IBM Corp. on Tuesday notified employees in its marketing and communications division that it’s making cuts, the latest large tech company to trim its payroll.

Source link

IBM Corp. on Tuesday notified employees in its marketing and communications division that it’s making cuts, the latest large tech company to trim its payroll.

Source link

The tech sector is having a big 2024. Nvidia just crushed earnings expectations. The artificial intelligence boom remains in full swing. The tech-heavy Nasdaq index is up more than 8 percent year to date.

The U.S. economy is also doing surprisingly well, adding 353,000 jobs in January, well ahead of economists’ forecasts. Hotter-than-expected inflation data may also keep the Fed from cutting rates as soon as the market expects, a sign that the economy remains strong enough to support tighter monetary policy for longer.

It’s a different story for tech workers, though.

“The layoffs to the start of 2024 signal a dramatic shift in the tech industry,” said Jeff Shulman, professor at the University of Washington’s Foster School of Business. “We’re going to continue to see layoffs happen as the future of work has changed, as the future of technology has changed and as investors’ appetite for risk and growth versus profitability has dramatically changed as well.”

The number of tech sector layoffs in 2024 has been outpacing the number of terminations in 2023. So far, about 42,324 tech employees were let go in 2024, according to Layoffs.fyi, which tracks layoffs in the tech industry. That averages out to more than 780 layoffs each day in 2024. In 2023, nearly 263,000 tech employees got laid off, averaging to about 720 layoffs each day that year.

There are several factors behind the churn. AI is at the forefront. Companies need to free up cash to invest in the chips and servers that power the AI models behind these new technologies. There’s also the stock market effect. Companies that conducted layoffs haven’t been punished, either by investors or on their bottom lines. In fact, they’ve been rewarded with rising stock prices.

Watch the video above to learn why another rough year of layoffs may lie ahead for tech workers, and why the surprising strength of the U.S. economy may not be coming to their rescue.

Layoff fears are taking hold of workers across America, with many worried about whether they’re next.

One expert says layoffs may be less widespread than they appear to be, but workers are still grappling with uncertainty.

Employee confidence has taken a nosedive. The share of workers reporting a positive six-month business outlook for their employer fell to 45.6% in January, according to job-search portal Glassdoor. That’s the lowest level on record since Glassdoor began tracking the sentiment in 2016.

“Everybody’s trying to prove their value at work,” said one North Carolina-based designer in the tech industry whose company has said it plans to reduce headcount. It’s been an “anxiety-inducing” experience, she said, because no one knows which teams will be affected.

“It made things kind of tense, and put people on edge for a while,” said the employee, who spoke anonymously because she is worried about job security.

In the last week alone, PayPal

PYPL,

Block

SQ,

iRobot

IRBT,

as well as the Los Angeles Times and Sports Illustrated, have all laid off workers as they’ve tried to make their businesses leaner. UPS

UPS,

Wayfair

W,

and Microsoft

MSFT,

were all hit by layoffs.

Yet the U.S. economy seems to be humming along just fine. In January, 353,000 new jobs were added, a surprisingly large gain that beat forecasts of an increase of 185,000. Unemployment is near the lowest level since the 1960s.

“Bang! What a way to start the new year as today’s January jobs report,” Ali Jaffery at CIBC Economics wrote in a note. The data shows that the “U.S. labor market [is] much stronger … than we believed.”

Yet given the onslaught of layoff news, especially in tech and media, “job security remains top of mind for employees,” Glassdoor noted. The share of reviews of companies on Glassdoor that mention layoffs was up in January by 27%, as compared with last year.

The tech designer whose company is planning layoffs said the fear has ignited a fire under her to work even harder and to be “as sharp as possible,” she said. She has survived two other rounds of layoffs — one in 2016 and one in 2022.

Another worried employee, who works at a San Diego-based biotech startup, said his company grew rapidly during the pandemic, but is now in the midst of “huge cuts.” His department shrunk from five employees to just him. “I’m the entire department,” he said.

“It’s been really challenging and stressful to be honest,” the worker said. He’s talked to recruiters, and has begun applying for jobs, but senses competition.

