Tobacco companies face an uncertain future, even as they try to

move beyond combustible cigarettes to smokeless products. But one thing is certain for investors in

Altria Group or British American Tobacco—the dividend is safe.

Tobacco companies face an uncertain future, even as they try to

move beyond combustible cigarettes to smokeless products. But one thing is certain for investors in

Altria Group or British American Tobacco—the dividend is safe.

Many view Warren Buffett as one of the greatest stock pickers of all time, if not the greatest, so you might be surprised to learn that he owns two ETFs in his Berkshire Hathaway (NYSE:BRK.B) portfolio. Not only that, but the only two ETFs that he owns are broad market ETFs — the Vanguard S&P 500 ETF (NYSEARCA:VOO) and the SPDR S&P 500 ETF Trust (NYSEARCA:SPY).

I’m bullish on these ETFs based on their fantastic long-term track records and their low fees. Plus, if they are worthy of a spot in Buffett’s portfolio, they are likely worth a spot in the portfolio of the everyday investor as well. Here are the likely reasons why the Oracle of Omaha owns these ETFs and why they could be good fits for your portfolio as well.

VOO is a $347.2 billion low-cost ETF from Vanguard that simply invests in the S&P 500 (SPX), an index representing 500 of the largest publicly-traded companies in the U.S. SPY employs the same strategy and is the largest ETF in the market, with $414.2 billion in assets under management (AUM).

While Buffett’s acumen for picking undervalued stocks is legendary, he has long espoused the virtues of low-cost index funds like VOO and SPY.

In 2008, Buffett famously placed a bet with a hedge fund manager that a simple S&P 500 index fund from Vanguard would beat a portfolio of five actively-managed hedge funds over the next 10 years, and Buffett won by a country mile. The S&P 500 fund returned over 125%, while the five actively-managed funds returned an average of just 36.3% net of fees.

Research from Standard & Poor’s shows that this likely wasn’t a fluke — after five years, 84% of actively-managed large-cap funds underperform their benchmarks, and by 10 years, 90% underperform.

Buffett wrote, “When trillions of dollars are managed by Wall Streeters charging high fees, it will usually be the managers who reap outsized profits, not the clients. Both large and small investors should stick with low-cost index funds.”

In fact, Buffett is such a proponent of index funds that he has even reportedly instructed that 90% of the money that his family inherits after he passes away will be invested in low-cost index funds.

Thanks to public data from 13F filings, we can see that Buffett owns about $16.8 million worth of SPY and $16.9 million worth of VOO in Berkshire Hathaway’s portfolio. To be clear, these are relatively small investments for Berkshire Hathaway, given that its portfolio of public equities is worth $313.2 billion, but Buffett clearly likes these ETFs.

The nice thing about these S&P 500 ETFs is that they allow investors to harness the power of 500 of the largest U.S. companies in their portfolios with one simple investment vehicle. This gives investors plenty of diversification as well as exposure to the dynamism of top U.S. companies from all sectors of the economy.

