

The next resistance now sits at $70,300. If there is a clear move above the $70,300 resistance zone, the price could start a fresh increase. In the stated case, the price could rise toward $71,200. The next major resistance is near the $72,000 zone. Any more gains might send Bitcoin toward the $73,500 resistance zone in the near term.

If Bitcoin fails to rise above the $70,000 resistance zone, it could start a downside correction. Immediate support on the downside is near the $69,000 level or the trend line.

The first major support is $67,800 or the 50% Fib retracement level of the upward move from the $65,116 swing low to the $70,300 high. The next support sits at $66,500. If there is a close below $66,500, the price could start a drop toward the $65,350 level. Any more losses might send the price toward the $62,500 support zone in the near term.

Technical indicators:

Hourly MACD – The MACD is now losing pace in the bullish zone.

Hourly RSI (Relative Strength Index) – The RSI for BTC/USD is now near the 50 level.

Major Support Levels – $68,800, followed by $67,800.

Major Resistance Levels – $69,800, $70,000, and $71,200.

Disclaimer: The article is provided for educational purposes only. It does not represent the opinions of NewsBTC on whether to buy, sell or hold any investments and naturally investing carries risks. You are advised to conduct your own research before making any investment decisions. Use information provided on this website entirely at your own risk.

Spot bitcoin exchange-traded funds (ETFs) concluded the week on an upbeat note, securing $203 million in positive inflows on Friday, as per the latest data. Despite an initial setback of $84.7 million in net outflows on April 1, the ETFs have since rebounded, gathering $569.4 million in net inflows. Bitcoin ETFs Overcome Early April Setback […]

Spot bitcoin exchange-traded funds (ETFs) concluded the week on an upbeat note, securing $203 million in positive inflows on Friday, as per the latest data. Despite an initial setback of $84.7 million in net outflows on April 1, the ETFs have since rebounded, gathering $569.4 million in net inflows. Bitcoin ETFs Overcome Early April Setback […]

Source link

After four days of consecutive inflows, the U.S. spot bitcoin exchange-traded funds (ETFs) experienced a downturn, with $85.7 million flowing out during Monday’s trading hours. U.S. Spot Bitcoin ETFs’ Momentum Halted With $85.7M in Outflows, Spotlight on GBTC Between March 25 and March 28, 2024, the U.S. spot bitcoin ETFs enjoyed an upward trend, amassing […]

After four days of consecutive inflows, the U.S. spot bitcoin exchange-traded funds (ETFs) experienced a downturn, with $85.7 million flowing out during Monday’s trading hours. U.S. Spot Bitcoin ETFs’ Momentum Halted With $85.7M in Outflows, Spotlight on GBTC Between March 25 and March 28, 2024, the U.S. spot bitcoin ETFs enjoyed an upward trend, amassing […]

Source link

A web3 membership designed to empower you with cutting-edge insights and knowledge, powered by Access Protocol. Learn more ›

Welcome! 👋 You are connected to CryptoSlate Alpha. To manage your wallet connection, click the button below.

If you don’t have enough, buy ACS on the following exchanges:

Access Protocol is a web3 monetization paywall. When users stake ACS, they can access paywalled content. Learn more ›

Disclaimer: By choosing to lock your ACS tokens with CryptoSlate, you accept and recognize that you will be bound by the terms and conditions of your third-party digital wallet provider, as well as any applicable terms and conditions of the Access Foundation. CryptoSlate shall have no responsibility or liability with regard to the provision, access, use, locking, security, integrity, value, or legal status of your ACS Tokens or your digital wallet, including any losses associated with your ACS tokens. It is solely your responsibility to assume the risks associated with locking your ACS tokens with CryptoSlate. For more information, visit our terms page.

Rivian Automotive (RIVN -2.52%) stock has bounced off a recent low, but the electric vehicle (EV) maker’s shares are still down by more than 45% this year. That’s because investors see several signs that EV demand has slowed. The big blow to Rivian stock came after the company released its outlook for 2024.

Management said it plans to produce just 57,000 EVs, or about the same number of units it made in 2023. That’s not what investors wanted to hear from what they considered a growth investment. But two weeks after that announcement, Rivian shocked the market with several news items, including a new plan that would save it more than $2 billion. Now investors want to know if Rivian stock is a bargain after its decline.