Even though recruiters have reached out, he hasn’t applied to as many positions as he would like, sending out only 20 applications over the last month, including some for jobs in other industries.

“I think there’s a lot of people out there aggressively looking for a new role” either because they’re laid off or are worried about being retrenched, he noted.

One career expert told MarketWatch that layoffs were top of mind for many business leaders as they headed into 2024. “Almost every CEO that I know is planning layoffs right now,” Tessa White, a career-navigation adviser and founder of the Job Doctor, said. “I think things are going to slow down much more than we expect.”

Yet much of workers’ anxiety seems disconnected from official measures of unemployment and job cuts, Daniel Zhao, lead economist at Glassdoor, told MarketWatch. Some of workers’ unease may be related to the fact that people are comparing the current moment with the hot job market of 2021 and 2022, when employees were job-hopping and getting big raises.

It’s a confusing time for employees. Troubling layoff news is mixed in with rosier reports about the overall economy, which seems to have avoided a recession so far as inflation finally cools off.

Although thousands of workers are losing their jobs in tech, media and other industries, there is little evidence so far that layoffs are spreading across the economy, Zhao said.

Reports of companies laying off thousands of workers, such as Wayfair losing 1,650 employees or Google shedding over 12,000 jobs — and counting — are cases that aren’t necessarily representative of the entire economy.

About 1.6 million people were laid off in December 2023, according to data from the U.S. Bureau of Labor Statistics, which is still below the pre-pandemic normal of 1.8 million, Zhao said.

“So a company that lays off 1,000, that sounds like a huge number, but it’s not even 1% of the monthly amount of people who are laid off,” he added.

When mom-and-pop restaurants that can’t operate shut down and lay off their staff, and local businesses go bust, that’s more of a reflection of widespread layoffs.

Employees searching for signs of layoffs at their company may find the biggest indicator to be the pace of hiring.

Outside of the pandemic, hiring has hit its slowest pace since 2014, Zhao noted, based on BLS data, which is worrying people. If workers are looking for jobs, they may find fewer opportunities. They may also find that some companies are putting hiring freezes in place.

“A company that is worried about the future will stop hiring pretty quickly because that’s an instantaneous action that a company can take to stop their costs from increasing,” Zhao said. “It’s a very slow process to actually undergo those layoffs or to cut annual budgets, but taking down a job posting or not extending an offer, that’s something that you can do today.”

Hiring freezes or seeing job openings come down will be the “best early indicators” about a company’s sentiment towards the future, he said, “which is itself an indicator of potential layoffs.”

The North Carolina tech worker who feared losing her job also noted that at her old companies, one key sign of impending layoffs was a reorganization.

“You can kind of read the signs that something is coming when they start moving people around, especially when it doesn’t make sense,” she explained. “That’s the biggest red flag.”

The biggest declines in employee confidence were among those in the utilities industry, transportation and warehousing, and the information industry, which spans technology and media.

Employees in the information sector have tended to be the most worried about layoffs, Zhao said. That’s because the sector spent much of last year dominating the headlines with tech-company layoffs.

Among employees, mid-level workers were the most spooked, with their confidence falling the most in January, Glassdoor said. Entry-level employees were second place in terms of shaken confidence.

“This is not just frontline employees who are concerned,” Zhao said. “Even for those folks who have more information about the business, their confidence is declining too.”

While some data suggest that remote employees were more likely to be laid off in 2023, Zhao said that the link between not being in the office and being at a higher risk of being let go was not fully clear.

“We know that many employers are pushing return-to-office plans and if those companies are doing layoffs at the same time, they might choose to target people who are either not complying with return-to-office mandates, or are unlikely to, because they live too far away from the office to come in,” he explained.

Not being in the office could also mean missing out on gossip or casual conversations about the state of the business and whether there was tension or stress, he added.

For those who are worried about losing their job, there are a couple of steps to consider taking. First, check if you will get a severance package if you’re laid off, which could help you juggle finances while you are on the hunt for a new job.

