HashiCorp Inc.’s shares climbed more than 12% after hours Friday, after a report revealed that the cloud-adoption software company is considering putting itself up for sale.

Source link

HashiCorp Inc.’s shares climbed more than 12% after hours Friday, after a report revealed that the cloud-adoption software company is considering putting itself up for sale.

Source link

The continued return of manufacturing to the U.S., coupled with the “robust” U.S. infrastructure program, will support strong demand for years.

Source link

Nvidia (NVDA -0.12%) is a stock many investors have missed out on. Its unbelievable market outperformance started at the beginning of 2023 and continues well into 2024, with the stock up more than 480%.

But just because it has risen that much doesn’t necessarily mean investors have missed out; you can always buy the stock now.

Many might be concerned about shares falling due to high expectations built into it. However, I can come up with three good reasons Nvidia is a buy right now, and investors of all opinions should consider these.

Nvidia’s primary products are graphics processing units (GPUs), the hardware often tasked with complex computing, like engineering simulations or gaming graphics. But they’re also useful for data gathering and training artificial intelligence (AI) models. That makes them a key factor in the AI revolution taking the world by storm.

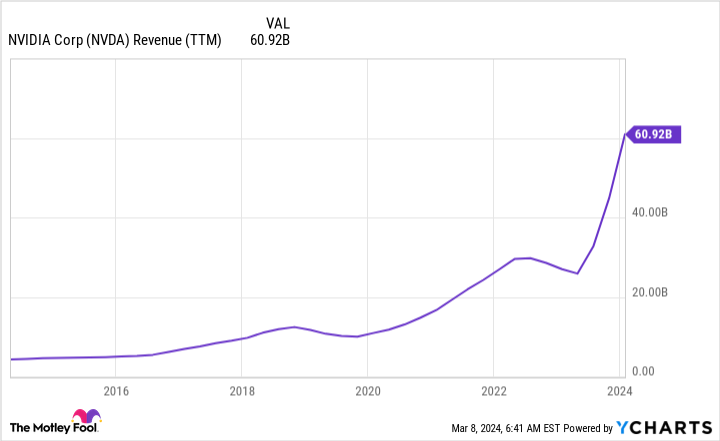

As companies rush to build data centers to increase computing capability and power these ever-improving models, Nvidia’s business has soared. In its latest quarter, Nvidia’s revenue was up 265% to $22.1 billion. This brought its revenue for the full-year 2024 (ending Jan. 28) to $60.9 billion. And many market analysts believe there is more in store for GPU production.

NVDA revenue (TTM) data by YCharts; TTM = trailing 12 months.

Precedence Research sees the GPU market expanding to $773 billion by 2032. Considering that Nvidia holds a firm grip on the GPU market, it will be the primary benefactor of this increase.

Just because Nvidia has experienced unbelievable growth doesn’t mean it’s done yet. But investors shouldn’t expect revenue to triple like it did over the past year.

AI is all the rage in the stock market, but how many people use it in their daily work? The reality is that very few people have been affected by its power. But with AI going mainstream through digital assistants, that is about to change.

GPUs will be needed to harness the power of these tools, which is another boost for Nvidia. More innovations will follow once the workforce becomes comfortable with using AI to improve productivity.

These innovations will require more computing power because previous models are being run on existing infrastructure, so GPUs will once again benefit from AI proliferation.

The last piece of the puzzle is Nvidia’s H100 GPU. This is its flagship model, but the company is working on its replacement already. The H200 GPU is expected to launch in Q2 2024, and will essentially double the computing capacity for a single GPU compared to the H100. The increase in computing power and efficiency will drive many to upgrade, which will be another boost for the chipmaker. Additionally, it keeps Nvidia ahead of the competition, further cementing its place on top of the GPU world.

We’re in the early innings of AI affecting work, and Nvidia is set to capitalize.

