Nov 29, 2023, 6:40 am EST

Share

Reprints

Investors can find plenty to admire in Charlie Munger, Warren Buffett’s business partner who has passed away just shy of his 100th birthday.

Continue reading this article with a Barron’s subscription.

Nov 29, 2023, 6:40 am EST

Share

Reprints

Investors can find plenty to admire in Charlie Munger, Warren Buffett’s business partner who has passed away just shy of his 100th birthday.

Continue reading this article with a Barron’s subscription.

Disney CEO Bob Iger speaking with CNBC’s David Faber at the Allen&Co. Annual Conference in Sun Valley, Idaho.

David A. Grogan | CNBC

ValueAct Capital has taken a significant stake in Disney (DIS) and has been in dialogue with Disney’s management, the Activist Spotlight has learned. This is a new stake not previously disclosed in filings or media reports.

Here’s a breakdown of the situation:

Business: Disney is one of the most iconic entertainment companies globally. It operates through two segments, Disney Media and Entertainment Distribution; and Disney Parks, Experiences and Products. Disney engages in film and TV content production and distribution activities, as well as operates television broadcast networks and studios.

Stock Market Value: $167 Billion ($91.07 a share)

Percentage Ownership: n/a

Average Cost: low $80s per share

Activist Commentary: ValueAct has been a premier corporate governance investor for over 20 years. ValueAct principals are generally on the boards of half of ValueAct’s core portfolio positions and have had 56 public company board seats over 23 years. ValueAct has filed 89 13D’s in their history and has had an average return of 57.57% versus 17.52% for the S&P 500 over the same period.

ValueAct knows technology very well as seen by their active investments at Salesforce, Microsoft, and Adobe where they had board seats. They also know media well as active investors at the New York Times, Spotify and 21st Century Fox.

ValueAct began buying Disney this summer during the WGA and SAG strikes and it is one of the firm’s largest positions. The activist investor has been in dialogue with Disney’s management and are still growing their position today.

ValueAct believes that Disney’s theme parks and consumer products businesses and their $10 billion in EBIT (earnings before interest and taxes) are alone worth low $80s per share, ValueAct’s approximate cost basis in the stock.

The theme parks unit has a high return on capital, allowing Disney to further monetize its intellectual property. Amongst its peers like Warner Bros, Paramount and Netflix, Disney is the only one who has this advantage. Moreover, this is a business that is not threatened by technology, but enhanced by it.

For example, Disney’s Genie app, which allows park visitors to be guided through the parks in a way that minimizes their wait time, greatly enhances the visitor experience. Moreover, Disney has recently announced that it will be investing $60 billion into theme parks, which will be money well spent.

Disney YTD

This theme park valuation implies an almost zero valuation for the rest of Disney’s business that includes ESPN, theatrical movie releases, Disney+, Hulu and its television networks. Like digital news and music, video streaming was greatly disrupted by the internet and the low cost of capital from 2016 to 2021 afforded streaming companies, almost unlimited capital to acquire customers at any cost. Then with rising interest rates and inflation, that bubble burst in 2022 and there was a massive re-rating of assets globally.

Many of the high-growth companies that had easy access to capital now find themselves the most capital constrained they had been in a long time. This gives a huge advantage to companies like Disney, which has a market leading brand and an incumbent business model with strong customer relations.

Now, these streaming wars are in the process of resolving and companies are focused more on profitability than acquiring customers at any cost. This means cutting costs and creating growing and sustainable revenue.

ValueAct has experience in both of these areas. At Salesforce, where ValueAct CIO Mason Morfit is on the board, margins have gone from 18% to 32% while the stock has gone from $130 to $220 in 10 months. Disney has already announced an aggressive cost cutting plan, but it is the revenue opportunity that is more interesting here.

At portfolio companies like Adobe, Microsoft, Salesforce, Spotify and the New York Times, ValueAct has advocated for and assisted in creating bundles, pricing tiers and advertising stacks that have led to less churn, more pricing power, higher average revenue per user and even better advertising technology.

Both the New York Times and Spotify increased their bundles (NYT with Wordle, the Athletic, etc.; Spotify with podcasting and audiobooks) and both increased subscription pricing. The New York Times’ stock went from $30 per share to $45 per share and Spotify went from approximately $80 per share to $175 per share. Disney has numerous opportunities for bundling, price tiers, etc. and there are many ways this can work out through its present assets, M&A, alliances and licensing, but intelligently bundling its products will lead to more stable and valuable revenue. Based on similar situations that ValueAct has been involved in, this could lead to up to $15 billion of EBIT for the media assets and a Disney stock price as high as $190 per share.

