Shares of Fisker Inc. dropped nearly 40% in the extended session Wednesday after a report said the embattled EV maker is exploring a bankruptcy filing.

Source link

Shares of Fisker Inc. dropped nearly 40% in the extended session Wednesday after a report said the embattled EV maker is exploring a bankruptcy filing.

Source link

Fool.com contributor Parkev Tatevosian evaluates SkyWater Technologies (SKYT -4.69%) stock and lets you know whether investors should buy.

*Stock prices used were the afternoon prices of March 10, 2024. The video was published on March 12, 2024.

Parkev Tatevosian, CFA has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. Parkev Tatevosian is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through his link, he will earn some extra money that supports his channel. His opinions remain his own and are unaffected by The Motley Fool.

Rivian Automotive (RIVN -2.52%) stock has bounced off a recent low, but the electric vehicle (EV) maker’s shares are still down by more than 45% this year. That’s because investors see several signs that EV demand has slowed. The big blow to Rivian stock came after the company released its outlook for 2024.

Management said it plans to produce just 57,000 EVs, or about the same number of units it made in 2023. That’s not what investors wanted to hear from what they considered a growth investment. But two weeks after that announcement, Rivian shocked the market with several news items, including a new plan that would save it more than $2 billion. Now investors want to know if Rivian stock is a bargain after its decline.

The latest news from Rivian came at a launch event on March 7 for its R2 next-generation EV platform. As expected, management unveiled its new mid-size SUV that it previously said would be a lower-priced option thanks to new efficiencies from the R2 design platform.

The new R2 SUV will also be priced about $30,000 lower than Rivian’s R1S. The $45,000 base price should bring in more potential customers. It also will have a battery range of over 300 miles and will accelerate from zero to 60 miles per hour in under three seconds. Shipments are expected to begin in early 2026.

The new R2 SUV will have a starting price of $45,000. Image source: Rivian Automotive.

But two additional announcements shocked investors and sent Rivian’s stock higher. Rivian introduced a crossover SUV model dubbed R3 that will follow production of the R2. That should give investors confidence that Rivian has a concrete plan to expand its potential market. Thus far, the company could only cater to wealthy consumers looking for luxury-level trucks and SUVs.

The other factor driving Rivian shares off recent lows was the company’s new strategy to initially produce the R2 from its existing Normal, Illinois facility. Previously it said those vehicles would come from its future Georgia plant. Pausing construction in Georgia will save the company more than $2.25 billion, it noted. In a press release, the company said, “The savings are expected to come from capital expenditures, product development investment, and supplier sourcing opportunities.”

Rivian ended the fourth quarter of 2023 with more than $9 billion in cash and equivalents on its balance sheet. But the company used more than $5 billion in growth capital last year and was expected to need about the same for 2024.

Saving nearly half of those capital expenditures puts a much different perspective on its financial picture. One of the biggest risks investors needed to consider when buying Rivian stock was the potential that it would run out of money before it could scale up its vehicle sales with its lower-priced models. That put the potential of a new capital raise or even bankruptcy as key investment risks.

While Rivian still needs to execute on its plan and attract buyers for its new products, that key risk has been meaningfully lowered. If it successfully does those things, the stock will look like a bargain at recent prices.

Howard Smith has positions in Rivian Automotive. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Super Micro Computer (NASDAQ: SMCI), also known as Supermicro, has become a fan-favorite for artificial intelligence (AI) investors over the past year or so. Since Jan. 2023, the stock has surged 1,290%.

The company supplies high-end, energy-efficient servers designed to enable high-performance computing, hyperscale data centers, and AI. The advent of generative AI has resulted in accelerating demand as businesses race to profit from this paradigm shift. This, in turn, has translated into surging financial results and a skyrocketing share price for Supermicro.

Now that the stage is set, let’s look at four reasons to buy Supermicro stock like there’s no tomorrow.

Supermicro has long been a key player in the server market, but its growth over the past year has been unprecedented.

A quick review of Supermicro’s recent results paints a compelling picture. For the company’s fiscal 2024 second quarter (ended Dec. 31), it generated record revenue that soared 103% year over year to $3.7 billion. At the same time, diluted earnings per share (EPS) surged 85% to $5.10.

