Markets often rise in the 12 months after concentration peaks.

Source link

Markets often rise in the 12 months after concentration peaks.

Source link

Shares of app monetization company AppLovin (APP 2.72%) soared 45.2% higher during February, according to data provided by S&P Global Market Intelligence. On Feb. 14, the company reported lovely financial results for the fourth quarter of 2023, solidly outpacing expectations on the top and bottom lines. This accounted for the majority of the gains for AppLovin stock during the month.

Prior to its earnings report, AppLovin’s management had guided for Q4 revenue of $930 million at the most. But in Q4, the company generated revenue of $953 million, up 36% year over year and far ahead of expectations.

It’s not just that AppLovin beat expectations; it’s how it did it. The company largely generates revenue from its software business that helps app companies grow and monetize their users. The software is powered by the new version of its artificial intelligence (AI) software.

AI stocks are the hottest on the stock market right now. AppLovin’s outperformance in Q4 demonstrated that it too is a top AI stock, which is why its jump higher was so pronounced.

As of this writing, AppLovin stock is up 500% from the start of 2023 — remarkable returns over the last 14 months. Investors previously questioned whether the company could truly grow its software revenue as the app economy cooled down and its peers struggled.

It’s safe to say AppLovin has answered its doubters. In 2020, the company had software revenue of just $207 million. In 2023, it had software revenue of over $1.8 billion.

AppLovin also generates revenue from first-party apps. But this isn’t the focus of the company. The focus is on software. And the benefit of software is that it’s high margin.

In 2023, AppLovin had free cash flow of $1 billion — quite good for a company with a market cap of just $22 billion as of this writing. And management has used some of the profits to repurchase shares. This means that AppLovin’s per-share free-cash-flow growth has been great, as the three-year chart below shows.

APP Average Diluted Shares Outstanding (Quarterly) data by YCharts

For the first quarter of 2024, AppLovin expects to generate revenue of $955 million to $975 million, which would represent 34% to 36% year-over-year growth. However, because AI is driving growth in its software business, higher-margin software revenue is increasingly accounting for a larger share of the mix.

Therefore, AppLovin expects at least a 50% margin for adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) compared to a 38% margin in the prior-year period.

With ongoing revenue growth and margin expansion, things still look good for AppLovin and its shareholders as 2024 gets going.

Jon Quast has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Savers who put money into traditional IRAs and 401(k)s get a nice tax break. Contributions up to an annual limit exempt some of your earnings from taxes, so if you fund one of these accounts, you get to not only set money aside for retirement, but pay the IRS a little less.

But because your contributions to a traditional IRA or 401(k) plan go in on a pre-tax basis, the IRS wants you to leave your money alone long enough for it to serve as income for retirement. As such, there’s a 10% early withdrawal penalty that generally applies to distributions from these accounts taken prior to age 59 1/2.

Now there are a few exceptions. IRAs, for example, allow you to withdraw up to $10,000 to purchase a first-time home. You can also tap an IRA early to pay for higher education.

Image source: Getty Images.

But even if you’re able to take an IRA or 401(k) withdrawal without incurring a penalty, doing so prior to actual retirement could hurt you in a very big way. Here’s why.

Clearly, a 10% early withdrawal penalty has the potential to cause you financial harm. But even if you’re able to avoid that penalty, raiding your IRA or 401(k) might harm you financially in another way.

The money in your IRA or 401(k) shouldn’t just sit in cash. Ideally, you’re investing that money so your balance grows nicely over time. As such, any dollar you remove from an IRA or 401(k) early is money you can’t keep investing. And the consequences there could be huge.

Let’s say you take a $10,000 withdrawal from your IRA at age 35 to purchase a home. But let’s also assume you then don’t retire until age 70. Furthermore, let’s assume that your IRA portfolio delivers an average annual return of 8%, which is a bit below the stock market’s average.

By missing out on the opportunity to earn 8% on your $10,000 withdrawal over 35 years, you’re losing out on almost $148,000 of retirement income. That could potentially constitute a few years’ worth of bills for your senior self, depending on what your costs turn out to be.

Once you turn 59 1/2, you can remove funds from your IRA or 401(k) without having to worry about a penalty. But even then, it’s important to be careful.

