The Federal Reserve should keep credit conditions tight for now.

Source link

The Federal Reserve should keep credit conditions tight for now.

Source link

U.S. small-cap stocks are “challenged” as Wall Street pushes out expectations for when the Federal Reserve may begin lowering interest rates due to concerns over persistent inflation, according to BofA Global Research.

Source link

Some exchange-traded funds rallied Wednesday even as stocks and bonds broadly fell, as hot inflation data stoked fears that interest rates will stay elevated for longer than anticipated.

Source link

US Federal Reserve Chair Jerome Powell attends a “Fed Listens” event in Washington, DC, on October 4, 2019.

Eric Baradat | AFP | Getty Images

A hotter-than-expected consumer price index report rattled Wall Street Wednesday, but markets are buzzing about an even more specific prices gauge contained within the data — the so-called supercore inflation reading.

Along with the overall inflation measure, economists also look at the core CPI, which excludes volatile food and energy prices, to find the true trend. The supercore gauge, which also excludes shelter and rent costs from its services reading, takes it even a step further. Fed officials say it is useful in the current climate as they see elevated housing inflation as a temporary problem and not as good a measure of underlying prices.

Supercore accelerated to a 4.8% pace year over year in March, the highest in 11 months.

Tom Fitzpatrick, managing director of global market insights at R.J. O’Brien & Associates, said if you take the readings of the last three months and annualize them, you’re looking at a supercore inflation rate of more than 8%, far from the Federal Reserve’s 2% goal.

“As we sit here today, I think they’re probably pulling their hair out,” Fitzpatrick said.

CPI increased 3.5% year over year last month, above the Dow Jones estimate that called for 3.4%. The data pressured equities and sent Treasury yields higher on Wednesday, and pushed futures market traders to extend out expectations for the central bank’s first rate cut to September from June, according to the CME Group’s FedWatch tool.

“At the end of the day, they don’t really care as long as they get to 2%, but the reality is you’re not going to get to a sustained 2% if you don’t get a key cooling in services prices, [and] at this point we’re not seeing it,” said Stephen Stanley, chief economist at Santander U.S.

Wall Street has been keenly aware of the trend coming from supercore inflation from the beginning of the year. A move higher in the metric from January’s CPI print was enough to hinder the market’s “perception the Fed was winning the battle with inflation [and] this will remain an open question for months to come,” according to BMO Capital Markets head of U.S. rates strategy Ian Lyngen.

Another problem for the Fed, Fitzpatrick says, lies in the differing macroeconomic backdrop of demand-driven inflation and robust stimulus payments that equipped consumers to beef up discretionary spending in 2021 and 2022 while also stoking record inflation levels.

Today, he added, the picture is more complicated because some of the most stubborn components of services inflation are household necessities like car and housing insurance as well as property taxes.

“They are so scared by what happened in 2021 and 2022 that we’re not starting from the same point as we have on other occasions,” Fitzpatrick added. “The problem is, if you look at all of this [together] these are not discretionary spending items, [and] it puts them between a rock and a hard place.”

Further complicating the backdrop is a dwindling consumer savings rate and higher borrowing costs which make the central bank more likely to keep monetary policy restrictive “until something breaks,” Fitzpatrick said.

The Fed will have a hard time bringing down inflation with more rate hikes because the current drivers are stickier and not as sensitive to tighter monetary policy, he cautioned. Fitzpatrick said the recent upward moves in inflation are more closely analogous to tax increases.

While Stanley opines that the Fed is still far removed from hiking interest rates further, doing so will remain a possibility so long as inflation remains elevated above the 2% target.

“I think by and large inflation will come down and they’ll cut rates later than we thought,” Stanley said. “The question becomes are we looking at something that’s become entrenched here? At some point, I imagine the possibility of rate hikes comes back into focus.”