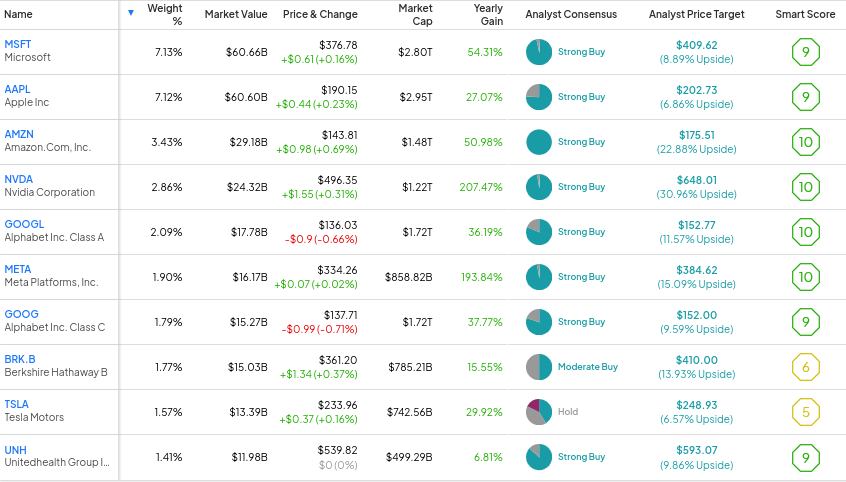

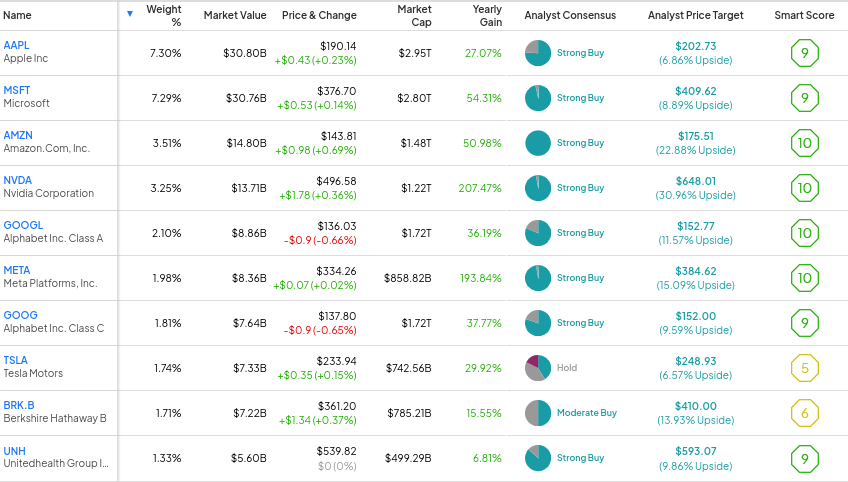

Because they both passively invest in the S&P 500 index, the holdings for VOO and SPY are more or less the same. VOO owns 506 stocks, and its top 10 holdings account for 31.1% of the fund. SPY owns 503 stocks, and its top 10 holdings make up 32.0% of the fund.

Below, you’ll find an overview of VOO’s top 10 holdings using TipRanks’ holdings tool, as well as an overview of SPY’s top 10 holdings.

As you can see, both funds own many of the U.S.’s top companies. The holdings for both portfolios feature a strong assortment of Smart Scores. The Smart Score is a proprietary quantitative stock scoring system created by TipRanks. It gives stocks a score from 1 to 10 based on eight market key factors. A score of 8 or above is equivalent to an Outperform rating.

Each fund features eight top 10 holdings with Outperform-equivalent Smart Scores of 8 or above, and holdings like Amazon (NASDAQ:AMZN), Nvidia (NASDAQ:NVDA), Alphabet (NASDAQ:GOOGL), and Meta Platforms (NASDAQ:META), all score 10 out of 10.

VOO and SPY both boast Outperform-equivalent ETF Smart Scores of 8 out of 10.

In addition to these strong portfolios of top U.S. companies, both VOO and SPY have compiled impressive track records of long-term performance for many years.

VOO has returned 10.3% on an annualized basis over the past three years (as of October 31), 11.0% over the past five, and 11.1% over the past 10. Since its inception in 2010, it has provided annualized returns of 12.9%.

Unsurprisingly, because they both invest in the same index, SPY has produced similar results. Over the past three years, SPY has generated an annualized return of 10.2%. Over the past five years, its annualized return stands at 10.9%, while its 10-year annualized return comes in at 11.0%. SPY is much older than VOO, having launched in 1993, but it has returned an excellent 9.6% on an annualized basis since then.

This return since 1993 is especially impressive when considering that the ETF has gone through the dot-com bubble, the Global Financial Crisis, and the COVID-19 crash all happened within this multi-decade time frame. The fact that SPY has generated such positive results, even with these periods of steep market declines taken into account, truly illustrates the power of long-term investing.

Both ETFs have generated excellent returns over time, highlighting why it has been difficult for the majority of active managers to beat the S&P 500 over the long run.

A stickler for value, Buffett is likely a fan of the low fees that both of these ETFs feature. VOO has an expense ratio of just 0.03%, while SPY charges 0.09%. Both are extremely low fees, but it has to be said that VOO is cheaper.

An investor putting $10,000 into VOO would pay just $3 in fees in year one, while an investor in SPY would pay $9.

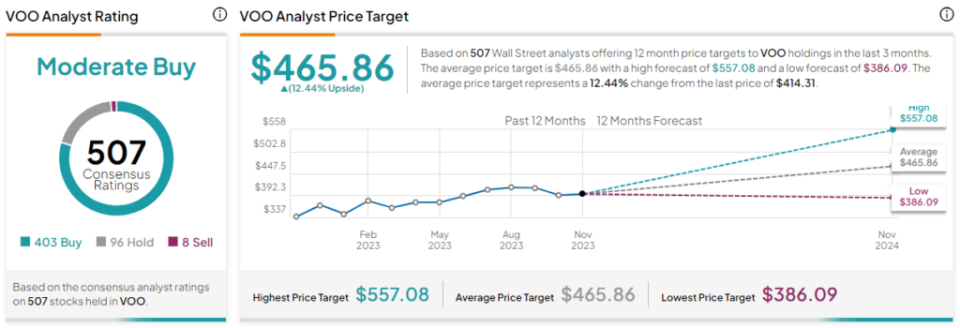

Turning to Wall Street, VOO earns a Moderate Buy consensus rating based on 403 Buys, 96 Holds, and eight Sell ratings assigned in the past three months. The average VOO stock price target of $465.86 implies 12.5% upside potential.