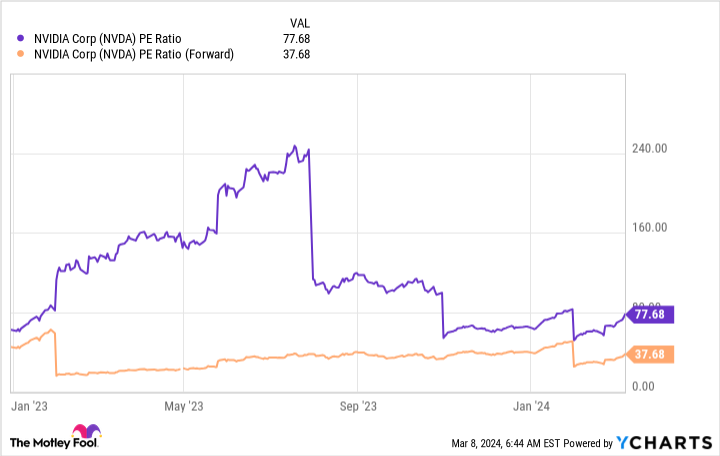

The previous two reasons don’t involve the stock; they only concern the future. However, thanks to Nvidia’s growth, the stock isn’t as expensive as it used to be.

When a company is undergoing a massive transformation, it’s useful to look at the forward price-to-earnings (P/E) ratio, which uses analyst projections. This analysis isn’t perfect, but it gives investors a better idea of where Nvidia is heading rather than looking at where it has been.

NVDA PE ratio data by YCharts.

While Nvidia’s P/E ratio has been sky-high at times, its forward earnings have hovered around reasonable levels — 38 times forward earnings is still a very expensive price tag for a stock, but it looks much more palatable than 78 times trailing earnings.

And when the world’s largest company, Microsoft, trades at 35 times forward earnings despite slower growth, Nvidia’s stock price doesn’t look all that bad.

Investors are unlikely to see the incredible growth Nvidia experienced in 2023 again, but there is still plenty of room for steady, market-beating growth, which makes it a stock that investors can confidently invest in, even now.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

Salesforce‘s (CRM -1.54%) stock rallied nearly 50% over the past three years and set a new all-time high in early March. It achieved those gains even as its growth slowed down and it was besieged by activist investors in the first half of 2023.

The cloud software giant pacified its critics by laying off thousands of employees, reining in its marketing expenses, suspending its ecosystem-expanding acquisitions, and launching its first buyback plan to boost its earnings per share (EPS). It also recently initiated its first dividend with a forward yield of 0.5%.

Image source: Getty Images.

Those moves convinced many investors that Salesforce was still a worthwhile investment, even if the macro and competitive headwinds were throttling its long-term sales growth. But can Salesforce climb to new highs over the next three years?

Salesforce owns the world’s largest cloud-based customer relationship management (CRM) platform. It controls over a fifth of the market, according to Gartner, while its four closest competitors — Microsoft, Oracle, SAP, and Adobe — each hold mid- to low-single-digit shares.

Salesforce capitalized on the growth of its CRM platform to launch additional cloud-based marketing, e-commerce, analytics, app development, and data visualization services. It significantly expanded its ecosystem through acquisitions over the past decade, and it processes all of that data with its Einstein artificial intelligence (AI) platform to help companies make more informed decisions.

From fiscal 2011 to fiscal 2022 (which ended in January 2022), Salesforce’s revenue grew at a compound annual growth rate (CAGR) of 29%. But over the past three fiscal years, its revenue growth slowed down as the macro headwinds drove companies to rein in their software spending. Fierce competition from Microsoft, which integrates its Dynamics CRM platform into its other cloud-based services, could be exacerbating that pressure. However, Salesforce’s cost-cutting measures significantly boosted its adjusted operating and free-cash-flow (FCF) margins as its buybacks lifted its adjusted EPS.

|

Metric |

FY 2022 |

FY 2023 |

FY 2024 |

|---|---|---|---|

|

Revenue growth |

25% |

18% |

11% |

|

Adjusted operating margin |

18.7% |

22.5% |

30.5% |

|

FCF margin |

19.9% |

20.1% |

27.2% |

|

Adjusted EPS growth |

(3%) |

10% |

57% |

Data source: Salesforce.

For fiscal 2025, Salesforce expects its revenue to rise 8% to 9% as its adjusted operating margin expands to 32.5%. Analysts expect its revenue and adjusted EPS to increase 9% and 19%, respectively. Those growth rates are stable, but they still imply that the company’s high-growth days are over and its business is maturing.

From fiscal 2024 to fiscal 2027, analysts expect Salesforce’s revenue to grow at a CAGR of 10% as its EPS rises at a CAGR of 29%. But at 31 times forward earnings, it seems like a lot of that future growth has also been baked into its stock price.