ValueAct has a history of creating value through board seats, including at Salesforce and Microsoft, but has also added value as active shareholders in situations like Spotify and the New York Times.

I would expect that they would want a board seat here and as someone who has a reputation of working amicably and constructively with boards, the Disney board should welcome them with open arms. Aside from their extensive experience at technology companies and media companies and their innovative and relevant history of growing sustainable revenue at similar companies, there is one other reason shareholders should welcome them to the board.

Bob Iger returned to Disney in 2022 with an initial two-year contract with the explicit goal of righting the ship. The board formed a succession planning committee at that time. Iger subsequently extended his employment agreement through 2026 but longer-term succession remains one of the board’s most important priorities. Having a shareholder representative on the board is very helpful in that area particularly one like ValueAct, whose CIO participated in one of the most audacious and successful CEO successions ever when Satya Nadella replaced Steve Ballmer as CEO of Microsoft. Someone with that experience and perspective would be invaluable in navigating CEO succession at Disney.

Finally, we cannot ignore the fact that Disney is presently the target of a proxy fight by Nelson Peltz and Trian Partners that is turning somewhat confrontational. This certainly gives the Disney board an alternative they were not expecting.

Ken Squire is the founder and president of 13D Monitor, an institutional research service on shareholder activism, and the founder and portfolio manager of the 13D Activist Fund, a mutual fund that invests in a portfolio of activist 13D investments.

Michael Burry, who famously shorted subprime mortgages during the 2008 financial crisis, closed his bets against the S&P 500 and the Nasdaq 100 in the third quarter.

But he also found another industry to short: semiconductors.

Burry’s hedge fund Scion Capital disclosed Tuesday in a federal filing with the SEC that it had closed out “put” positions on the SPDR S&P 500 ETF (SPY) and Invesco QQQ Trust (QQQ), which tracks the Nasdaq 100 index, as of the end of September.

Those bearish bets amounted to more than $1.6 billion as of the last trading day of the second quarter. The indexes fell 3.6% and 3%, respectively, during the third quarter.

Burry gained fame for his moves during the 2008 crisis, a severe downturn that began with a US housing bust. Burry predicted a collapse in residential real estate prices as early as 2007 and then shorted a number of subprime deals through the use of credit default swaps.

He became a central figure in Michael Lewis’s 2010 book “The Big Short,” and Christian Bale later portrayed Burry in a 2015 film adaptation of the Lewis book.

Scion Capital broadly shrank its exposure to the stock market in the third quarter, according to its new SEC filing, selling 76% of the stocks it disclosed at the end of the second quarter.

But Scion reopened positions in JD.com and China-tech giant Alibaba (BABA) after selling out of the companies in the second quarter.

The hedge fund also eliminated its remaining exposure to regional lender New York Community Bank (NYCB). In the first quarter, Scion spent more than $23 million betting on financial stocks during a chaotic period marked by several prominent bank failures.

Burry, however, isn’t finished shorting stocks.

Scion opened two new positions, one shorting 100,000 shares of BlackRock’s semiconductor ETF, the iShares Semiconductor ETF (SOXX), and another 2,500 shares betting against online travel website Booking Holdings Inc. (BKNG).

The firm also purchased 1,500 shares of Booking Holdings Inc. outright.

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance

Garlinghouse emphasized the need for the SEC to reassess its regulatory approach, moving away from a pattern of enforcement through lawsuits.

During the just-concluded Ripple’s Swell conference in Dubai, the company’s CEO Brad Garlinghouse shared his views regarding the United States Securities and Exchange Commission’s (SEC) role in protecting consumers against bad actors.

In an interview with CNBC’s Dan Murphy, Garlinghouse stated that, in his opinion, the SEC has strayed from its commitment to investor protection, questioning the agency’s priorities in the process.

“I think the SEC, in my opinion, has lost sight of their mission to protect investors. And the question is, who are they protecting in this journey?” Garlinghouse told CNBC.

Garlinghouse’s opinion stemmed from the SEC’s enforcement actions against the crypto industry, as the agency has chosen a litigious approach to regulating the emerging economy instead of working with Congress to introduce befitting regulations for the crypto space.

In 2020, the financial watchdog sued Ripple alongside two executives, including the CEO, for orchestrating a $1.3 billion securities fraud by selling XRP to retail investors in the US.

