Nvidia and Broadcom shares are BofA’s leading ways to play the AI trend within the chip sector, but several other players could carve out a “profitable niche.”

Source link

Nvidia and Broadcom shares are BofA’s leading ways to play the AI trend within the chip sector, but several other players could carve out a “profitable niche.”

Source link

Nvidia (NVDA 0.12%) stock is one of the most followed stocks in the market. That’s because shares of the artificial intelligence (AI) chip leader have been performing fantastically, and investors are optimistic about the company’s long-term growth potential.

If you’re considering investing in Nvidia stock, it’s extremely helpful to know how the company makes its money.

The following chart shows the company’s revenue breakdown by platform for its most recently reported quarter.

|

Platform |

Revenue Fiscal Q4 2024 (Ended Jan. 28) |

Percentage of Total Fiscal Q4 2024 Revenue* |

|---|---|---|

| Data center |

$18.4 billion |

83% |

| Gaming |

$2.9 billion |

13% |

| Professional visualization |

$463 million |

2% |

| Automotive | $281 million | 1% |

| OEM and other | $90 million | Less than 1% |

|

Total |

$22.1 billion |

100% |

Data source: Nvidia. OEM = original equipment manufacturer; OEM and other is not a target market platform. *Calculations by author.

Together, Nvidia’s data center and gaming platforms accounted for 96% of its total revenue in its most recently reported quarter. So, the performances of its other platforms currently make little difference in the company’s overall financial results.

Nvidia’s data center platform supplies graphics processing unit (GPU) chips and related products for speeding up the processing of AI and high-performance computing workloads. This platform’s revenue growth has significantly revved up over the last year because companies and other entities across industries are hungry to acquire generative AI capabilities. This new tech, which powers OpenAI’s wildly popular ChatGPT chatbot, greatly increases the potential applications for AI.

Demand for Nvidia’s data center GPU, the H100, and related products has been so mighty that the company’s supply can’t keep up with it. Moreover, management expects powerful demand for the H100’s successors launching this year — H200 and B100, the first GPU based on the company’s new Blackwell architecture.

Nvidia is the world’s No. 1 supplier of graphics cards — under the GeForce brand — for computer gaming, a market that has grown steadily. In the fourth quarter of 2023, it had an 80% share of the desktop discrete GPU market, according to Jon Peddie Research. Advanced Micro Devices (AMD) captured a 19% share, while market newcomer Intel had a 1% share.

|

Platform |

Fiscal Q4 2024 Revenue Growth YOY |

|---|---|

| Data center | 409% |

| Gaming | 56% |

| Professional visualization | 105% |

| Automotive | (4%) |

| OEM and other | 7% |

|

Total |

265% |

Data source: Nvidia. YOY = year over year.

As shown in the top table, Nvidia’s data center platform accounted for 83% of its total revenue in its most recently reported quarter. This percentage will continue to rise if the data center continues to grow faster than the other platforms.

Nvidia doesn’t break out any form of profits by platform in its quarterly earnings releases. But we can make good deductions about this topic by using data it provided in its recent 10-K filing with the Securities and Exchange Commission (SEC). In this document, Nvidia breaks out its fiscal year 2024 revenue and operating income by its two reporting segments, and lists what business components are included in each segment.

|

Segment |

Revenue Fiscal Year 2024 (Ended Jan. 28) |

Percentage of Total Fiscal Year 2024 Revenue* |

Operating Income Fiscal Year 2024 |

Percentage of Total Fiscal Year 2024 Segment Operating Income* |

|---|---|---|---|---|

| Compute and networking | $47.4 billion | 78% |

$32.0 billion |

85% |

| Graphics | $13.5 billion | 22% | $5.9 billion | 15% |

| Segment total | $60.9 billion | 100% | $37.9 billion | 100% |

Data source: Nvidia. *Calculations by author.

The compute and networking segment is more profitable than the graphics segment. In Nvidia’s fiscal year ended Jan. 28, the compute and networking segment’s operating income (or operating profit) contributed 78% of the company’s total revenue, and an even greater percentage of its total segment operating income. The opposite is true of the graphics segment.

Nearly all parts of the data center platform are included in the compute and networking segment, according to the 10-K filing. So, we can deduct from this fact and the chart data that Nvidia’s data center platform is more profitable than its overall business.

Nvidia’s profits (or “earnings”) are growing faster than its revenue because its fastest growing platform, the data center, is more profitable than its overall business. This is a winning formula for powering its stock price higher.

This dynamic is poised to continue for the quarter ending in late April. Management has guided for the quarter’s revenue to grow 234% and adjusted earnings per share (EPS) to soar 396% year over year.