By comparison, analysts expect Microsoft’s revenue and earnings to grow at CAGR of 15% and 17%, respectively, from fiscal 2023 to fiscal 2026 (which ends in June 2026). Microsoft’s stock also looks a bit pricey at 30 times forward earnings, but its business is more diversified and it’s heavily exposed to the AI market via its hefty investment in OpenAI.

Microsoft’s integration of OpenAI’s generative AI tools into Dynamics CRM and its other cloud-based software could also cause long-term headaches for Salesforce. In its latest quarter, Microsoft’s Dynamics 365 revenue rose 24% year over year in constant currency terms. Salesforce’s comparable Sales Cloud revenue only grew 10% on the same basis.

Over the next three years, Salesforce will likely keep cutting costs and buying back shares to offset its slower sales growth. But by pursuing that strategy, it risks becoming a slow-growth tech company like IBM — which focused too heavily on cost-cutting measures and buybacks in the 2010s instead of expanding its cloud business to drive its long-term sales growth.

Salesforce insists its expansion of Einstein’s ecosystem will help it keep pace with the broader shift toward AI-driven services. But its focus on expanding its operating margins and boosting its earnings could clash with those plans. Simply put, Salesforce will need to walk a fine line between investing in its growth and maintaining healthy margins.

Salesforce’s stock looked cheap relative to its growth when it dropped to $170 per share last March, but it doesn’t seem like a bargain right now. Its stock might gradually rise over the next three years as investors focus on its earnings instead of its revenue, but it could underperform the market as its valuations limit its upside potential. It could also generate less impressive gains than more exciting AI plays like Microsoft.

Leo Sun has positions in Adobe. The Motley Fool has positions in and recommends Adobe, Microsoft, Oracle, and Salesforce. The Motley Fool recommends Gartner and International Business Machines and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The power of ‘I don’t know.’

Source link

Late in December, Nvidia Corp. topped a list of favorite stocks among analysts working for brokerage firms. But with the stock continuing to soar this year, running the same screen of the S&P 500 produces a different result, with Nvidia no longer even making the top 20.

Back in December, the great majority of analysts polled by FactSet who covered Nvidia NVDA rated the stock a buy or the equivalent. Before the market opened on Dec. 26, their consensus price target for the stock was $668.11, which was 37% higher than the Dec. 22 closing price of $488.30.

Nvidia’s stock closed out 2023 at $495.22, having risen 239% for the year. So far in 2024, the stock has climbed another 83.5% to close at $908.88 on Wednesday. That is slightly above the new consensus 12-month price target of $904.55 for the stock.

Even though 54 out of 60 analysts still rate Nvidia a buy, the stock has gotten ahead of the analysts’ traditional consensus 12-month price target. That combination of favorable ratings and a target below the current price gives some food for thought: A year isn’t a lengthy period for a committed long-term investor.

Last week, we looked at Nvidia’s price-to-earnings valuation, which has come down significantly over the past year.

Beginning with the S&P 500 SPX, we narrowed the list to 74 stocks with at least 75% buy or equivalent ratings among analysts polled by FactSet.

Here are the 20 remaining stocks in the S&P 500 that are buy-rated by at least 75% of analysts and that have the highest 12-month upside potential indicated by the consensus price targets:

|

Company |

Ticker |

March 13 price |

Consensus price target |

Implied 12-month upside potential |

Share buy ratings |

|

United Airlines Holdings Inc. |

UAL |

$43.04 |

$63.46 |

47% |

77% |

|

First Solar Inc. |

FSLR |

$158.04 |

$226.83 |

44% |

82% |

|

Insulet Corp. |

PODD |

$175.54 |

$237.18 |

35% |

83% |

|

Aptiv PLC |

APTV |

$79.72 |

$103.73 |

30% |

80% |

|

Schlumberger Ltd. |

SLB |

$52.57 |

$68.15 |

30% |

94% |

|

Halliburton Co. |

HAL |

$36.53 |

$47.28 |

29% |

88% |

|

Zoetis Inc. Class A |

ZTS |

$176.23 |

$227.20 |

29% |

88% |

|

MGM Resorts International |

MGM |

$42.86 |

$55.24 |

29% |

80% |

|

Baker Hughes Co. Class A |

BKR |

$31.75 |

$40.55 |

28% |

80% |

|

Lamb Weston Holdings Inc. |

LW |

$102.94 |

$129.15 |

25% |

93% |

|

Carnival Corp. |

CCL |

$16.65 |

$20.88 |

25% |

83% |

|

Delta Air Lines Inc. |

DAL |

$43.91 |

$53.89 |

23% |

96% |

|

VICI Properties Inc. |

VICI |

$29.31 |

$35.78 |

22% |

88% |

|

UnitedHealth Group Inc. |

UNH |

$488.00 |

$595.73 |

22% |

88% |

|

Take-Two Interactive Software Inc. |

TTWO |

$144.89 |

$176.11 |

22% |

77% |

|

News Corp Class A |

NWSA |

$26.35 |

$32.02 |

22% |

78% |

|

Las Vegas Sands Corp. |

LVS |

$53.35 |

$63.95 |

20% |

83% |

|

SBA Communications Corp. Class A |

SBAC |

$219.80 |

$262.36 |

19% |

82% |

|

Teledyne Technologies Inc. |

TDY |

$421.24 |

$500.55 |

19% |

90% |

|

NextEra Energy Inc. |

NEE |

$59.54 |

$70.32 |

18% |

77% |

|

Source: FactSet |

|||||

Click on the tickers for more about each company.

News Corp NWSA is the corporate parent of MarketWatch publisher Dow Jones.

Don’t miss: Alphabet is the bargain stock among the ‘Magnificent Seven’

Also read: Why Japan’s stock market could keep soaring — plus three stock picks there

Fool.com contributor Parkev Tatevosian discusses why he places this growth stock on his list of top stocks to buy.

*Stock prices used were the afternoon prices of March 11, 2024. The video was published on March 13, 2024.

Parkev Tatevosian, CFA has positions in PayPal. The Motley Fool has positions in and recommends PayPal. The Motley Fool recommends the following options: short March 2024 $67.50 calls on PayPal. The Motley Fool has a disclosure policy.

Parkev Tatevosian is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through his link, he will earn some extra money that supports his channel. His opinions remain his own and are unaffected by The Motley Fool.

He may be the world’s best stock picker. But that doesn’t mean every single one of Warren Buffett’s picks held by Berkshire Hathaway dishes out gains each and every year. And that’s OK — the Oracle of Omaha is in it for the long haul. He likely understands you’re going to take some short-term lumps while waiting for a company’s long-term performance to be reflected in its stock’s price.

That said, every now and then the proverbial planets align for one of Berkshire’s holdings, setting the stage for a parabolic move. The fund’s position in The Kraft Heinz Company (KHC -0.61%) could be on the cusp of such a move now. Here’s why.

It’s been an uncharacteristically poor performer since Buffett helped orchestrate the merger of food giants Kraft and Heinz back in 2015. Shares have been more than halved since the post-merger stock began trading, in fact, with most of that setback taking shape before the COVID-19 pandemic.

What gives? As it turns out, the anticipated cost savings and competitive edges weren’t so easy to achieve. Supply chain disruptions stemming from the pandemic followed by soaring inflation have held the stock down in the meantime. It’s been so long since the company’s made a truly healthy fiscal showing, in fact, that many investors and analysts may be throwing in the towel now, presuming Kraft Heinz is beyond repair.

But that could be a big mistake. This year could mark the beginning of a long overdue turnaround.

To be clear, there’s still much work to be done. The analyst community is essentially calling for no sales growth this year, with per-share earnings only projected to grow from last year’s $2.98 to $3.04 per share. That’s anything but thrilling.

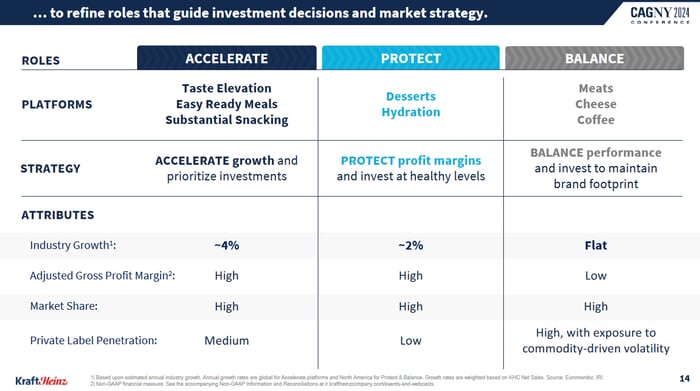

There are some initiatives that relatively new CEO Carlos Abrams-Rivera is leading, however, that will take time to measurably matter. One of these is a rethinking of the company’s innovation priorities. It’s ramping up its reach into the easy-ready meals and what it refers to as “substantial snacking” categories, for instance, as well as doubling down on taste elevation.

