“My brother is named executor, and he also has the sign-in passwords to all our father’s investment accounts.”

Source link

“My brother is named executor, and he also has the sign-in passwords to all our father’s investment accounts.”

Source link

In a recent analysis, economist Peter Schiff draws stark comparisons between the current U.S. economic optimism and the prelude to the 2008 financial crisis. Schiff, leveraging his expertise, warns of impending financial turmoil, emphasizing the critical role of money supply in understanding economic health. Peter Schiff Warns: U.S. Economy on the Brink, Echoes of 2008 […]

In a recent analysis, economist Peter Schiff draws stark comparisons between the current U.S. economic optimism and the prelude to the 2008 financial crisis. Schiff, leveraging his expertise, warns of impending financial turmoil, emphasizing the critical role of money supply in understanding economic health. Peter Schiff Warns: U.S. Economy on the Brink, Echoes of 2008 […]

Source link

If you’re taking a required minimum distribution from an IRA, 401(k) or other tax-deferred account and don’t need the money to cover living expenses, where should you stash that unneeded cash?

Investors now need to start taking RMDs at age 73 or, if they were born after 1960, at age 75. Depending on the balances of your accounts, that distribution can be a sizable amount of money, perhaps more than you need to live on. One option is to reinvest that money, and a Roth IRA would seem to be a perfect choice: withdrawals from Roth accounts are tax-free – including all gains on your investments – and you’ll never need to take any of those pesky RMDs during your lifetime.

There’s just one catch: You can’t directly convert your RMDs to a Roth. But for some people, there is a potential workaround. For 2024, you can contribute up to $7,000 plus another $1,000 if you’re at least 50 years old – if you have enough earned income.

Get matched with a financial advisor to discuss your own retirement strategy.

The IRS defines earned income as money you get for working, such as wages, commissions, bonuses, tips and honorariums for speaking, writing or taking part in a conference or convention. Income generated by self-employment also counts. Income that doesn’t qualify includes taxable pension payments, interest income, dividends, rental income, alimony and withdrawals from Roth IRAs or other nontaxable retirement accounts, along with annuities, welfare benefits, unemployment compensation, worker’s compensation payments and your Social Security income.

Another restriction on Roth contributions is the income limit. Once your modified adjusted gross income (MAGI) hits $146,000 for a single filer or $230,000 for joint filers, your maximum Roth contribution starts phasing out up to $161,000 (single filers) or $240,000 (joint filers). After that, you’re no longer eligible to contribute.

You also need to remember that you need to wait five tax years after your first contribution to any Roth account before you can make withdrawals. Heirs who inherit your Roth will need to withdraw the entire balance within 10 years.

Consider speaking with a financial advisor to develop a tax-efficient retirement strategy.

If you don’t qualify to make a Roth contribution, you still have options to eliminate, reduce or delay your RMDs.

Roth conversion: You can convert your IRA to a Roth account, once you’ve taken your RMD for the year. You’ll pay taxes on the amount you convert, so one tactic is to convert the maximum amount available without pushing yourself into a higher tax bracket. Each Roth conversion carries its own five-year rule.

Charitable contribution: You can use a Qualified Charitable Distribution to donate some or all of your RMD to a charity recognized by the IRS and you won’t be taxed on the donated amount. To qualify, the money must be transferred directly from your IRA to the charity.

Keep working: Your 401(k) account with your current employer isn’t subject to RMDs if you’re still on the payroll. One tactic is to roll 401(k)s from previous employers into your current plan so that they won’t be subject to RMDs. Once you stop working, however, RMDs are required.

Be careful: The punishment for failing to take an RMD during the required time period is a hefty one – up to 50% of the missed RMD amount.

A financial advisor can help you navigate the particular risks and tradeoffs in your situation.

Structuring your retirement withdrawals to reduce your tax bite means looking at all your sources of income, including retirement accounts, RMDs, Social Security benefits, pensions and taxable investment income. For some people, withdrawing money from an IRA early in retirement can reduce the size of their eventual RMDs. If they also delay collecting their Social Security benefits, their benefit amount to increase by 8% each year until they reach 70 years old. Also, be sure to coordinate taxes, withdrawals and RMDs between spouses, and remember that a younger spouse’s RMDs won’t need to be taken until they reach age 73 or 75.