If that weren’t enough, management suggests demand will continue to accelerate. Supermicro is guiding for third-quarter revenue of $3.9 billion at the midpoint of its outlook, which would represent year-over-year growth of 205% — and that could end up being conservative if history is any guide.

The advent of AI sparked the beginning of a massive data center upgrade cycle. Existing data center servers aren’t equipped with the computational horsepower necessary to withstand the rigors of AI. Fearing they will be left behind, data center operators are spending at a breakneck pace to increase the capabilities of their operations.

Estimates suggest this will result in more than $1 trillion in upgrades over the next several years. As one of the leading providers of AI-centric servers, Supermicro is well positioned to ride these secular tailwinds higher.

Furthermore, Bank of America analyst Ruplu Bhattacharya suggests that demand for AI servers will be much greater in the coming years than many believe. He believes this demand will grow at a compound annual rate of 50% over the next three years, while Supermicro’s revenue could “grow even faster.”

Even as overall demand for AI-centric servers is increasing, Supermicro is stealing share from the incumbents. Late last year, Barclays analyst George Wang noted that Supermicro’s “superior design capability and strong AI partnerships” would help drive market share gains. “[Supermicro] has 7% market share globally, implying further share gains ahead are likely,” Wang said. He further suggested the company is taking share from larger competitors, including Dell Technologies and Hewlett Packard Enterprise.

Rosenblatt analyst Hans Mosesmann sees that trend accelerating too. “We expect Supermicro to achieve significant market share gains, potentially reaching double digits in the next few years from its current mid-single digits with a special emphasis on enterprise solutions,” he wrote in a note to clients.

Excitement about the potential represented by AI has investors flocking to AI stocks, which has driven valuations on many popular companies higher than they’ve been in years. Supermicro hasn’t been immune to this phenomenon, but the stock is still surprisingly cheap.

The stock is currently selling for about 3 times next year’s sales (fiscal 2025). While that looks relatively inexpensive, even that figure doesn’t take into account the company’s surging profits. Using the price/earnings-to-growth (PEG) ratio shows a valuation of less than 1 — the standard for an undervalued stock.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 11, 2024

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Danny Vena has positions in Super Micro Computer. The Motley Fool has positions in and recommends Bank of America. The Motley Fool recommends Barclays Plc. The Motley Fool has a disclosure policy.

4 Reasons to Buy Super Micro Computer Stock Like There’s No Tomorrow was originally published by The Motley Fool

Fool.com contributor Parkev Tatevosian reviews Fisker‘s (FSR -9.12%) challenges in gaining market share in the EV industry.

*Stock prices used were the afternoon prices of March 8, 2024. The video was published on March 10, 2024.

Parkev Tatevosian, CFA has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Parkev Tatevosian is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through his link, he will earn some extra money that supports his channel. His opinions remain his own and are unaffected by The Motley Fool.

We are in an artificial intelligence (AI) boom or perhaps an AI bubble. Maybe a bit of both. Either way, any stock considered a beneficiary of AI spending by companies and governments is soaring, like Nvidia or Super Micro Computer, for example. Analysts are predicting the world will spend hundreds of billions on AI tools in a few years, maybe even a trillion dollars or more if you believe the most optimistic analysts.

One stock considered an AI winner is Palantir (PLTR -2.65%). The software-analytics provider for the U.S. military, its allies, and commercial customers has seen its stock soar 300% since the beginning of 2023. The Nasdaq 100 — which is currently in one of its best bull runs ever — is up 65% over the same time frame.

Retail investors love Palantir and are extremely optimistic about its prospects. As one of the largest technology-growth stocks to go public in the last few years, many are even calling it the next “Magnificent Seven” stock ready to reach a market cap of $1 trillion. Can Palantir join the $1 trillion market-cap club with the rest of the Magnificent Seven? Let’s run through the numbers and find out.

With its name inspired by a crystal ball in the fantasy tale The Lord of The Rings, Palantir aims to be the software and AI “crystal ball” for the U.S. military and its allies. Its software programs give insights for divisions of the military from mundane back-office tasks to the actual battlefield. The U.S. military alone has a budget of $877 billion, meaning there is plenty of money to go to new-age software providers such as Palantir. In fact, Palantir’s government revenue was over $1.22 billion in 2023.