One such development is the creation of a boxed kit allowing consumers to recreate Taco Bell’s Crunchwrap Supreme and Chipotle Chicken Quesadilla at home. The company is also repositioning its popular brands of macaroni and cheese into being meals themselves. These are higher-growth opportunities that Kraft Heinz says could one day account for three-fourths of its revenue, versus less than two-thirds of its sales right now.

The Kraft Heinz Company also understands it must still look beyond food itself to be better. It’s got to spend more efficiently as well. That’s why it’s now using artificial intelligence (AI) to plan its promotional calendar. It’s also getting a better handle on demand forecasting. These efforts are paying off. The company says it’s still on track to realize this year’s target of $2.5 billion worth of new spending efficiencies.

To be fair, at first blush much of what Abrams-Rivera appears to be doing now doesn’t look all that different than what his predecessor, Miguel Patricio, appeared to be doing then. All food companies strive to innovate in order to remain competitive. All companies look for ways to cut costs.

Dig deeper though. Kraft Heinz is emerging from a years-long period of disappointing management followed by an inflation-spurring pandemic. It’s stronger now than it was then, and is certainly more in tune with what consumers as well as its institutional customers actually want.

This includes (among other things) more plant-based eating options like plant-based Oscar Mayer hot dogs in addition to making comfort foods like mac and cheese even more accessible. This is actually the most holistic strategic thinking the company’s demonstrated in quite some time.

Image source: The Kraft Heinz Company’s CAGNY 2024 presentation.

That’s also why analysts expect Kraft Heinz’s top- and bottom-line growth to start showing some measurable acceleration beginning next year.

Do Buffett and Berkshire’s other managers fully understand the turnaround The Kraft Heinz Company is finally piecing together for itself? Maybe. Maybe not. But he certainly sees enough to stick with all 326 million shares of the company Berkshire’s been holding since 2015, when Kraft and Heinz merged. That speaks volumes.

Maybe the dividend has something to do with it. The stock is yielding 4.6% right now, based on a dividend that’s been paid every quarter — even if it hasn’t grown — since the beginning of 2020. Earnings have more than adequately funded the dividend, too. In fact, although the company’s management has made no mention of it, analysts’ projected earnings growth along with Kraft Heinz’s recent cash-flow growth could be setting the stage for a dividend bump in the foreseeable future.

KHC Cash from Operations (Quarterly) data by YCharts

Even if that’s not in the near-term cards, forward progress is. The hard part is the waiting. But there’s still reason to take a shot sooner rather than later. Kraft and Heinz are both iconic brand names the market wants to support. Once enough investors and analysts start seeing a glimmer of hope on the horizon, don’t be surprised to see some real movement in the stock.

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway. The Motley Fool recommends Kraft Heinz. The Motley Fool has a disclosure policy.

Utilities are conservative income stocks with a reputation for being safe enough to be appropriate for widows and orphans. That’s true for some utilities, but NextEra Energy (NEE 0.55%) bucks the trend (in a good way). While NextEra operates a boring utility, it also owns a rapidly growing renewable power business.

For both growth and income and dividend growth investors, it’s a great stock to consider. And now is a unique opportunity to buy it. Here’s what you need to know.

