Either gold shares rise from here or gold prices take a dive.

Source link

Either gold shares rise from here or gold prices take a dive.

Source link

Telecommunications giant AT&T Inc. (NYSE:T) recently disclosed a significant data breach dating back to 2021 that resulted in the exposure of sensitive information belonging to 73 million users and is now circulating on the dark web.

The leaked data includes a wealth of personal details such as Social Security numbers, email addresses, phone numbers and dates of birth, affecting both current and former account holders. AT&T revealed that among the impacted people, 7.6 million are current account holders.

“Currently, AT&T does not have evidence of unauthorized access to its systems resulting in exfiltration of the data set. The company is communicating proactively with those impacted and will be offering credit monitoring at our expense where applicable,” AT&T said in its press release about the situation.

Don’t Miss:

The hacker behind this brazen cyberattack is ShiningHacker, a notorious figure known for previous data breaches targeting platforms such as Wattpad, Tokopedia, and Microsoft Corp.’s GitHub, according to Bleeping Computer.

Initially, AT&T denied any internal data breach when a small portion of the stolen data surfaced in 2021, claiming no knowledge of leaked information from their servers or vendors.

However, subsequent investigations revealed a different story. While AT&T refuted the claims initially, ShiningHacker admitted to the breach, dismissing AT&T’s stance with the assertion, “I don’t care if they don’t admit. I’m just selling,” according to Bleeping Computer.

The hacker attempted to monetize the stolen data by offering it for sale on the RaidForums data theft forum, setting the starting price at $200,000 and accepting incremental offers of $30,000. ShiningHacker indicated a willingness to immediately sell the data for $1 million, underscoring the severity and audacity of the cybercrime.

Trending: Long overdue disruption in the moving industry is underway. Here’s how to invest in it with just $100.

Telecommunications providers have become recent targets of cyberattacks, with T-Mobile facing a breach in 2023 affecting 37 million customers, and Verizon Communications Inc. experiencing a leak impacting 63,000 customers and employees.

In December, the Federal Communications Commission (FCC) adopted a new role to ensure that “providers of telecommunications, interconnected voice over internet protocol (VoIP) and telecommunications relay services (TRS) adequately safeguard sensitive customer information.”

The same ruling expanded the definition of “breach” in this context, to include inadvertent access, use or disclosure of customer information, except in cases where such information is acquired in good faith by an employee or agent of a carrier or TRS provider and such information is not used improperly or further disclosed.

Read About Startup Investing:

“ACTIVE INVESTORS’ SECRET WEAPON” Supercharge Your Stock Market Game with the #1 “news & everything else” trading tool: Benzinga Pro – Click here to start Your 14-Day Trial Now!

Get the latest stock analysis from Benzinga?

This article 73 Million AT&T Users’ Data Leaked As Hacker Said, ‘I Don’t Care If They Don’t Admit. I’m Just Selling’ Auctioned At Starting Price Of $200K originally appeared on Benzinga.com

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Veteran trader and renowned chartist Peter Brandt has doubled down on his bullish outlook for bitcoin. After raising his bitcoin price target for this bull market cycle to $200K, Brandt pointed to “huge monthly bars” on his bitcoin price chart, stating: “My bet is that this is a ‘starting’ candle.” Peter Brandt’s Bitcoin Bull Run […]

Veteran trader and renowned chartist Peter Brandt has doubled down on his bullish outlook for bitcoin. After raising his bitcoin price target for this bull market cycle to $200K, Brandt pointed to “huge monthly bars” on his bitcoin price chart, stating: “My bet is that this is a ‘starting’ candle.” Peter Brandt’s Bitcoin Bull Run […]

Source link

The new year is a great time for younger workers to set themselves up for future financial security — even those who are still decades away from retirement. In fact, the sooner they start, the better.

Now’s the perfect time for even entry-level workers just starting out in their careers to develop new rituals to save for retirement, as well as any other long-term goals. And sticking to these habits early and often can amass a small fortune, even upwards of a million or more dollars.

Take, for example, a 25-year-old worker in a new job earning a $50,000 salary. If she contributed $400 a month (or 10% of her salary) into a retirement account, then she could have more than $1.1 million saved by age 67 (her Full Retirement Age, according to the Social Security Administration), assuming a 6% rate of return and consistent contributions. And even if that same person could only contribute half that amount, or $200 a month, then she’d still have more than half a million put away for the future by 67, assuming the same factors.