Other common retirement tax moves include investing in tax-free bonds, moving to a state with no income tax or estate tax, harvesting tax losses in taxable investment accounts and holding any taxable assets long enough to qualify for lower long-term capital gains tax rates.

To learn more about retirement planning and how to work toward your goals, talk to a financial advisor for free.

How to manage your RMDs – and all the other many tax questions that can arise in retirement – can be complicated. Take the time to estimate your retirement taxes before you start collecting pensions, Social Security and taking withdrawals from retirement accounts.

Balancing taxes and retirement income – and figuring out how to minimize taxes in retirement – is a crucial issue. A knowledgeable financial advisor can help you decide how to structure and coordinate these payments over the span of your retirement.

Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three vetted financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you.

Make sure you’re protecting your cash reserves from inflation by securing them in an account that generates a competitive interest rate. Leaving cash in a checking account or low-yield savings account can stifle your purchasing power over time.

Photo credit: ©iStock.com/skynesher

The post Can I Use My RMDs to Transfer Money Into My Roth IRA? appeared first on SmartReads by SmartAsset.

“She flipped the title on his car, sold all his furniture and told us that our dad didn’t leave me or my sister anything.”

Source link

Politically diverse fund-management teams perform better.

Source link

Over the long run, Wall Street is a bona fide wealth-creating machine. Although gold, oil, housing, and Treasury bonds have increased in value over multiple decades, no asset class has come close to replicating the average annual returns delivered by stocks over the past century.

For example, including dividends paid, the benchmark S&P 500 has delivered just a hair north of a 10% annualized return since its official inception as a 500-company index in 1957. That’s a hearty return that can double investors’ money about every seven years.

But on an aggregate growth basis, the S&P 500 doesn’t hold a candle to what semiconductor stock Nvidia (NASDAQ: NVDA) has done for investors since becoming a publicly traded company in 1999.

Not too long before the dot-com bubble burst in 2000, Nvidia made its grand entrance as a publicly traded company. Its initial public offering (IPO) occurred on Jan. 22, 1999, with shares being sold at $12. Of course, a lot has changed since then.

If investors had the wherewithal to purchase $1,000 worth of Nvidia stock for its IPO, they would have received 83 shares, not including commission costs and fractional shares. In the quarter of a century since going public, this Wall Street darling has split its stock on five separate occasions. The figure in parenthesis behind each split denotes what the original 83-share position would have grown into:

June 27, 2000: 2-for-1 stock split (166 shares)

Sept. 12, 2001: 2-for-1 stock split (332 shares)

April 7, 2006: 2-for-1 stock split (664 shares)

Sept. 11, 2007: 3-for-2 stock split (996 shares)

July 20, 2021: 4-for-1 stock split (3,984 shares)

IPO-day investors have seen their share count in Nvidia grow by a factor of 48. At the same time, the IPO offering price has been reduced to a split-adjusted $0.25 per share.

Based on Nvidia’s closing price of $878.36 on March 15, 2024, a 3,984-share position would equate to $3,499,386. For those of you keeping score at home, Nvidia has produced a 351,244% gain since its IPO, which compares to just a 318% return for the benchmark S&P 500 over the same period. Keep in mind that I’m not including the additional returns from Nvidia’s nominal dividend in this 351,244% figure, either.

Throughout its 25 years as a public company, Nvidia has had moments where it’s thrived. For quite some time, the company’s graphics processing units (GPUs) used for gaming on personal computers were its calling-card to success. The company also gained momentum from 2016 through 2018 as cryptocurrency prices soared. Cryptocurrency miners gobbled up the company’s high-powered GPUs.

But there’s little question that Nvidia’s role as the infrastructure backbone of the artificial intelligence (AI) movement has done most of the heavy lifting.

Though estimates vary wildly, the analysts at PwC believe AI can add $15.7 trillion to global gross domestic product by 2030. Utilizing software and systems to handle tasks that would normally be assigned to humans, and seeing these systems evolve over time and become smarter, is what gives AI application across virtually every sector and industry.