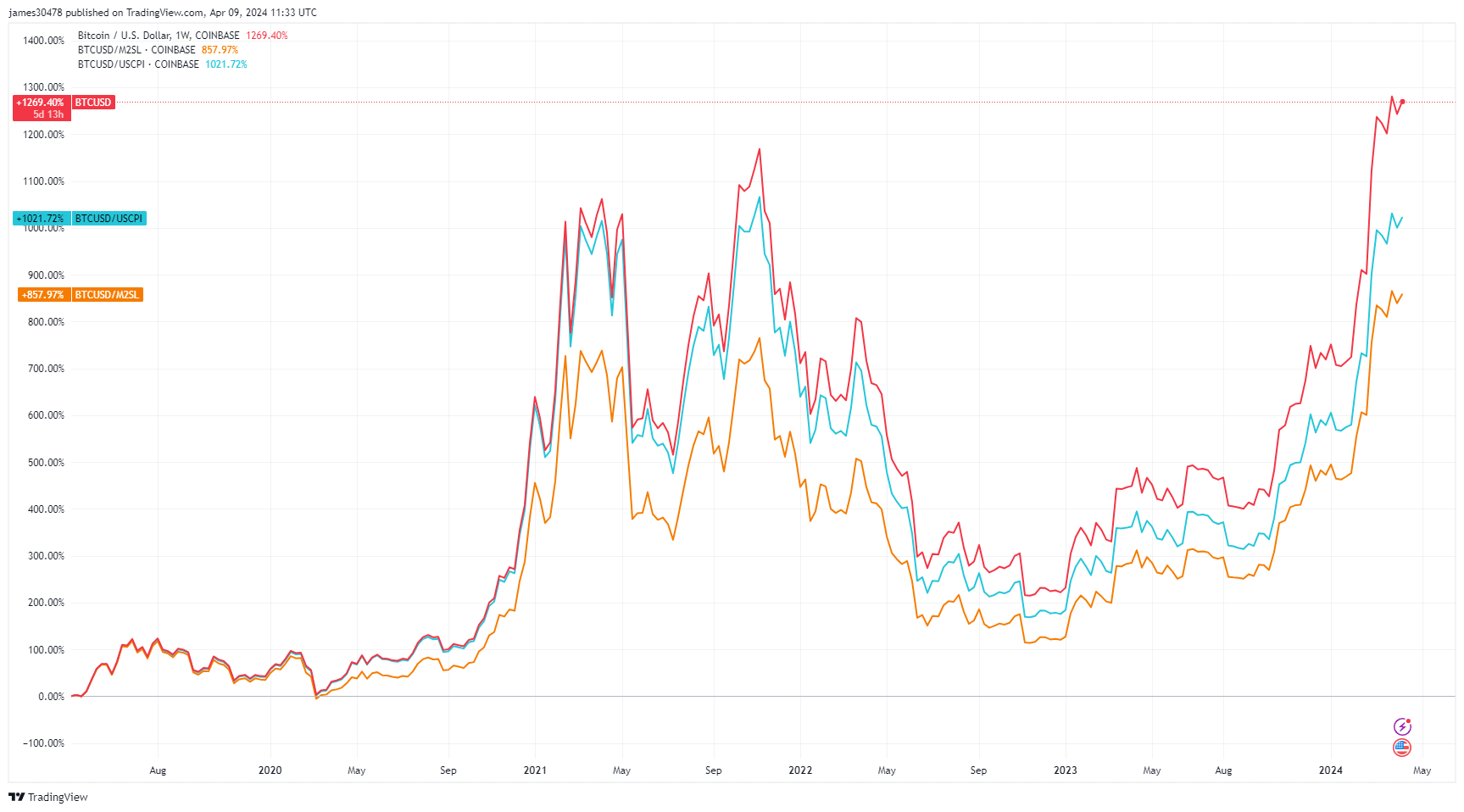

When assessing the performance of assets or currencies, it is essential to consider both nominal and real returns, the latter of which accounts for inflation. Inflation can be gauged through different metrics, such as the consumer price index (CPI) or indicators related to the money supply (e.g., M2). While the money supply is not a direct measure of inflation, it can play a role in shaping it. However, when evaluating an asset’s performance in a local currency, such as the British Pound (GBP), it is often useful to benchmark it against the US Dollar.