Beth McKenna has positions in Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices and Nvidia. The Motley Fool recommends Intel and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short May 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

The AI bull market is here. Stocks are back at all-time highs, thanks largely to a new boom in artificial intelligence (AI).

The launch of ChatGPT has set off a race to be a leader in what top CEOs and major investors think will be the next transformative technology, generative AI. Nvidia, which sells the graphics processing unit (GPU) components that are the backbone of the advanced computing systems required for AI, has been the biggest winner so far. However, there are several other stocks primed to be winners as well. Let’s take a closer look at two of them.

Micron Technologies (NASDAQ: MU) is a leader in memory chips. Historically, its business has been highly cyclical, fluctuating from boom times to busts as the semiconductor industry tends to be sensitive to supply gluts and demand shifts. Just a year ago, the company was operating at a wide loss as coming out of the pandemic, the slowdown in demand for PCs and tablets crushed prices for memory chips.

However, Micron is now emerging as a beneficiary of the AI boom as memory chips play a key role in AI servers. As Micron management explained on a recent earnings call, AI server demand is driving growth in high-bandwidth memory, which tightened the supply for the DRAM and NAND chips that Micron specializes in.

Because of that trend, the company expects DRAM and NAND prices to increase through calendar 2024. It now expects record revenue and “much-improved profitability” in fiscal 2025.

CEO Sanjay Mehrotra also said, “We are in the very early innings of a multiyear growth phase driven by AI as this disruptive technology will transform every aspect of business and society.” Micron’s memory and storage components are valuable in both training and inference functions for AI algorithms, making Micron a likely winner in AI.

If the company can generate record revenue in fiscal 2025, it would top the $30.7 billion in revenue it made in fiscal 2022. At that level, Micron would trade at a price-to-sales ratio of around 4, which is an attractive valuation, compared to other AI stocks.

Micron also has the potential to be highly profitable as its operating margin reached 50% in 2019. If the company’s profitability surges, the stock could move a lot higher from here.

Another tech stock that seems well-positioned to ride the AI wave is Taiwan Semiconductor Manufacturing (NYSE: TSM). The company, better known as TSMC, is the world’s largest contract semiconductor foundry. It handles manufacturing for many of the world’s biggest chip designers, including Apple, Nvidia, Broadcom, and Advanced Micro Devices.

TSMC has more than a 50% market share of the third-party chip manufacturing industry, giving it tremendous market power in the semiconductor industry more broadly and in AI chips specifically. It handles approximately 90% of the third-party market of advanced chips, which AI models rely on.

Because of its virtual monopoly in third-party chip manufacturing, TSMC is more resilient than a company like Nvidia, which needs to maintain its competitive edge and pricing power for the stock to keep gaining. Chip manufacturing has high entry barriers, which makes it unlikely that TSMC’s leadership will be challenged in the coming years.

Like Micron, TSMC is also emerging from the earlier slump in the semiconductor industry, but its growth is picking up with the help of AI. Through the year’s first two months, revenue was up 9.4% and revenue growth accelerated to 11.3%. Investors took this as a sign of AI demand picking up as it was a significant improvement from flat revenue growth in the fourth quarter.

TSMC is also highly profitable, further proving its competitive advantages and pricing power. In the fourth quarter, it recorded an operating margin of 41.6%.

Finally, TSMC is affordably priced, trading at a price-to-earnings ratio of 28, and profits are expected to improve as AI provides a tailwind. The chip manufacturing giant was already a rock-solid business, but its economic moat seems poised to widen in the AI era.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Jeremy Bowman has positions in Broadcom. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

2 No-Brainer Artificial Intelligence (AI) Stocks (not Named Nvidia) to Buy Right Now was originally published by The Motley Fool

Nvidia (NVDA -0.17%) has been one of the market’s hottest chip stocks. The chipmaker was originally known for making gaming GPUs, but the rapid expansion of the artificial intelligence (AI) market over the past few years drove more companies to purchase its high-end data center GPUs to process complex AI tasks.

Nvidia’s rally of more than 2,000% over the past five years boosted its market cap to $2.4 trillion and minted a lot of millionaires. But it’s also driving more investors to search for the next big chipmaker that could follow Nvidia’s footsteps.

Image source: Micron.

Could that chipmaker be Micron (MU 2.32%), one of the world’s top producers of DRAM and NAND memory chips? Let’s review the key differences between Micron and Nvidia to see if Micron has a shot at replicating Nvidia’s gains.

Micron designs its memory chips and manufactures them at its own foundries. That makes it different from Nvidia, which designs its chips but outsources its production to third-party foundries like Samsung and Taiwan Semiconductor Manufacturing Company. Micron operates that capital-intensive model at much lower margins than Nvidia.