Nvidia’s A100 and H100 GPUs are nothing short of the standard in AI-accelerated data centers. With demand easily outweighing the supply of these high-powered chips, Nvidia has enjoyed otherworldly pricing power, which more than double its sales in fiscal 2024 (ended in late January).

Additionally, Nvidia’s ramp of A100 and H100 chips looks to be in its early innings. Its four largest customers — and fellow “Magnificent Seven” members — Microsoft, Meta Platforms, Amazon, and Alphabet, have been aggressively gobbling up supply for their own AI-fueled ambitions.

However, sustaining this success in the years to come could prove challenging.

For the past year, Nvidia has blown the doors off of Wall Street’s revenue and profit forecasts. But don’t expect this to continue for much longer.

One problem Nvidia may be contending with in the second-half of 2024, if not well beyond, is margin contraction. The scarcity of the company’s AI-GPUs is what’s lifted prices for these chips into the stratosphere. With supply chain issues beginning to ease and external competitors entering the arena, AI-focused GPUs will be far less scarce in the second-half of 2024 than they are now. That’s a recipe for weaker pricing power and lower margins for Nvidia.

What’s arguably an even bigger concern for Nvidia than the external competitors that’ll be challenging its AI-accelerated data center dominance is that its aforementioned top four customers, which account for 40% of its sales, are developing AI-GPUs of their own. Regardless of whether these internally developed GPUs are to complement Nvidia’s chips or replace them, we’re very likely witnessing a peak of orders that will taper into subsequent years.

Nvidia is also getting no help from U.S. regulators. Following an initial round of export restrictions to China for its top-notch A100 and H100 GPUs, the company developed the toned-down A800 and H800 chips. Late last year, U.S. regulators axed the shipment of these GPUs to China as well. Nvidia is missing out on billions of dollars in potential quarterly sales because of these restrictions.

The final damning factor for Nvidia, aside from its lofty valuation, is that every next-big-thing investment trend over the past 30 years has navigated its way through an early stage bubble, without exception. Investors have a terrible habit of overestimating the adoption/demand of new innovations or trends, leading to bubbles. It’s highly unlikely that Nvidia/AI is going to be the exception to this unwritten rule.

Although Nvidia has made patient investors richer, locking in some of those gains would likely be a wise decision.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 18, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Sean Williams has positions in Alphabet, Amazon, and Meta Platforms. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

If You Invested $1,000 in Artificial Intelligence (AI) Stock Nvidia for Its IPO in 1999, Here’s the Jaw-Dropping Amount of Money You’d Have Now was originally published by The Motley Fool

Many people worry about their finances, stressing over whether they’re saving enough, spending too much or heading toward a debt crisis.

But several often-overlooked signs may indicate that you’re in better financial shape than you realize. While having a significant nest egg or being debt-free are obvious indicators of financial wellness, there are more subtle clues that your money-management skills are on point.

Don’t Miss:

Are you rich? Here’s what Americans think you need to be considered wealthy.

The average American couple has saved this much money for retirement — How do you compare?

One way to gauge whether you’re in better financial shape than you realize is by looking at your savings account balance relative to national averages. The Motley Fool Ascent survey found that 71% of Americans have $5,000 or less in savings, with 41% having $500 or less set aside.

Specifically, the survey revealed:

11% have $0 in savings

30% have between $1-$500

8% have $500-$1,000

22% have $1,001-$5,000

So if your savings exceed $5,000, you are already outpacing most American households in terms of having a financial cushion. And if your balance tops $10,000, you find yourself in the minority of only 21% of people who have managed to amass a five-figure safety net.

Looking at net worth, which is the total of all assets (retirement accounts, home equity, investments, etc.) minus total debts, can provide perspective. If your net worth exceeds the median level for your age group, it signals you have accumulated more wealth than the typical household in your cohort.

For example, according to the Federal Reserve’s Survey Of Consumer Finances published in October 2023, the median net worth for ages 35-44 is $135,600. For ages 45-54 it’s $247,200. Having a net worth higher than these medians suggests you are ahead of the curve in building up a financial backbone.