The latest news from Rivian came at a launch event on March 7 for its R2 next-generation EV platform. As expected, management unveiled its new mid-size SUV that it previously said would be a lower-priced option thanks to new efficiencies from the R2 design platform.

The new R2 SUV will also be priced about $30,000 lower than Rivian’s R1S. The $45,000 base price should bring in more potential customers. It also will have a battery range of over 300 miles and will accelerate from zero to 60 miles per hour in under three seconds. Shipments are expected to begin in early 2026.

The new R2 SUV will have a starting price of $45,000. Image source: Rivian Automotive.

But two additional announcements shocked investors and sent Rivian’s stock higher. Rivian introduced a crossover SUV model dubbed R3 that will follow production of the R2. That should give investors confidence that Rivian has a concrete plan to expand its potential market. Thus far, the company could only cater to wealthy consumers looking for luxury-level trucks and SUVs.

The other factor driving Rivian shares off recent lows was the company’s new strategy to initially produce the R2 from its existing Normal, Illinois facility. Previously it said those vehicles would come from its future Georgia plant. Pausing construction in Georgia will save the company more than $2.25 billion, it noted. In a press release, the company said, “The savings are expected to come from capital expenditures, product development investment, and supplier sourcing opportunities.”

Rivian ended the fourth quarter of 2023 with more than $9 billion in cash and equivalents on its balance sheet. But the company used more than $5 billion in growth capital last year and was expected to need about the same for 2024.

Saving nearly half of those capital expenditures puts a much different perspective on its financial picture. One of the biggest risks investors needed to consider when buying Rivian stock was the potential that it would run out of money before it could scale up its vehicle sales with its lower-priced models. That put the potential of a new capital raise or even bankruptcy as key investment risks.

While Rivian still needs to execute on its plan and attract buyers for its new products, that key risk has been meaningfully lowered. If it successfully does those things, the stock will look like a bargain at recent prices.

Howard Smith has positions in Rivian Automotive. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

On Wednesday, the crypto market experienced a modest downturn, with a 1% decrease in its overall value across the board, as bitcoin and ethereum saw declines of 0.51% and 0.45%, respectively. Bitcoin momentarily reached the $53,000 mark the day prior, while ether soared past the $3,000 threshold on Tuesday, though both cryptocurrencies traded significantly lower […]

On Wednesday, the crypto market experienced a modest downturn, with a 1% decrease in its overall value across the board, as bitcoin and ethereum saw declines of 0.51% and 0.45%, respectively. Bitcoin momentarily reached the $53,000 mark the day prior, while ether soared past the $3,000 threshold on Tuesday, though both cryptocurrencies traded significantly lower […]

Source link

Over multidecade periods, Wall Street has proved unstoppable. But over shorter time lines, the stock market’s most prominent indexes have often been volatile and unpredictable — perhaps none more so than the growth-fueled Nasdaq Composite (NASDAQINDEX: ^IXIC).

Whereas the ageless Dow Jones Industrial Average and benchmark S&P 500 have galloped to fresh, record-closing highs in 2024, the Nasdaq Composite is the only one of the three major stock indexes that’s not fully recovered from the 2022 bear market. As of the closing bell on Feb. 7, the Nasdaq remained about 2% below its all-time closing high.

For some investors, a roughly 2% decline over a 26-month period will be viewed as a disappointment. But for patient investors with a long-term mindset, any notable decline in a major index represents an opportunity to snag high-quality stocks — in this instance, growth stocks — at a perceived discount.

What follows are four appealing growth stocks you’ll regret not buying in the wake of the Nasdaq bear market dip.

The first phenomenal growth stock you’ll be kicking yourself for not picking up with the Nasdaq still below its record-closing high is China-based electric vehicle (EV) maker Nio (NYSE: NIO). Though EV demand has weakened in the U.S. and shows signs of slowing in global markets as competition picks up, Nio has well-defined competitive advantages that can help it succeed.

Nio should benefit as the Chinese economy continues to find its footing following the end of three years of stringent COVID-19 lockdowns and supply chain kinks. Even though this won’t be a straight-line recovery for the world’s No. 2 economy, the country’s burgeoning middle class offers hope that growth rates can continue to outpace most developed markets.