Changing any of the factors will affect the outcome, of course, which is to be expected in the decades leading up to retirement. Oftentimes, savers may find they have to adjust what they contribute — some years saving more, other years less. Market volatility will affect the performance of a portfolio from year to year, as well.

Still, there are a few strategies young Americans can employ to prepare themselves for a more comfortable retirement. Here are a few tasks to try in 2024 to set yourself up for success:

Meet the employer match

Financial advisers typically suggest saving somewhere between 10%-15% of a worker’s salary for long-term goals, such as retirement, but that isn’t always feasible. If it’s not, then start where you can. For employees of companies that offer a retirement account with an employer match, aim to contribute at least up to the match amount to take advantage of that extra money. If that’s not possible, then make meeting that match a short-term goal. Contribute however much you can, to start, and prioritize increasing the contribution to meet the match as soon as you can (and then going beyond that eventually).

One strategy with financial and non-financial goals alike is to use SMART goals, which stand for specific, measurable, achievable, relevant and time-bound goals. Using this approach may make meeting goals, like increasing retirement plan contributions, feel more attainable.

Automate your savings

Workers can automate their savings in their 401(k) plan through payroll deduction, but savers can also use the same tactic outside of the employer-sponsored retirement account. Try setting up automatic contributions to various savings accounts, or investment accounts like an IRA, through your bank. Many financial institutions work together for automatic transfers, as well, if your checking, savings or investment accounts are housed at different firms.

For many retirement plans, workers can also set up automatic increases in their contributions. They can pick one time of the year to do that, such as on their work anniversary, a birthday, a holiday or when they typically expect to get an annual raise.

Understand your asset allocation

The new year is a good time to review retirement accounts’ asset allocation, which is how the portfolio is invested. Many young workers are advised to invest aggressively, since they have decades for their money to grow and rebound from market downturns. Regardless of the strategy that workers choose, it is important to regularly check retirement plans (such as once every six months, or quarterly, perhaps) to see that their portfolio is still invested accordingly, or if it has shifted because of market movement.

Open a Roth account

Roth accounts are invested with after-tax dollars, as opposed to traditional IRAs or 401(k) plans, which use pre-tax contributions. Roth accounts can be powerful tools for members of younger generations who are likely in low tax brackets. If they expect to be in higher tax brackets in the future, the Roth account basically provides a discount on taxes — investors pay the taxes on the contributions up front, and then can withdraw the money later with no tax bill.

Roth accounts have specific distribution rules. For example, investors must have had the account open for five years and be 59 ½ years old to avoid paying any taxes or penalties on their withdrawals. But the principal (which is what investors contributed) — not the earnings — are always available for distribution tax- and penalty-free. There are exceptions, such as an allowance of up to $10,000 from a Roth IRA for a first-time home purchase, where investors may be subject to taxes but not penalty.

Shares of Apple Inc. dropped Monday, after the Wall Street Journal reported the technology giant would halt some Apple Watch sales in a preemptive move to comply with a U.S. import ban regarding the use of blood-oxygen sensors.

The company

AAPL,

confirmed to CNN it will no longer be selling its Apple Watch Series 9 and Apple Watch Ultra 2, starting Thursday on Apple.com and from retail locations after Dec. 24.

“While the review period will not end until December 25, Apple is preemptively taking steps to comply should the ruling stand,” the company said in a statement, according to the report. “Apple strongly disagrees with the order and is pursuing a range of legal and technical options to ensure that Apple Watch is available to customers.”

If the order stands, Apple said it will “continue to take all measures to return Apple Watch Series 9 and Apple Watch Ultra 2 to customers in the U.S. as soon as possible.”

The ban, which would include the Apple Watch Series 9 and Apple Watch Ultra 2, comes after the U.S. International Trade Commission found that Apple violated patents in most new models of its smartwatches since 2020, the WSJ report said.

Apple’s stock fell 0.85% in trading Monday, to buck the rallies in the technology sector

XLK

and the broader stock market.

SPX

The stock’s decline snapped a seven-week win streak in which it has soared 17.4%, and included a record close of $198.11 on Dec. 14.

Apple said it believes the ITC’s findings are inaccurate and should be reversed. It said it plans to take the decision to the Federal Circuit.

