Some exchange-traded funds rallied Wednesday even as stocks and bonds broadly fell, as hot inflation data stoked fears that interest rates will stay elevated for longer than anticipated.

Source link

Some exchange-traded funds rallied Wednesday even as stocks and bonds broadly fell, as hot inflation data stoked fears that interest rates will stay elevated for longer than anticipated.

Source link

Even with $300, many Buffett investments are within reach of the average investor.

Warren Buffett became one of the world’s best-known investors through his long track record of consistency. Since 1965, his portfolio has earned an average yearly gain of 20%, approximately double that of the S&P 500.

However, with Buffett now in his 90s, many investment decisions are in the hands of his lieutenants, Todd Combs and Ted Weschler. This has changed the philosophy of Berkshire Hathaway a bit, and to that end, it incorporates more growth stocks.

Consequently, investors — even with a modest budget of $300 — can find some intriguing growth stocks in the Berkshire portfolio that could deliver market-beating returns over time.

Berkshire did not buy Amazon (AMZN 1.67%) until 2019. As to why it took so long to buy, Buffett said he was “too dumb” to buy Amazon earlier. He was long skeptical of tech stocks but, in time, came to realize the staying power of such businesses.

Now, Amazon is the world’s second-largest retailer, according to the National Retail Federation. Moreover, it pioneered the cloud computing business through Amazon Web Services (AWS), a segment that now accounts for most of the company’s operating income.

Additionally, it operates fast-growth businesses such as digital advertising, online seller services, and its subscription service, known to the public as Amazon Prime. They helped generate revenue of $575 billion in 2023, a 12% increase from last year. This made it a highly diversified business that investors can buy for around $185 per share right now.

Admittedly, Amazon’s forward price-to-earnings (P/E) ratio of 44 may appear expensive, considering that investors often associate Buffett with finding bargains. Still, investors should remember that Amazon has always sold at a high multiple, and the portfolio has sought more expensive stocks since Buffett handed off some investment decisions to others.

Ultimately, with a comparatively reasonable valuation and its diverse business lines, it should remain a stock that serves Buffett and other investors well.

NuBank parent Nu Holdings (NU -0.17%) is one of the world’s largest online banks, but since it only operates in Brazil, Mexico, and Colombia, it is likely not on the radar of most investors. Nonetheless, it probably should be, and not just because Berkshire was an early investor in this business.

Nu presents a unique opportunity since just a few institutions had previously dominated banking in this region. For that reason, a large percentage of the population did not have a bank account or credit card. Nu has changed this by issuing the first credit card to millions of Brazilians. Now, 53% of all adult Brazilians (88 million of Nu’s 94 million customers) have at least one account with Nu.

Additionally, the company is now repeating this formula in Mexico and Colombia, meaning its rapid growth can continue. So fast is this growth that the company’s $8 billion in revenue for 2023 grew 68% over the previous year.

Moreover, with the stock at around $12 per share, investors can not only buy a few shares with a $300 budget but also buy at levels just above its IPO price from late 2021. Furthermore, at a forward P/E ratio of 31, the shares are priced reasonably when considering the outsized revenue growth of this fintech stock.

DaVita (DVA -0.50%) is probably not a company most investors think of as a growth stock. It offers kidney dialysis to more than 200,000 patients in the U.S. and 10 other countries.

However, the need for such services never disappears, making it the type of business that has always drawn Buffett’s attention. Additionally, approximately 10,000 baby boomers age into Medicare every day, and chronic kidney disease affects about 34% of U.S. adults aged 65 or older. While that may serve as a warning to watch one’s kidney health, it also means a growing customer base for DaVita as kidney disease rises.

Admittedly, considering that its 2023 revenue of $12 billion grew by only 5%, it may not look like much of a “growth” business. Nonetheless, the stock has been in a state of recovery as excess deaths (due to COVID-19) and missed appointments weighed on its performance for most of 2022, and rising labor costs have remained an ongoing challenge.

Moreover, analysts expect its cost-cutting to boost net income by 21% in 2024. Thus, considering its P/E ratio is around 18, the stock is arguably a bargain. Also, with the stock trading at about $135 per share as of the time of this writing, investors with a $300 budget can afford its shares. Investors who follow Buffett’s lead will likely continue to profit from this healthcare stock.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Will Healy has positions in Berkshire Hathaway and Nu Holdings. The Motley Fool has positions in and recommends Amazon and Berkshire Hathaway. The Motley Fool recommends Nu Holdings. The Motley Fool has a disclosure policy.