Beyond macroeconomic factors, Nio’s innovation is what stands out. The company has been regularly introducing at least one new EV annually for years. Moreover, it refreshed its lineup with its next-generation NT 2.0 platform, which provides an array of improved, advanced driver-assistance systems. Deliveries of the company’s EVs perked up when models housed on NT 2.0 began hitting showrooms last year.

Out-of-the-box innovation matters, too. Nio introduced its battery-as-a-service (BaaS) subscription during the pandemic as a way to bolster initial sales and keep early buyers loyal to the brand. It recently opened its battery-swap network to the entire EV industry in China.

Another catalyst worth noting is that Nio’s premium sedans and SUVs primarily target middle- and upper-income buyers. People with higher incomes tend to be less sensitive to fluctuations in economic activity and changes in inflation. This should help insulate Nio’s operating cash flow year in and year out.

Lastly, Nio is flush with cash. It takes a lot of capital to build an automaker from the ground up to mass production. Nio closed out September with $6.2 billion in cash, cash equivalents, and various short- and long-term investments, as well as received a $2.2 billion equity investment from CYVN Investments in December.

A second appealing growth stock you’ll regret not purchasing in the wake of the Nasdaq bear market swoon is small-cap furniture stock Lovesac (NASDAQ: LOVE). While the furniture industry is typically filled with slow-growing, brick-and-mortar based businesses, Lovesac has shown that its unique approach is a game changer.

What makes Lovesac so special is its furniture. Whereas most traditional furniture retailers rely on the same small group of wholesalers, approximately 90% of Lovesac’s net sales can be traced to its unique “sactionals” — modular couches that can be rearranged a variety of ways to fit most living spaces. Aside from unparalleled functionality, sactionals come with over 200 different cover choices, and the yarn used in their production is made entirely from recycled plastic water bottles. There’s no other product providing this level of functionality, optionality, and eco-friendliness.

Lovesac’s omnichannel sales platform is another critical differentiator. Although it does have physical stores in 40 U.S. states, the company’s success has been a function of its ability to move sales online, as well as rely on pop-up showrooms and a handful of brand-name partnerships. In short, Lovesac’s overhead expenses have been markedly lower than its peers’, which has resulted in superior margins.

Similar to Nio, Lovesac tends to focus its efforts on consumers with higher incomes. Sactionals have a number of high-margin upgrade options (e.g., wireless charging and built-in surround sound), and well-to-do consumers are unlikely to alter their spending habits during modest fluctuations in the U.S. economy.

The feather in Lovesac’s cap is that it’s cheap. Shares can be purchased for about 10 times forward-year earnings, yet Wall Street’s consensus anticipates average annual-earnings growth of 30% over the next five years.

The third amazing growth stock you’ll regret not buying with the Nasdaq not having yet put the 2022 bear market in the rearview mirror is biotech stock Exelixis (NASDAQ: EXEL). Despite being heavily reliant on a single drug (Cabometyx, or cabozantinib in its scientific form), Exelixis has the innovation needed to reward its patient shareholders.

As noted, Cabometyx is this company’s superstar. It’s approved to treat first- and second-line renal cell carcinoma, as well as advanced hepatocellular carcinoma. Cancer-drug developers usually have exceptionally strong pricing power with health insurers. Furthermore, demand for cancer drugs doesn’t ebb and flow with the U.S. economy. Helping improve patient quality of life is going to be a steady need in any economic climate, which is good news for Exelixis’ operating cash flow.

One of the more exciting developments is the potential for label-expansion opportunities. In the first half of 2024, Exelixis hopes to carve out a path for a supplemental new drug application for Cabometyx in advanced pancreatic and extra-pancreatic neuroendocrine tumors, as well as for patients with metastatic castration-resistant prostate cancer. The latter is a trial conducted in combination with Roche‘s Tecentriq. Label expansions not only bolster the company’s sales, but they can protect Exelixis’ cash flow from generics for years to come.

We’re also seeing early evidence that the company’s investments in internally developed compounds and collaborations are paying off. For instance, zanzalintinib (previously XL092) is being examined in a half-dozen clinical trials, including an early-stage collaboration to treat advanced clear cell renal cell carcinoma in combination with AB521, which is being developed by Arcus Biosciences.

Even though Exelixis is forging its future through clinical innovation, it hasn’t forgotten about its shareholders. Following the completion of a $550 million share-repurchase program in 2023, the company’s board authorized a new $450 million buyback program for the current year. Buybacks are made easy with Exelixis sitting on a whopping $1.72 billion in cash, cash equivalents, and investments.