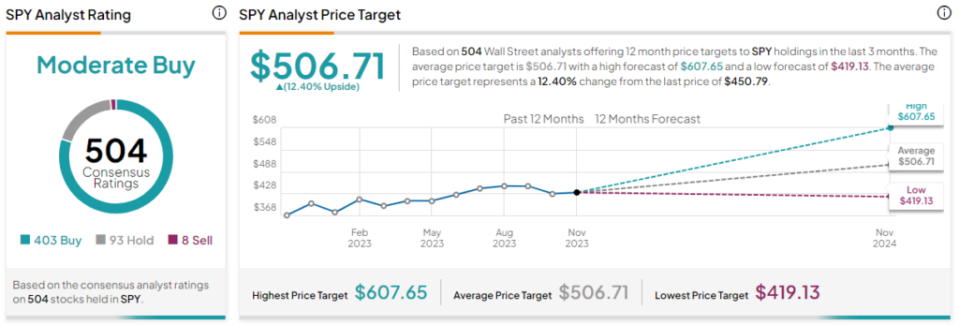

Meanwhile, SPY also earns a Moderate Buy consensus rating based on a nearly identical 403 Buys, 93 Holds, and eight Sell ratings assigned in the past three months. The average SPY stock price target of $506.71 implies 12.4% upside potential.

Both VOO and SPY employ simple strategies of investing in the S&P 500 index, but both have produced excellent results for investors over the long term. They offer diversified exposure to the top stocks in the U.S. market for a minuscule fee. Warren Buffett is a big believer in the power of index funds and likes them enough to include them in his own portfolio, and that’s good enough for me. Of the two funds, I like VOO better because of its lower expense ratio.

Instacart operates similarly; shoppers see a list of batches that are available to them in their area, as well as the expected customer tip, and they may select the one they want to shop, according to the company.

Uber drivers may not see the expected tip in advance, but at one point they could see a rider’s tip history, or whether they were a “top tipper,” which may have factored into who drivers chose to pick up.

“It was a wonderful tool for a driver,” said Sergio Avedian, a driver and senior contributor at The Rideshare Guy, a blog aimed at helping rideshare drivers earn more money.

Uber phased out the top tipper rider designation earlier this year. The company did not immediately respond to a request for comment.

“Drivers depend more and more on tips these days,” Avedian said. Still, his tips average only about 12% to 13% of the fare, he estimated.

In most cases, consumers face more opportunities to tip for a wider range of services than ever before, a trend also referred to as “tip creep.” But recent surveys show shoppers are experiencing “tip fatigue” and starting to tip less — while resenting tipping prompts even more.

Two-thirds of Americans have a negative view of tipping, according to a report by Bankrate, especially when it comes to the predetermined point-of-sale options.

“Consumers are dissatisfied with the current state of tipping, and a lot of it has to do with being asked to give tips before service rather than after,” Lynn said.

However, tipping in advance is not entirely new, he added. “People have long given bartenders generous tips as a bribe for future services, like getting a more generous pour.”

The S&P 500 (^GSPC 0.94%) has rebounded sharply from its bear market lows, but the benchmark index is still 9% below its record high, and the economy is sending mixed signals about where the stock market is headed next.

Read on to see why some investors are bullish and others are bearish, and pick up a few potentially life-changing tips from Warren Buffett.

Some signals point to the stock market soaring higher. The U.S. economy expanded at its fastest pace in two years during the third quarter. Unemployment remains well below the long-term average, and wages are increasing faster than inflation.

Additionally, analysts expect revenue and earnings growth to accelerate across the S&P 500 next year, and the number of companies that have mentioned “recession” on earnings calls has declined for four consecutive quarters.

However, some signals point to a stock market drawdown in the offing. Surging bond yields could lure investors away from equities and stifle economic growth by raising borrowing costs for businesses. The Federal Reserve has also intimated that interest rates will fall more slowly than previously anticipated, which could choke the economy into a recession.

Building on that, a closely watched section of the U.S. Treasury yield curve has been inverted for the past year, and such events have accurately predicted every recession since 1955, with only one false positive. The S&P 500 declined by an average of 31% during those recessions.

Suffice it to say, investors are being bombarded with mixed economic signals, which makes it easy to overthink or second-guess decisions.

Warren Buffett has built Berkshire Hathaway (BRK.A 0.66%) (BRK.B 0.80%) into one of the largest businesses in the world, and he has amassed a $100 billion fortune in the process. That success makes him an excellent source of economic insight and financial wisdom.

Detailed below is an overview of Buffett’s investment philosophy, pulled together from various shareholder letters, SEC filings, and interviews.