As AI strengthens these companies’ offerings, they can be great long-term investments.

Artificial intelligence (AI) has been the hottest topic in tech over the past year and a half. It has seemingly become unavoidable as the technology has been thrust into the mainstream, largely because of the commercial success of generative AI tools like ChatGPT.

The commercialization of AI has been a catalyst for many tech companies’ stock prices recently as well. Lots of companies even remotely dealing with AI have seen their stock prices surge as investors rushed to capitalize on the recent boom. Despite the success of many of these companies, there seems to be a lot more room for growth.

Investors looking to get exposure to the industry should consider the following three companies that are ready for a bull run.

After years of trailing behind Apple, Microsoft (MSFT -1.19%) has become the world’s most valuable public company, with a market cap of over $3.1 trillion.

Microsoft’s AI involvement primarily comes from its strategic partnership with ChatGPT creator OpenAI. What began as an initial $1 billion investment in OpenAI in 2019 has become deeply mutually beneficial.

OpenAI needs vast, scalable supercomputing capabilities to operate as effectively as possible. That’s where Microsoft comes into the picture. Microsoft’s cloud platform, Azure, serves as OpenAI’s main computing infrastructure, and in return, Microsoft gets exclusive licenses to OpenAI’s large language models (LLMs).

Having access to OpenAI’s LLMs has given Microsoft a leg up because it’s able to integrate them into its products and services and boost its offerings. Microsoft already has a diverse ecosystem of services that many consumers and corporations rely on. Add an AI component to make them more effective and “intelligent,” and the potential for these services to dominate their industries increases.

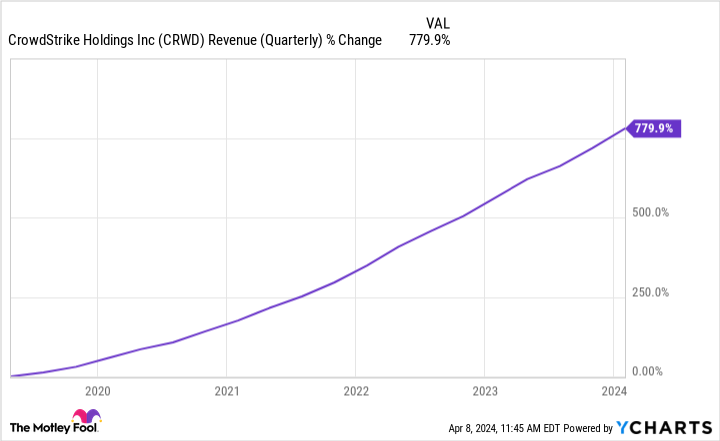

CrowdStrike (CRWD 0.84%) is one of the first pure AI cybersecurity companies, having used the technology to automate cybersecurity processes for well over a decade.

Other companies are undoubtedly adding AI capabilities to their cybersecurity platforms, but CrowdStrike has a competitive advantage that should hold strong: data. For AI-based tools to be as effective as possible, they must be trained on tons of data, and “tons” is putting it lightly. CrowdStrike’s head start means it has years’ worth of data that can’t be matched.

Business and financial results highlight just how effective CrowdStrike’s platforms have been. Around 27% of its clients use seven or more of its modules (products in its ecosystem), and 64% use five or more. CrowdStrike’s dollar-based net retention rate was also 119% in the fourth quarter of its fiscal 2024, meaning its established customers spent 19% more with it, on average, than they had in the prior-year period.

CRWD Revenue (Quarterly) data by YCharts.

According to CrowdStrike and market intelligence firm IDC, the AI-native cybersecurity market is estimated to be around $100 billion this year. By 2028, it’s expected to hit $225 billion. This gives CrowdStrike plenty of opportunity to continue asserting its market dominance and providing good long-term investor value.

As a semiconductor foundry, Taiwan Semiconductor Manufacturing Company (TSM 1.03%) (TSMC) may not seem like an AI stock, but its importance to the AI ecosystem can’t be overstated.