Let’s say you’re thinking of removing $20,000 from your 401(k) to renovate your home at age 60. That money is yours free and clear of penalties. But let’s also assume you’re not retiring until age 68, and that your portfolio delivers a yearly return of 6% in your 60s (since, by then, it’s good to shift to more conservative investments).

Losing out on a 6% return on $20,000 over eight years means missing out on about $32,000 in retirement income. That’s still a notable sum. It could, for example, end up being money you need to pay for healthcare down the line.

The fact that the IRS imposes early withdrawal penalties on IRAs and 401(k)s is actually sort of a good thing, since it may be the factor that helps you stay disciplined and avoid tapping your savings prematurely. But even if you’re able to avoid a penalty, it still pays to try not to take a withdrawal from your IRA or 401(k) until you’re actually retired and absolutely need that money.

The stock market has recently reached new all-time highs, but that doesn’t mean all stocks are expensive. In this video, I’ll reveal all five stocks I’m buying in my own portfolio this month and why I’m a big fan of each one right now.

*Stock prices used were the afternoon prices of March 5, 2024. The video was published on March 6, 2024.

Matt Frankel has positions in Block, EPR Properties, Roblox, SoFi Technologies, and Vanguard Specialized Funds-Vanguard Real Estate ETF. The Motley Fool has positions in and recommends Block, Roblox, and Vanguard Specialized Funds-Vanguard Real Estate ETF. The Motley Fool recommends EPR Properties. The Motley Fool has a disclosure policy. Matthew Frankel is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through their link they will earn some extra money that supports their channel. Their opinions remain their own and are unaffected by The Motley Fool.

Dogecoin recently jumped to the $0.2 level for the first time since November 2021 amidst a month of exceptional bullish price action. Notably, DOGE is currently up by 128% this month and 97% in the past seven days, giving DOGE holders something to be happy about. According to a crypto analyst, this price surge is expected to continue and go parabolic to the $1 mark in this market cycle.

Current market dynamics and bullish sentiment have seen DOGE shooting up in market capitalization after an extended consolidation period. A recent surge past the $0.20 price level saw DOGE briefly overtaking Cardano and jumping up to the eighth position in market cap rankings.

In a post shared on social media platform X, a crypto analyst known as Altcoin Sherpa, noted this recent surge as a sign of better things to come in this cycle. While the analyst didn’t give a particular price point, he noted that a $1 price per Dogecoin wouldn’t be too surprising.

$DOGE: Several notes on this one-

-Its going to go to crazy #s this cycle, I don’t know what. $1 wouldn’t honestly surprise me.-Chart itself looks good, consolidated for like 600 days.

-Given the overall mc, this one is NOT going to give you as big of gains as… pic.twitter.com/ifNdTGCr9L

— Altcoin Sherpa (@AltcoinSherpa) February 29, 2024

Interestingly, the $1 level would mean a ride to uncharted territory for DOGE, as the crypto is yet to cross above $0.8. A surge to $1 would mean a 465% surge from the current price level and past its current all-time high of $0.74.

The analyst noted that he doesn’t expect DOGE to perform as well as other meme-inspired cryptocurrencies with lower market caps like WIF, PEPE, and BONK, but its deep liquidity provides more of a stable investment. He also noted that DOGE and SHIB will probably take turns leading gains among meme coins.

The meme coin market has grown significantly since the early days of DOGE’s creation, which started out as a joke. Since then, tons of meme coins have been created, but Dogecoin continues to solidify its position as the largest meme coin in terms of market cap, demonstrating signs of renewed enthusiasm every so often.

At the time of writing, DOGE is trading at $0.18. Data from Coinglass shows that the open interest on DOGE futures contracts is now at $1.62 billion, a 10% increase in the past 24 hours.

Other meme coins are also witnessing strong interest. According to Santiment, SHIB, PEPE, FLOKI, and BONK have seen an increase of over 3,000% in trading volume in the past week. The on-chain analytics platform credits the increase in trading volume to surging prices and increased crowd interest.

📈 #Memecoins, particularly those that have been trending over the past week, have skyrocketed in trading volume due to surging prices and increased crowd interest. On average, $SHIB, $PEPE, $FLOKI, and $BONK has seen volume rise +3,000% in the past week. pic.twitter.com/AiIaEbgGIz

— Santiment (@santimentfeed) March 4, 2024

SHIB, PEPE, FLOKI, and BONK are up by 277%, 256%, 204%, and 145% respectively in the past seven days, outperforming DOGE during the time frame.