The processes described above are very involved. Buffett once said that “successful investing takes time, discipline, and patience.” But most people probably don’t want to spend a lot of time researching stocks. Fortunately, Buffett has pounded the table on a much simpler investment strategy for decades.

Buffett believes most people should consistently buy an S&P 500 index fund. That strategy spreads capital across many of the most influential businesses in the world — companies Buffett says “are bound to do well” in aggregate over time — and it requires almost no work.

Better yet, Buffett believes that know-nothing investors “can actually outperform most investment professionals” by periodically buying an S&P 500 index fund.

Historical data backs that assertion. Less than 8% of large-cap funds have outperformed the S&P 500 over the last 15 years, meaning most money managers could have saved themselves a lot of effort (and earned higher returns for their clients) by simply buying an S&P 500 index fund.

Trevor Jennewine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple and Berkshire Hathaway. The Motley Fool has a disclosure policy.

Traders work on the floor of the New York Stock Exchange (NYSE) on November 02, 2023 in New York City.

Spencer Platt | Getty Images

Friday’s market reaction to the jobs report comes down to a simple premise: bad news is good news, as long as it isn’t too bad.

Stocks rallied sharply after the Labor Department said nonfarm payrolls rose by 150,000 in October — 20,000 fewer than expected but a difference attributable pretty much completely to the auto strikes, which appear to be over.

For the Federal Reserve, the relatively muted job creation coupled with wage gains nearly in line with expectations adds up to a scenario in which the central bank doesn’t really have to do anything. It can just continue to let the data flow in, without having to move on interest rates as it evaluates the impact of its previous 11 hikes.

“The Fed finally got what it’s been looking for — a meaningful slowdown in the labor market,” said Mike Loewengart, head of model portfolio construction for Morgan Stanley’s Global Investment Office.

“We’ve seen one or two head fakes in this direction before, but the fact that this report followed other weaker-than-expected economic data points this week may encourage investors who have been waiting for a less-hawkish Fed,” he added.

Markets reacted in more ways than one to the report. Traders in fed funds futures reduced the probability for a December rate hike to less than 10% and now see the first cut coming as soon as May, according to CME Group tracking.

However, that cut could be the really bad news, as it likely would signal the Fed’s concern that the economy is slowing so much that it needs a boost from monetary policy. Slow, controlled growth is something the markets and the Fed are seeking in the current climate, negative growth is not.

“Investors who are eager for the Fed to be cutting rates should be careful what they wish for,” Michael Arone, chief investment strategist at State Street Global Advisors, said in an interview earlier this week.

Despite market pricing, it seems like cuts aren’t around the corner if recent statements from Fed officials are any indication. Fed Chairman Jerome Powell said Wednesday that cuts have not been a part of the conversation among policymakers.

“It seems like that’s still a ways off in my mind,” Richmond Fed President Thomas Barkin said during an interview Friday on CNBC’s “Squawk on the Street.” “You could imagine scenarios where demand comes off and you have to do something. You could imagine a scenario where inflation is starting to settle and you want to lower real rates. Both of those imaginary things still feel pretty far out the distance.”

Don’t miss these stories from CNBC PRO:

Apple (AAPL 1.87%) isn’t messing around this holiday season. The tech company added to an already exhaustive lineup of new products this week, announcing new chips and Macs, including 14-inch and 16-inch MacBook Pros in a new “space black” finish. The new devices build on a range of new product introductions headed into the holidays, including updated smartphones and smartwatches. Apple even brought to market a new Apple Pencil.

All of this positions Apple strategically to capture wallet share from increasingly strapped consumers who are pressured by inflation and high interest rates. More importantly, Apple’s latest round of new products increases the odds of the iPhone maker returning to growth during a quarter in which it typically rakes in the lion’s share of its annual net income.

On the surface, Apple’s product event on Oct. 30 may seem unimportant. After all, it was a Mac-focused event, and Mac only accounted for about 10.2% of Apple’s fiscal 2022 revenue. But investors shouldn’t count out this product event as a key catalyst for the holidays yet. There are several reasons new Mac products could be important catalysts for Apple when combined with the already-robust lineup of new products Apple has going into the holidays.

First, other than Apple’s move in the summer of 2022 to update its 13-inch MacBook Pro to include a new processor, the company’s MacBook Pro lineup was an aging product line going into the holidays last year. For instance, the last major refreshes to its 14-inch and 16-inch MacBook Pro devices were in October of 2021. With the help of these new products, Apple’s Mac business grew 25% year over year during the calendar 2021 holiday quarter. Indeed, Apple management specifically credited the segment’s growth to the “newly redesigned MacBook Pro” during the earnings call for the period. While 25% growth from Mac during the holiday quarter is unlikely, given the current macroeconomic backdrop, Apple’s well-timed refresh of the MacBook Pro will almost undoubtedly help the important period’s results in some fashion, particularly since Apple is going up against a period last year when the Mac lineup was aging.