If AI apps like ChatGPT or other LLMs are the end products of a tree, the semiconductors fabricated by TSMC are the initial seeds. And it all begins with data and data centers. Data centers are vital because they are the only way to store the vast amount of data needed to train AI, and these data centers rely heavily on graphic processing units (GPUs), which function as the brains for computing power.

Before you have functioning GPUs, you need semiconductors, and TSMC is the global leader in fabricating semiconductors. That’s why companies like Nvidia are among TSMC’s biggest customers; they know other semiconductors pale in comparison to TSMC’s, cementing it as the go-to for other major corporations.

Without TSMC’s advanced processes, the AI pipeline would surely take a hit, as it’s likely that progress in the field would be slowed. That reliance alone makes TSMC one of the more important AI-adjacent companies. This domino effect is also expected to make AI-related semiconductors account for a decent portion of TSMC’s revenue (high teens) by 2027.

TSMC is far from the only semiconductor foundry in the AI world, but it’s the most critical.

Stefon Walters has positions in Apple and Microsoft. The Motley Fool has positions in and recommends Apple, CrowdStrike, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

These companies are close to launching new products that could supercharge revenue.

Eli Lilly shares have soared more than 100% over the past year, bringing the company to a market value of more than $740 billion. Investors are excited about the pharma company because of its dominance in the billion-dollar weight loss drug market. Lilly sells two weight-loss drugs that, together, are bringing in billions of dollars in revenue, and demand for the products has even outpaced supply.

If you’ve missed out on Lilly’s big gains, though, don’t worry. You still can catch other opportunities thanks to the biotech and pharma industries’ endless flow of innovation and product launches. These may fuel immediate as well as long-term share price gains. Let’s check out two healthcare stocks with big catalysts on the horizon that could supercharge your portfolio right away and over time.

Image source: Getty Images.

Moderna (MRNA 6.18%) today is known for its blockbuster coronavirus vaccine. That product, the company’s one and only, helped the stock soar in earlier stages of the pandemic but, in more recent times, prompted investors to worry about future growth as demand for vaccination dropped.

The good news is Moderna may not be a one-product player for long. The company has a big catalyst coming up, with the U.S. Food and Drug Administration (FDA) set to decide on its respiratory syncytial virus (RSV) vaccine by May 12.

Though Pfizer and GSK already have commercialized their RSV vaccines, Moderna could have an edge for two reasons. First, the two big pharma companies reported cases of rare neurological condition Guillain-Barre syndrome in their clinical trials. Moderna didn’t. So, healthcare providers may prefer the safety profile of the potential Moderna product.

And second, Moderna’s investigational vaccine is the only one to come in a prefilled syringe format. This, too, could win over those who administer the vaccine because it cuts down on the potential for errors and speeds up the vaccination process. All of this means that, even though Moderna is later to market than Pfizer and GSK, it still could carve out significant share and even leadership.

The peak annual RSV market could be $10 billion, according to Moderna, so this vaccine may become a significant growth product for the biotech. And that makes now a great time to get in on Moderna, at the bargain level of 8.5 times forward earnings estimates.

Vertex Pharmaceuticals (VRTX 0.02%) doesn’t just have one big catalyst around the corner: It has two. The biotech giant aims to submit two approval requests to the FDA by the middle of this year, one for a new cystic fibrosis (CF) treatment candidate and another for its investigational pain medication. Both of these have blockbuster potential.

Vertex already is known as the world’s leader in CF treatment thanks to its drugs’ top performance, extending patients’ lives and quality of life. It already has the drugs and intellectual property to maintain this through the mid-2030s. Now, it may extend this by launching “the vanza triple,” an investigational treatment that’s even better than its current best-seller.

The big biotech also is expanding beyond this specialty, and through its clinical trials has shown it has what it takes to excel in other areas too. Vertex recently reported positive data from phase 3 trials of its non-opioid pain candidate, VX-548. The company aims to win a broad label for the treatment of moderate-to-severe acute pain, and later gain approval in chronic pain indications. This could be a huge opportunity because, today, pain treatments are limited to over-the-counter ones with limited efficacy or prescription opioids, which are linked to addiction.

The vanza triple and VX-548 could offer Vertex’s already solid revenue growth a big boost. And that makes the shares, trading at 24 times forward earnings estimates today, look like a great deal.

Adria Cimino has positions in Vertex Pharmaceuticals. The Motley Fool has positions in and recommends Pfizer and Vertex Pharmaceuticals. The Motley Fool recommends GSK and Moderna. The Motley Fool has a disclosure policy.