Trending: Breaking records, mortgage loans generated $12.25 trillion of household debt nationwide – What are the other major categories of debt?

With a mortgage being most families’ largest debt, having paid down more principal than what remains outstanding is an encouraging sign. Once you owe the bank less than your home’s value, you are positioned with some protective equity.

Nationally, the average mortgage debt is around $241,815, according to Bankrate. If your remaining balance is comfortably below this level, it implies you’ve made serious headway in reducing your housing debt burden.

Experts advise keeping consumer debt payments (student loans, auto loans, credit cards, etc.) below 15% of your gross monthly income. If you meet this threshold, it means you likely have affordable, manageable debt loads that don’t risk putting you in an overly strained cash flow situation.

For the average U.S. household income of around $70,000 per year, 15% would equate to debt payments of less than $875 per month. Lower debt obligations give you more financial breathing room.

A general personal finance rule of thumb is to have enough readily accessible cash savings to cover approximately three to six months’ worth of basic living expenses in case of job loss or income disruption. If your liquid cash reserves allow you to meet at least the lower three-month benchmark, it demonstrates an ability to weather short-term financial hardships.

Based on the average monthly expenditure of $6,081, three months’ worth of expenses would require cash savings of $18,243 to meet the lower benchmark of the three- to six-month rule of thumb for financial preparedness.

Regular contributions to retirement accounts such as a 401(k), individual retirement account (IRA) or another pension plan are indicative of forward-thinking financial planning. Starting early and contributing consistently to your retirement savings can leverage the power of compound interest, significantly impacting your financial security in later years.

A professional advisor can analyze your current savings levels, projected retirement expenses and risk tolerance to determine whether you’re on track to reach your retirement goals or if you need to make adjustments. They can also ensure your investment portfolio is properly allocated and diversified based on your age and retirement timeline.

Making the effort to consult an adviser every few years demonstrates a commitment to objectively assessing your retirement readiness. Small course corrections now can have a significant positive impact down the road versus leaving your retirement planning on autopilot indefinitely.

Read Next:

*This information is not financial advice, and personalized guidance from a financial adviser is recommended for making well-informed decisions.

Jeannine Mancini has written about personal finance and investment for the past 13 years in a variety of publications including Zacks, The Nest and eHow. She is not a licensed financial adviser, and the content herein is for information purposes only and is not, and does not constitute or intend to constitute, investment advice or any investment service. While Mancini believes the information contained herein is reliable and derived from reliable sources, there is no representation, warranty or undertaking, stated or implied, as to the accuracy or completeness of the information.

“ACTIVE INVESTORS’ SECRET WEAPON” Supercharge Your Stock Market Game with the #1 “news & everything else” trading tool: Benzinga Pro – Click here to start Your 14-Day Trial Now!

Get the latest stock analysis from Benzinga?

This article Are You Secretly Doing Better With Your Money Than You Think? Here Are Some Signs You’re Financially Healthy originally appeared on Benzinga.com

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Over lengthy periods, it’s tough to outpace equities in the return column. Compared to gold, oil, housing, and Treasury bonds, the annualized return of stocks trumps them all over the long run.

However, the predictability of directional moves in the Dow Jones Industrial Average (DJINDICES: ^DJI), S&P 500 (SNPINDEX: ^GSPC), and Nasdaq Composite (NASDAQINDEX: ^IXIC) gets thrown out the window when the time frame is narrowed. Since the start of 2020, these three indexes have traded off bear and bull markets in successive years.

Even though forecasting directional moves for the major indexes can’t be done with 100% accuracy, it doesn’t stop investors from trying to gain an edge. This is where a very select group of economic data points and predictive indicators comes into play. Though Wall Street offers no short-term guarantees, a couple of data points and indicators do have exceptional track records of correlating with moves higher or lower in the broader market.