Now, Palantir is taking the next step with its software with Palantir AIP, a new suite of AI tools that leverage the breakthroughs we’ve seen in large language models. I’m not going to pretend to understand exactly how all these AI tools work, but in his annual letter to shareholders, founder Alex Karp said that the entire Palantir organization is focused on AI development and that the new products are already leading to momentum in revenue and customer wins. Investors should expect this to show up on the income statement over the next few years and beyond.

Being a preferred provider for the U.S. government is lucrative, but Palantir’s work goes beyond just public-sector applications. It has a rapidly growing commercial segment as companies around the globe aim to have custom-software analytics and AI tools built by Palantir. The proof is in the pudding, with Palantir’s U.S. commercial revenue hitting $457 million in 2023, a tenfold increase from $47 million in 2019. In 2024, management is expecting the segment to reach $640 million in revenue.

Large enterprises ranging from Merck to Morgan Stanley are customers of Palantir. These companies have huge budgets, with more and more going to Palantir each year. There’s no reason for this growth to stop anytime soon.

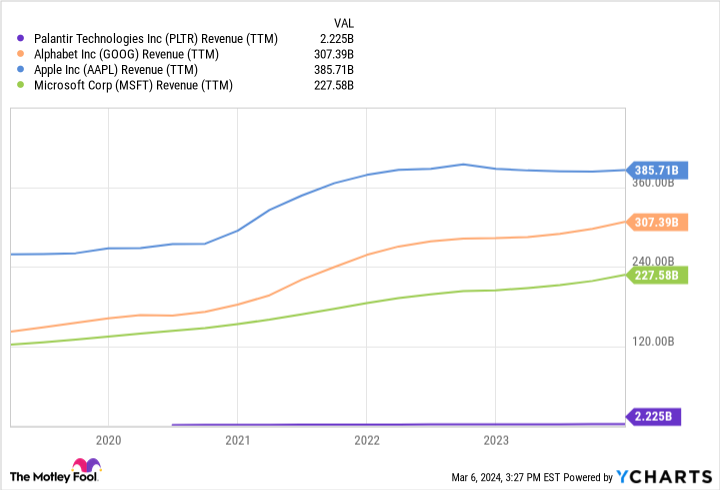

PLTR Revenue (TTM) data by YCharts.

It is hard to argue Palantir isn’t a great business with a bright future. But any investor claiming this is the next company to reach a trillion-dollar market cap is way too optimistic. Frankly, the company is just not big enough compared to the technology giants of today.

Microsoft generates $228 billion in revenue. Alphabet‘s is over $300 billion. Apple’s is close to $400 billion. And Palantir’s? Just $2.2 billion. So even if Palantir’s revenue goes up tenfold, it will still have just 10% of the sales as the technology giants. And Palantir’s revenue will not multiply 10 times for a long, long time. When you lay out the numbers and forget the bull market narratives, it is clear that Palantir is nowhere near ready to join the trillion-dollar market-cap club. Perhaps in two decades. But not anytime soon.

Investors shouldn’t be asking whether Palantir will be the next Magnificent Seven stock. They should be asking whether Palantir can still provide solid returns to investors after running up 300% since the beginning of 2023. At a market cap of $55 billion with just $2.2 billion in revenue and minimal profits, the growth expectations for Palantir are high. Quite high. But perhaps it will surpass them.

This is a risky stock to buy right now but one that has proven the doubters wrong time and time again.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Brett Schafer has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Apple, Microsoft, Nvidia, and Palantir Technologies. The Motley Fool recommends Super Micro Computer and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Cathie Wood is the chief investment officer at Ark Invest, an asset management company that runs thematic index funds focused on disruptive technologies like artificial intelligence. Wood and her team currently manage a $13.5 billion portfolio, 3.1% of which is invested in Zoom Video Communications (NASDAQ: ZM).

Ark published a valuation model for Zoom in 2022 that outlined three possible trajectories the stock could follow through 2026. The base-case scenario, or the most optimistic plausible trajectory, posited a per-share price of $1,500, which now implies about 2,170% from the current price of $66 per share in the next two years. The odds of that happening, I think, are virtually zero, but Zoom still warrants closer consideration.

Here’s what investors should know.