DOGE bulls hold up price | Source: DOGEUSD on Tradingview.com

Featured image from StormGain, chart from Tradingview.com

Disclaimer: The article is provided for educational purposes only. It does not represent the opinions of NewsBTC on whether to buy, sell or hold any investments and naturally investing carries risks. You are advised to conduct your own research before making any investment decisions. Use information provided on this website entirely at your own risk.

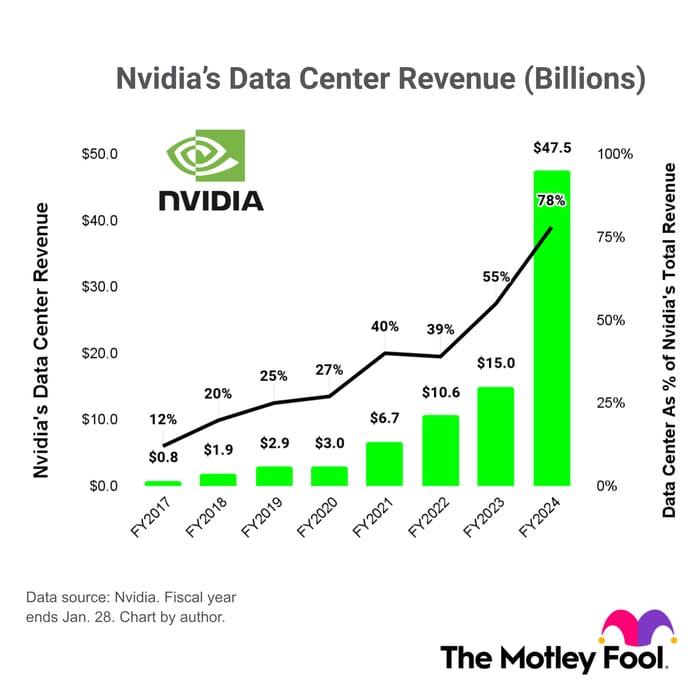

Nvidia (NVDA -0.22%) stock has soared 258% over the past 12 months. The initial hype surrounding artificial intelligence (AI) centered around OpenAI and its ChatGPT platform, which quickly attracted a $10 billion investment from Microsoft in early 2023.

However, the technology industry quickly realized OpenAI’s success wouldn’t have been possible without Nvidia’s specialized data center chips, which are designed specifically to process AI workloads. As a result, Nvidia experienced a tidal wave of demand — from the smallest of AI start-ups to the world’s largest tech giants.

Nvidia’s H100 graphics processing unit (GPU) was the hottest piece of AI hardware last year, and it drove the company’s data center revenue to $47.5 billion during its fiscal 2024 year (ended Jan. 28). That was a 217% increase from fiscal 2023.

As the below chart shows, the data center segment accounted for 78% of Nvidia’s total revenue ($60.9 billion) in fiscal 2024. That’s a substantial increase from just 12% in fiscal 2017, when the company generated just $830 million in revenue from the data center. Gaming dominated Nvidia’s business back then.

Nvidia will ramp up shipments of its new H200 GPU this year, which can inference (ingest live data so AI models can make predictions) twice as fast as the H100, while consuming half the amount of energy. That’s a winning combination for data center operators, so demand could be off the charts for the new chip.

Nvidia is now a $2 trillion company, yet despite its surge in value over the past year, its stock isn’t necessarily expensive based on forecast earnings per share for its fiscal 2025, which just began. Therefore, it won’t be a surprise if Nvidia stock continues to trend higher.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Microsoft and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The Shiba Inu price is going absolutely parabolic these days. Within the last 9 days, the SHIB price surged by more than 380%. Today, SHIB marked a two-year high at $0.00004574. Although the price suddenly dropped below $0.00002, marking a 54% within 2 hours, the price already recovered to above $0.000038. Here are four reasons driving the Shiba Inu price:

Bitcoin’s price rally, particularly after the US Securities and Exchange Commission’s (SEC) approval of spot Bitcoin Exchange-Traded Funds (ETFs) in January, has set the stage for a broader cryptocurrency market rally. The approval not only enhanced Bitcoin’s legitimacy among traditional investors but also acted as a catalyst for its price to approach its all-time high.

The Bitcoin halving event, anticipated in April, further adds to the bullish sentiment, as historical data suggest that halving events, which reduce the reward for mining new blocks by half, tend to lead to substantial price increases due to the reduced supply of new Bitcoins entering the market.