Data source: YCharts

Micron’s memory chips also cost a lot less than Nvidia’s GPUs, and it doesn’t dominate its core markets in the same way as Nvidia. Micron is the world’s third-largest supplier of DRAM chips and the fifth-largest supplier of NAND chips, but Nvidia is the leading producer of discrete GPUs by a wide margin. According to JPR, Nvidia controlled 80% of the market at the end of 2023, while AMD only held a 19% share.

Compared to Nvidia, Micron operates in a more commoditized market, has less pricing power against its competitors, and is more exposed to cyclical downturns as the memory chip market goes through its boom-and-bust cycles. However, Micron still produces denser and more power-efficient DRAM and NAND chips than its two largest competitors, Samsung and SK Hynix. That technological edge helps Micron lock in producers of higher-end PCs, mobile devices, and servers.

Micron endured a rough slowdown over the past two years as personal computer (PC) shipments declined in a post-pandemic market, the 5G upgrade cycle ended, and the macro headwinds curbed its chip sales to the enterprise and industrial markets. The Chinese government also barred its key infrastructure providers from buying Micron’s memory chips. All of those challenges offset its stronger growth in the automotive and AI markets.

Micron’s revenue grew 29% in fiscal 2021 (which ended in September 2020), but only rose 11% in fiscal 2022 and tumbled 49% in fiscal 2023. However, analysts expect its revenue to rise 56% in fiscal 2024 and 43% in fiscal 2025 as three tailwinds kick in. First, the PC and smartphone markets should gradually stabilize. Second, it should sell more chips to the enterprise, industrial, and automotive markets as the macro environment warms up again.

Lastly, the explosive growth of the generative AI market will drive more data centers to upgrade their memory chips alongside Nvidia’s GPUs. During Micron’s latest conference call, CEO Sanjay Mehrotra said the memory chip market was still in “the very early innings of a multiyear growth phase driven by AI” and that those technologies would transform “every aspect of business and society.” As an example, Mehrotra predicted that AI-enabled phones would “carry 50% to 100% greater DRAM content compared to non-AI flagship phones today.”

That’s a bright outlook, but Micron’s new growth cycle will still likely end in a few years. That’s because companies drive up memory prices by buying a lot of chips when a certain market — like smartphones, cloud data centers, and AI — runs hot.

In response, Micron and its peers usually ramp up their production of new chips to satisfy that demand. But once the hot market cools, the chip shortage quickly turns into a supply glut as companies are left with an excess inventory of chips. That’s why Micron’s chip sales fell in 2019 and 2022 — and why they’ll likely drop again once the AI market matures.

This next growth cycle could last a lot longer than previous ones, but it will eventually end in a downturn. Nvidia will also face a similar slowdown, but its cyclical declines have been much milder than Micron’s over the past decade. That’s because Nvidia’s dominance of the discrete GPU market grants it more pricing power during market downturns — while Micron remains heavily exposed to the price cuts at its larger competitors.

Micron’s stock trades at less than 4 times next year’s sales, and it could run higher as its next growth cycle begins. If its valuations hold steady and it grows its revenue at a CAGR of 30% over the next five years, its stock could nearly quadruple. That would be an impressive gain, but it could end in a cyclical downturn and won’t come close to replicating Nvidia’s gains over the past five years. Simply put, Micron is still a promising semiconductor play — but it’s probably not the next Nvidia.

Leo Sun has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Tesla CEO, Elon Musk (L), and Nvidia CEO, Jensen Huang (R).

Reuters

In November 2023, at an all-hands meeting with employees, Nvidia CEO Jensen Huang was asked whether the company would follow the lead of Apple and Disney and suspend its advertising on X due to rising levels of antisemitism and other hate speech on the platform.

X owner Elon Musk said earlier that month that he agreed with a post on the site that accused “Jewish communities” of pushing “hatred against whites.” Numerous brands — Disney and Apple among them — moved quickly to pause their ad campaigns.

Huang’s response was firm but diplomatic, according to people who were listening to the meeting but asked not to be named because they weren’t authorized to speak to the press. He said the chipmaker hadn’t advertised on X in a very long time and had no plans to do so. However, Huang also emphasized that Nvidia would never make public statements against another business.

Left out of Huang’s commentary at the time was any detail regarding Nvidia’s increasing coziness with Musk’s business empire.

Nvidia is seeing soaring demand for its graphics processing units (GPUs) and related hardware and services, a boom that’s lifted the company’s market cap well past $2 trillion. Nvidia’s products, including new accelerator chips, provide computing power for generative artificial intelligence workloads, robotics, research and data center projects.

Revenue in the latest quarter jumped a whopping 265% to $22.1 billion, and last year Nvidia surpassed Intel in total sales.

Musk has made promises that his companies will develop sophisticated AI products, and doing so requires buying up a lot of Nvidia’s technology.