The commission had found in October that Apple violated medical-technology company Masimo Corp.’s

MASI,

patents related to measuring blood-oxygen levels. That led the commission to issue an order to ban the import of certain Apple Watches.

The Biden administration has 60 days to overrule the Trade Commission’s order.

Masimo shares rallied 5.5% in afternoon trading Monday.

While Apple didn’t provide data on Apple Watch sales in its latest earnings report, it did say wearables, home and accessories revenue came in at $9.3 billion during the fiscal fourth-quarter ended Sept. 30.

The device, which initially struggled to gain an identity of its own in a product line bejeweled with iPhone, iPad and Mac products, is now among Apple’s hottest-selling products. Its growing popularity in great measure is as a safe, easy-to-monitor proxy for iPhone. As a result, Apple is pushing its nearly decade-old product as never before.

Read more: The Apple Watch may now be a back-to-school necessity

Apple’s stock, which has eased 1% since closing at a record $198.11 on Dec. 14, has run up 50.8% year to date while the Nasdaq Composite

COMP,

has rallied 42.4% and the Dow Jones Industrial Average

DJIA,

has gained 12.6%.

On-chain data shows the Bitcoin SOPR hasn’t yet reached high levels that have been associated with heated bull market phases in the past.

In a CryptoQuant Quicktake post, an analyst has explained how market psychology has driven the BTC price during the past few years. The on-chain indicator that best represents the Bitcoin trader psychology according to the quant is the “Spent Output Profit Ratio” (SOPR).

The SOPR basically tells us about whether the BTC investors are selling their coins (or more precisely, transferring them on the blockchain) at a net amount of profit or loss.

When the indicator has a value greater than 1, it means that the average holder in the sector is selling their coins at some profit right now. On the other hand, a value under this threshold implies that loss-selling is dominant among the participants.

Naturally, when the SOPR has a value exactly equal to 1, the overall market can be assumed to be just breaking even on their selling, as the number of profits being realized is exactly canceling out the losses.

Now, here is a chart that shows the trend in the Bitcoin SOPR over the past few years:

Looks like the value of the metric has been slightly positive in recent weeks | Source: CryptoQuant

In the above graph, the analyst has marked the pattern that the Bitcoin SOPR has followed in recent years. During the 2018 bear market, the BTC SOPR dropped to pretty low values below 1 following the November 2018 crash. Coinciding with these lows in the metric, the price also found its bottom.

In the 2022 bear market, the BTC investors were keeping still in the red as they participated in only a relatively low amount of loss selling until the FTX crash occurred and the holders finally capitulated to a significant degree.

So far, it would appear that the low after the FTX collapse was indeed the bottom for the current cycle, as BTC has only gone and doubled in value since then. The pattern of this bottom has also been consistent with the one of the 2018 bear market.

In between these two major bottoms, there was also a large-scale capitulation event back in 2020, but this crash was mostly an anomaly caused by the unexpected emergence of the COVID-19 pandemic.

From the chart, it’s visible that the trend during rallies has generally been just the opposite: investors start selling at large profits and once the profit-taking attains extreme levels, the top is hit.

Earlier this year, the BTC SOPR spiked to high levels around when BTC hit its local top in April. Since then, though, the indicator has remained relatively calm, with some mild profit-taking coming after the latest leg in the rally.

“There will be many corrections and declines in the current market until it reaches the peak of the bull market, but from a psychological perspective, there still seems to be enough time left until the latter half of the bull market,” thinks the quant.

Bitcoin had registered a decline below the $37,000 level during the past day, but the asset has pulled itself back up since then as it’s just floating above the mark now.

The price of the asset appears to have seen some drawdown recently | Source: BTCUSD on TradingView

Featured image from Shutterstock.com, charts from TradingView.com, CryptoQuant.com

According to on-chain analytics, the next strong Dogecoin rally might be closer than we think. The meme token has been giving traders mixed signals for the past month, but signs like on-chain transaction volume and DOGE’s mission to the moon are starting to point to the next surge being right around the corner.

Despite the majority of cryptocurrencies being in the red over the past 24 hours as consolidation and modest selloffs continue, Doge has managed to post a gain of 6.87%.

Price activity indicates that Dogecoin has gained more than 10% over the course of the past week. The cryptocurrency struggled to post gains like other popular cryptocurrencies for the most part of October’s rally.