Find spots to trim. Cut off any memberships or subscriptions that aren’t necessities, which could help save some money.

Start networking with people from your past, as well as find new connections. It’s less nerve-wracking to put yourself out there when you’re still employed, and for some, it can be exhausting to juggle. Still, it could pay off: One expert advised that searching for a job while holding on to one “gives you leverage when it comes to negotiating terms for the new gig.”

Finally, step back and reset, Zhao said. Get into the right state of mind and address your emotional and mental health before starting your job search. See if you can find opportunities in other less recession-sensitive industries, like healthcare.

The San Diego biotech worker, who has been laid off three times over nearly two decades in the industry due to companies winding down, knows the drill.

“So it’s not my first rodeo, as they say. It’s still nerve-wracking when you’re the primary person in the family as far as wage-earning goes,” he said.

If he were to be laid off, he would expect a severance package.

Meanwhile, the North Carolina tech worker who is anticipating layoffs said if she gets laid off again, she may just quit the industry.

“I might transition to finance-based roles, because it feels a bit more secure, or something related to healthcare,” she said.

But for now, she isn’t about to jump into job search mode just yet. “At this point, I’d rather be laid off than to quit and start searching for a job and have interviews. At least if I get laid off, I know I’m going to get a severance package.”

Developing story. Check back for updates.

The numbers: The number of Americans who applied for unemployment benefits at the end of January rose to a nearly three-month high of 224,000, possibly a sign of some softening in what’s been an incredibly strong labor market.

Initial jobless claims increased by 9,000 in the seven days ended Jan. 27 from 215,000 in the prior week, based on seasonally adjusted figures.

New jobless claims are starting to become more normal again after the usual fluctuations during the holiday season stretching Thanksgiving until Martin Luther King Jr. Day.

While they still show a surprisingly resilient labor market characterized by low layoffs and low unemployment, new claims appear to have wafted higher in the new year.

Key details: New jobless claims rose in 29 of the 53 states and territories that report these figures to the federal government. The biggest increases were in California, Oregon and New York.

New claims fell slightly in 24 other states.

The number of people collecting unemployment benefits in the U.S., meanwhile, rose by 70,000 to 1.9 million. That’s the highest level since mid-November.

A gradual rise in these so-called continuing claims over the past year is a sign it’s taking longer for people to find new jobs.

Looking at actual or unadjusted figures, initial jobless claims might be even weaker than it appears. They totaled 261,029 last week, compared to 225,026 in the same week a year earlier.

Unadjusted claims bear close watching in the next few weeks to see if they subside again. A spate of companies have announced layoffs in the new year and it remains to be seen how widespread they become.

Big picture: Business are hiring at a slower pace compared to last year, but they have been reluctant to lay off workers because of a tight labor and steadily growing economy.

The labor market could get a boost later in the year if the Federal Reserve cuts interest rates as widely expected.

What is unclear is whether wages would start to rise faster under that scenario and complicate the Fed’s job to fully tame inflation.

Market reaction: The Dow Jones Industrial Average

DJIA

and S&P 500

SPX

were set to rise in Thursday trading.

Skynesher | E+ | Getty Images

Microsoft joined a list of big tech companies that announced major layoffs at the start of 2024.

The technology company plans to cut about 9% its Gaming Unit headcount, amounting to 1,900 laid off workers, according to a memo obtained by CNBC.

Earlier this week, EBay said it plans to let go 1,000 employees, or 9% of the company’s staff. These announcements join a flurry of layoffs from tech behemoths like Amazon and Google.

Amazon let go of 30 employees in its Buy with Prime unit while Google has more job cuts slated for the year after paring its headcount of central engineer and hardware workers.

More from Personal Finance:

What to do if you can’t find an accountant for tax season

Americans can’t pay an unexpected $1,000 expense

Employers and workers are at odds over work-life balance

Meanwhile, SAP, the German software company, plans to offer job changes or voluntary buyouts for 8,000 employees as part of its restructuring program for 2024.

With all these recent layoffs, if you find your company aims to carry out voluntary buyouts, there are a few things to consider before you accept.