Their cozy relationship was on display this week at Nvidia’s annual GTC conference in San Jose, California. The event, which attracted roughly 16,000 attendees including celebrities like Ashton Kutcher and Kendrick Lamar, had two sessions featuring leaders of xAI, the startup Musk formally revealed in July 2023.

Christian Szegedy, a co-founder and research scientist at xAI who previously worked at Google, spoke at a fireside chat with Bojan Tunguz, a data scientist at Nvidia. Another co-founder and research engineer from xAI, Igor Babuschkin, a veteran of OpenAI and Google, gave an overview of how Musk’s startup is using Nvidia GPUs to help “accelerate training and inference of their Grok model,” referring to the startup’s AI chatbot.

In Nvidia’s press release on Monday announcing the launch of its Blackwell AI chips, Musk was quoted saying, “There is currently nothing better than NVIDIA hardware for AI.”

Musk, who helped create OpenAI before a public split with CEO Sam Altman and other founders, launched xAI to develop AI models and software products.

Meanwhile, his electric vehicle maker Tesla has spent years working on AI software to turn its cars into autonomous vehicles. It’s also now developing the Tesla Bot, or Optimus, a humanoid robot.

While the vast majority of Tesla’s revenue comes from its automotive business, Musk often encourages shareholders to think of it differently. In January he said, in a post on X, “Tesla is an AI/robotics company that appears to many to be a car company.”

Tesla first discussed plans to build a “Dojo supercomputer” at an AI Day presentation in August 2021. The aim for Dojo was to process and train AI models with huge amounts of video and data captured by Tesla vehicles.

Nvidia is at the heart of its AI efforts. Last August, former Tesla AI engineer Tim Zaman posted on X that a Tesla AI cluster, built using 10,000 of Nvidia’s H100 chips, was ready to go live.

Musk said a post on X in January that while a Dojo supercomputer cost $500 million to build, “Tesla will spend more than that on Nvidia hardware this year.” He added, “The table stakes for being competitive in AI are at least several billion dollars per year at this point.”

Musk said Tesla was “pursuing the dual path of Nvidia and Dojo,” seemingly implying that it’s building Dojo without Nvidia’s technology but using it elsewhere. Musk described Dojo as “a long shot worth taking because the payoff is potentially very high. But it’s not something that is a high probability.”

Oracle founder Larry Ellison, a close friend of Musk’s, former Tesla board member and investor in X, said in December on his company’s earnings call that xAI had secured Nvidia GPUs through Oracle to create the first version of Grok, but that Oracle wasn’t able to meet Musk’s demands.

“Boy, do they want a lot more GPUs than we gave them,” Ellison said. “We gave them quite a few, but they wanted more and we are in the process of getting them more.”

Larry Ellison, chairman and co-founder of Oracle Corp., speaks during the Oracle OpenWorld 2017 conference in San Francisco, California, U.S., on Sunday, Oct. 1, 2017.

David Paul Morris | Bloomberg | Getty Images

While Musk and Huang have a longstanding connection and are now doing more business together than ever, the relationship hasn’t always appeared friendly.

Last June, Musk went so far as to call Nvidia monopolistic, in response to a post on X that accused Nvidia of “spiking the price” of its GPUs, which it could do because of the supply shortage.

Musk wrote that competitive chips were in development, and that “Nvidia will not have a monopoly on large-scale training & inference forever.”

The remarks failed to provoke Huang.

Speaking at The New York Times’ DealBook summit a few months later, Huang credited Musk and OpenAI for the decision to develop Nvidia’s first AI supercomputer, the DGX system, starting back in 2012.

Huang said it took Nvidia about five years to perfect and ship the supercomputer, which he personally delivered to Musk for use by OpenAI.

“Elon saw it, and he goes, ‘I want one of those’ — he told me about OpenAI,” Huang said on stage. “I delivered the world’s first AI supercomputer to OpenAI on that day.”

A spokesperson for Nvidia declined to comment. Tesla and xAI didn’t respond to requests for comment.

Fool.com contributor Parkev Tatevosian elaborates on the risks Nvidia (NVDA 1.07%) stock investors face.

*Stock prices used were the afternoon prices of March 16, 2024. The video was published on March 18, 2024.

Parkev Tatevosian, CFA has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

Parkev Tatevosian is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through his link, he will earn some extra money that supports his channel. His opinions remain his own and are unaffected by The Motley Fool.

Over the long run, Wall Street is a bona fide wealth-creating machine. Although gold, oil, housing, and Treasury bonds have increased in value over multiple decades, no asset class has come close to replicating the average annual returns delivered by stocks over the past century.

For example, including dividends paid, the benchmark S&P 500 has delivered just a hair north of a 10% annualized return since its official inception as a 500-company index in 1957. That’s a hearty return that can double investors’ money about every seven years.