No next-big-thing investment trend has arguably been hotter since the advent of the internet than artificial intelligence (AI) is right now.

When discussing “AI,” I’m referring to software and systems handling tasks that would normally be overseen by humans. Machine learning gives software and systems the ability to learn and evolve without human intervention, which can make these systems more proficient at their tasks over time.

The utility of AI can’t be overstated enough. Almost every sector and industry can benefit from its use, which is probably why the analysts at PwC believe artificial intelligence will add $15.7 trillion to the global economy come 2030.

While most institutional money managers and Wall Street analysts view AI and the companies deploying AI infrastructure and software favorably, this bullishness isn’t universal. Based on the low-water price targets issued by a select group of Wall Street analysts, the following five AI stocks could plunge by as much as 86%!

The first AI stock that could tumble after a monstrous run higher is none other than the infrastructure backbone of the AI revolution, Nvidia (NASDAQ: NVDA). In February, D.A. Davidson analyst Gil Luria raised his and his firms’ price target on Nvidia to $620 from $410. Despite this epic increase, it implies that the third-largest public company by market cap in the U.S. will shed 30% of its value, based on where it closed on April 5.

Although Nvidia’s A100 and H100 graphics processing units (GPUs) have been the overwhelming top choice of businesses for AI-accelerated data centers, there are plenty of reasons to be believe Nvidia stock could be in a bubble.

To start with, Nvidia’s top four customers, which comprise about 40% of its sales, are all developing AI GPUs of their own. Even if these companies continue to rely on Nvidia’s GPUs as complements to their in-house GPUs, future orders from these industry leaders would be expected to decline.

To add to the above, Nvidia’s pricing power on its A100 and H100 GPUs is expected to take a hit in the latter-half of 2024. The lion’s share of its 217% increase in data center sales in fiscal 2024 (ended Jan. 28, 2024) was driven by GPU scarcity. As new competitors enter the arena and Nvidia ramps up its own production, GPU scarcity will diminish — as will the company’s pricing power.

Further, every next-big-thing trend over the last 30 years has navigated its way through an early stage bubble. Suffice it to say, I fully expect Luria’s price target to be hit.

A second artificial intelligence stock that could plummet in the not-too-distant future if one Wall Street analyst is correct is server and storage solutions company Super Micro Computer (NASDAQ: SMCI). Senior equity research analyst Mehdi Hosseini of Susquehanna stood firm on his price target of $250 for Super Micro just two months earlier in an interview on CNBC. This would imply Super Micro Computer losing almost three-quarters of its current value.

It’s understandable why investors have gone head over heels for Super Micro. The company incorporates Nvidia’s top-tier GPUs in its energy-efficient and highly customizable rack servers that are utilized in AI-accelerated data centers. Sales for the company are expected to double in 2024 to north of $14 billion.

However, we’ve been here before with Super Micro. It was expected to be a prime beneficiary of the cloud-computing revolution in the late 2010s, but failed to maintain its sales momentum. This speaks to the fact that investors have a terrible habit of overestimating the adoption of new trends and innovations.

Super Micro Computer also finds itself at the mercy of Nvidia. If the latter continues to deal with supply issues/scarcity for its GPUs, Super Micro will fail to realize its full potential.

While a retracement to $250 may not be in the cards anytime soon, Super Micro Computer definitely has a lot to prove after its stock appreciated by 767% over the trailing year.

The potential disaster du jour among AI stocks is North America’s leading electric-vehicle (EV) manufacturer Tesla (NASDAQ: TSLA). CEO and founder Gordon Johnson of GLJ Research believes Tesla will retrace to $23.53 per share, which would represent 86% downside from where it closed on April 5.

On one hand, Tesla has made history by becoming the first automotive company to build itself from the ground up to mass production in well over a half-century. It’s also the only EV pure-play that’s generating a recurring profit (four consecutive years, as of the end of 2023).

At the same time, Tesla is encountering game-changing challenges as EV demand tapers off. The company slashed the sales price of its four production models (3, S, X, and Y) on more than a half-dozen occasions in 2023. The end result has been a more-than-halving in Tesla’s operating margin since the end of September 2022 (17.2% to 8.2%, as of Dec. 31, 2023).