Additionally, it’s worth noting that Apple’s MacBook Pro lineup commands some serious pricing power. The 16-inch MacBook Pro, for instance, starts at $2,499. Strong orders and shipments of the new product could really move the needle for not only Apple’s Mac segment but its entire business.

Finally, something tells me Apple’s new space black color will be popular with pro users. Call it speculation, but that’s my hunch.

There’s also something to be said about an improving global supply chain. As the world recovers from COVID-19-related factory shutdowns, Apple is likely better prepared to build and ship more products going into the holidays this year than it was in the year-ago period. Indeed, this is likely one key reason why Apple has introduced so many new products leading up to the holidays. Chances are, Apple’s new MacBook Pro will both solicit strong demand but also be followed up with good production volume — at least compared to recent years, which often saw manufacturing interrupted by sudden and unplanned factory shutdowns due to China’s zero-COVID policies at the time and some disruptions in other markets as well.

Finally, it’s worth emphasizing that Apple is going up against an easy comparison during the holiday quarter (the first fiscal quarter of 2024) particularly when it comes to Mac. Apple’s total revenue fell 5% year over year in its first quarter of fiscal 2023 (the fiscal quarter coinciding with the fourth calendar quarter of 2022), with Mac revenue declining about 29% year over year.

Apple’s new space black MacBook Pro, along with its refreshed iMacs, could be the determining factor for the company returning to year-over-year revenue growth in the holiday quarter.

Fortunately, however, Apple isn’t entirely dependent on the MacBook Pro for a good holiday quarter. It has overhauled other major products going into the final calendar quarter as well. This loaded product pipeline will help Apple grab as much share from consumers’ holiday-spending budgets as possible.

Investors may get some insight into what Apple expects from its holiday quarter when the company reports earnings for its fiscal Q4 after market close on Thursday, Nov. 2.

Daniel Sparks has no position in any of the stocks mentioned. His clients may own shares of the companies mentioned. The Motley Fool has positions in and recommends Apple. The Motley Fool has a disclosure policy.

As we move closer to November, savers ask the perennial question: Do you buy I Bonds right now or wait until a new rate is announced on Nov. 1?

Spoiler alert: You might not need to rush here.

The current rate on an I Bond bought from May through October is 4.3%. That includes a key fixed rate of 0.9% for I Bonds bought through October − and an annualized inflation-adjusted rate of 3.38% that is added on top of the fixed rate.

Based on the latest inflation data announced Oct. 12, the inflation-linked rate for I Bonds is expected to be 3.94%, according to Ken Tumin, who founded DepositAccounts in 2009, which is now part of LendingTree. The site tracks and compares bank rates.

If you add a fixed rate of 0.9% on top of that, Tumin said, you might be looking at a composite rate of 4.86%.

But Tumin and others suggest you might want to wait until November to buy I Bonds for another key reason. Remember, even if you buy I Bonds now, you’d still get that higher inflation-adjusted rate down the road. What you wouldn’t get if you buy now is a higher fixed rate.

Experts say that the odds are high for a more attractive fixed rate for new I Bonds and that a higher fixed rate will stay with that bond for the 30-year life of the Series I U.S. Savings Bond.

Tumin says the fixed rate for I Bonds bought from November through April 2024 could very well be higher than 0.9%.

“If you’re in it for the long term, it makes sense to wait,” Tumin said.

The new fixed rate, he estimates, could be in the range of 1% to 1.5%. The actual rate won’t be announced until Nov. 1, or possibly slightly earlier, by the U.S. Treasury Department.

“Although the Treasury doesn’t disclose how it chooses the I Bond fixed rate, it is generally believed that there is some correlation with the real yield of 10-year TIPS,” Tumin said.

David Enna, who has a website called Tipswatch.com, expects that the fixed rate for I Bonds issued from November through April could be as high as something in the 1.4% to 1.7% range.

“That would be a dramatic increase, but seems justified,” Enna said, who has noted that you’d have to go back to November 2007 to find an I Bond fixed rate at 1% or higher.

He said it’s clear that the fixed rate will go up for I Bonds issued in November, given yield activity. On the lower end, he said, “a fixed rate of at least 1.2% seems highly likely, but you never know.”

Much will depend, Enna said, on the bond market activity and real yields over the next three weeks.

The fixed rate for I Bonds reflects the real yields of Treasury Inflation Protected Securities, or TIPS, which have risen considerably in the past six months.

Inflation, while a bit cooler than last year, remains very much part of the economic picture.

Consumer prices rose 3.7% over the past 12 months through September, according to the U.S. Bureau of Labor Statistics. The rising cost of shelter was the largest contributor to the month-over-month increase of 0.4%.