But on an aggregate growth basis, the S&P 500 doesn’t hold a candle to what semiconductor stock Nvidia (NASDAQ: NVDA) has done for investors since becoming a publicly traded company in 1999.

Not too long before the dot-com bubble burst in 2000, Nvidia made its grand entrance as a publicly traded company. Its initial public offering (IPO) occurred on Jan. 22, 1999, with shares being sold at $12. Of course, a lot has changed since then.

If investors had the wherewithal to purchase $1,000 worth of Nvidia stock for its IPO, they would have received 83 shares, not including commission costs and fractional shares. In the quarter of a century since going public, this Wall Street darling has split its stock on five separate occasions. The figure in parenthesis behind each split denotes what the original 83-share position would have grown into:

June 27, 2000: 2-for-1 stock split (166 shares)

Sept. 12, 2001: 2-for-1 stock split (332 shares)

April 7, 2006: 2-for-1 stock split (664 shares)

Sept. 11, 2007: 3-for-2 stock split (996 shares)

July 20, 2021: 4-for-1 stock split (3,984 shares)

IPO-day investors have seen their share count in Nvidia grow by a factor of 48. At the same time, the IPO offering price has been reduced to a split-adjusted $0.25 per share.

Based on Nvidia’s closing price of $878.36 on March 15, 2024, a 3,984-share position would equate to $3,499,386. For those of you keeping score at home, Nvidia has produced a 351,244% gain since its IPO, which compares to just a 318% return for the benchmark S&P 500 over the same period. Keep in mind that I’m not including the additional returns from Nvidia’s nominal dividend in this 351,244% figure, either.

Throughout its 25 years as a public company, Nvidia has had moments where it’s thrived. For quite some time, the company’s graphics processing units (GPUs) used for gaming on personal computers were its calling-card to success. The company also gained momentum from 2016 through 2018 as cryptocurrency prices soared. Cryptocurrency miners gobbled up the company’s high-powered GPUs.

But there’s little question that Nvidia’s role as the infrastructure backbone of the artificial intelligence (AI) movement has done most of the heavy lifting.

Though estimates vary wildly, the analysts at PwC believe AI can add $15.7 trillion to global gross domestic product by 2030. Utilizing software and systems to handle tasks that would normally be assigned to humans, and seeing these systems evolve over time and become smarter, is what gives AI application across virtually every sector and industry.

Nvidia’s A100 and H100 GPUs are nothing short of the standard in AI-accelerated data centers. With demand easily outweighing the supply of these high-powered chips, Nvidia has enjoyed otherworldly pricing power, which more than double its sales in fiscal 2024 (ended in late January).

Additionally, Nvidia’s ramp of A100 and H100 chips looks to be in its early innings. Its four largest customers — and fellow “Magnificent Seven” members — Microsoft, Meta Platforms, Amazon, and Alphabet, have been aggressively gobbling up supply for their own AI-fueled ambitions.

However, sustaining this success in the years to come could prove challenging.

For the past year, Nvidia has blown the doors off of Wall Street’s revenue and profit forecasts. But don’t expect this to continue for much longer.

One problem Nvidia may be contending with in the second-half of 2024, if not well beyond, is margin contraction. The scarcity of the company’s AI-GPUs is what’s lifted prices for these chips into the stratosphere. With supply chain issues beginning to ease and external competitors entering the arena, AI-focused GPUs will be far less scarce in the second-half of 2024 than they are now. That’s a recipe for weaker pricing power and lower margins for Nvidia.

What’s arguably an even bigger concern for Nvidia than the external competitors that’ll be challenging its AI-accelerated data center dominance is that its aforementioned top four customers, which account for 40% of its sales, are developing AI-GPUs of their own. Regardless of whether these internally developed GPUs are to complement Nvidia’s chips or replace them, we’re very likely witnessing a peak of orders that will taper into subsequent years.

Nvidia is also getting no help from U.S. regulators. Following an initial round of export restrictions to China for its top-notch A100 and H100 GPUs, the company developed the toned-down A800 and H800 chips. Late last year, U.S. regulators axed the shipment of these GPUs to China as well. Nvidia is missing out on billions of dollars in potential quarterly sales because of these restrictions.

The final damning factor for Nvidia, aside from its lofty valuation, is that every next-big-thing investment trend over the past 30 years has navigated its way through an early stage bubble, without exception. Investors have a terrible habit of overestimating the adoption/demand of new innovations or trends, leading to bubbles. It’s highly unlikely that Nvidia/AI is going to be the exception to this unwritten rule.