The relationship between Bitcoin’s price movements and the altcoin market, including meme coins like Shiba Inu, is well-documented. Bitcoin’s rally has a “halo effect” on the broader market, creating a risk-on environment where investors are more willing to explore higher-risk assets, leading to increased investments in altcoins and meme coins.

This phenomenon is further amplified by the Fear Of Missing Out (FOMO), as investors rush to capitalize on potential gains, driving up prices in a self-reinforcing cycle.

As reported yesterday, meme coins like SHIB could be one of the hottest bets in this crypto bull run. Why? Andrew Kang, co-founder and partner at Mechanism Capital, offered an analysis of meme coin psychology.

The appeal of meme coins lies in their ability to galvanize a community-driven speculative wave. Meme coins serve as a more accessible and globally available speculative vehicle compared to traditional stocks or more complex cryptocurrency projects.

The characterization of meme coins as a “Skill-based Global Lottery Platform” by Kang encapsulates the unique blend of community effort, skill, and luck that defines their market dynamics. This communal aspect, coupled with the thrill of speculation, fosters a highly engaging and participatory market environment.

Furthermore, the global accessibility and simplicity of meme coins make them an attractive entry point for new investors in the cryptocurrency market, thereby expanding the market base and increasing the liquidity and volatility of these assets. This broad appeal is crucial during bullish market phases, where the influx of new participants can significantly amplify price movements.

Elon Musk, renowned for his significant influence on crypto markets, particularly with meme coins like Dogecoin and FLOKI, has once again made waves with his social media activities. On February 26, Musk hinted at returning to “meme grindstone,” indirectly impacting meme coins.

Fine, I will get back on the meme grindstone 😂

— Elon Musk (@elonmusk) February 26, 2024

While not mentioning SHIB directly, the timing of Musk’s tweet corresponded with a notable uptick in its market performance. Several meme coins started to rally on February 26. The market seems to have interpreted his tweet as an indication that the present moment is opportune for investing in DOGE and other meme coins such as SHIB.

The Shiba Inu price exhibited a clear technical bullish setup. Last December, the price of SHIB surged past a two-year ascending triangle pattern and underwent a successful retest until early February. This development laid the groundwork for the substantial price surge, in conjunction with the previously mentioned factors.

SHIB’s breakthrough past the 20-, 50-, and 100-week Exponential Moving Averages (EMAs) affirmed its strong bullish trend. After surpassing the August 2022 peak of $0.00001791, SHIB’s upward momentum became unstoppable.

Featured image created with DALLE, chart from TradingView.com

Disclaimer: The article is provided for educational purposes only. It does not represent the opinions of NewsBTC on whether to buy, sell or hold any investments and naturally investing carries risks. You are advised to conduct your own research before making any investment decisions. Use information provided on this website entirely at your own risk.

As retirement approaches you must face the question, “What is the best age for me to claim Social Security?”

They almost unanimously advise waiting until full retirement age (66 and 6 months in 2024) to receive 100% of benefits earned. Postponing until the maximum payout at age 70 is even better, since 8% is added to your monthly check for each year you delay.

From a purely financial perspective, the logic is irrefutable. But there is another asset often ignored. One that could be considered even more valuable than money because it is constantly being spent and can never be saved.

Time.

We both started receiving Social Security at age 62, and it has turned out to be one of the best decisions we have ever made. Well, actually the choice was made for us when the 2007-09 recession of 2008 swept away our careers and much of our net worth.

Had what seemed at the time like a calamity not happened, we would have most likely followed conventional wisdom and kept working to save more money. Instead we took a leap of faith, moved abroad to a lower cost of living, and found ourselves staring at a blank canvas titled “Our Future” far sooner than planned.

It is said there are three phases of retirement — Go-Go (age 60 to 70), Slow-Go (70 to 80) and No-Go (80 and up). We hit the ground running at the beginning of our Go-Go period, and what an unexpected blessing those extra years have turned out to be in the following important aspects of life.

Also read: Think Donald Trump has promised not to change Social Security? Think again.

It is estimated that 7 out of 10 Americans aged 65 and older will need some form of costly long-term care. The most proactive way to be among the 30% who avoid this expense is by optimizing your health.