The lawsuit centered around Ripple’s failure to register the continuous sale of XRP tokens, leaving investors without essential information about the digital asset and Ripple’s business activities.

After over two years of court battles between the SEC and Ripple, US District Judge Analisa Torres in Manhattan finally ruled in July that XRP is not a security and possesses no qualities of a security token.

The SEC’s request for an interlocutory appeal was subsequently denied, and in October, the agency dropped securities law violation charges against Garlinghouse and another Ripple executive, Chris Larsen.

Garlinghouse, reflecting on the developments, expressed optimism not only for Ripple but for the entire industry. He sees the SEC being put in check as a positive step, hoping it will pave the way for the crypto industry to flourish in the United States.

“I think it is a positive step for the industry, not just for Ripple, not just for Chris and Brad, but for the whole industry, that the SEC has been put in check in the United States. And I’m hopeful this will be a thawing of the permafrost in the United States for really seeing an amazing industry that has immense potential to thrive in the largest economy in the world,” Garlinghouse told CNBC.

In criticizing the SEC’s regulatory strategy, Garlinghouse drew parallels with other legal battles in the industry. The Ripple CEO referenced Grayscale’s victory regarding a Bitcoin exchange-traded fund (ETF), where a federal judge accused the SEC of being “arbitrary and capricious.”

Garlinghouse emphasized the need for the SEC to reassess its regulatory approach, moving away from a pattern of enforcement through lawsuits.

“Generally, judges tend to be pretty down the middle and try not to be dramatic — those are damning words. So I think at some point the SEC has to step back and realize that their regulatory approach through enforcement, let’s bring lawsuits, has to break,” said he.

Garlinghouse, influenced by the SEC’s regulatory style against the industry, asserted that Ripple had redirected its recruitment focus to other jurisdictions.

During a September interview at the Token2049 conference in Singapore, he outlined the company’s strategy to recruit 80% of its workforce from countries he deemed more proficient in crypto regulation.

Expressing his dissatisfaction, Garlinghouse pointed out the contrast in markets like Singapore, where governments collaborate with the industry, provide explicit regulations, and witness substantial growth.

“It’s super frustrating to see markets like we have here in Singapore … where the governments are partnering with the industry, and you’re seeing leadership providing clear rules and growth. And frankly, that’s why Ripple is hiring there,” explained the CEO.

next

A Roth individual retirement account (IRA) is retirement savings account that a person can contribute to each year. Under certain circumstances, funds can be withdrawn tax-free.

The money saved in a Roth IRA can be invested in financial instruments, such as equities, bonds, or savings accounts. Contributions to a Roth IRA are made with after-tax money, meaning that the contributions are made after income taxes have been paid on the income used for the contributions.

Roth IRAs offer a long-term tax benefit since withdrawals of contributions and investment earnings are not taxed in retirement. However, Roth IRAs may not be the right retirement account for everyone. Although there are benefits to Roth IRAs, there are also distinct disadvantages that should be considered.

Roth and traditional IRAs are excellent ways to stash money away for retirement. However, there are annual contribution limits. For 2023, individuals can contribute a maximum of $6,500 each year or $7,500 if they’re age 50 or older. For 2024 the standard limit is $7,000, and the limit for those 50 and older is $8,000.

To contribute to either, you must have earned income, which is money earned from working or owning a business. Also, you cannot deposit more than you’ve earned in a given year. Despite these similarities, the accounts are quite different. Below are the disadvantages of Roth IRAs.

One disadvantage of the Roth IRA is that you can’t contribute to one if you make too much money. The limits are based on your modified adjusted gross income (MAGI) and tax filing status. To find your MAGI, start with your adjusted gross income (AGI)—you can find this on your tax return—and add back certain deductions.

In general:

Below is a rundown of the Roth IRA income and contribution limits for 2023 and 2024.