Although Nvidia has made patient investors richer, locking in some of those gains would likely be a wise decision.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 18, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Sean Williams has positions in Alphabet, Amazon, and Meta Platforms. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

If You Invested $1,000 in Artificial Intelligence (AI) Stock Nvidia for Its IPO in 1999, Here’s the Jaw-Dropping Amount of Money You’d Have Now was originally published by The Motley Fool

March 8 was a wild day in the stock market. Shares of Nvidia (NVDA -0.12%) surged to an all-time high of $974 only to fall over 10% from that high to end the day at $875.28. At the peak, Nvidia was less than 9% away from surpassing Apple (AAPL -0.22%) in market cap. By close, it was a little over 20% away.

Given Nvidia’s big swings, it seems like the stock could very well surpass Apple to become the second most valuable “Magnificent Seven” stock behind Microsoft. Here’s why Nvidia could keep outperforming Apple in the short term, but why Apple is the better long-term buy.

Image source: Getty Images.

Nvidia is not an unprofitable growth stock that is rallying based on optimism and greed alone (although those are contributing factors). The business is doing phenomenally well, achieving a level of sales and earnings growth paired with margin expansion.

NVDA Revenue (TTM) data by YCharts

The only concern with Nvidia is its valuation. Its price-to-earnings (P/E) ratio based on its trailing 12-month (TTM) earnings is 73.6. But consensus analyst estimates expect Nvidia’s earnings per share (EPS) to more than double from the $11.90 it earned in fiscal 2024 to $24.50 in fiscal 2025. That gives Nvidia a forward P/E of 35.7 — which is far more reasonable.

The easiest way for Nvidia to pass Apple in market cap is for investors to keep bidding up the stock. But the more realistic way is if Nvidia’s earnings live up to expectations.

Nvidia will report its full-year fiscal 2025 results some time in late February or early March next year. If it reports $24.50 in earnings, the stock would likely be far higher, especially if there is optimism for even more growth ahead. A business that is more than doubling earnings with high margins and leading the artificial intelligence (AI) revolution deserves a premium valuation, probably something like double the P/E of the S&P 500.

Nvidia deserves the highest P/E of all the Magnificent Seven companies, but the company is nearing a point where it is running up too far, too fast.

Nvidia benefited from earnings growth and a valuation expansion. It’s hard to assume the valuation will continue to expand, but the stock could still go up if the first half of fiscal 2025 goes as analysts expect. Each new quarter of high earnings will increase the trailing-12-month number and lower the P/E, leaving room for the stock to rise to fill the gap. There is nothing better in the stock market than earnings growth, and right now Nvidia has it, and Apple doesn’t.

So why is Apple the better buy if Nvidia has such an easy path forward? Simply put, I think the setup for Apple makes it a much better investment. Nvidia may be the better trade, but a more surefire way of building wealth is by compounding over the long term.

Market sentiment is negative toward Apple. So negative, in fact, that Apple trades at a discount to the S&P 500. The only reason that should ever happen is if something serious was going wrong with Apple. The company has its challenges, but none of them warrant an underperformance like we have been seeing for the last six months or so.

The abridged version of why Apple stock is under pressure is because it hasn’t captured the spotlight with some major AI monetization announcement (Nvidia, Microsoft, and Meta Platforms have). iPhone sales are down in China, and growth is sluggish in general. But Apple has endured these periods before and overcome competition.

Piper Sandler‘s fall 2023 survey found that 87% of Gen Z had an iPhone, 88% expected their next phone to be an iPhone, and 34% owned an Apple Watch. The iPhone is essentially a consumer staple in the U.S. and is growing well across international markets outside of China.

Investors should focus less on the competition and more on Apple’s ability to further monetize its existing devices through services and AI. The key for Apple has always been to increase the depth (services) and breadth (more products like phones, computers, tablets, wearables, ear buds, and more) of its ecosystem. Having lifetime customers consistently increase their spending relies on product improvements.

The pressure is on Apple to make a splash this summer to drive iPhone demand and upgrades. If Apple delivers the improvements that drive growth, the stock could soar. But even if it doesn’t, it generates plenty of extra cash to make an acquisition and grow that way, or return cash to shareholders while maintaining a rock-solid balance sheet.

Apple’s brand, market position, and financial health give it the time and the wiggle room needed to make mistakes. The company is known for not leading investors on and only makes announcements when it feels the product or service is ready.

Nvidia has to hit sky-high earnings forecasts to keep going up. The semiconductor industry is also highly cyclical, and a downturn in customer spending could stall its growth trajectory. Nvidia may keep growing at a breakneck pace in the near term, but eventually, it will slow down. When that time comes, investors may be less willing to give Nvidia a multiple that is triple the market average.

Meanwhile, Apple is already a good value and has a clear path toward regaining Wall Street’s favor.