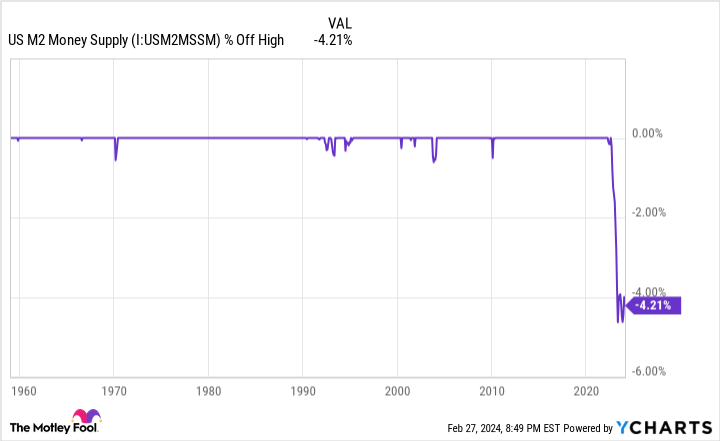

One such data point that speaks volumes at the moment is U.S. money supply.

Among the five money supply measures, two receive the bulk of the attention from economists and investors: M1 and M2. M1 factors in all the cash and coins in circulation, as well as demand deposits in a checking account. Think of M1 as cash that’s easily accessible and can be spent in the blink of an eye.

Meanwhile, M2 takes into account everything in M1 and adds in savings accounts, money market accounts, and certificates of deposit (CDs) below $100,000. M2 is still factoring in cash that consumers can spend, but it’s adding in capital that takes a bit more effort to get to. It’s this figure, M2, that is causing alarm in the investing world.

For well over a century, U.S. money supply has been rising with little interruption. Since a growing economy requires more cash and coins in circulation to complete transactions, rising money supply is something economists and investors tend to take for granted and assume is a given.

But on rare occasions, U.S. money supply contracts in a big way — and that’s historically portended bad news for the U.S. economy and stock market.

In July 2022, U.S. M2 money supply peaked at an all-time high of roughly $21.7 trillion. Based on the Feb. 27 data release from the Board of Governors of the Federal Reserve, M2 stood at $20.78 trillion, as of January 2024. All told, we’re looking at a year-over-year drop of 1.44% and an aggregate decline from the July 2022 peak of 4.21%. This is the first significant drop in M2 since the Great Depression.

The caveat to the decline since July 2022 is that M2 expanded at a truly historic pace during the COVID-19 pandemic. Fiscal stimulus increased M2 by a record 26% on a year-over-year basis. Thus, a case could be made that a 4.21% retracement is merely a reversion to the mean. Then again, history has been incredibly unforgiving when M2 money supply has fallen by at least 2% on a year-over-year basis.

According to research conducted by Reventure Consulting CEO Nick Gerli, which relied on data from the U.S. Census Bureau and the Federal Reserve, there have only been five instances, when back-tested to 1870, where M2 has declined by at least 2%: 1878, 1893, 1921, 1931-1933, and July 2022 through at least January 2024. The previous four instances all coincided with deflationary depressions and double-digit unemployment rates.

WARNING: the Money Supply is officially contracting. 📉

This has only happened 4 previous times in last 150 years.

Each time a Depression with double-digit unemployment rates followed. 😬 pic.twitter.com/j3FE532oac

— Nick Gerli (@nickgerli1) March 8, 2023

If I can offer a ray of hope, two of the four previous incidences occurred prior to the creation of the nation’s central bank, and the other two date back more than nine decades. The Federal Reserve’s knowledge of monetary policy, and the fiscal tools available to the federal government, make it highly unlikely that a depression would materialize today.

On the flip side, declining money supply isn’t something that should be swept under the rug. If the core inflation rate remains above the Fed’s 2% long-term target and M2 continues to decline, there will be less discretionary income to go around.

Based on data from Bank of America Global Research, about two-thirds of the S&P 500’s max drawdowns occur after, not prior to, a U.S. recession being declared. In short, a persistent decline in M2 money supply could spell trouble for a currently red-hot stock market.