“Buyout regret is real,” said Suzy Welch, a career expert and CNBC contributor. “People take them in the moment. They think, ‘The money’s good, and ‘Non-voluntary layoffs are going to be next.'”

If you ever receive a buyout deal, first assess the value of the financial package.

“How many months of severance pay will you get? Will you have health coverage and for how long? How will your retirement benefits be affected?” said Julia Pollak, chief economist at ZipRecruiter.

Afterwards, see if there’s room for negotiation, experts say. For example, explore options to work fewer hours or find ways to boost your buyout deal, they advise.

Always make sure you get a written letter of recommendation and not the promise of one before signing the dotted line.

“Management is not expecting 100% acceptance.” Welch said. “Maybe a deal can be struck for different [or] less work so you can keep doing what you love.”

Ask if you can stay in your job under different leadership or on a different team, Pollak added.

If not, seek an additional month or two of severance pay based on your performance and tenure, or an extra six months of health insurance coverage, she said.

“These kinds of improvements can be worth a great deal of money and have a large effect on your financial situation during your job search,” Pollak said. “Try to negotiate a departure on the best possible terms, with the longest possible benefits coverage and severance pay, or largest possible lump sum payout.”

The worst possible outcome is if the only alternative to the buyout is being involuntarily terminated without the benefits, Pollak explained.

“Always make sure you get a written letter of recommendation and not the promise of one before signing the dotted line,” Welch said.

BlackRock, the world’s largest money management firm, plans to announce layoffs in the coming days of about 3 percent of its global workforce, Fox Business has learned.

The job cuts of around 600 employees, which have yet to be reported, are being described internally as routine, according to a source familiar. Last year, BlackRock did a similar round of layoffs gauged on employee performance metrics, the source added.

Shares of BlackRock rebounded in 2023, up 6 percent after falling 21 percent in 2022. New customer money into BlackRock’s solid Exchange Traded Fund business exploded last year with $187 billion of inflows into the products that follow a basket of securities and trade like stocks on major exchanges.

On Wednesday, BlackRock is expecting approval from the Securities and Exchange Commission for its new Bitcoin “spot” ETF — the first time a crypto investment product tracking the daily price of the world’s most popular digital coin will be approved by securities regulators to trade on a public stock market. Other asset managers are also expecting approval for their ETFs.

BLACKROCK, STATE STREET FACE SUBPOENAS IN HOUSE ESG PROBE

A BlackRock spokesman would not comment on the layoffs. BlackRock is scheduled to announce fourth quarter earnings on Friday.

One possible impetus for the layoffs is that BlackRock, after years of wild growth in assets under management or AUM, is settling into a more mature phase in its business. Analyst consensus for earnings in its fourth quarter projects a 2.46 percent decline year-over-year to $8.71 a share.

BlackRock finished the third quarter of 2023 with $9 trillion in AUM though the firm has seen significant asset declines since it reached a peak of more than $10 trillion in 2022 amid wobbly financial markets. The decline in assets also came as BlackRock became a political lightning rod over its embrace of Environmental Social Governance investing, or ESG, which directs investment dollars into public companies in the sustainable energy space, or those that are taking steps to reduce their carbon footprint and advocate corporate governance measures such as boardroom diversity.

DECEMBER JOBS BREAKDOWN: WHICH INDUSTRIES HIRED THE MOST WORKERS LAST MONTH?

The firm has been de-emphasizing its ESG business in the U.S. amid the controversy, Fox Business has learned. U.S. portfolio managers are no longer required to consider ESG metrics when not using ESG funds. In 2023, many so-called green investment funds have seen declines in asset amid weak performance as investments in sustainable energy products fail to produce significant returns.

Company founder and CEO Larry Fink told Fox Business he won’t use the mention of the letters E-S-G any longer because of the controversy it has stirred up in political circles.

US ECONOMY ADDS 216K JOBS IN DECEMBER, BEATING EXPECTATIONS

As top Republicans, including several running for the GOP presidential nomination, have attacked BlackRock and ESG, those running pension funds in red states have yanked about $6 billion from BlackRock funds as a form of protest.