The new variable, the inflation-driven rate for I Bonds, is expected to be 3.94% at the November reset, according to Enna and Tumin.

If the new fixed rate is 1.2%, Enna said, those buying I Bonds from November through April might generate a composite rate of 5.2% for I Bonds issued then.

“But that isn’t certain,” Enna noted.

The inflation rate for I Bonds is the percent change in the Consumer Price Index for Urban Consumers over a six-month period ending before May 1 and Nov. 1.

The inflation-linked rate can change, and often does, every six months after your I Bonds were issued.

The inflation adjustment is added onto I Bonds that you bought earlier, say if you bought those bonds a year ago or even when your kids were born 10 years ago. Series I savings bonds were introduced 25 years ago − and the initial bonds keep earning interest and seeing new inflation adjustments along the way if you hold onto them.

The fixed rates on I Bonds vary significantly over time, depending on when the bonds were issued.

I Bonds issued in 2021 and 2022, for example, have a 0% fixed rate. Enna notes that I Bonds with a 0% fixed rate would see an estimated 3.94% composite rate − reflecting recent inflation − over a six-month period.

The highest fixed rate on I Bonds was 3.6% for bonds issued from May through October 2000 − making those the last bonds you’d want to cash in. If we saw an inflation adjustment of 3.94%, those bonds would be paying 7.54% over a six-month stretch.

I Bonds had three sizzling rates in a row from late 2021 through early 2023 after sky-high inflation.

Savers who bought I Bonds issued from November 2021 through April 2022 grabbed a composite 7.12% rate that applied to the first six months after the bonds were issued. The fixed rate on I Bonds issued then was 0%.

And then that eye-popping rate was eclipsed by 9.62% for six months after the bond was issued for savers who bought I Bonds from May 2022 through October 2022. The fixed rate for bonds issued then was 0%.

Those who bought I Bonds issued from November 2022 through April snagged an attractive 6.89% that applied for six months after the issue date for those bonds. The fixed rate was 0.4%. The annualized rate of inflation was 6.48%.

Savers who held onto their old I Bonds issued years ago also benefited from the higher inflation adjustments. The inflation rate that the Treasury Department sets each May and November for I Bonds applies for a six-month period for all I Bonds that were ever issued and were not yet cashed in by savers.

You can find the current value of an electronic I Bond at TreasuryDirect.gov when you look in your account information there. If the bond is paper, you can use the Savings Bond Calculator at TreasuryDirect.gov.

For bonds less than five years old, the values shown in TreasuryDirect and through the savings bond calculator don’t include the last three months of interest. That’s because, the TreasuryDirect site notes, if you cash a bond before five years, you wouldn’t receive the final three months of interest.

Seeing I Bonds near 4% or 5% isn’t going to trigger much buzz at all − especially for savers who want a short-term fix. If you shop around, some CDs are offering very attractive rates.

Rates on competing certificates of deposit issued at a bank or credit union − which remained low when inflation kicked off − have risen significantly.

Online banks are offering one-year certificates of deposit with an average annual percentage yield of 5.18%, Tumin said. Some of these better-yielding CDs require only a minimum $1,000 deposit.

I’ve seen some local credit unions with CD or certificate specials in the 4.25% to 5.2% range on short-term CDs. Again, though, you need to shop around for the best rates on CDs, because they can range quite a bit.

“CDs are currently a better deal for a one-year period than I Bonds,” Tumin said.

Tumin gave this example: If someone planned to redeem the I Bond shortly after 13 months, the annualized yield would be 3.51% after you take into account a three-month penalty for not holding the bond at least five years. This specific example is based on an I Bond that was bought in October and redeemed a bit more than a year later in November 2024.

Tumin explained further that the 3.51% example would apply if someone bought an I Bond and redeemed it on the exact same date, such as Oct. 21, and then later cashed it on Nov. 21, 2024. It’s possible, he noted, to slightly boost returns by buying the I bond later in the month and redeeming earlier in the month.

Savers who live in states like California or New York that have high state income tax rates could still want to turn to I Bonds instead of CDs, Tumin said, because interest on U.S. savings bonds is tax-exempt at the state level.

But, he added, that the current I Bond rates aren’t even high enough for the state exemption to matter much in many places.

Longer-term savers, though, might want I Bonds as part of their savings to hedge against inflation, set aside some emergency savings, and see returns that pay more than a typical savings account.

Key points to remember about I Bonds: You cannot cash an I Bond until after you’ve held it for one year. And if you cash them before five years, you’d lose the previous three months of interest.

Interest is added monthly and compounded semiannually.