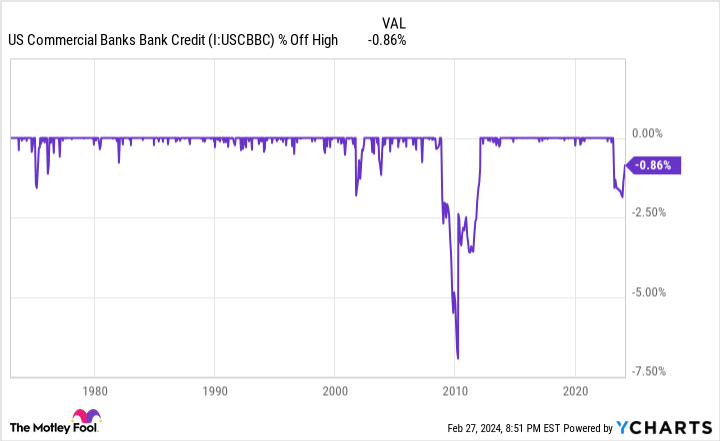

The worry for investors is that M2 represents just one money metric that looks to be working against the U.S. economy and stocks, as a whole. Another key money-based data point that’s cause for concern is commercial bank credit.

Commercial bank credit is reported by the Board of Governors of the Federal Reserve on a weekly basis and factors in all of the loans, leases, and securities held by U.S. commercial banks. Over the past 51 years, commercial bank credit has expanded from around $567 billion to roughly $17.44 trillion, as of the week ended Feb. 14, 2024.

Just as M2 rising over time makes complete sense, so does the regular expansion of commercial bank credit. As the U.S. economy grows, it’s only natural that consumers and businesses are going to increase their borrowing. Furthermore, commercial banks offset the cost of taking in deposits by lending.

Trouble arises when this steadily climbing metric heads decisively south.

Since data reporting began in January 1973, there have only been three instances where commercial bank credit has pulled back at least 2% from its all-time high:

In October 2001, during the dot-com bubble, commercial bank credit slipped a maximum of 2.09%.

In March 2010, shortly after the Great Recession, commercial bank credit troughed at a 6.94% decline.

In November 2023, commercial bank credit hit a peak drop of 2.07%.

While it is worth noting that commercial bank credit has begun climbing in recent weeks, the drop throughout 2023 pretty clearly shows that banks have tightened their lending standards. When lending institutions become pickier about how they lend their money, it’s not uncommon for businesses to pare back hiring, innovation, and acquisitions. Put another way, a notable decline in commercial bank credit can be a precursor to an economic downturn.

Although Wall Street and the economy aren’t intertwined, recessions tend to negatively impact corporate earnings, which in turn would be expected to send the Dow Jones, S&P 500, and Nasdaq Composite lower. For context, the S&P 500 lost around half of its value during the previous two sizable contractions in commercial bank credit.

Considering that the Dow Jones Industrial Average and S&P 500 have rocketed to record-closing highs in 2024, a prognostication of downside in the broader market probably isn’t what you want to hear. But just as history can, at times, serve as a short-term guide that portends downside in stocks, it’s often the greatest ally of patient investors.

As much as workers and investors might dislike recessions, the fact remains that they’re a normal and unavoidable part of the economic cycle. They’re also notoriously short-lived. Only three recessions of the 12 that have occurred since the end of World War II made it to the 12-month mark, and none of the remaining three lasted longer than 18 months. In other words, downturns in the U.S. economy are fleeting.

Compare this to periods of growth over the past 78 years and change. Though there are a couple of growth spurts that lasted around a year, most expansions were multiyear events. In fact, two periods of growth surpassed the 10-year mark.

This disparity between U.S. economic growth and contractions is seen in Wall Street’s major indexes. As an example, the S&P 500 has endured 40 separate double-digit percentage corrections since the start of 1950. However, each and every one of these downturns was eventually put in the back seat by a bull market rally. Despite never knowing precisely when these declines will occur, history has pretty conclusively shown that the major indexes will rise in value over time.

To add to the above, the analysts at Bespoke Investment Group put out a dataset in June 2023 that compared the average length of bear markets in the benchmark S&P 500 to bull markets since the start of the Great Depression in September 1929. While the average bull market has endured 1,011 calendar days, the 27 bear markets over the past 94 years have stuck around for an average of only 286 calendar days (about 9.5 months).

The final data set that overwhelmingly demonstrates the power of time and perspective for investors is updated annually by Crestmont Research.