| 2023 and 2024 Roth IRA Income and Contribution Limits | ||||

|---|---|---|---|---|

| Filing Status | MAGI 2023 | Contribution Limit 2023 | MAGI 2024 | Contribution Limit 2024 |

| Married Filing Jointly or Qualifying Widow(er) | ||||

| Less than $218,000 | $6,500 ($7,500 if age 50+) | Less than $230,000 | $7,000 ($8,000 if age 50+) | |

| $218,000 to $228,000 | Phase out range | $230,000 to $240,000 | Phase out range | |

| More than $228,000 | Ineligible for direct Roth IRA | More than $240,000 | Ineligible for direct Roth IRA | |

| Married Filing Separately | ||||

| Less than $10,000 | Phase out range | Less than $10,000 | Phase out range | |

| $10,000 or more | Ineligible for direct Roth IRA | $10,000 or more | Ineligible for direct Roth IRA | |

| Single or Head of Household | ||||

| Less than $138,000 | $6,500 ($7,500 if age 50+) | Less than $146,000 | $7,000 ($8,000 if age 50+) | |

| $138,000 to $153,000 | Phase out range | $146,000 to $161,000 | Phase out range | |

| More than $153,000 | Ineligible for direct Roth IRA | More than $161,000 | Ineligible for direct Roth IRA | |

Married taxpayers filing separately can use the single/head of household limits if they have not lived with their spouse at any time during the tax year.

There’s a tricky but perfectly legal way for high-income earners to contribute to a Roth IRA even if their income exceeds the limits. This is called a backdoor Roth IRA, which entails contributing to a traditional IRA and immediately rolling over the money into a Roth account.

This transaction must be done strictly by Internal Revenue Service rules.

The biggest difference between traditional and Roth IRAs is when taxes are due. A traditional IRA deducts your contributions in the year when you earn them. This provides an immediate tax break that leaves you with more money in your pocket. The downside is that income taxes are due on funds when withdrawals are made during retirement.

Roth IRAs work the opposite way. You don’t get an up-front tax break with your contributions but you may be eligible for a saver’s tax credit. When you plan to use your money, withdrawals in retirement are generally tax-free.

You make Roth IRA contributions with after-tax dollars, so you don’t get the up-front tax break traditional IRAs offer.

However, no up-front tax break means that you’ll get less money in your paycheck to spend, save, and invest. And tax-free withdrawals in retirement are something to look forward to—unless you’ll be in a lower tax bracket in the future than you are now.

Depending on your situation and whether you qualify for a saver’s tax credit, you could benefit more from a traditional IRA’s up-front tax break and then pay taxes at your lower rate in retirement. It’s worth crunching the numbers before you make any decisions since there’s potentially a lot of money at stake.

With a Roth IRA, you can withdraw your contributions at any time, for any reason, without tax or penalty. In addition, qualified withdrawals (which include contributions and account earnings) in retirement are also tax and penalty-free. To be qualified, the withdrawals must occur when you’re at least 59½ years old and it’s been at least five years since you first contributed to a Roth IRA—also known as the five-year rule.

If you don’t meet the five-year rule, then any earnings that you withdraw could be subject to taxes or a 10% penalty—or both, depending on your age:

The five-year rule should be carefully considered if you start a Roth later in life. For example, if you first contributed to a Roth at 58, you must wait until you’re 63 to make tax-free withdrawals of earnings—although you may still be able to withdraw contributions within this five-year window. For those who need the earnings to be accessible tax-free in less than five years, the five-year rule is a hinderance. For those who are saving for retirement on a longer timeline, the rule may be insignificant.

Yes. Your contributions to a Roth IRA can be withdrawn at any time without penalty or taxes. Only earnings are subject to the five-year rule.

Your modified adjusted gross income (MAGI) is your adjusted gross income (AGI) with a few deductions added back. Deductions reapplied include half of the self-employment tax, deductions for student loan interest, rental losses, and more.

No. There are no income limits to contribute to a traditional individual retirement account (IRA). Roth IRAs base your ability to contribute the maximum of $6,500 for 2023 or $7,000 in 2024 on your MAGI. People over age 50 can contribute an additional $1,000 catch-up contribution. However, the deduction for your contributions to a traditional IRA may be limited if you or your spouse is covered by a retirement plan at work and your income exceeds certain levels.

Roth IRAs offer many benefits; tax-free growth, tax-free withdrawals in retirement, and no required minimum distributions (RMDs) while the owner of the IRA is alive. However, there are potential drawbacks.

Typically, individuals benefit from saving for retirement in an IRA. However, whether a traditional or Roth IRA is better depends on several factors, including your income, age, and when you expect to be in a lower tax bracket—now or during retirement. Please consult a tax expert, financial planner, or financial advisor to help you make a more informed decision so that your retirement plan is customized for your specific financial situation.

Correction—May 28, 2023: This article has been edited to clarify that the five-year rule applies to Roth IRA earnings, not contributions.

Investing in the stock market is one of the best ways to build lasting wealth. Even seemingly small sums of capital can turn into huge amounts given enough patience and discipline to stay the course. And what’s most encouraging is that even beginners can do well over time.