Price data from Coinmarketcap shows the crypto only spiked 19.7% from its October bottom of $0.0579 to end the month at $0.069. However, things changed in early November, as bulls and whales started to inject capital into the cryptocurrency. This influx pushed the cryptocurrency over the strong $0.76 support.

According to crypto analyst Rekt Capital, this breakout was the beginning of a shift in trend, with a spike to a $0.15 price target now in formation.

Various on-chain monitors reveal that on-chain transactions have spiked at the same time. According to on-chain analytics platform Santiment, Dogecoin reached a total transaction volume of $665 million yesterday, its highest level in three months. Data from Coinmarketcap also puts the total transaction volume in the past 24 hours at $1.83 billion, an increase of over 240% from the previous day.

🐶 #Dogecoin has had a modest +5% surge on a mostly flat #crypto market day. It has been aided by $665M in #onchain transaction volume, its highest level in 3 months. There is also a notable amount of $DOGE longs opening as traders bet on prices rising. pic.twitter.com/DussxIPJN2

— Santiment (@santimentfeed) November 16, 2023

Dogecoin millionaires figures are currently in decline, but that has not stopped whale activities as large transactions have spiked in the past week amid greater market pullback. IntoTheBlock’s large on-chain transaction metric shows that DOGE’s large on-chain transactions totaled $1.37 billion in the past 24 hours, a 69% increase from the prior day.

Source: IntoTheBlock

Most of this heightened trading activity can be linked to increasing enthusiasm within the Dogecoin community surrounding robotics company Astrobotic’s launch of a physical Dogecoin token to the moon in December. For a token whose price is mostly driven largely by hype and excitement, the anticipation and achievement of this Moon mission could very well start a sustained upward trend for Dogecoin.

Popular trading platform Robinhood has also been a major factor in this uptick in large transaction volume. A series of large-scale transactions linked to Robinhood started on November 7, when it received a transfer of 250 million DOGE, worth approximately $18.9 million at the time. Other notable transfers include a transfer of $10.6 million worth of DOGE from Robinhood to an unknown wallet and a transfer of 690 million DOGE between two private wallets.

According to whale transaction tracker Whale Alerts, 375 million DOGE worth approximately $30.3 million was recently transferred to Robinhood.

🚨 🚨 375,000,000 #DOGE (30,335,217 USD) transferred from unknown wallet to #Robinhood

— Whale Alert (@whale_alert) November 17, 2023

DOGE bulls take control | Source: DOGEUSD on Tradingview.com

Featured image from CNET, chart from Tradingview.com

There are a handful of signals that point to the strong US consumer finally slowing down.

Macquarie strategist Thierry Wizman, foresees the US economy slipping into a consumer-led slowdown.

He said a downturn could hit sometime between now and the end of the first quarter of 2024.

American consumers are finally showing signs of slowing as they blow through their savings, and there are a handful of warning signs that the economy could soon tip into a spending recession.

Thierry Wizman, a strategist at Macquarie Global, foresees the US economy slipping into a consumer-led slowdown sometime between now and the end of the first quarter in 2024. A major pullback in consumer spending could force GDP growth to grind to halt, he told Insider, pushing the overall economy into borderline recession territory.

Wizman’s downbeat forecast is counter to what other commentators have said, as consumers have kept up their spending spree over the third quarter in a row this year. Retail sales, jumped 0.7% during the month of September, more than double what economists were expecting.

But the resilient spending is itself the problem: spending has been so strong, it’s bound to whiplash in the other direction as savings run dry and Americans financial situations change, Wizman said.

“There were reasons why Q3 was very strong. Getting through all the revenge travel … the concert tours,” Wizman said. “The problem, of course, is that it’s usually followed by a hangover.”

“Like all hangovers, this one will happen soon after the binge,” he added in a note this week.

The economy is now flashing a handful of warning signs that the US consumer is running out of steam. Here are five signals of weakness that point to a spending recession on the way.