The researchers at Crestmont analyzed the rolling 20-year total returns, including dividends, of the S&P 500 dating back to 1900. Even though the S&P didn’t come into existence until 1923, researchers were able to trace its components to other major indexes at the time, thereby allowing total returns data to be back-tested to the start of the 20th century. This left Crestmont with 105 rolling 20-year periods (1919-2023) to analyze.

What Crestmont’s dataset showed is that all 105 rolling 20-year periods produced a positive total return. Hypothetically speaking, as long as an investor purchased an S&P 500 tracking index since 1900 and held that position for 20 years, they made money, without fail, every time.

No matter what M2 money supply and commercial bank credit suggest will happen with stocks, long-term investors are perfectly positioned to succeed.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has nearly tripled the market.*

They just revealed what they believe are the 10 best stocks for investors to buy right now…

*Stock Advisor returns as of February 26, 2024

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Sean Williams has positions in Bank of America. The Motley Fool has positions in and recommends Bank of America. The Motley Fool has a disclosure policy.

U.S. Money Supply Is Making History for the First Time Since the Great Depression, and It Implies a Big Move in Stocks Is on the Way was originally published by The Motley Fool

Joining the world’s most exclusive club — the top 1% — has arguably never looked more doable, but a lot depends on the country in which you’re trying to achieve that status.

That’s according to the 2024 Knight Frank Wealth Report, which lays out how many millions it takes for an individual to join the most-moneyed club across the world.

As exclusive as the one-percenter appellation may sound, it’s “actually easier to become a member of this particular club than it is to gain UHNWI status,” observes the Knight Frank report, released Wednesday.

Anyone who has achieved UHNWI status is an ultra-high-net-worth individual with net wealth of $30 million or more.

Define “easier,” right? The country with the highest barrier to 1% entry is Monaco, where more than $12.8 million is required to be part of that top-percentage-point category as of the end of 2023.

The five countries with the highest bars to entry are Monaco, Luxembourg, Switzerland, the U.S. and Singapore.

In the U.S., the threshold is $5.8 million. And for those seeking a fast track into the 1% club, and with unrestricted freedom to relocate, in China, at the bottom of that list of 17 countries, just over $1 million is required to qualify as a one-percenter, and, just ahead of it is Japan, where just under $2 million is needed.

Knight Frank, a global real-estate firm, said the number of UHNWI individuals globally rose by 4.2% to 626,619 from 601,300 a year earlier, which more than reversed a decline seen in 2022.

The report included an attitudes survey that showed how optimistic money managers were that their clients would amass more wealth in 2024. On a scale of 1 to 5, the Middle East came out on top, with North America lower down, according to this chart:

Looking across generations, the report found one group in particular was most optimistic about building their wealth — Generation Z (born between 1997 and 2012, by the Pew Research Center’s reckoning), of whom 75% said they expected their wealth to increase in 2024. Boomers (born, according to the U.S. Census Bureau, between mid-1946 and mid-1964) were, among survey respondents, at the lower end, with Generation X (born from the end of the postwar baby boom through 1980) not far behind, at just over 50% each.

Read on: Retirement balances are at their highest in nearly two years, with 20% jump in 401(k) millionaires

Nvidia (NASDAQ: NVDA) stock’s stunning rally since the beginning of 2023 was primarily driven by the rapid growth of the company’s data center business, which benefited from the booming demand for its artificial intelligence (AI) graphics cards.

In the company’s recently concluded fiscal year 2024 (which ended on Jan. 28), the data center business produced a record $47.5 billion in revenue, accounting for 79% of its top line. That was a massive increase of 217% from the year-ago period.

The data center business recorded a much stronger year-over-year increase of 409% in revenue to $18.4 billion in fiscal Q4, significantly outpacing the segment’s annual growth.

This suggests Nvidia’s data center business is still gaining momentum, which also explains why the company’s outlook for the current quarter was well ahead of consensus estimates. Nvidia expects revenue of $24 billion in the first quarter of fiscal 2025, which would be a 233% increase from the year-ago period.

Given that Nvidia relies on sales of chips that are being deployed in data centers for AI training and inference purposes, it can be easily concluded that this business segment can continue to be a major catalyst for the company.