Noticeably quiet from the BlackRock bashing is the GOP front-runner, former President Donald Trump. One reason may be because BlackRock once managed Trump’s fortune, estimated in the billions of dollars. In 2017, Trump said of Fink: “Larry did a great job for me. He managed a lot of my money. I have to tell you, he got me great returns.”

People close to BlackRock tell Fox Business that savings from the job cuts will be used to expand into growth businesses such as technology investing and investing in so-called alternative products as opposed to stocks and bonds.

ESG, meanwhile, remains a big business with BlackRock’s foreign customers, including large sovereign wealth funds in Europe and the Middle East. Mark Wiedman, head of BlackRock’s client business, speaking at a recent event sponsored by the news outlet Semafor, called ESG “a demand from clients,” with around $1 trillion in pure sustainable assets being managed by BlackRock.

Original article source: BlackRock layoffs coming as firm matures, ESG pullback and Bitcoin ETF approval

Jane Fraser, CEO of Citigroup Inc., during an interview for an episode of “The David Rubenstein Show: Peer-to-Peer Conversations” at the Economic Club of Washington in Washington, D.C., March 22, 2023.

Valerie Plesch | Bloomberg | Getty Images

Citigroup will soon begin layoffs in CEO Jane Fraser’s corporate overhaul, CNBC has learned.

Employees affected by the cuts will be informed starting Wednesday, with new dismissals announced daily through early next week, according to people with knowledge of the situation.

Those impacted will include chiefs of staff, managing directors and some lower-level employees, said the people. The cuts will spread to more rank-and-file staff by February, they added.

The move tracks with a timeline set by Fraser in a Sept. 13 memo. She announced five new divisions whose heads report directly to her, resulting in the departure of a handful of senior executives. The next phase of disruption will be “communicated and implemented by the end of November,” and “final changes” will be done by the end of March 2024, Fraser said at the time.

Fraser is under pressure to improve Citigroup, which has been mired in a stock slump as headcount and expenses have ballooned in recent years. The CEO, who took over in March 2021, is at a pivotal moment as she faces deep investor skepticism that the bank can hit performance targets she outlined last year.

Employees who have lost their roles may be able to apply for other positions, and Citigroup will offer severance pay where eligible, the company’s human resources chief told workers last month.

The full extent of job cuts is still being determined, but managers and consultants working on the project — known internally by its code name, “Project Bora Bora” — have discussed dismissals of at least 10% of workers in several businesses, CNBC reported last week.

New Citigroup organizational charts have been created, and managers are now deciding which employees they will retain and who will be left out, said one of the people.

Workers have flocked to internal chat platforms with questions about the impending cuts, according to the people, who declined to be identified speaking about personnel matters.

A Citigroup spokeswoman declined to comment Wednesday beyond the statement it offered to CNBC previously:

“We’ve acknowledged the actions we’re taking to reorganize the firm involve some difficult, consequential decisions, but they’re the right steps to align our structure to our strategy and deliver the plan we shared at our 2022 Investor Day.”

Don’t miss these stories from CNBC PRO:

The largest American banks have been quietly laying off workers all year — and some of the deepest cuts are yet to come.

Even as the economy has surprised forecasters with its resilience, lenders have cut headcount or announced plans to do so, with the key exception being JPMorgan Chase, the biggest and most profitable U.S. bank.

Pressured by the impact of higher interest rates on the mortgage business, Wall Street deal-making and funding costs, the next five largest U.S. banks have cut a combined 20,000 positions so far this year, according to company filings.

The moves come after a two-year hiring boom during the Covid pandemic, fueled by a surge in Wall Street activity. That subsided after the Federal Reserve began raising interest rates last year to cool an overheated economy, and banks found themselves suddenly overstaffed for an environment in which fewer consumers sought out mortgages and fewer corporations issued debt or bought competitors.

“Banks are cutting costs where they can because things are really uncertain next year,” Chris Marinac, research director at Janney Montgomery Scott, said in a phone interview.