Perhaps an even bigger issue is that Tesla has failed to become more than just a car company. Its Energy Generation and Storage segment sales have stagnated in recent quarters, while Services is generating a low-single-digit gross margin. I’ll add that solar has been a money-loser since SolarCity was acquired in 2016.

Despite being nothing more than a car company, Tesla is valued at nearly 60 times forecast earnings in 2024. With most auto stocks trading in a range of 6 to 8 times expected earnings per share (EPS), there’s definite reason to believe Tesla stock will head lower.

A fourth artificial intelligence stock that could get absolutely crushed if the most-bearish Wall Street analyst proves accurate is enterprise analytics software company MicroStrategy (NASDAQ: MSTR). Last August, Jefferies analyst Brent Thill defended his firms’ lowball price target of $210 for MicroStrategy, which would imply a decline of 85% from where shares closed this past week.

One issue for MicroStrategy is that its AI-driven enterprise analytics software division stopped growing 10 years ago. Sales have fallen by an aggregate of 14% since peaking.

But let’s face the facts: MicroStrategy is best-known for CEO Michael Saylor’s strategy of issuing convertible debt and using the proceeds to buy Bitcoin (CRYPTO: BTC), the largest cryptocurrency by market cap. On March 19, Saylor made a post on X (the platform formerly known as Twitter) that noted his company held 214,246 Bitcoin — more than 1% of the eventual supply — at an average price of roughly $35,160 per token.

With each Bitcoin valued at $67,600, as of the time of this writing, MicroStrategy’s crypto stake is worth $14.5 billion. However, the company’s market cap currently stands at $24.4 billion. Accounting for the company’s modestly profitable (but non-growing) software business, as well as its growing debt pile, MicroStrategy is trading at around a 70% premium to the Bitcoin it holds.

If investors want to buy Bitcoin, a spot Bitcoin exchange-traded fund (ETF) or a direct purchase of the cryptocurrency on an exchange would be a considerably smarter move than buying into MicroStrategy, whose premium valuation to the current price of Bitcoin makes no sense.

The fifth AI stock that could plunge, according to the prognostication of one Wall Street analyst, is data-mining company Palantir Technologies (NYSE: PLTR). Analyst Rishi Jaluria of RBC Capital doesn’t believe Palantir’s Commercial segment margins can continue expanding at their current pace. This compelled Jaluria to recently reiterate his and his firms’ $5 price target on Palantir, which implies 78% downside.

There’s no question Palantir’s stock is pricey. The company’s nearly $51 billion market cap is closing in on a multiple of 19 times forecast sales this year. It’s also valued at 70 times consensus EPS in 2024 despite slowing sales growth.

But one thing Palantir has working for it that merits a hefty premium is its irreplaceability. No company at scale comes anywhere close to the solutions it can provide. Palantir’s AI-driven Gotham platform helps governments cull data and plan military operations. The contracts Palantir wins from the U.S. government tend to span multiple years and generate highly predictable cash flow.

Meanwhile, its Foundry platform is just getting off the ground and helping businesses make sense of their data so they can streamline their operations. Whereas a sales ceiling exists with Gotham — i.e., Palantir won’t offer access to its platform to certain countries (e.g., China) — Foundry has a theoretical growth runway that stretches decades into the future.

Though it could take some time for Palantir to grow into its current valuation, I don’t anticipate Jaluria’s low-water price target being hit.

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $539,230!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 8, 2024

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bitcoin, Jefferies Financial Group, Nvidia, Palantir Technologies, and Tesla. The Motley Fool has a disclosure policy.

5 Artificial Intelligence (AI) Stocks That Can Plunge Up to 86%, According to Select Wall Street Analysts was originally published by The Motley Fool

In this video, I will talk about two beaten-down stocks that are down 78% from their all-time highs and down 40% and 60% in the past five years.

*Stock prices used were from the trading day of April 5, 2024. The video was published on April 8, 2024.

Before you buy stock in Alibaba Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alibaba Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $539,230!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 8, 2024

Neil Rozenbaum has positions in PayPal. The Motley Fool has positions in and recommends PayPal. The Motley Fool recommends Alibaba Group and recommends the following options: short June 2024 $67.50 calls on PayPal. The Motley Fool has a disclosure policy. Neil is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through his link, he will earn some extra money that supports his channel. His opinions remain his own and are unaffected by The Motley Fool.

