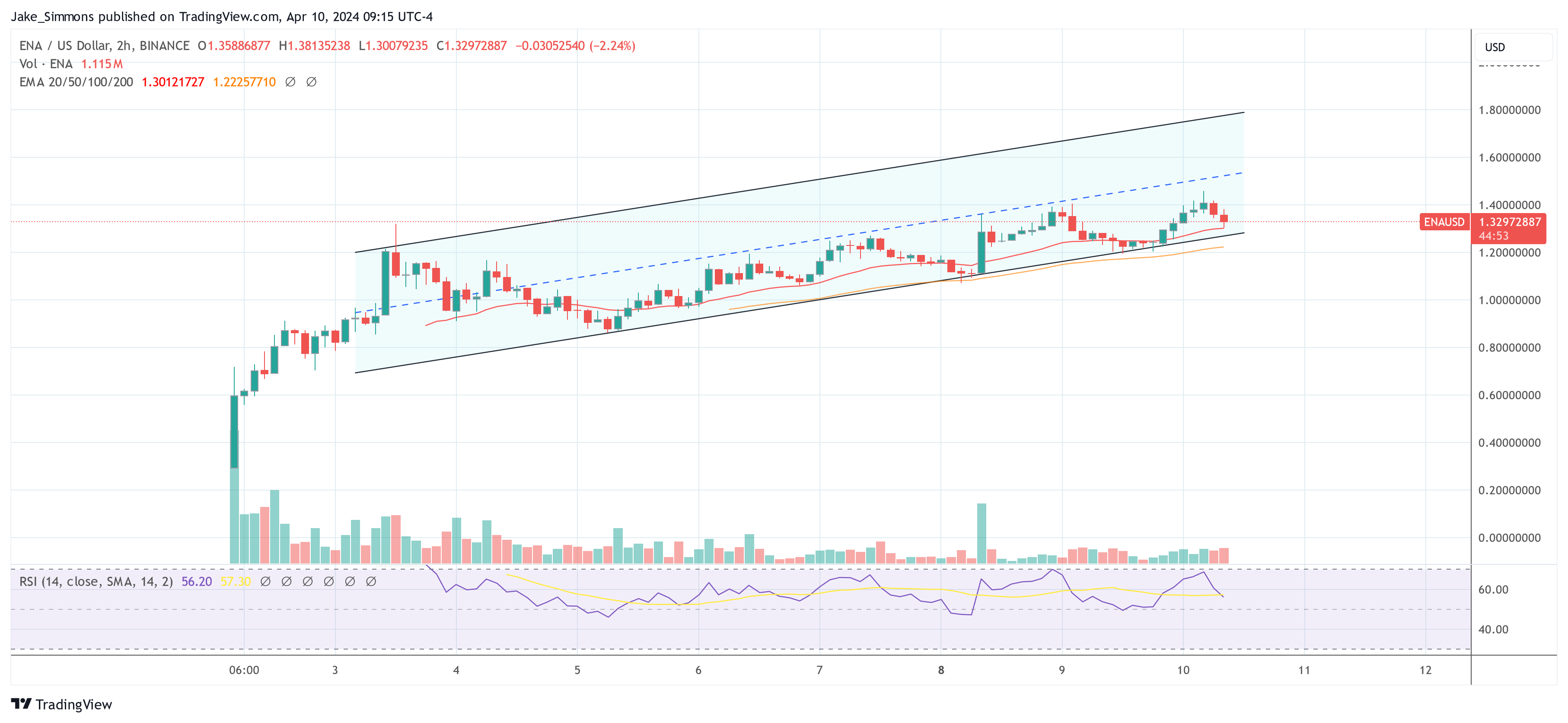

As of April 15, 2024, bitcoin presents a mixed landscape of consolidation and subtle recovery hints, reflecting a crucial moment for potential bullish or bearish trends. Bitcoin Despite the current market indecisiveness indicated by the 1-hour chart, the 4-hour and daily charts suggest underlying movements that could influence future price actions. The 1-hour chart displays […]

As of April 15, 2024, bitcoin presents a mixed landscape of consolidation and subtle recovery hints, reflecting a crucial moment for potential bullish or bearish trends. Bitcoin Despite the current market indecisiveness indicated by the 1-hour chart, the 4-hour and daily charts suggest underlying movements that could influence future price actions. The 1-hour chart displays […]

Source link

Ethereum price action in the last three months. Source:

Ethereum price action in the last three months. Source:

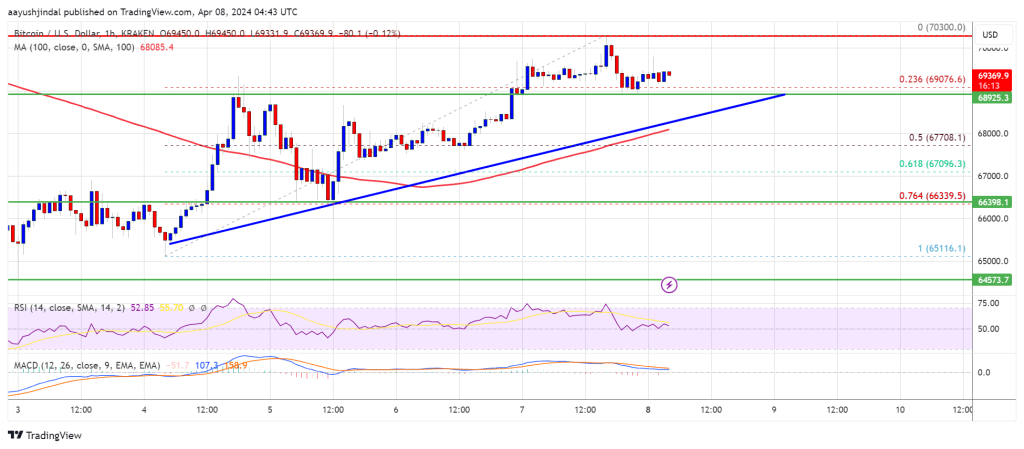

On March 29, 2024, with a trading price of $70,075, and oscillating within a 24-hour range of $68,362 to $71,754, bitcoin’s current market behavior reveals significant consolidation and neutrality. Bitcoin Bitcoin’s 1-hour chart reveals recent volatility, with a significant bounce from a low of approximately $68,362, suggesting a strong support level. Conversely, the resistance near […]

On March 29, 2024, with a trading price of $70,075, and oscillating within a 24-hour range of $68,362 to $71,754, bitcoin’s current market behavior reveals significant consolidation and neutrality. Bitcoin Bitcoin’s 1-hour chart reveals recent volatility, with a significant bounce from a low of approximately $68,362, suggesting a strong support level. Conversely, the resistance near […]

PRESS RELEASE. LBank Labs has achieved a new milestone by participating in the $3 million funding round for QED. This innovative venture is poised to revolutionize the Bitcoin ecosystem with its groundbreaking zk-Native blockchain protocol. The funding round, spearheaded by Arrington Capital, saw contributions from renowned venture capital firms such as Starkware, Draper Dragon, Blockchain […]

PRESS RELEASE. LBank Labs has achieved a new milestone by participating in the $3 million funding round for QED. This innovative venture is poised to revolutionize the Bitcoin ecosystem with its groundbreaking zk-Native blockchain protocol. The funding round, spearheaded by Arrington Capital, saw contributions from renowned venture capital firms such as Starkware, Draper Dragon, Blockchain […]