Zoom shares jumped on better-than-expected financial results in the fourth quarter, though growth continued to slow throughout fiscal 2024 (ended Jan. 31, 2024). Full-year revenue rose 3.1% to $4.5 billion, down from 7% growth one year ago and 55% two years ago. However, non-GAAP net income jumped 19% to $5.21 per diluted share due to disciplined expense management.

The investment thesis for Zoom centers on its ability to simplify communications. The company is best known as the market leader in videoconferencing software (Zoom Meetings), but its platform also includes phone system, contact center, and team chat applications. Businesses can often reduce cost and complexity by consolidating their communications tools through a single vendor.

Zoom also has monetization opportunities with adjacent artificial intelligence (AI) products. Specifically, its portfolio includes virtual agent technology that automates customer service interactions in Zoom Contact Center, and conversational intelligence software that analyzes interactions in Zoom Meetings and Zoom Phone to improve sales team productivity.

Currently, the company makes most of its money through Zoom Meetings. But Zoom Phone surpassed 10% of total revenue in the first quarter of fiscal 2024, and Zoom Contact Center will probably reach that milestone in the not-to-distant future given that licenses increased nearly threefold over the past year. Add-on AI solutions could also become a meaningful revenue stream as core communications products see greater adoption.

On that note, Zoom recently debuted generative AI software that can summarize conversations, draft messages, and answer questions on meeting content, among other functions. CFO Kelly Steckelberg, on the fourth-quarter earnings call, said, “Zoom AI Companion has grown tremendously in just five months, with over 510,000 accounts enabled.” The product is currently free, but Zoom could monetize it in the future.

In short, Zoom once again reported sluggish revenue growth in fiscal 2024, and management expects that trend to continue next year, as guidance implies 1.6% revenue growth in fiscal 2025. However, Zoom is well positioned to drive adoption of adjacent communications and AI products given its leadership position in videoconferencing software, so revenue growth could accelerate in the future, especially in a more favorable economic environment.

Ark Invest’s valuation model for Zoom builds on the idea that adoption of core communications software and adjacent AI products could push sales to $52 billion in 2026. Even if we apply that figure to fiscal year 2027, most of which will take place during calendar year 2026, that forecast implies annual revenue growth of 125%. That is beyond the realm of possibility.

Wall Street has a more dour outlook. Analysts expect Zoom to grow revenue at 3.9% annually over the next five years. That estimate aligns with the sluggish growth we’ve seen in recent quarters, but it also leaves room for upside depending on how successful the company is with newer products like Zoom Phone, Zoom Contact Center, and add-on AI software.

With that in mind, the stock currently trades at 4.5 times sales, near its all-time low of 4 times sales. That valuation is a bit pricey if Wall Street is correct in its expectations. But should revenue grow more quickly — say, 10% annually over the next five years — the current valuation would be a bargain in hindsight.

So, investors who think Zoom could meaningfully top the Wall Street consensus should consider buying a small position in this stock today, provided they understand that the odds of a 2,170% return by 2026 are essentially zero.

Should you invest $1,000 in Zoom Video Communications right now?

Before you buy stock in Zoom Video Communications, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Zoom Video Communications wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 8, 2024

Trevor Jennewine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Zoom Video Communications. The Motley Fool has a disclosure policy.

1 Artificial Intelligence (AI) Stock to Buy Before It Soars 2,170%, According to Cathie Wood’s Ark Invest was originally published by The Motley Fool

The U.S. stock market is facing an inflation reading that will test its 2024 bull run and offer clues as to whether the economy remains on course for an anticipated soft landing.

Source link

Shares of C3.ai (AI -0.22%) shot up impressively in the past month thanks to the company’s better-than-expected quarterly results. The pure-play enterprise artificial intelligence (AI) software provider is on track to take advantage of the huge end-market opportunity on offer in this space.

The stock surged 50% in February and analysts at Wedbush Securities expect the bull run to continue. The firm has raised its price target on C3.ai stock from $35 to $40, which points toward a 25% upside from current levels. But can C3.ai stock sustain its momentum for the next three years? Let’s find out.

In the third quarter of fiscal 2024 (ended on Jan. 31, 2024), C3.ai reported an 18% year-over-year increase in revenue to $78.4 million. The figure exceeded the company’s guidance range of $74 million to $78 million. For the current quarter, C3.ai is forecasting $82 million to $86 million in revenue, the midpoint of which is slightly higher than consensus estimates of $83.9 million.