The stock market isn’t just reserved for experts; new investors can position their portfolios to produce strong returns. Buying these two growth stocks is a wonderful place to start. Let’s take a closer look.

The first business to consider owning is Costco Wholesale (COST 2.46%). Even though it sells high-quality merchandise in a range of product categories, this chain of buyers’ club stores is known for having some of the lowest prices around. And this has been especially important for consumers in the past couple of years, when inflation has been running hotter than normal.

Costco’s fiscal 2023 net sales of $237.7 billion were 59% higher than in pre-pandemic fiscal 2019, a clear indicator of the company’s relevance in a turbulent economy.

The retailer’s customers must be members to shop at one of its 863 locations. This means paying $60 a year for the basic membership or $120 for the Executive plan that comes with added perks, like 2% back on purchases.

Based on the worldwide renewal rate of 90.4% in the latest fiscal quarter, these memberships are extremely popular. Consumers can more than make up the annual fee in savings while shopping, so Costco has created a loyal and sticky customer base.

Investors might assume that due to its massive size, this business doesn’t have lots of growth potential, but that’s an incorrect assumption. The leadership team opened 23 net new warehouses in fiscal 2023, with 10 planned for the current 12-week period.

And even in the U.S., Costco’s most mature market, there is plenty of opportunity to add more stores. This should help boost revenue and earnings in the years ahead.

Investors should also take a closer look at Lululemon Athletica (LULU 1.74%). The business continues to show no signs of slowing down, despite ongoing headwinds.

Revenue in the second quarter (ended July 30) of $2.2 billion was up 18% year over year. And diluted earnings per share jumped 19% to $2.68. These strong double-digit gains have been normal in the past few years, something rival Nike can’t say.

Lululemon’s key asset is its strong brand presence. The business sells quality merchandise for men and women that is at the higher end of the price spectrum, generating outsize profitability. It posted a gross margin of 58.8% last quarter, well ahead of industry peers. And the company’s operating margin has averaged a stellar 20.9% in the last three fiscal years.

Management expects the good times to keep rolling. In April last year, it announced a growth plan called the Power of Three x2 to build off a previous financial outlook that the business hit well ahead of schedule.

By fiscal 2026, sales are expected to total $12.5 billion, which would be double fiscal 2021’s total. Investors can be optimistic about this forecast because this would mark slower growth than in previous years. Lululemon will prioritize growing its men’s, digital, and international revenue.

It’s hard for anyone to argue that Costco and Lululemon aren’t great businesses. Their strong financial performances and meaningful prospects are attractive characteristics that any investor would dream about for their own portfolio.

There is one factor, however, that deserves a closer look. And that’s the valuation. As of this writing, shares of Costco trade at a forward price-to-earnings (P/E) ratio of 36, while Lululemon sells at a forward P/E of 33.4. These are both higher than the S&P 500‘s forward ratio of 19.3.

At first glance, investors who are strictly focused on value might turn away from these two stocks. But I believe their quality makes these companies worth paying up for.

Neil Patel and his clients have no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Costco Wholesale, Lululemon Athletica, and Nike. The Motley Fool recommends the following options: long January 2025 $47.50 calls on Nike. The Motley Fool has a disclosure policy.

Byron Wien, noted investor whose annual “Ten Surprises” list became required reading on Wall Street, has died at age 90.

His death was reported by Blackstone, where he spent the past 14 years, and was most recently vice chairman of its private wealth solutions business.

Wien published his “Ten Surprises” list for 38 consecutive years, which was considered a must-read by many on Wall Street. In his most recent list, he predicted a bottom for financial markets would arrive by mid-2023, followed by a drastic rebound.

Wien said a “surprise” was an event that the average investor would assign only a 1-in-3 chance of happening but that he believed is “probable” with a more than 50% likelihood of taking place.

He started the list tradition in 1986 when he was the chief U.S. investment strategist at Morgan Stanley.

Byron Wien, American investor and vice chairman of Blackstone Advisory Partners

Adam Jeffery | CNBC

In recent years, he wrote the list alongside Joe Zidle, chief investment strategist for Blackstone’s private wealth solutions group.

“Byron’s life was remarkable in so many ways,” Steve Schwarzman and Jon Gray wrote in an internal note sent to Blackstone. “Orphaned at a young age, he began working at 15, graduated from Harvard and led a successful career on Wall Street that spanned many decades.”