Full-time workers have trouble finding enough hours in their schedule for fitness and healthy food preparation. A recent study reveals only 25% of American adults meet CDC exercise standards, while another indicates a paltry 10% eat enough vegetables.

Early retirement provides an opportunity to jump-start improving one’s health. In addition to our pedestrian lifestyle (we haven’t owned a car for 14 years), devoting time each week to strength training, yoga and cardiovascular exercise keeps us in outstanding physical condition. Creating nutritious meals filled with lots of fresh fruits and vegetables is a fun activity instead of a chore.

Also see: I have about $3 million in pension and savings. Should I claim Social Security earlier than 70?

According to the American Psychological Association, stress is at an all-time high in the U.S. At the same time, research from Age Wave and Merrill Lynch reveals that retirement is the happiest and most content period of our lives.

Our experience certainly mirrors those findings. Leaving behind financial worries and the daily grind by retiring early has rewarded us with bonus years to expand our social network and pursue long-postponed activities and new interests.

More: Many retirees can’t wait until 70 to collect Social Security benefits, but they could if they used this strategy

Before moving to Ecuador we lived three time zones from our family. That travel distance combined with limited vacation days made visits shorter and less frequent than we desired.

Now, even though our residence is on a different continent, we have been fortunate to spend weeks at a time each year being with our grandchildren as they’ve grown from infants to pre-teens. This level of connection would have been difficult with only occasional long weekend trips.

We can share from a travel perspective that the Go, Slow and No-Go periods are accurately described. During the first decade of early retirement we flew back to the States multiple times each year as our four grandchildren were born. Between visits we explored Ecuador, cruised around the tip of South America, and spoke at conferences throughout Latin America.

Post-COVID, we recently concluded a full-time travel adventure of 2½ years to Mexico, Europe, Colombia, Argentina and locations within the U.S. Now squarely in the Slow-Go years, we are acutely aware that the level of activity we sustained for over a decade is no longer possible despite being in excellent health.

Our bank balance would without a doubt be higher if we could have waited until age 67 or 70 to begin collecting Social Security. Yet looking back, how thankful we are to have retired early and been able to share so many priceless memories during those initial retirement years.

You might like: This style of travel is growing more popular among the 50-plus set, and it can offer a richer, more relaxing experience

As you contemplate when to begin receiving Social Security benefits, carefully envision your ideal retirement. What do you want to accomplish, see and do? If you intend to work until the maximum retirement age of 70, keep in mind that the Social Security Administration estimates that American men who reach that age are likely to live another 13½ years, on average; American woman, almost another 16 years.

Keeping this information in mind, be realistic about your physical capabilities when making plans. Do you really want to spend the most active years you have left in the office and your entire, extended retirement in your Slow-Go and No-Go years? How unfortunate it would be to devote your Go-Go years to the workplace, only to find yourself having to use the extra income to pay for health issues instead of enjoying those activities you’ve looked forward to.

Also see: Vacations, cars and roof repairs: You may be surprised by how much you spend in retirement

It is tempting to fear you can never accumulate sufficient assets to retire comfortably. Instead, consider asking yourself, “How can I manifest the future I’ve dreamed of with what I have?”

Discovering ways to make more money in retirement is possible. But you can never create another minute of precious time.

Edd and Cynthia Staton write about retirement, expat living and health and wellness. They are authors of three bestselling books and creators of Retirement Reimagined!, an online program to help people considering the retirement option of moving abroad. Visit them at eddandcynthia.com.

This article is reprinted by permission from NextAvenue.org, ©2024 Twin Cities Public Television, Inc. All rights reserved.

More from Next Avenue:

The age at which you begin taking Social Security will affect your monthly income for the rest of your life, so it’s critical to make this decision carefully.

You can begin claiming at age 62 or anytime after that, and the longer you wait (up to age 70), the more you’ll receive each month. The age at which you file can affect your payments by hundreds of dollars per month, and if you’re going to be relying heavily on your benefits, this decision could make or break your retirement.

The age at which you should start taking benefits will depend largely on your situation, but it can be helpful to see the average payments at various ages. Here’s exactly how much the average retiree receives, as well as a few tips for deciding on the right age to make your claim.

Image source: Getty Images.

Your age is one of the most important factors influencing your benefit amount. To receive the full payments you’re entitled to based on your work history, you’ll need to wait until your full retirement age (FRA) to file. This age varies by birth year, but it’s 67 years old for everyone born in 1960 or later.