Job losses in the financial industry could pressure the broader U.S. labor market in 2024. Faced with rising defaults on corporate and consumer loans, lenders are poised to make deeper cuts next year, said Marinac.

“They need to find levers to keep earnings from falling further and to free up money for provisions as more loans go bad,” he said. “By the time we roll into January, you’ll hear a lot of companies talking about this.”

Banks disclose total headcount numbers every quarter. While the aggregate figures mask the hiring and firing going on beneath the surface, they are informative.

The deepest reductions have been at Wells Fargo and Goldman Sachs, institutions that are wrestling with revenue declines in key businesses. They each have cut roughly 5% of their workforce so far this year.

At Wells Fargo, job cuts came after the bank announced a strategic shift away from the mortgage business in January. And even though the bank cut 50,000 employees in the past three years as part of CEO Charlie Scharf’s cost-cutting plan, the firm isn’t done shrinking headcount, executives said Friday.

There are “very few parts of the company” that will be spared from cuts, said CFO Mike Santomassimo.

“We still have additional opportunities to reduce headcount,” he told analysts. “Attrition has remained low, which will likely result in additional severance expense for actions in 2024.”

Meanwhile, after several rounds of cuts in the past year, Goldman executives said that they had “right-sized” the bank and don’t expect another mass layoff like the one enacted in January.

But headcount is still headed down at the New York-based bank. Last year, Goldman brought back annual performance reviews where people deemed low performers are cut. In the coming weeks, the bank will terminate around 1% or 2% of its employees, according to a person with knowledge of the plans.

Headcount will also drift lower because of Goldman’s pivot away from consumer finance; the firm agreed to sell two businesses in deals that will close in coming months, a wealth management unit and fintech lender GreenSky.

Pedestrians walk along Wall Street near the New York Stock Exchange in New York.

Michael Nagle | Bloomberg | Getty Images

A key factor driving the cuts is that job-hopping in finance slowed drastically from earlier years, leaving banks with more people than they expected.

“Attrition has been remarkably low, and that’s something that we’ve just got to work through,” Morgan Stanley CEO James Gorman said Wednesday. The bank has cut about 2% of its workforce this year amid a protracted slowdown in investment banking activity.

The aggregate figures obscure the hiring that banks are still doing. While headcount at Bank of America dipped 1.9% this year, the firm has hired 12,000 people so far, indicating that an even greater amount of people left their jobs.

While Citigroup‘s staff figures have been stable at 240,000 this year, there are significant changes afoot, CFO Mark Mason told analysts last week. The bank has already identified 7,000 job cuts linked to $600 million in “repositioning charges” disclosed so far this year.

CEO Jane Fraser’s latest plan to overhaul the bank’s corporate structure, as well as sales of overseas retail operations, will further lower headcount in coming quarters, executives said.

“As we continue to progress in those divestitures … we’ll see those heads come down,” Mason said.

Meanwhile, JPMorgan has been the industry’s outlier. The bank grew headcount by 5.1% this year as it expanded its branch network, invested aggressively in technology and acquired the failed regional lender First Republic, which added about 5,000 positions.

Even after its hiring spree, JPMorgan has more than 10,000 open positions, the company said.

But the bank appears to be the exception to the rule. Led by CEO Jamie Dimon since 2006, JPMorgan has best navigated the surging interest rate environment of the past year, managing to attract deposits and grow revenue while smaller rivals struggled. It’s the only one of the Big Six lenders whose shares have meaningfully climbed this year.

“All these companies expanded year after year,” said Marinac. “You can easily see several more quarters where they go backwards, because there’s room to cut, and they have to find a way to survive.”

Don’t miss these CNBC PRO stories:

– CNBC’s Gabriel Cortes contributed to this article.

Over the last 2 years, there have been a few cuts within the company as part of its goal to “deliver durable savings through improved velocity and efficiency”.

Tech giant Google LLC (NASDAQ: GOOGL) has cut at least 40 jobs in its Google News division. According to those familiar with the matter, the reason behind the layoff round is the uncertainty and sensitive time for online platforms and publishers. The exact number of those who lost their job at the Google News unit is not confirmed. As the spokesperson stated, there are still hundreds of employees working on the product.