A prime example is the FTSE 100, which has risen approximately 23% since 2007 and recently achieved an all-time high, surpassing 8,000 in GBP terms. At first glance, this may appear impressive. However, when converted to US Dollars, the FTSE 100 has actually declined by 22% over the same period, while the GBP has fallen 37% against the Dollar. The situation becomes even more alarming when measured against the UK’s M2 money supply, revealing a staggering 62% decrease.

Bitcoin, over its historical trajectory benchmarked in USD, has consistently surged to new highs with each cycle, surpassing a remarkable 1200% increase in the past five years. Furthermore, it has demonstrated the capacity to outperform the M2 money supply and is nearing record highs relative to the US Consumer Price Index (CPI).

To gain a comprehensive understanding of an asset’s true performance, I believe it should first be converted into US Dollars (if measured in a local currency) and then adjusted for local CPI inflation and money supply changes. This approach provides a more accurate and holistic view of the asset’s real value and performance over time.

The post FTSE 100’s illusion of growth unmasked by currency and inflation adjustments appeared first on CryptoSlate.

Forecasts lacked realistic representations of price and wage setting.

Source link

In a recent analysis, economist Peter Schiff draws stark comparisons between the current U.S. economic optimism and the prelude to the 2008 financial crisis. Schiff, leveraging his expertise, warns of impending financial turmoil, emphasizing the critical role of money supply in understanding economic health. Peter Schiff Warns: U.S. Economy on the Brink, Echoes of 2008 […]

In a recent analysis, economist Peter Schiff draws stark comparisons between the current U.S. economic optimism and the prelude to the 2008 financial crisis. Schiff, leveraging his expertise, warns of impending financial turmoil, emphasizing the critical role of money supply in understanding economic health. Peter Schiff Warns: U.S. Economy on the Brink, Echoes of 2008 […]

Source link

The Bank of England in the City of London, after figures showed Britain’s economy slipped into a recession at the end of 2023.

Yui Mok | Pa Images | Getty Images

LONDON — The Bank of England is widely expected to keep interest rates unchanged at 5.25% on Thursday, but economists are divided on when the first cut will come.

Headline inflation slid by more than expected to an annual 3.4% in February, hitting its lowest level since September 2021, data showed Wednesday. The central bank expects the consumer price index to return to its 2% target in the second quarter, as the household energy price cap is once again lowered in April.

The larger-than-expected fall in both the headline and core figures was welcome news for policymakers ahead of this week’s interest rate decision, though the Monetary Policy Committee has so far been reluctant to offer strong guidance on the timing of its first reduction.

The U.K. economy slid into a technical recession in the final quarter of 2023 and has endured two years of stagnation, following a huge gas supply shock in the wake of Russia’s invasion of Ukraine. Berenberg Senior Economist Kallum Pickering said that the Bank will likely hope to loosen policy soon in order to support a burgeoning economic recovery.

Pickering suggested that, in light of the inflation data of Wednesday, the MPC may “give a nod to current market expectations for a first cut in June,” which it can then cement in the updated economic projections of May.

“A further dovish tweak at the March meeting would be in line with the trend in recent meetings of policymakers gradually losing their hawkish bias and turning instead towards the question of when to cut rates,” he added.

At the February meeting, two of the nine MPC decision-makers still voted to hike the main Bank rate by another 25 basis points to 5.5%, while another voted to cut by 25 basis points. Pickering suggested both hawks may opt to hold rates this week, or that one more member may favor a cut, and noted that “the early moves of dissenters have often signalled upcoming turning points” in the Bank’s rate cycles.

Berenberg expects headline annual inflation to fall to 2% in the spring and remain close to that level for the remainder of the year. It is anticipating five 25 basis point cuts from the Bank to take its main rate to 4% by the end of the year, before a further 50 basis points of cuts to 3.5% in early 2025. This would still mean interest rates would exceed inflation through at least the next two years.

“The risks to our call are tilted towards fewer cuts in 2025 – especially if the economic recovery builds a head of steam and policymakers begin to worry that strong growth could reignite wage pressures in already tight labour markets,” Pickering added.

A key focus for the MPC has been the U.K.’s tight labor market, which it feared risked entrenching inflationary risks in the economy.

January data published last week showed a weaker picture across all labor market metrics, with wage growth slowing, unemployment rising and vacancy numbers slipping for the 20th consecutive month.