If you file before your FRA, your benefits will be reduced by up to 30%. By delaying past your FRA, you’ll earn your full benefit plus a bonus of between 24% and 32% per month. These adjustments are permanent, too, so the age at which you file will affect your income for the rest of your retirement.

The average retirement benefit varies widely by age. Here’s what those averages look like, according to the Social Security Administration’s most recent data released in December 2022:

| Age | Average Monthly Retirement Benefit |

|---|---|

| 62 | $1,275 |

| 63 | $1,365 |

| 64 | $1,412 |

| 65 | $1,505 |

| 66 | $1,720 |

| 67 | $1,845 |

| 68 | $1,848 |

| 69 | $1,819 |

| 70 | $1,963 |

Source: Social Security Administration. Table by author.

The average retiree at age 70 collects nearly $700 per month more than the average retiree at age 62. If your savings fall short or even run dry in retirement, those higher payments can go a long way.

There’s no one-size-fits-all approach as to when you should begin claiming Social Security. But to make the decision a little easier, there’s one question to ask yourself: What’s your biggest priority in retirement?

If maximizing your monthly income is your primary goal, delaying benefits until age 70 will help you achieve that. Because delaying benefits will result in larger checks for the rest of your life, this strategy can help you enjoy a more financially secure retirement — even if your savings eventually run out.

Waiting a few years to claim can also be a smart idea if you’re worried about benefit cuts. While Social Security isn’t going away, there could potentially be cuts within the next decade or so if Congress can’t fund a solution to the program’s cash shortfall. If that happens, having bigger checks to begin with can help cushion the blow.

That said, there are valid reasons to consider filing early, too. For example, if you’re battling health issues or have reason to believe you won’t live well into your 70s or beyond, it may not make sense to delay benefits. While you’ll still receive smaller monthly payments by claiming early, you could collect more over a lifetime than if you were to delay.

Finally, if you have a robust retirement fund and don’t necessarily need the extra cash from Social Security, filing early can make it easier to retire earlier. You don’t have to file for benefits as soon as you retire, but doing so can give you some extra income each month so you’re not relying entirely on your savings — and risking depleting your retirement fund too quickly.

There’s not necessarily a “best” time to take Social Security, as it will depend on your unique circumstances. But when you know how your age will affect your benefit amount, it can help make the decision a little easier.

Joining the world’s most exclusive club — the top 1% — has arguably never looked more doable, but a lot depends on the country in which you’re trying to achieve that status.

That’s according to the 2024 Knight Frank Wealth Report, which lays out how many millions it takes for an individual to join the most-moneyed club across the world.

As exclusive as the one-percenter appellation may sound, it’s “actually easier to become a member of this particular club than it is to gain UHNWI status,” observes the Knight Frank report, released Wednesday.

Anyone who has achieved UHNWI status is an ultra-high-net-worth individual with net wealth of $30 million or more.

Define “easier,” right? The country with the highest barrier to 1% entry is Monaco, where more than $12.8 million is required to be part of that top-percentage-point category as of the end of 2023.

The five countries with the highest bars to entry are Monaco, Luxembourg, Switzerland, the U.S. and Singapore.

In the U.S., the threshold is $5.8 million. And for those seeking a fast track into the 1% club, and with unrestricted freedom to relocate, in China, at the bottom of that list of 17 countries, just over $1 million is required to qualify as a one-percenter, and, just ahead of it is Japan, where just under $2 million is needed.

Knight Frank, a global real-estate firm, said the number of UHNWI individuals globally rose by 4.2% to 626,619 from 601,300 a year earlier, which more than reversed a decline seen in 2022.

The report included an attitudes survey that showed how optimistic money managers were that their clients would amass more wealth in 2024. On a scale of 1 to 5, the Middle East came out on top, with North America lower down, according to this chart:

Looking across generations, the report found one group in particular was most optimistic about building their wealth — Generation Z (born between 1997 and 2012, by the Pew Research Center’s reckoning), of whom 75% said they expected their wealth to increase in 2024. Boomers (born, according to the U.S. Census Bureau, between mid-1946 and mid-1964) were, among survey respondents, at the lower end, with Generation X (born from the end of the postwar baby boom through 1980) not far behind, at just over 50% each.

Read on: Retirement balances are at their highest in nearly two years, with 20% jump in 401(k) millionaires