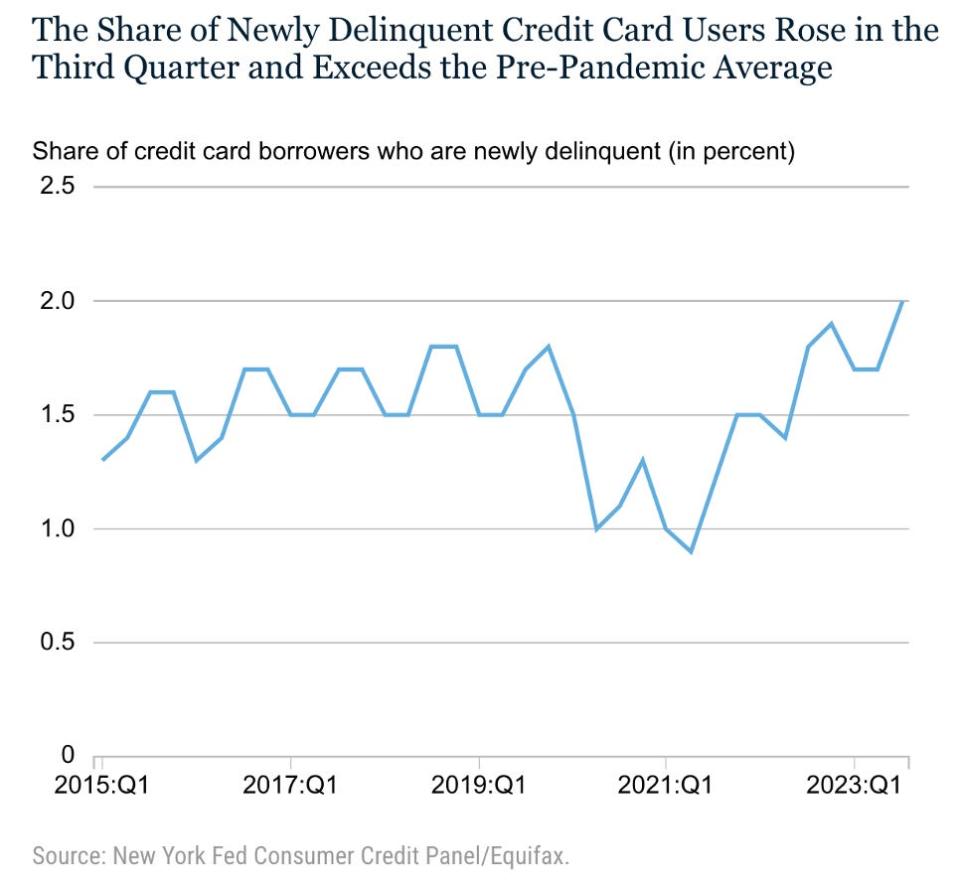

Credit card holders that became newly delinquent rose to 2% the last quarter, about double the rate recorded in the first quarter of 2021. Meanwhile, Americans who were seriously late in paying their credit card balances – by at least 90 days – rose to nearly 6% the last quarter, according to the New York Fed’s latest Household Debt and Credit report.

Credit card delinquencies also saw a particularly high jump for those who already had auto and student loan debt, the report added. That’s a sign financial stress is growing, Wizman said, which is likely to lead people to pull back on spending.

The personal savings rate slumped further last month. Americans saved an average 3.4% of their disposable personal income in September, down from 4% in August, according to the Bureau of Economic Analysis. That’s well-below the pre-pandemic savings rate, when Americans were stashing away around 7% of their disposable personal income.

“That’s actually very, very low compared to historic norms,” Wizman said of the current savings rate. “So there has to be at some point an adjustment.”

Consumers have also drawn down much of their savings from the pandemic. Excess savings were likely depleted at the end of last quarter, according to a study from the San Francisco Fed.