A fourth appealing growth stock you’ll regret not buying in the wake of the Nasdaq bear market dip is none other than FAANG stock Alphabet (NASDAQ: GOOGL)(NASDAQ: GOOG). Although the advertising climate has been challenging over the past two years, Alphabet has sustained moats in place that can grow its operating cash flow at a double-digit annual pace throughout the decade.

There’s no question that recessions and downturns in ad spending are an inevitable aspect of the economic cycle. But what investors often overlook is that recessions are short lived. Only three of the one dozen recessions since the end of World War II have lasted 12 months, with none of these three surpassing 18 months. Comparatively, most periods of expansion endure for years, which is what allows ad-fueled companies like Alphabet to thrive.

The foundation here continues to be internet search engine Google. In January, Google accounted for a 91.5% global share of internet search, which was 88 percentage points higher than its next-closest competitor. This veritable monopoly in search, which Google has had for more than a decade, ensures it’s the go-to for businesses wanting to target consumers. This should give Alphabet exceptional ad-pricing power in most economic environments.

Alphabet’s fast-growing ancillary segments offer plenty of excitement, too. It’s the parent of YouTube, which is the second most-visited social site on the planet. Viewership of YouTube Shorts (short-form videos often lasting less than 60 seconds) soared from 6.5 billion per day in 2021 to more than 50 billion daily by February 2023. This represents another big-time ad-growth opportunity for Alphabet.

Additionally, the company’s cloud-infrastructure service segment, Google Cloud, recently delivered its fourth consecutive quarter of operating income following years of losses. Enterprise cloud spending is still in its relative infancy, and cloud-service margins are notably higher than traditional advertising margins.

Best of all, Alphabet remains historically cheap. Shares can be purchased right now for 13 times estimated cash flow in 2025, which represents a 28% discount to its average price-to-cash flow ratio over the past five years.

Should you invest $1,000 in Nio right now?

Before you buy stock in Nio, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nio wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 5, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Sean Williams has positions in Alphabet, Exelixis, and Lovesac. The Motley Fool has positions in and recommends Alphabet and Nio. The Motley Fool recommends Exelixis, Lovesac, and Roche Ag. The Motley Fool has a disclosure policy.

4 Appealing Growth Stocks You’ll Regret Not Buying in the Wake of the Nasdaq Bear Market Dip was originally published by The Motley Fool

Dogecoin, the Shiba Inu-faced cryptocurrency born from a meme, finds itself in an intriguing scenario. Despite a recent 23% price plunge since December, the network is experiencing an unprecedented boom in user adoption, marking a fascinating dichotomy in its current state.

On the bullish side, non-zero wallets, indicating active users holding DOGE, have witnessed a staggering 7.2% growth since January 22nd. This translates to roughly 414,000 new wallets joining the network in just two weeks, representing the fastest growth in Dogecoin’s decade-long history. These new users primarily hold smaller amounts, suggesting potential for future engagement within the ecosystem.

🐶 #Dogecoin‘s value is -23% since its top on Dec. 9th. But the #memecoin‘s wallets with >0 $DOGE coins has been growing at the fastest rate in the network’s decade long history. 413.8K new wallets, mostly holding 0.001-1 $DOGE, have been added in 2 weeks. pic.twitter.com/l6Pv0KvkKW

— Santiment (@santimentfeed) February 6, 2024

Furthermore, Dogecoin adoption has skyrocketed by a mind-boggling 86% in the past week, with over 890,000 new addresses appearing on the blockchain, analysts at IntoTheBlock disclosed.

Analysts attribute this surge to several factors, including the revival of “Doginals” (NFTs on the Dogecoin chain), the recent release of the iconic game Doom on the Dogecoin blockchain, and the growing popularity of Xpayments, a platform enabling DOGE transactions in the real world.

This price volatility highlights a key challenge for Dogecoin: balancing user growth with sustainable value appreciation. While the increasing user base indicates potential for future adoption, the lack of diverse use cases and inherent inflationary nature might hinder long-term price stability. Unlike Bitcoin with its capped supply, Dogecoin has an inflationary model, meaning new coins are continuously created, potentially impacting its value.