New York Magazine named him as one of the most influential people on Wall Street in 2006. “Though fortune-telling is de rigueur on Wall Street, Wien’s predictions are anticipated with the sweaty angst reserved for interest-rate hikes,” the magazine wrote at the time.

— CNBC’s Yun Li and Claudia Johnson contributed to this article.

In contrast to some housing market doomsayers, Steve Eisman, who foresaw the 2007–2008 US housing crisis and whose exploits in profiting from the bubble’s collapse were documented in the Big Short, believes there is no impending housing crisis on the horizon.

Instead, Eisman is basing his current investing strategy on a thesis he calls “revenge of the old school,” and is venturing into bonds for the first time in his career and acquiring stocks from traditional, established industries, all in anticipation of benefiting from the U.S. government’s increased spending initiatives.

“This is the first industrial policy in the U.S. we’ve seen in several decades,” Eisman, who is now a managing director at Neuberger Berman, recently said. “The money isn’t spent yet—it’s the government, it doesn’t take a week. There has been no revenue impact at this point, and I don’t think most of the spending has been embedded in any stocks.”

So, which stocks is Eisman eyeing? He’s pointing towards construction firms, utilities, industrials, and materials, favoring them over flashy, rule-breaking tech companies.

With this in mind, we used the TipRanks database to seek out the details on two stocks boasting such attributes, ones that the Street’s experts believe make good additions to the portfolio right now. Both of these stocks enjoy a ‘Strong Buy’ rating from analysts. Let’s dive into the details.

Vulcan Materials Company (VMC)

Vulcan Materials Company, the first ‘old school’ stock we’re looking at, is a leading US producer of construction materials. With its history dating all the way back to 1909, the company has grown to become one of the nation’s largest and most prominent suppliers of essential construction aggregates, such as crushed stone, sand, and gravel. Vulcan Materials plays a pivotal role in supporting infrastructure development, including highways, bridges, and commercial and residential construction projects across the country.

Its expansive network of quarries, distribution yards, and asphalt and ready-mix concrete production facilities allows it to serve a diverse range of markets and customers, a value proposition that enabled the company to deliver a strong financial statement in the most recent readout for Q2.

Revenue climbed by 8.2% year-over-year to $2.11 billion, beating the Street’s call by $60 million. Adjusted EBITDA saw a 32.2% increase from $450.2 million in the same period a year ago to $595.3 million, also coming in ahead of the Street’s $529 million forecast. Moreover, the EBITDA margin improved by 520 bps from 23% in the prior year quarter to 28.2%, and at the bottom line, adj. EPS of $2.29 beat the analysts’ forecast by $0.37.

Moving forward, the company anticipates achieving full-year adjusted EBITDA in the range between $1.9 to $2 billion, representing a $150 million increase from the initial projections shared in February.

Stifel analyst Stanley Elliot sees several reasons to keep a positive slant on this vintage construction name. “We remain optimistic on VMC’s leading aggregate business with healthy fiscal stimulus combining with improving res/non-res markets to provide a backdrop for multiple years of healthy volumes,” said the 5-star analyst. “Additionally, VMC has an opportunity to improve margins in its downstream businesses over time…”

Conveying his confidence, Elliot rates VMC a Buy along with a $260 price target, suggesting shares will climb 29% over the coming year. (To watch Elliot’s track record, click here)

Overall, the 14 recent analyst reviews on VMC break down to 13 Buys vs. 1 Hold, making the analyst consensus rating a Strong Buy. The forecast calls for one-year returns of ~25%, considering the average target stands at $251.17. (See VMC stock forecast)

Construction Partners (ROAD)

For our next pick, we’ll stay in the building industry with the aptly named Construction Partners, a prominent player in the construction and infrastructure sector.

The Dothan, Alabama-based firm has established a strong presence in the industry, particularly in the Southeastern region of the country. With a focus on civil infrastructure, its core competencies lie in the construction and maintenance of roads, highways, bridges, and related projects. While CPI serves both public and private sector clients, its extensive involvement in public infrastructure projects like state highways and municipal roadways has been a significant contributor to its growth.

And growth has certainly been on the menu. Boosted by a series of acquisitions but also contract work and revenues generated by sales of products such as hot mix asphalt and aggregates, revenues climbed from $785.7 million in fiscal 2020 (which ends in September) to $1.30 billion in 2022. At the same time, the backlog increased to $1.41 billion from $608.1 million.