Google representative commented:

“We’re deeply committed to a vibrant information ecosystem, and news is a part of that long-term investment. We’ve made some internal changes to streamline our organization. A small number of employees were impacted. We’re supporting everyone with a transition period, outplacement services and severance as they look for new opportunities at Google and beyond.”

Over the last 2 years, there have been a few cuts within the company as part of its goal to “deliver durable savings through improved velocity and efficiency”. In November 2022, Google’s parent Alphabet Inc (NASDAQ: GOOGL) announced it would let go of 10,000 employees. In January, Alphabet announced a layoff of as many as 12,000 workers, or roughly 6% of its headcount. In September, Google reduced its recruiting team by hundreds of positions.

Last year, DeepMind, Alphabet’s division responsible for developing general-purpose artificial intelligence (AI) technology, also reduced employee expenses by 39% within its cost-cutting strategy.

Other tech giants like Amazon.com Inc (NASDAQ: AMZN), Microsoft Corporation (NASDAQ: MSFT), Meta Platforms Inc (NASDAQ: META), and Alphabet Inc (NASDAQ: GOOGL) also conducted layoffs, driving the downsizing trend into 2023.

The world is now shaken by two ongoing wars. The Russian invasion of Ukraine has been in place since February 2022, and since October 7, there has been a war between Israel and Hamas that has already claimed thousands of lives. At this uncertain time, the spread of fake news and misinformation is an especially sensitive issue, therefore, it is important for platforms that users trust to provide up-to-date and reliable news.

On Tuesday, Senator Michael Bennet asked several tech giants to provide information about their efforts to respond to the spread of misinformation about the conflict between Israel and the Palestinian militant group Hamas. In a letter sent to Google, Meta Platforms Inc, X (formerly Twitter), and TikTok, Bennet stated that their algorithms of work ‘have amplified this content, contributing to a dangerous cycle of outrage, engagement, and redistribution’.

Google spokesperson said:

“These internal changes have no impact on our misinformation and information quality work in News.”

The spread of fake news is further fueled and escalated by the existing AI chatbots. For example, when asked about the ongoing Israel-Hamas conflict, Google’s Bard mentioned that “both sides are committed” to maintaining peace. Similarly, Microsoft’s AI-powered Bing chatbot stated that “the ceasefire indicates the cessation of immediate bloodshed”. Following that, Google released a statement, asking users to understand that mistakes can happen and how they are doing everything to avoid them.

next

Darya is a crypto enthusiast who strongly believes in the future of blockchain. Being a hospitality professional, she is interested in finding the ways blockchain can change different industries and bring our life to a different level.