2 Growth Stocks Down 78% to Buy Before It’s Too Late was originally published by The Motley Fool

Here’s a key lesson for Financial Literacy month: Be real and study market history.

Source link

Although Nvidia should continue to prosper, other tech companies are also poised for outsize returns.

The massive growth of Nvidia undoubtedly caught many investors by surprise last year. As ChatGPT redefined the benefits of artificial intelligence (AI), the lead designer of AI chips jumped to the forefront of investor portfolios, generating growth and returns rarely matched in the market.

While such returns are uncommon, Nvidia will likely not be the only success story, meaning other tech stocks could also produce “once-in-a-generation” growth as they stage recoveries.

Asking different investors can also increase the odds of finding such stocks, and three Motley Fool contributors suggest that Palantir Technologies (PLTR 2.13%), Axon (AXON 1.00%), and Sea Limited (SE 3.46%) could become such investment opportunities.

Jake Lerch (Palantir Technologies): What makes for a once-in-a-generation stock buying opportunity? For me, the most important factor is a secular growth story. And today, nothing fits that bill better than the rise of artificial intelligence. So it should come as no surprise that my pick is an AI stock: Palantir Technologies.

Palantir specializes in AI-driven data analysis and pattern recognition. Through its software platforms, Palantir can help various organizations achieve very different ends. On the one hand, it could help law enforcement track and apprehend cybercriminals. On the other, it might assist healthcare organizations deliver better outcomes to patients.

In short, almost every organization today could benefit from its products in some capacity. Moreover, AI is only getting better. As it improves, the results it can deliver will also scale — making Palantir’s products even more appealing to organizations looking to increase revenue, cut costs, or improve customer satisfaction.

Best of all for potential investors, Palantir remains in the early stages of its life cycle. The company got its start partnering with governmental organizations — law enforcement, national security agencies, and military branches. Recently, however, Palantir’s commercial customer base has expanded.

In its most recent quarter (the three months ending on Dec. 31, 2023), Palantir reported commercial revenue of $284 million — up 32% from a year earlier and representing 47% of its overall sales. American-based commercial revenue grew even faster — 70% year over year.

To sum up, American companies are flocking to Palantir. Yet, the company still has ample room to grow — a fantastic combination for investors.

Justin Pope (Axon Enterprise): Years from now, investors may look back at Axon as a generational company that hid in plain sight. The company started with Tasers but has evolved into a full-fledged technology business offering cloud-based solutions for law enforcement.

In addition to non-lethal weapons, Axon sells body cameras and cloud-based software for evidence management and law enforcement operations. These products help protect law enforcement and citizens, ensuring accountability from all parties.

Axon’s revenue has grown virtually uninterrupted for years, benefiting from dependable government budgets:

AXON Revenue (TTM) data by YCharts

Today, Axon has over 17,000 customers, and the business boasts a 122% net revenue retention rate, meaning that solid growth is baked into the business even without it acquiring new customers.

The stock has already been a big winner. Shares have returned a staggering 54,000% over their lifetime. Axon could continue to deliver. The business still does “just” $1.5 billion in annual revenue.

Management estimates that its current addressable market is $63 billion, leaving a clear opportunity for growth over the coming decade and beyond.

Will Healy (Sea Limited): Considering the successes of Amazon and MercadoLibre, e-commerce conglomerates have become a source of outsize investor returns. As these e-commerce companies branched out into tech-based businesses, they leveraged their names and frequently-visited websites into multiple sources of revenue.

Fortunately, investors who missed out on these companies may have an opportunity in Sea Limited. Sea Limited started as gaming company Garena but since branched out into Shopee e-commerce and a fintech arm, SeaMoney.

Sea operates in the often-forgotten Southeast Asian market. Its core markets in that region constitute an addressable market of more than 630 million people, nearly double the population of the U.S.

Also, the stock is down by around 85% from its 2021 high. Garena’s loss of Free Fire in the Indian market and Shopee’s missteps in Europe and Latin America led to a massive sell-off in the stock.

However, Shopee has refocused on Southeast Asia, announcing on the fourth-quarter 2023 earnings call that it is investing heavily in logistics in its home region to bolster its competitive advantage. Also, Garena has addressed security concerns and appears close to regaining approval to operate in India.