Each calendar year, an individual can buy up to $10,000 in electronic I Bonds in the TreasuryDirect system at TreasuryDirect.gov. You can invest as little as $25 or any amount above that to the penny. Each year, savers can also buy up to $5,000 in paper I Bonds using your federal income tax refund but you must file Form 8888 when you file the tax return.

Contact personal finance columnist Susan Tompor: stompor@freepress.com. Follow her on Twitter @tompor.

This article originally appeared on Detroit Free Press: I Bonds rates could top 5% in November. Should you buy them?

Contrary to what many are saying, it might not be a bad time to buy a house.

That’s because buyers waiting for rates to drop may be waiting a long time.

When mortgage rates do go down, competition and demand will come roaring back.

By many metrics, the US housing market has never been more unaffordable, and all of the prevailing wisdom right now says buyers should wait it out, either for mortgage rates to drop or prices to come down.

And yet, there’s an argument to be made for getting in now if you can find something, even amid 20-year high mortgage rates and stubbornly high prices.

Mortgage rates at 8% have sidelined a good portion of the competition. While it might not seem like it, the current landscape might be more of a buyer’s market than in recent years, particularly compared to the height of the pandemic when sellers could demand any contingencies be waived and buyers were snapping up homes sight unseen.

More importantly though, the lack of competition now means that when borrowing costs do ease, buyers can expect a flood of pent up demand to wash over the market.

“The days of the 2%-3% interest rates are never going to come back. Forget about that. But they will come down,” “Shark Tank” investor and real estate mogul Barbara Corcoran said in a post on Instagram this week.

“The minute they drop…the whole world’s going to jump back in the market. There’s going to be no houses around, and prices are going to go up by 10%, or even 15%. So don’t get out of the market. This is the very best time.”

The Corcoran Group founder’s estimate for price increases when rates drop is on the high end, but other experts agree that costs might not come down anytime soon. Other real estate experts are forecasting a more mild increase in home prices once mortgage rates ease, with a slight boost of about 1%-2%, National Association of Realtors chief economist Lawrence Yun told Insider previously.

But buyers who remain persistent in the current market could end up finding good opportunities, Redfin chief economist Daryl Fairweather said. Once mortgage rates pull back, there will likely only be a small period of improved affordability before prices jump, she predicted.

“If you wait and you’re really trying to time it for interest rates, maybe you can get a better rate later on when rates fall, but it’s really hard to time that, because that’s what everyone’s going to do,” Fairweather said. “The market will correct for that and prices would go up and in such a way that mortgage rates aren’t enough to make it more affordable.”

In the meantime, home prices could in the near-term even see a modest drop, Fairweather said, thanks to high mortgage rates crushing buyer demand.

That message doesn’t appear to be getting through to prospective homebuyers, who have made themselves scarce as mortgage rates have continued their steady rise in 2023. Existing home sales in September plunged to a seasonally adjusted rate of 3.96 million homes a year, the slowest pace of sales since 2010, according to NAR data.

But experts say that high mortgage rates are probably here to stay for some time, and even if they drop below their current elevated levels, a return to the days of 3% is unlikely. This is especially true as the Federal Reserve maintains its outlook for higher-for-longer interest rates to keep a lid on inflation.

Fairweather sees mortgage rates staying where they are until the Fed begins to cut rates in mid-2024. That could cause mortgage rates to ease around 100 basis-points next year, dropping as low as 7%.

“I think that it’s potentially a good time to buy, but there’s still risk in the market,” Fairweather added.

Over the near term, most experts still expect housing affordability to remain strained, especially when compared to pre-pandemic standards. Incomes would need to spike 55% or mortgage rates would need to drop by 4 full percentage points to return the market to pre-pandemic affordability conditions, according to one industry executive.

But overall, the message from experts boils down to: don’t try to time the market. Buyers waiting for something to change might be disappointed, and there’s no telling when affordability metrics might improve. With that in mind, the old advice still stands—buy when and what you can afford.

Read the original article on Business Insider

One notable adjustment pertained to the Net Asset Value (NAV) calculations, which ARK Invest acknowledged were not aligned with Generally Accepted Accounting Principles (GAAP), the accounting standard endorsed by the SEC.

Eric Balchunas, an ETF analyst at Bloomberg, recently took to the social media platform X to reveal that ARK Invest’s latest amendment to its spot Bitcoin Exchange Traded Fund (ETF) filing may signify a positive step toward future approvals for a Bitcoin ETF.

It’s worth noting that the Securities and Exchange Commission (SEC) had sent comments and questions to issuers a few weeks prior, seeking clarifications and adjustments to their S-1 documents.

In response, ARK Invest and 21Shares submitted an updated application for their spot Bitcoin ETF on Wednesday, which included additional information detailing the fund’s operational processes, such as asset custody and valuation methodologies.