I don’t have a crystal ball, but if I had to guess, I would say Nvidia will briefly become more valuable than Apple. But three to five years from now, I think Apple will be worth more than Nvidia while also being a safer and less volatile investment.

Nvidia stands out as a high-risk/high-potential-reward play, while Apple is more like a low-risk/medium-potential-reward investment. Investors who are confident about sustained high demand for Nvidia’s products will want to watch each quarterly earnings report, understanding the importance earnings play in the story. The big gains have already been made in Nvidia, and investors should expect more reasonable returns going forward.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

When it comes to artificial intelligence (AI), applications in machine learning, large language models, and compute networking garner most of the attention. But what investors may not realize is that use cases packaged around AI are evolving in real time.

One area that is getting particular interest is robotics. Indeed, companies such as Amazon and Alibaba have implemented robotics throughout their warehouses for years, creating efficiencies as it relates to packaging and logistics.

However, a rising number of the world’s largest technology companies are increasingly focusing on the next frontier of robotics: humanoid bots. In late February, Nvidia‘s (NVDA -0.12%) CEO, Jensen Huang, said “humanoid robotics should be right around the corner” during a panel discussion about AI.

Let’s dig into the rise of humanoid robotics and analyze the moves Nvidia is making in the space.

Robotics is an interesting part of the overall AI narrative because it is uniquely positioned at the intersection of software and hardware. And believe it or not, there are lots of companies working to develop humanoid bots.

Two of the more recognized brands in robotics include Boston Dynamics and Tesla. Over the last year, Tesla has teased investors with previews of its humanoid bot Optimus — which is planned to be used across the company’s factories and assembly lines in the future.

One lesser-known robotics start-up called 1X hails from Norway. The company has raised $125 million in venture capital (VC) funding over the last year from high-profile investors including OpenAI, Samsung, and Tiger Global.

Image source: Getty Images.

About a week after Huang’s comments regarding humanoid robots, Nvidia was cited as an investor in a $675 million funding round for start-up Figure AI. Nvidia joined Microsoft, OpenAI, Intel, and Amazon co-founder Jeff Bezos as investors.

Figure AI is developing humanoid robots that it plans to commercialize in industries such as manufacturing, warehousing, and retail. Figure AI’s robots are being trained on generative AI models to learn how to perform basic tasks. The theme? The company is seeking to disrupt the workforce — a market estimated to be worth $42 trillion annually.

Nvidia has incredibly lucrative opportunities in robotics. Currently, the company is primarily a hardware player — developing high-performance semiconductors called graphics processing units (GPUs).

However, Nvidia is quietly expanding outside compute networking. Specifically, the company’s enterprise software and services business is already operating at an annual revenue run rate of $1 billion. While this is impressive, it pales in comparison to Nvidia’s data center business — which generated $47 billion in sales last year.

Moreover, Nvidia is aggressively pursuing the enterprise software market through a combination of investments and strategic partnerships. The company is an investor in start-up Databricks, which largely competes with Palantir Technologies. Additionally, Nvidia also partners with Snowflake, helping bring AI capabilities to the company’s data cloud platform.

Given Nvidia’s distinctive position as both a hardware and software developer, the company has a massive opportunity to play an integral role in the development of humanoid robotics. I see the investment in Figure AI as a first step that could lead to further strategic partnerships and revenue opportunities across both sides of its business.

The important idea here is that Nvidia is subtly building an end-to-end AI solution — spanning across both software and hardware. As such, I think the company is setting itself up for long-term sustained growth in a variety of areas in the overall AI realm.

My guess is that Huang will continue to drop breadcrumbs, alluding to AI-powered applications that he believes Nvidia can play a role in. Despite the run-up in the stock, I think now is a terrific time to scoop up some shares and plan to hold long term.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Amazon, Microsoft, Nvidia, Palantir Technologies, and Tesla. The Motley Fool has positions in and recommends Amazon, Microsoft, Nvidia, Palantir Technologies, Snowflake, and Tesla. The Motley Fool recommends Alibaba Group and Intel and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short January 2026 $405 calls on Microsoft, and short May 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

Nvidia (NVDA -0.12%) is a stock many investors have missed out on. Its unbelievable market outperformance started at the beginning of 2023 and continues well into 2024, with the stock up more than 480%.

But just because it has risen that much doesn’t necessarily mean investors have missed out; you can always buy the stock now.

Many might be concerned about shares falling due to high expectations built into it. However, I can come up with three good reasons Nvidia is a buy right now, and investors of all opinions should consider these.

Nvidia’s primary products are graphics processing units (GPUs), the hardware often tasked with complex computing, like engineering simulations or gaming graphics. But they’re also useful for data gathering and training artificial intelligence (AI) models. That makes them a key factor in the AI revolution taking the world by storm.