Dogecoin currently trading at $0.07834 on the daily chart: TradingView.com

Meanwhile, SpaceX – the leading private space exploration company – threw its weight behind Dogecoin by accepting it as payment for the rescheduled DOGE-1 Moon mission. This endorsement not only adds legitimacy to the meme coin but also injects a dose of excitement into the community.

Geometric Energy Corporation, the mission’s sponsor, revealed they paid SpaceX in DOGE to secure a new launch date following a delay. While the exact timing remains shrouded in mystery, the news has undoubtedly bolstered community sentiment.

However, amidst the user boom, Dogecoin’s price performance paints a contrasting picture. As of February 6th, DOGE is trading at $0.078, reflecting a 0.3% decrease in the last 24 hours and a 3.48% decline over the past week. This dip extends to a 2.77% loss for the month, marking a significant drop from its December peak.

Featured image from Adobe Stock, chart from TradingView

Disclaimer: The article is provided for educational purposes only. It does not represent the opinions of NewsBTC on whether to buy, sell or hold any investments and naturally investing carries risks. You are advised to conduct your own research before making any investment decisions. Use information provided on this website entirely at your own risk.

Bitwise chief investment officer Matt Hougan attributed the recent decline in the crypto market to overinflated expectations regarding the potential impact of the newly launched Bitcoin exchange-traded funds (ETFs).

In a Jan. 23 post on X (formerly Twitter), Hougan explained that the current market sell-off is driven by what he terms an “ETF Expectations-led” phenomenon.

According to him, investors anticipating “larger net flows into (these) ETFs” front-ran the approval news by piling into both spot and derivatives positions on the flagship digital asset. However, with the expected inflows not materializing, these investors are now “unwinding that bet,” prompting the current market situation.

“Just as the market overestimated the short-term impact of ETFs, it is underestimating the long-term impact,” Hougan concluded.

Since the Securities and Exchange Commission (SEC) approved the launch of several spot Bitcoin ETFs in the U.S., the value of the top cryptocurrency has been on a downturn. The digital asset fell to as low as under $39,000 on Jan. 23 but has recovered to $40,389 as of press time, according to CryptoSlate’s data.

This downward trend raised concerns within the crypto community, with some attributing it to the outflows from Grayscale’s Bitcoin Trust ETF (GBTC).

Contrary to this sentiment, analysts, including CryptoQuant founder Ki Young Ju, share a perspective aligned with Hougan’s.

Young Ju recently emphasized that Bitcoin operates in a futures-driven market, making it less susceptible to spot-selling activities from GBTC-related issues.

“BTC falls due to derivative market selling, not GBTC. OTC (over the counter) markets are very active, but no price impact,” he added.

Meanwhile, the Bitwise investment chief also clarified that the recently launched ETFs are net buyers of Bitcoin despite the outflows emanating from GBTC.

Hougan pointed out that while GBTC functions as a net seller, the cumulative BTC acquisitions from the new ETFs surpass that being offloaded by Grayscale.

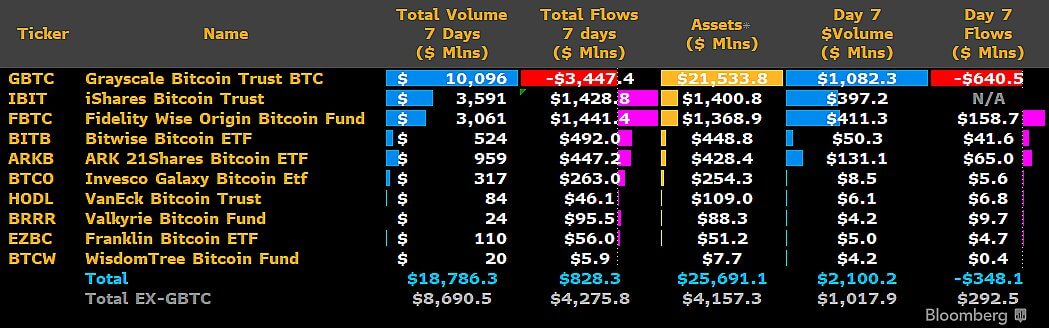

Bloomberg data corroborates Hougan’s view. As of Jan. 23, GBTC’s outflows stood at $3.45 billion, while the newly introduced nine ETFs had a combined inflow of more than $4 billion in assets under management.

This data stresses a compelling narrative—that the ETFs have seen substantial interest from the community, leading to a swift and significant accumulation of the leading cryptocurrency.