Balchunas, shared his perspective on these developments, stating that the amendments to the filing “mean ARK got the SEC’s comments and has dealt with them all, and now put the ball back in the SEC’s court.” Balchunas went on to express his optimism, referring to these changes as “a good sign” and a clear indicator of “solid progress”.

Similarly, James Seyffart, another ETF analyst at Bloomberg, suggested that this clarification demonstrates open communication between ARK Invest, 21Shares, and the SEC, a positive indication for future approval. While ARK’s responsiveness is a positive development, it does not necessarily guarantee immediate approval. Balchunas noted that the SEC might engage in further back-and-forth discussions on specific details, and the regulatory process may take time.

It is, however, crucial to recognize that the SEC’s rigorous scrutiny is part of its mandate to ensure investor protection and market integrity.

One notable adjustment pertained to the Net Asset Value (NAV) calculations, which ARK Invest acknowledged were not aligned with Generally Accepted Accounting Principles (GAAP), the accounting standard endorsed by the SEC.

Another critical change in the updated prospectus involves the handling of assets. The document mentions that the Trust’s assets held with the Custodian are kept in segregated accounts on the Bitcoin blockchain, often referred to as “wallets”. These assets are explicitly mentioned as not commingled with corporate or other customer assets.

This separation is a clear response to concerns regarding the safekeeping of assets in the crypto space. It demonstrates ARK’s commitment to ensuring the security and transparency of its Bitcoin holdings.

Scott Johnsson, general partner at Van Buren Capital, also weighed in on the amended filing. He highlighted a new addition in the filing, which addressed concerns related to the potential negative impacts on the ETF’s value.

Specifically, it mentioned the risk of Bitcoin being used for illegal purposes and the environmental implications of Bitcoin mining. Johnsson opined that ARK’s amendments demonstrate a willingness to cooperate with the SEC rather than create unnecessary obstacles through a disclosure review.

next

Benjamin Godfrey is a blockchain enthusiast and journalist who relishes writing about the real life applications of blockchain technology and innovations to drive general acceptance and worldwide integration of the emerging technology. His desire to educate people about cryptocurrencies inspires his contributions to renowned blockchain media and sites.

Amid the macro developments and geopolitical tensions, Bitcoin has continued to outperform the rest of the crypto market.

Despite the current selling pressure, billionaire investors continue to bet on Bitcoin (BTC) and see it as a potential hedge against the current geopolitical tensions. On Tuesday, October 10, billionaire hedge fund manager Paul Tudor Jones said that it’s extremely risky now to invest in risk assets, however, he has his hopes alive in Bitcoin.

In an interview with CNBC, Tudor Jones said:

“It’s a really challenging time to want to be an equity investor and in US stocks right now. You’ve got the geopolitical uncertainty… the United States is probably in its weakest fiscal position since certainly World War II with debt-to-GDP at 122%.”

Speaking about Bitcoin, apart from the geopolitical tensions, Tudor Jones also pointed out the concerning macro developments. As interest rates rise in the United States, a troubling cycle ensues. Elevated interest rates lead to increased borrowing costs, which in turn result in higher debt issuance.

This surge in debt issuance prompts additional selling of bonds, subsequently driving rates even higher. This sequence of events places us in an unsustainable fiscal predicament, remarked Jones. “I can’t love stocks,” he said, “but I love bitcoin and gold.” He added that both assets should “probably take on a larger percentage of your portfolio than historically they would.”

The billionaire hedge fund manager has been bullish on Bitcoin over the last few years. Back in 2021, Jones said:

“Bitcoin is math, and math has been around for thousands of years.”

He has also expressed that the largest cryptocurrency by market capitalization was a means for him to invest in predictability. During an appearance on CNBC, he disclosed his heightened investment in Bitcoin, considering it a wager on predictability amidst uncertain economic circumstances.

Over the last week, the broader cryptocurrency has been under strong pressure with the Bitcoin price facing a rejection at $28,000. At press time, Bitcoin is trading 2% down at a price of $27,084 and a market cap of $528 billion.

But despite this, Bitcoin has outperformed in comparison to other top altcoins. As a result, Bitcoin’s share in the broader cryptocurrency market has shot past more than 50% as of now. In total, Bitcoin has surged by 66% this year, whereas Ether has experienced a 32% increase.

Bitcoin is more likely to outperform amid the uncertain macro developments, in comparison to the broader markets. However, knowing the fact that it’s a risk asset, investors should still maintain caution.

next

Bhushan is a FinTech enthusiast and holds a good flair in understanding financial markets. His interest in economics and finance draw his attention towards the new emerging Blockchain Technology and Cryptocurrency markets. He is continuously in a learning process and keeps himself motivated by sharing his acquired knowledge. In free time he reads thriller fictions novels and sometimes explore his culinary skills.