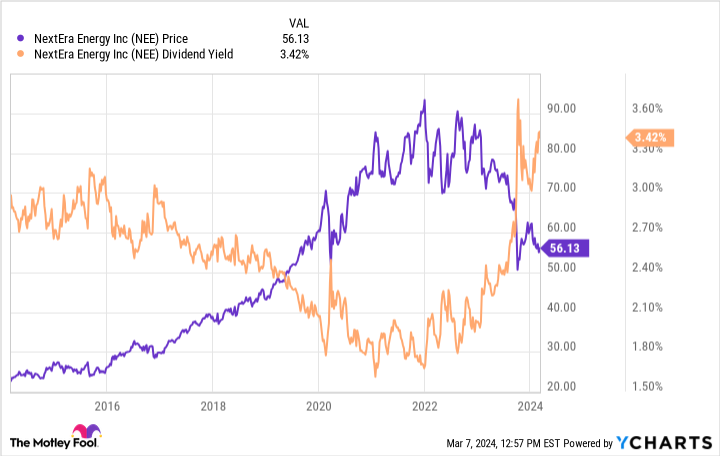

NextEra Energy’s dividend yield is around 3.5%. That’s basically in line with the utility average, using Vanguard Utilities Index ETF as an industry proxy. While income-focused investors might see NextEra’s yield as modest, it’s important to note that the 3.5% yield is near the highest levels of the past decade. So in this way, the stock looks historically cheap right now.

That said, management expects to increase the dividend by roughly 10% in 2024, which is both attractive on an absolute level and extremely high for a utility. But that’s right in line with the rate of dividend growth over the past decade. The dividend has been increased annually for 29 years, so an increase in 2024 would bring that record up to a cool three decades. NextEra Energy is a dividend growth machine, and there’s no reason to think that the growth is going to come to a halt anytime soon.

Notably, management projects earnings growth of between 6% and 8% a year through 2026. There’s a chance that dividend growth will slow down and simply track along with earnings growth, but even that would suggest an attractive dividend growth rate. This is particularly true of a utility stock.

That’s notable because dividend growth investors and growth and income investors looking to create a diversified portfolio will probably find it hard to add utility exposure. Most stocks in the sector are simply slow-growing on the earnings and dividend fronts. NextEra Energy’s historically high yield and robust growth outlook make the stock an ideal diversification pick for investors looking for something with a little more growth.

The really big reason for NextEra’s high yield is that interest rates have risen. There are two issues for investors to consider here. First, other income options are now more competitive, like certificates of deposit. Second, and more importantly, higher interest rates will make it more expensive for NextEra to grow its business. The utility sector is capital-intensive and makes heavy use of leverage. Don’t get too worried about this.

There are two distinct businesses here to consider. First, NextEra owns Florida Power & Light, which is the largest regulated utility in Florida and about 70% of the utility’s business. The Sunshine State has benefited from population growth for years. More customers mean more revenue and more opportunity to invest in regulated assets. This is a very stable and reliable business, because NextEra has been granted a monopoly in exchange for accepting government oversight of the rates it charges and its capital investment plans. Regulators generally adjust so that utilities can earn a reliable return. Thus, it’s highly likely that the rates NextEra can charge will eventually be updated to account for higher interest rates.

The rest of NextEra is NextEra Energy Resources, one of the largest renewable power generators in the world. This is a fast-growing business with a very long runway for growth as carbon-heavy power sources get replaced by renewable sources like solar and wind. NextEra currently operates around 34 gigawatts of clean energy. It has plans to add as much as 41.8 gigawatts to that total by 2026. This side of the business is not regulated, so higher interest rates will have to be dealt with on a contract-by-contract basis. Market forces are likely to ensure NextEra can profitably grow this side of its business even if there’s some near-term disruption to deal with.

In all, higher interest rates are a headwind. But they’re highly unlikely to change the long-term growth trajectory of NextEra and its dividend.

There’s no such thing as a perfect investment, but the current concerns about NextEra’s growth seem likely to be temporary and, perhaps, a little overblown. That’s an opportunity for investors that think in decades. Growth-and-income and dividend growth-focused investors have the chance to add a reliable utility stock to their portfolios with a historically attractive yield. That’s not something you should pass up without giving NextEra a deep dive.

Fool.com contributor Parkev Tatevosian highlights one stock in Warren Buffett’s Berkshire Hathaway portfolio that investors can buy now and hold for the long run.

*Stock prices used were the afternoon prices of March 11, 2024. The video was published on March 13, 2024.

Should you invest $1,000 in Paramount Global right now?

Before you buy stock in Paramount Global, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Paramount Global wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 11, 2024

Parkev Tatevosian, CFA has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Parkev Tatevosian is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through his link, he will earn some extra money that supports his channel. His opinions remain his own and are unaffected by The Motley Fool.

1 Ridiculously Cheap Warren Buffett Stock Down 89% to Buy Now and Hold Forever was originally published by The Motley Fool