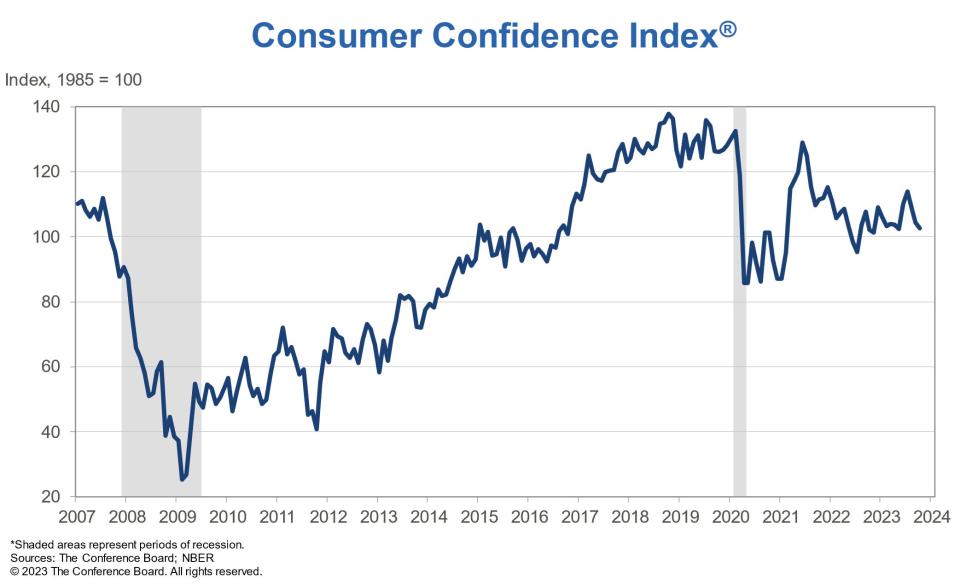

Consumer confidence slipped to 102.6 in October, down from a reading of 104.3 the prior month, according to the Conference Board. That marks the third month in a row that consumers’ attitudes have soured, based on factors like inflation, stock prices, and interest rates.

Meanwhile, the Conference Board’s Expectations Index, which reflects consumers’ short-term economic outlooks, slipped to 75.6 in October. It remains slightly below a key threshold of 80, which has traditionally signaled a recession coming within the next 12 months.

“Consumer fears of an impending recession remain elevated, consistent with the short and shallow economic contraction we anticipate for the first half of 2024,” the Conference Board said in a statement.

Americans are looking less likely to splurge, even as they head into the holiday season. A McKinsey survey of 1,000 US consumers found that just 35% say they plan to spend big this year, lower than the 39% of people who said they were willing to splurge ahead of the holidays in 2022.

A separate Morgan Stanley survey found that 69% of people are waiting for retailers to offer discounts before they start shopping. On average, consumers are looking for a discount of around 30%, strategists said.

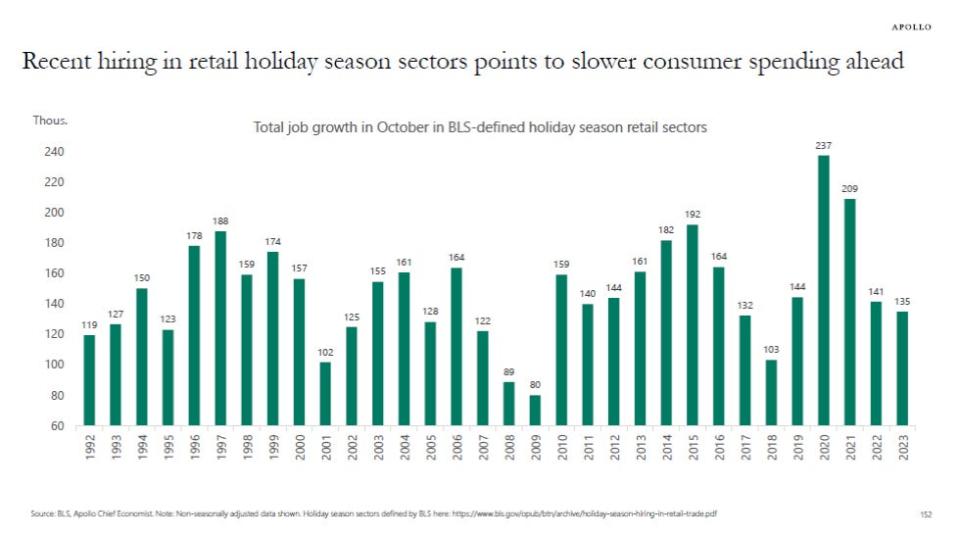

Holiday hiring among retailers slumped to 135,000, the lowest level in about five years, according to data from the Bureau of Labor Statistics.

“Hiring for the holiday season is generally done in October, and adding up new jobs created in the BLS-defined holiday season retail sectors in the latest employment report shows that retailers expect a weaker holiday season,” Apollo chief economist Torsten Slok said in a note on Tuesday.

Read the original article on Business Insider

There’s one group of Americans that’s missing from the picture of this year’s strong consumer spending: families that pay for childcare.

Since May, spending by households that pay for childcare has lagged behind the rest of the population, according to a new report by the Bank of America Institute

BAC,

Not only have they been curbing their spending more than others, but they also are dipping into their savings more, the report found.

Though the difference in spending is “fairly modest,” it “could point to the increasing financial pressure that families with young children face,” the report’s authors said.