Victoria Clarke, U.K. chief economist at Santander CIB, said that, after last week’s softer labor market figures, the inflation reading of Wednesday was a further indication that embedded risks have reduced and that inflation is on a path towards a sustainable return to target.

“Nevertheless, services inflation is largely tracking the BoE forecast since February, and remains elevated. As such, we do not expect the BoE to conclude it is ‘home and dry’, especially with April being a critical point for U.K. inflation, with the near 10% National Living Wage rise and many firms already having announced, and some implemented, their living wage-linked pay increases,” Clarke said by email.

“The BoE needs data on how broad an uplift this delivers to pay-setting, and hard information on how much is passed through to price-setting over the months that follow.”

Santander judges that the Bank could decide it has seen enough data to cut rates in June, but Clarke argued that an August trim would be “more prudent” given the “month-to-month noise” in labor market figures.

This sentiment was echoed by Moody’s Analytics on Wednesday, with Senior Economist David Muir also suggesting that the MPC will need more evidence to be satisfied that inflationary pressures are contained.

“In particular, services inflation, and wage growth, need to moderate further. We expect this necessary easing to unfold through the first half of the year, allowing a cut in interest rates to be announced in August. That said, uncertainty is high around the timing and the extent of rate cuts this year,” Muir added.

The housing market is showing signs of a recovery as the spring home-buying season gets underway.

Mortgage rates fell for the second week in a row, declining to the lowest level in more than a month. The average rate on the benchmark 30-year fixed mortgage fell to 6.74% from 6.88% the week prior, per Freddie Mac.

And as mortgage rates decline, supply is starting to rebound. New listings hit a 17-month high in February, while the total number of homes for sale rose to the highest level in a year, according to Redfin (RDFN).

Read more: Mortgage rates hover around 7% — is this a good time to buy a house?

It’s an improvement from last year’s depressed levels, but supply-demand remains far from balanced. The culprit: Side effects of the Fed’s aggressive rate-hiking campaign.

Top economist Gary Shilling told Yahoo Finance that the Fed’s change in interest rate policy created a “perfect storm” for the industry, with higher rates prompting would-be sellers to stay put, as many have locked in ultra-low rates during the pandemic or in the years prior.

The giant gap between current and past mortgage rates is creating “artificial tightness” in the housing market. “It won’t continue indefinitely, but it certainly is disruptive right now,” Shilling said.

Redfin CEO Glenn Kelman expects the Fed’s recent moves to affect the housing sector for decades, warning it will take years to work through the aftershocks of the central bank’s aggressive rate-hiking campaign.

“There’s going to be low supply for a long time to come,” Kelman told Yahoo Finance. “What the Fed did … will have a 30-year tail on it.”

Lackluster supply has kept home prices elevated. The median price of previously owned homes rose 5.1% in January from a year ago, with all four US regions showing price growth, according to the National Association of Realtors.

Any hope of relief for the housing sector may be postponed. A series of hotter-than-expected inflation prints has bolstered the case for policymakers to delay rate cuts, according to Oppenheimer’s John Stoltzfus. He told Yahoo Finance Live that he thinks the Fed won’t cut rates until at least its June meeting.

A delayed rate cut suggests, at least in the near term, that mortgage rates are unlikely to fall much further, potentially postponing a more substantial rebound in the housing market.

“We need more supply. The real gate on home sales has been the number of homes for sale,” Kelman explained. “If interest rates don’t come down significantly, we’ll see a modest uptick in inventory, but to see a big gain, you’re going to have to see a real drop in mortgage interest rates.”

Moody’s Analytics expects a total housing deficit of 1.5 million to 2 million units this year, with a shortfall of up to 1.2 million for single-family homes.

Seana Smith is an anchor at Yahoo Finance. Follow Smith on Twitter @SeanaNSmith. Tips on deals, mergers, activist situations, or anything else? Email seanasmith@yahooinc.com.

Click here for real estate and housing market news, reports, and analysis to inform your investing decisions.

Jerome Powell just revealed a hidden reason why inflation is staying high: The economy is increasingly uninsurable

Source link