Going by the latest financial update, there will be more growth on tap this year. The company recently released preliminary results for FY 2023 that show revenue is expected to hit the range between $1.547 billion to $1.557 billion, vs. last year’s $1.30 billion. FY 2023 net income is anticipated to come in between $44.8 million to $47 million, compared to 2022’s $21.4 million. Looking to FY 2024, revenue is expected to further rise to the range between $1.750 billion to $1.825 billion with net income hitting the $63 million to $70 million range.

With all this to come, it’s no wonder Raymond James’s Patrick Tyler Brown, a 5-star analyst ranked right at the top end of Wall Street experts, is buoyant regarding CPI’s future.

“We contend that CPI remains a key beneficiary of a generational investment in infrastructure through recently enacted federal programs (IIJA) and significantly improved funding at state DoTs (department of transportation),” Brown said. “As such, we get the sense that not only does the near-term demand outlook for CPI look constructive, but so does the next few years as these funding mechanisms should continue to yield momentum.”

“We remain convinced that CPI can likely growth organically in the high-single-digit range over the next few years given flush state DoTs, IIJA ramp, and as near/re-shoring trends become more meaningful,” the analyst went on to say.

These comments form the basis for Brown’s Strong Buy rating on ROAD, while his $45 price target makes room for additional gains of 18% in the year ahead. (To watch Brown’s track record, click here)

4 other analysts have recently waded in with ROAD reviews and like Brown, all are positive, providing the stock with a Strong Buy consensus rating. Going by the $43.40 average target, a year from now, shares will be changing hands for ~14% premium. (See ROAD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

When interest rates were low, it was difficult for bond investors to earn a decent yield.

Just ask DoubleLine Capital Founder Jeffrey Gundlach.

Speaking at a recent investment conference in New York, Gundlach recalled what the bond market was like in 2016. He said if you wanted to earn a 5% annual yield on a bond portfolio in those days, you had to buy a junk bond index, use leverage to boost returns and pray that issuers wouldn’t default.

Things have changed dramatically since then.

Bond yields have been surging. While high borrowing costs could slow the economy, it also means that investors can potentially earn higher returns on fixed-income investments.

Gundlach said that he’s “much happier” with bonds today than in 2016.

“Now you can buy a T-bill and chill,” he said.

Treasury bills, or T-bills, are short-term debt obligations issued by the U.S. Department of the Treasury. They’re considered among the safest investments because they are backed by the full faith and credit of the U.S. government.

Among the different types of government-issued securities, T-bills have the shortest maturity at one year or less.

The yield on the one-year Treasury bill stood at 5.432% on Oct. 6.

Compared to the hottest tickers in the stock market, T-bills may seem a bit boring. But remember, T-bills are backed by the U.S. government and are considered among the safest investments globally in terms of credit risk.

Because of their short-term nature, T-bills are less sensitive to interest rate fluctuations, making them less susceptible to interest rate risk.

Gundlach knows about bonds. Over the years, his uncanny ability to predict trends and make profitable decisions in the bond market has earned him the moniker Bond King.

If you want to follow the Bond King’s suggestion and “buy a T-bill and chill,” there are several ways to do it.

One of the most direct methods is through TreasuryDirect, an online platform offered by the U.S. Department of the Treasury, where people can purchase T-bills directly from the government.

Alternatively, many brokerage firms allow clients to buy T-bills either in competitive or noncompetitive bidding processes. Certain banks and financial institutions also might offer the option for their customers to invest in T-bills, so check with your local branch to explore available opportunities. Just make sure that you understand the maturity terms and associated fees before making a purchase.

Exchange-traded funds (ETFs) can provide another way for investors to gain exposure to T-bills. By investing in ETFs, you can access the performance of a basket of T-bills without having to buy each one individually. This method also provides the convenience of trading, as ETFs can be bought and sold on stock exchanges just like individual stocks.

Blackstone made a $13 billion bet on the growth in student housing. Here’s how you can carve out your own piece of the student housing market with just $500.

Don’t miss real-time alerts on your stocks – join Benzinga Pro for free! Try the tool that will help you invest smarter, faster, and better.

This article ‘Buy A T-Bill And Chill’: Bond King Jeffrey Gundlach Says He’s Happier As A Bond Investor Now — Here’s How To Get In On The Action originally appeared on Benzinga.com

.