However, investors shouldn’t ignore the progress Nvidia is making in its second-largest business segment — which was originally the company’s bread and butter before AI arrived — as it has the potential to supercharge the company’s already impressive growth.

Nvidia brought major innovation to personal computers (PCs) in 1999 when it introduced what it calls the world’s first graphics processing unit (GPU), an additional processor tacked on to a PC’s motherboard for running graphics-intensive workloads such as video games.

Nvidia’s GPU technology evolved over the years, and it is now being used in multiple industries ranging from automotive to digital twins to AI. But at the same time, the company continues to be a major player in the market for discrete PC graphics cards with a share of more than 80%. The good part is that this dominance is leading to robust financial gains for Nvidia.

The company generated $10.4 billion in revenue in fiscal 2024 from the gaming segment, an increase of 15% from the prior-year period. That’s a nice recovery considering that the gaming GPU market was not in great shape a year ago on account of poor PC sales and oversupply. However, Nvidia’s 56% year-over-year increase in gaming revenue in the fourth quarter of fiscal 2024 suggests that this market gained tremendous momentum.

One of the reasons why that’s happening is because of the recovery in the PC market. Market research firm Canalys estimates that PC sales could increase by 8% in 2024 following last year’s drop of 12.4%. AI is going to play a key role in this growth. According to IDC, AI-enabled PCs capable of running generative AI applications locally could gain solid traction from 2024 with shipments of 50 million units.

IDC predicts that annual shipments of such AI-enabled PCs could climb to an impressive 167 million units in 2027. Even then, this emerging niche will have a lot of room for growth as AI PCs are expected to account for 60% of overall PC shipments in 2027. For Nvidia, the adoption of AI PCs will unlock a massive growth opportunity, and the good part is that the company has already started capitalizing on this nascent market.

In its latest earnings release, Nvidia said that it enabled generative AI capabilities for an installed base of 100 million users who are using the RTX series of graphics cards.

Moreover, the company released new RTX 40 Super series graphics cards starting at $599 in January, which come equipped with generative AI capabilities. In a presentation in October 2023, Nvidia pointed out that 47% of its installed base of discrete GPU users were using RTX graphics cards. Meanwhile, only 20% of the installed base is using a graphics card more powerful than an RTX 3060, a chip that’s now more than three years old.

So, a big chunk of Nvidia’s user base can be expected to upgrade to its new, AI-capable GPUs as generative AI adoption gains steam. At the same time, the increase in the adoption of AI-enabled PCs suggests that there is a huge addressable opportunity for Nvidia to tap into.

Annual shipments of AI-powered PCs could hit 167 million units in 2027, as per IDC. The researcher also points out that these PCs will be equipped with dedicated chips to run generative AI workloads. Nvidia’s latest RTX 40 series GPUs come with Tensor Cores to enable AI workloads. These Tensor Cores offer between 242 and 1,321 tera operations per second (TOPS) of performance.

This puts Nvidia’s RTX 40 series GPUs in the category of advanced AI chips, IDC said. It said AI PCs equipped with a dedicated chip that offers more than 60 TOPS of performance are categorized as advanced AI PCs.

Nvidia controls 80% of the AI GPU market. If the company can maintain that share in 2027, it could sell a whopping 133 million AI GPUs for PCs that year. If Nvidia can maintain an average selling price of even $400 per AI GPU, which is significantly lower than the $599 starting price for the RTX 40 Super Series, it can generate a whopping $53 billion in annual gaming revenue in 2027.

That would be more than 5 times Nvidia’s gaming revenue in the latest fiscal year, suggesting that the company could still enjoy solid growth in a market that propelled it into the limelight years ago and was its bread and butter for a long time. Throw in the potential growth the company could witness in the data center business over the next five years, and it won’t be surprising to see it sustain its red-hot stock market rally in the long run.

That’s why investors would do well to buy this semiconductor stock while it is available at an attractive 33 times forward earnings, which is almost in line with the Nasdaq-100 index’s forward earnings multiple of 31.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 26, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

Nvidia Is Making a Lot of Money Selling Artificial Intelligence (AI) Chips, but You May Be Surprised About How Much It Could Make From This Traditional Market was originally published by The Motley Fool