Nationally, families spent an average of more than $700 a month on childcare in September, according to Bank of America, a 32% increase since 2019. San Francisco and Seattle had the highest average childcare costs in September, nearly twice as much as the national average, the report found.

Average childcare costs per household have jumped the most for higher-income families, with annual incomes of $100,000 to $250,000, the report found. Those households may be experiencing bigger cost increases for childcare in part because they can afford to pay more for it, while lower-income families are more likely to cut out childcare when prices go up, said Anna Zhou, an economist at the Bank of America Institute and author of the report.

A growing number of higher-income households started using childcare in 2022 following a small baby boom that was largely concentrated among women with college degrees, who tend to have better finances, Zhou said. Overall, the level of households paying for childcare services ticked up slightly from 2019 to 2022, the report said.

Some cities have seen average childcare expenses rise at a faster rate than the national average. Tampa, Fla., had the fastest growth in childcare expenses in September; the pace was 12% faster than the national level. Atlanta, Orlando, Dallas and Seattle followed.

Consumer spending continued to be strong in September, although some economists have warned that it might not be sustainable because of how much consumers have been relying on their savings to spend.

Across income groups ranging from $50,000 to $250,000 a year, families that pay for childcare saw a deeper year-over-year drawdown of their savings in September compared with other households, the Bank of America report found.

However, many parents and families still have some financial breathing room because their cash savings amount is 30% higher in 2023 than it was in 2019, according to Bank of America internal data, Zhou told MarketWatch. Those who do not pay for childcare have more money in their bank accounts, she continued.

“For now, [parents] are fine because they still have money to draw on,” Zhou said. “But if this continues for the foreseeable future, it could impact these families and the overall consumer spending in a more significant way.”

While American families saw a boost in their wealth overall during the pandemic, couples with children on average saw slower growth to their net worth, according to the Federal Reserve. Couples without kids on average had a net worth of $398,960 in 2022, up 37% from their 2019 level. That is compared with couples with at least one kid having $291,770 in 2022, up 34% from their 2019 level.

Bank of America researchers said there’s evidence that parents could be leaving the workforce because of rising childcare costs. The average number of payrolls deposited into Bank of America accounts for households that pay for childcare was 1.34 payrolls a month, slightly lower than in 2019, when it was 1.39 payrolls per month, the study found.

Some $24 billion in pandemic-era government funding for childcare expired Sept 30, setting the stage for childcare prices to become more expensive because of the surging operating costs for providers. In some states such as Pennsylvania, Wisconsin and North Carolina, childcare centers and programs have closed down, and some have had to raise prices. The Biden administration asked Congress last week for an additional $16 billion to reverse what some experts called “the childcare cliff,” but it’s uncertain how a Republican-led House will decide on it.

PayPal stated in an email to select users on Aug. 14 that it will temporarily pause crypto buying services in the U.K. in the coming months.

That message states that the service will be paused starting on Oct. 1, 2023, and will resume at an unspecified date in early 2024.

Though buying will be unavailable, PayPal said that users will be able to hold and sell their cryptocurrency during the service disruption. The company did not state whether users will be able to transfer cryptocurrency to other wallets and exchanges, though it appears that this feature is only available to users in the U.S. at present.

The company assured users their crypto remains safe and said holding will not incur a charge. It apologized for the inconvenience to customers.

PayPal said it is pausing crypto purchases due to introducing new rules from the U.K. Financial Conduct Authority (FCA). It said that those rules will require it to “implement additional steps before customers can purchase crypto.”

The company did not specify which rules are concerned. The U.K. will begin to enforce a Crypto Travel Rule in September 2023 that requires crypto companies to collect information about parties involved in transactions, though this rule’s September deadline does not seem to line up with PayPal’s October service change.

The FCA also recently introduced new promotional rules that aim to control how crypto can be promoted or advertised to potential investors. These rules come into effect in October but do not seem to match PayPal’s description of user-focused requirements.

PayPal’s reduced U.K. services are particularly notable due to the fact that the company is expanding its crypto offerings in the United States.

The company said that it would offer its own USD stablecoin on Aug. 7. Later, one PayPal executive suggested that the stablecoin could see extensive use in DeFi. Other reports suggest the company is combining its features into a “Cryptocurrency Hub.”

The post PayPal to pause UK crypto purchases starting in October appeared first on CryptoSlate.