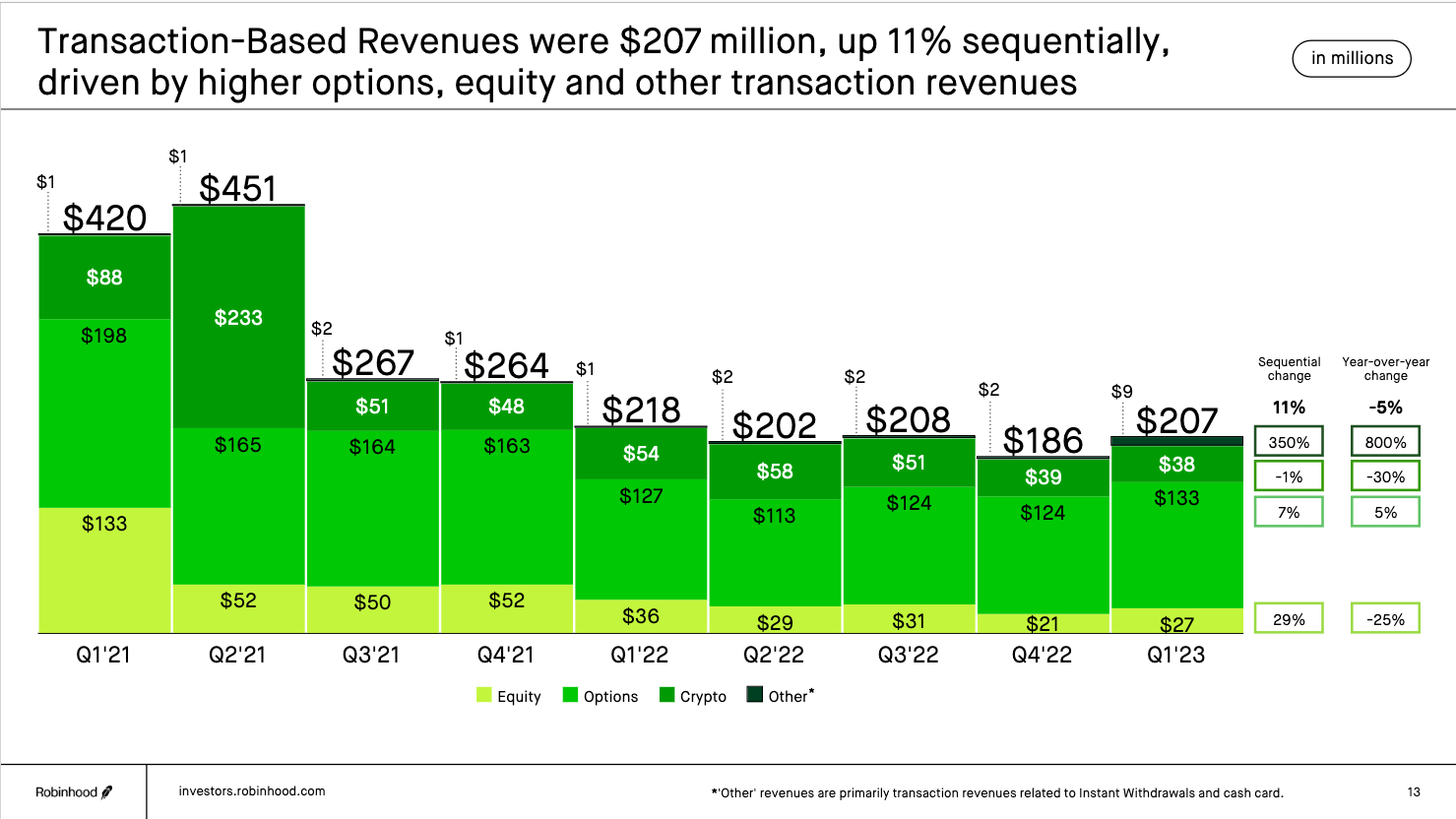

Online brokerage firm Robinhood Markets will reportedly lay off roughly 150 full-time staff — 7% of its total workforce — in its third round of layoffs in just over a year.

According to an internal company message seen by The Wall Street Journal, Robinhood Chief Financial Officer Jason Warnick reportedly wrote that the cuts were being made to “adjust to volumes and to better align team structures.”

A Robinhood spokesperson did not confirm or deny the layoffs in comments to Cointelegraph, but stated:

“We’re ensuring operational excellence in how we work together on an ongoing basis. In some cases, this may mean teams make changes based on volume, workload, org design, and more.”

The reported layoffs come just five days after Robinhood acquired credit card firm X1 in a $95 million deal. Last year, Robinhood cut its total headcount by 9% in April and let go of 23% of its remaining staff in August as a decline in trading activity and subdued prices of equities and cryptocurrencies saw profit margins shrink.

The two cuts accounted for the loss of more than 1,000 staff.

Related: Robinhood will end support for 3 tokens named in SEC lawsuits

At its peak, in the second quarter of 2021, Robinhood boasted 21.3 million active users and more than $565 million in revenue. Things have soured for the brokerage firm of late, with Robinhood’s Q1 2023 results showing a 44% decline in monthly active users and a 30% year-over-year decline in revenue.

Robinhood shares are currently changing hands for $9.63, up 18% for the year despite having fallen more than 82% from its all-time-high, notched in August 2021.

Magazine: Bitcoin 2023 in Miami comes to grips with ‘shitcoins on Bitcoin’