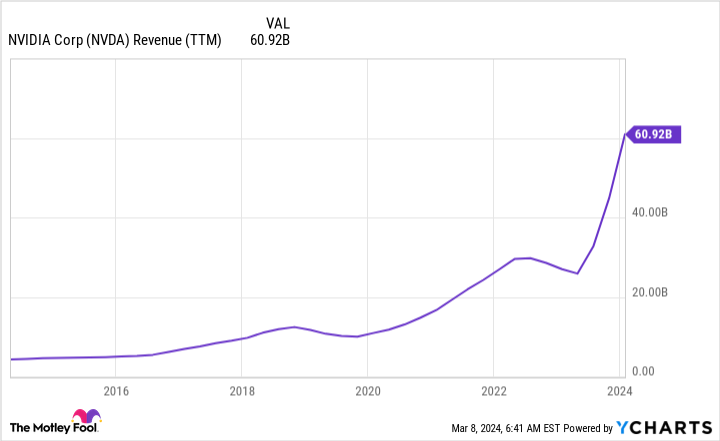

As companies rush to build data centers to increase computing capability and power these ever-improving models, Nvidia’s business has soared. In its latest quarter, Nvidia’s revenue was up 265% to $22.1 billion. This brought its revenue for the full-year 2024 (ending Jan. 28) to $60.9 billion. And many market analysts believe there is more in store for GPU production.

NVDA revenue (TTM) data by YCharts; TTM = trailing 12 months.

Precedence Research sees the GPU market expanding to $773 billion by 2032. Considering that Nvidia holds a firm grip on the GPU market, it will be the primary benefactor of this increase.

Just because Nvidia has experienced unbelievable growth doesn’t mean it’s done yet. But investors shouldn’t expect revenue to triple like it did over the past year.

AI is all the rage in the stock market, but how many people use it in their daily work? The reality is that very few people have been affected by its power. But with AI going mainstream through digital assistants, that is about to change.

GPUs will be needed to harness the power of these tools, which is another boost for Nvidia. More innovations will follow once the workforce becomes comfortable with using AI to improve productivity.

These innovations will require more computing power because previous models are being run on existing infrastructure, so GPUs will once again benefit from AI proliferation.

The last piece of the puzzle is Nvidia’s H100 GPU. This is its flagship model, but the company is working on its replacement already. The H200 GPU is expected to launch in Q2 2024, and will essentially double the computing capacity for a single GPU compared to the H100. The increase in computing power and efficiency will drive many to upgrade, which will be another boost for the chipmaker. Additionally, it keeps Nvidia ahead of the competition, further cementing its place on top of the GPU world.

We’re in the early innings of AI affecting work, and Nvidia is set to capitalize.

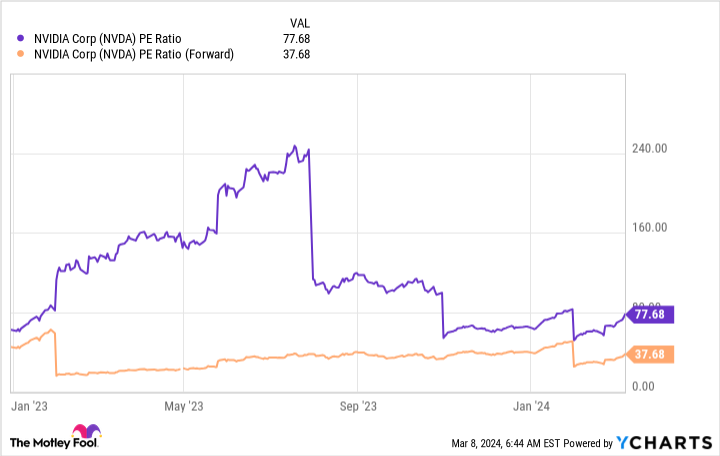

The previous two reasons don’t involve the stock; they only concern the future. However, thanks to Nvidia’s growth, the stock isn’t as expensive as it used to be.

When a company is undergoing a massive transformation, it’s useful to look at the forward price-to-earnings (P/E) ratio, which uses analyst projections. This analysis isn’t perfect, but it gives investors a better idea of where Nvidia is heading rather than looking at where it has been.

NVDA PE ratio data by YCharts.

While Nvidia’s P/E ratio has been sky-high at times, its forward earnings have hovered around reasonable levels — 38 times forward earnings is still a very expensive price tag for a stock, but it looks much more palatable than 78 times trailing earnings.

And when the world’s largest company, Microsoft, trades at 35 times forward earnings despite slower growth, Nvidia’s stock price doesn’t look all that bad.

Investors are unlikely to see the incredible growth Nvidia experienced in 2023 again, but there is still plenty of room for steady, market-beating growth, which makes it a stock that investors can confidently invest in, even now.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.