© 2023 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

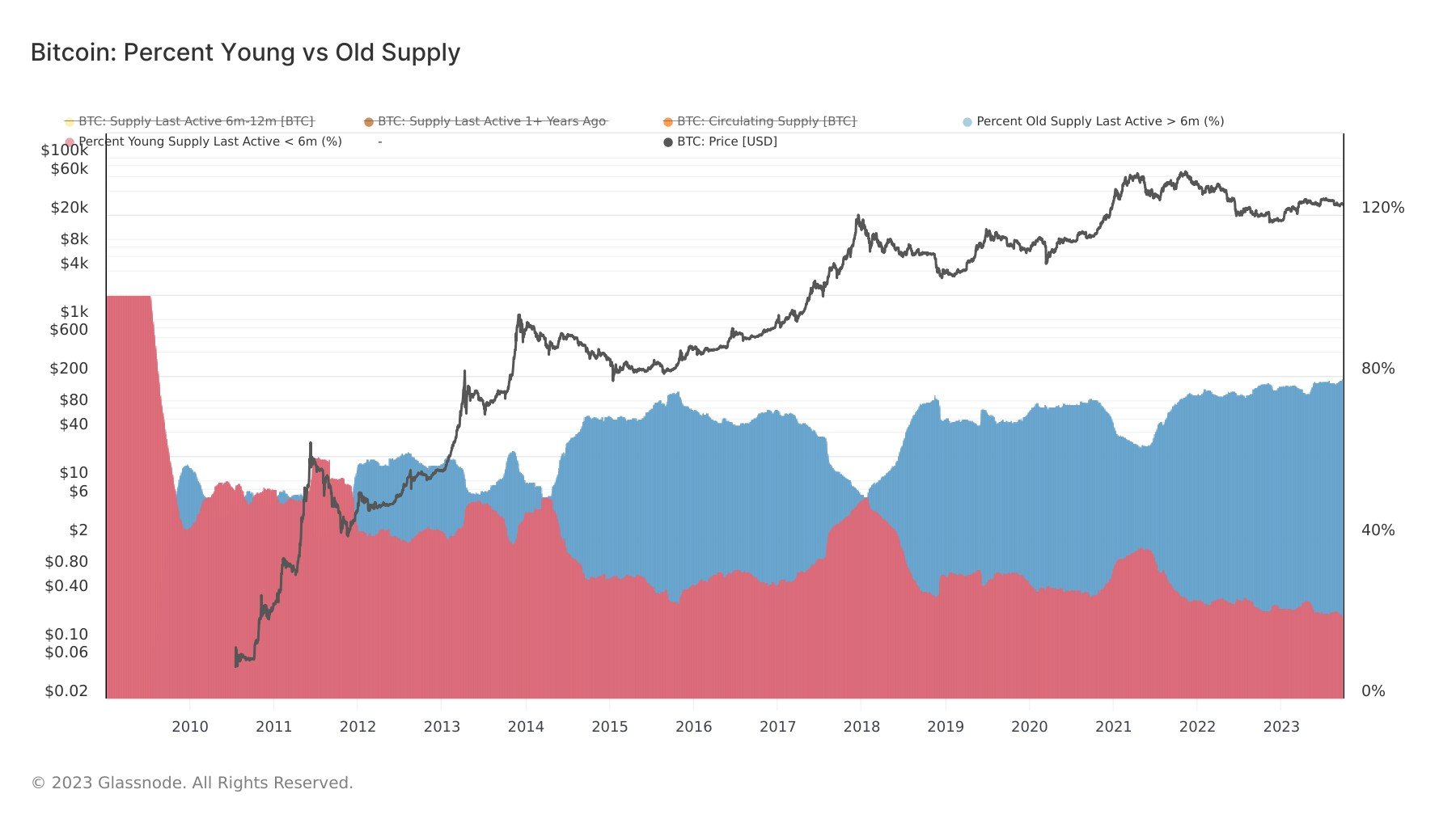

For the first time in its history, Bitcoin has seen an 80/20 split in its circulating supply. The data reveals that approximately 80% of the Bitcoin supply is currently held by investors who have retained their holdings for six months or longer. This indicates a shift in investor behavior towards long-term holding, and potentially, a belief in the cryptocurrency’s future value growth.

On the other hand, the remaining 20% of the supply has been transacted within the last six months, reflecting the actions of more short-term, possibly speculative, traders. This division, visualized through contrasting colors, illustrates the differing strategies within the Bitcoin market and the balance between patience and swift action.

The post First-ever 80/20 investor split in Bitcoin market shines a spotlight on long-term holding appeared first on CryptoSlate.