The midpoint of this quarter’s revenue guidance indicates that C3.ai’s revenue could jump 16% year over year. That would be a nice improvement over the same quarter last year when its revenue remained almost flat on a year-over-year basis. Additionally, C3.ai has narrowed its revenue guidance range for the current fiscal year. It expects to finish the year with $308 million in revenue at the midpoint, which is slightly higher than the earlier forecast of $307.5 million.

The upgraded revenue guidance indicates that C3.ai’s revenue in fiscal 2024 is on track to jump 15.4% from the previous guidance. That would be a major improvement over the 5.6% revenue growth it registered in fiscal 2023. C3.ai is witnessing an uptick in growth largely because its AI software solutions are gaining greater traction in the market.

The company provides ready-to-use AI applications, as well as an application development platform to help make custom enterprise AI applications. Last quarter, C3.ai struck 50 agreements for deploying its solutions, which was an increase of 85% from the year-ago period. Additionally, C3.ai started 29 new pilot projects in fiscal Q3, an increase of 71% from last year, suggesting that it could continue to win new business going forward.

It is also worth noting that 27 of the new agreements that C3.ai closed last quarter were made possible by its partner ecosystem. The company has made its enterprise AI applications available on leading cloud computing platforms such as Alphabet‘s Google Cloud and Microsoft Azure. C3.ai’s current and potential customers can develop and deploy AI applications on these platforms, and the good part is that the company seems to be getting new business because of these partnerships.

C3.ai points out that its partner-supported bookings grew a whopping 337% year over year in the previous quarter. What’s more, the company says that its pipeline of potential customers has increased by 73% year over year in the previous quarter. All this tells us why Wedbush has increased its price target on C3.ai. More importantly, C3.ai’s potential revenue growth over the next couple of fiscal years shows that it could deliver impressive upside.

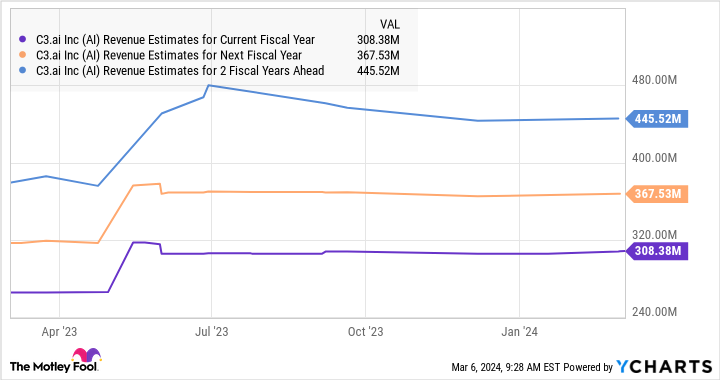

We have already seen that C3.ai is expected to finish fiscal 2024 with $308 million in revenue. More importantly, its revenue growth rate is expected to improve to 19% in fiscal 2025.

AI Revenue Estimates for Current Fiscal Year data by YCharts

Even better, analysts are forecasting a 21% increase in C3.ai’s fiscal 2026 revenue as per the chart above. Assuming it can maintain this pace and record a 20% jump in revenue in fiscal 2027, its top line could increase to almost $535 million after three years.

C3.ai is currently trading at 13.4 times sales. While that’s rich when compared to the Nasdaq-100 Technology Sector index’s price-to-sales ratio of 8.4, C3.ai could continue to command a higher sales multiple because of an AI-powered acceleration in growth.

However, if we assume that C3.ai trades at a slightly discounted sales multiple of 10 after three years, its market cap could jump to $5.35 billion based on the projected fiscal 2027 revenue. That would be a 43% increase from current levels. But don’t be surprised to see this AI stock deliver stronger gains.

The AI software market is expected to clock annual growth of 37% through 2030. This solid opportunity suggests that C3.ai’s revenue growth could outpace expectations over the next three years and the market could reward it with a premium valuation. Its stock could soar substantially in the future as a result.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet and Microsoft. The Motley Fool recommends C3.ai and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Tobacco stocks have long been ripe territory for income investors, and after years of consolidation and decline, the industry has been whittled down to three major players: Altria (MO 0.77%) and Philip Morris International (PM 1.28%), which were once part of the same company; and British American Tobacco. BAT deserves consideration from income investors open to tobacco stocks, but here we’ll focus on just Altria and Philip Morris, two companies with similar product portfolios and who have a history of working together.