Recovery in gaming could be game-changing for Sea Limited. In 2023, its revenue of $13 billion grew 5%. Nonetheless, Shopee’s revenue rose 24% during that time, while SeaMoney experienced a 44% increase. Thus, reversing the 44% revenue decline in Garena would likely bring back massive growth on a companywide basis.

Moreover, Sea earned $163 million in net income in 2023, its first yearly profit and a milestone that increases its appeal as an investment. Analysts expect Sea to build on that growth, forecasting an earnings increase of 116% this year and a 159% profit surge in 2025.

Assuming those forecasts come to pass, such improvements could bring about a dramatic recovery in Sea Limited stock, bringing investors to the forefront of the massive and potentially lucrative Southeast Asian market.

What could be more magnificent than Nvidia? Analysts think these stocks could be going forward.

Nvidia (NVDA 2.45%) has been the darling of Wall Street for a while. The chip stock skyrocketed nearly 240% in 2023, and so far this year, its shares are up around 80%.

But analysts don’t expect this sizzling momentum to continue. The consensus price target for Nvidia is barely above its current share price. Here are three “Magnificent Seven” stocks Wall Street thinks will soar more than Nvidia over the next 12 months.

Apple (AAPL 0.45%) has been a laggard in 2024. It even lost the spot as the biggest company in the world, based on market cap, to Microsoft. However, analysts are more bullish about Apple than any other Magnificent Seven stock right now.

The average 12-month price target for Apple reflects an upside potential of over 9%. Of the 36 analysts surveyed by LSEG in April, 32 rate the stock as a buy or a strong buy. The others recommend holding the stock.

It might be surprising that Wall Street is so optimistic about Apple. The tech giant’s sales growth has slowed considerably, and its valuation is relatively high, with shares trading at a forward earnings multiple of nearly 26.

Analysts, though, could be anticipating a catalyst with Apple’s June developer conference. The company is widely expected to unveil its generative AI strategy at the event.

Amazon (AMZN 2.82%) hasn’t delivered Nvidia’s jaw-dropping returns. However, the e-commerce and cloud services leader nonetheless pleased investors with a gain of 80% last year and a 20% jump so far this year.

Wall Street thinks Amazon can move even higher. The consensus price target for the stock is roughly 6.5% above the current share price. Forty-three of the 47 analysts surveyed by LSEG in April rate Amazon as a buy or a strong buy.

Generative AI continues to provide a major tailwind for Amazon Web Services (AWS), as customers like to run apps where their data is. Since AWS commands the leading market share among cloud platforms, it’s where many organizations are training and deploying their generative AI apps.

Amazon’s advertising business is also enjoying strong momentum. The company is using AI to boost the relevancy of the ads displayed to customers. It has also expanded advertising on Prime Video.

Shares of Google parent Alphabet (GOOG 1.32%) (GOOGL 1.31%) jumped 58% in 2023. The stock is up over 10% year to date in 2024. Like Apple and Amazon, Alphabet still has more room to run in Wall Street’s view.

The average analyst’s 12-month price target is nearly 6% higher than the current price. Wall Street is overwhelmingly bullish about the tech stock, with 38 of the 43 analysts surveyed by LSEG in April rating Alphabet as a buy or a strong buy.

Alphabet’s Google unit has experienced a couple of embarrassments with its generative AI apps — first, with Bard last year, and more recently, with Gemini earlier this year. However, these missteps don’t seem to have concerned analysts very much. They’re more focused on the growth opportunities for Google Cloud and Google’s continued dominance in search. Some also have great long-term expectations for Alphabet’s Waymo self-driving car business.

You can’t depend on Wall Street’s price targets. Even highly paid analysts focused on scrutinizing companies’ operations can’t predict the future with a high level of accuracy. However, I suspect Wall Street could be right about Apple, Amazon, and Alphabet. They could be right about Nvidia, too.

Nvidia could continue to soar higher, but competition is increasing. Any hiccup could cause the stock to tumble. I think Apple’s shares could jump on good news at the upcoming developer conference. Amazon and Alphabet should deliver solid growth in the next few quarters, largely due to the generative AI tailwinds.

Wall Street isn’t always right. In this case, though, I agree with the analysts’ takes on these Magnificent Seven stocks.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Keith Speights has positions in Alphabet, Amazon, Apple, and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Either gold shares rise from here or gold prices take a dive.

Source link