When the old Philip Morris split in 2008 into Philip Morris International and Altria, which is the parent of Philip Morris USA, PMI took the territory outside the U.S., while Altria retained domestic operations, and the two companies have evolved since. Let’s take a look at how the two stocks stack up in various categories to see which is the better buy today.

Image source: Getty Images.

Both tobacco stocks are subject to similar industry trends, including declining cigarette consumption. In its fourth-quarter earnings report, Altria reported a 7.6% decline in cigarette shipment volumes to 18.2 billion, and overall revenue, excluding excise taxes, fell 2.4% to $4.35 billion.

Historically, Altria has made up for falling cigarette volumes by raising prices, and it’s also looked to new businesses to deliver growth. However, most of those attempts have fallen flat. In 2018, it spent $12.8 billion to acquire a 35% stake in Juul Labs, though a regulatory crackdown erased nearly all the value of that investment, and what’s left of it now is some heated tobacco intellectual property rights.

An investment in Canadian cannabis grower Cronos Group also led to write-downs and losses, as that industry has underperformed since Canadian legalization.

Now, Altria is pinning its hopes on NJOY, which it acquired a year ago for $2.75 billion in cash. NJOY brings a diverse portfolio of both disposable e-cigarettes, branded Daily, and a vape with reusable pods, Ace. NJOY’s revenue is believed to be a fraction of Altria’s, so its value is in its own growth potential. Altria also sold the commercialization rights in the U.S. for Philip Morris International’s heat-not-burn system IQOS back to PMI, showing that it’s solely focused on NJOY as its next-gen product.

By comparison, Philip Morris seems to have several advantages over Altria. It reported a decline in cigarette volume of just 1.9% to 151.1 billion, as international markets have faced less tobacco regulation as the U.S. has. Philip Morris has also done better at developing its next-gen business as sales of its heated tobacco units (HTUs), largely IQOS, rose 6.1% to 34 billion, which is more cigarettes than Altria sold in total. PMI’s purchase of IQOS rights for the U.S. from Altria for $2.7 billion indicates confidence that it can make that product successful in the U.S.

Because of its success in HTUs, Philip Morris’s overall product shipment volume is nearly flat, and it is on the verge of driving positive growth as HTUs, which were up 6.1% in the latest quarter, replacing cigarettes. More than any other tobacco stock, Philip Morris has found success with next-gen products. That’s led to solid revenue growth as well, with adjusted revenue up 8.3% to $9 billion in the fourth quarter.

While Philip Morris is growing revenue faster than Altria, it’s the more profitable of the two companies based on margins, which is likely a reflection of much of its sales coming from the premium Marlboro brand, and the increased disposable income in the U.S. Altria recorded an adjusted operating income margin of 59.9% last year, compared to 33% for Philip Morris.

Still, Philip Morris managed to grow adjusted operating income by 3.7%, while Altria’s was flat.

Altria currently trades at a price-to-earnings ratio of 8.3 and offers an impressive dividend yield of 9.6%. Philip Morris, on the other hand, offers a P/E of 17.2 and a dividend yield of 5.8%. That gives Altria a clear edge here.

Altria might be more appealing to dividend investors strictly looking for yield, but Philip Morris is the better choice. The company has a much brighter future as its next-gen business has reached scale and cigarette volumes are declining more slowly, and it doesn’t face the same regulatory restrictions that Altria does.

Altria’s dividend does look safe for now, but it can’t rely on raising cigarette prices forever. While the NJOY acquisition could pay off, it could also take years for it to positively impact the bottom line. Only one of these stocks offers growth, stability, and high yield, and that’s Philip Morris.

Jeremy Bowman has no position in any of the stocks mentioned. The Motley Fool recommends British American Tobacco P.l.c. and Philip Morris International and recommends the following options: long January 2026 $40 calls on British American Tobacco and short January 2026 $40 puts on British American Tobacco. The Motley Fool has a disclosure policy.