These Stocks Are Screaming Recession. It’s Almost Time to Buy Them.

Source link

These Stocks Are Screaming Recession. It’s Almost Time to Buy Them.

Source link

Almost Half of Warren Buffett’s $337 Billion Portfolio Is Invested in Only 1 Stock

This Forecasting Tool Hasn’t Been Wrong Since the 1960s, and It Offers a Very Clear Picture of What’s Next for Stocks

Cathie Wood’s Ark Invest Is Selling Tesla and Nvidia, and Buying 1 Little-Known Artificial Intelligence (AI) Growth Stock

1 Stock-Split AI Growth Stock to Buy Now Before It Soars 860%, According to Cathie Wood’s Ark Invest

The September jobs report exceeded expectations with the addition of 336,000 jobs last month, nearly double the amount anticipated on Wall Street.

Add that ‘goldilocks’ figure to minimal wage inflation, and the scene is set for a soft landing for the economy, says Wedbush’s Daniel Ives, a 5-star analyst rated in the top 2% of the Street’s stock pros. This, in turn, is great news for the tech sector. In fact, with earnings season about to kick off, Ives thinks Wall Street is poised to be caught off-guard by the strength of reporting, laying the groundwork for a big end-of-year surge.

“Our view is that 3Q earnings over the coming weeks will be an eye-opener for the Street, as the transformational AI growth and stabilizing IT spending environment will create a massive tech rally heading into year-end, during which we expect tech stocks to be up another 12%-15% in 4Q,” Ives opined.

While Ives acknowledges that bears may try to temper the bulls’ enthusiasm, his advice remains clear: Ignore the noise and direct your attention towards the potential of this generational AI growth, with $1 trillion in tech spending anticipated on the horizon over the next decade.

With the prospect of all this about to take place, Ives believes certain names are well-positioned to gain, and we decided to take a closer look at some of his picks. Do these equities receive support from the rest of the Street? According to the TipRanks database, they certainly do; both are rated as ‘Strong Buys’ by the analyst consensus. Let’s see what makes them so.

Progress Software (PRGS)

We’ll start with a leading American infrastructure software company, the aptly titled Progress Software. This firm specializes in providing a wide range of software tools and solutions to help businesses enhance their operational efficiency and accelerate digital transformation. Since being founded in 1981, Progress has established itself as a trusted partner for enterprises seeking to harness the power of data and applications in an evolving digital landscape.

The company’s product portfolio includes a variety of software platforms, such as Progress OpenEdge, which enables the development of robust, scalable business applications, and Progress Telerik, a suite of developer tools for building modern web and mobile applications.

Progress’ customer roster is notably extensive, encompassing a diverse array of prominent clients, including Meta, Microsoft, IBM, Barclays, and S&P Global.

All the above helped the company deliver a strong fiscal Q3 report (August quarter). Revenue climbed by 15.7% year-over-year to $175 million, beating the Street’s forecast by $1.9 million. Adj. EPS of $1.08 also exceeded expectations by $0.08.

The company also delivered a net retention rate – a key software metric – above 100% and is actively seeking out its next M&A transaction. Earlier in the year, the company closed the $355 million acquisition of the document-oriented database operator MarkLogic.

For Daniel Ives, the prospect of more such activity is enticing and should further cement its standing in the space.

“The company continues to maintain an accretive M&A strategy as this environment now provides an attractive opportunity for PRGS to capitalize on a diminished valuation marketplace with $138.0 million in cash to spend on undervalued assets coming to market,” Ives explained. “We maintain our bullish stance on Progress as the company improves its cost structure while positioning to capitalize on growing demand for its entire product portfolio while maintaining an accretive inorganic growth strategy.”

These comments form the basis for Ives’ Outperform (i.e., Buy) rating on PRGS, while his $65 price target makes room for 12-month returns of 23%. (To watch Ives’ track record, click here)

In general, other analysts echo Ives’ sentiment. 3 Buys and 1 Hold add up to a Strong Buy consensus rating. Based on the average price target of $63.75, the upside potential comes in at ~21%. (See PRGS stock forecast)

Microsoft (MSFT)

If we’re talking about tech and how companies stand to gain from the AI revolution, then not much digging is required to get to one of the firms that stands to benefit the most. Microsoft has been at the forefront of tech’s rise, has played a pivotal role in shaping the modern technology landscape, and only Apple ranks higher on the list of the world’s most valuable companies.

Its ubiquitous Windows operating system is used by billions of computers worldwide, and it also offers a wide range of software applications and services, including the Microsoft Office suite, Azure cloud computing platform, and the Xbox gaming console.

Microsoft is also betting big on AI. It is heavily invested in ChatGPT maker OpenAI and has already announced that Microsoft CoPilot – the AI assistant feature for Microsoft 365 applications – is set to become widely available for enterprise customers next month.

Its positioning in this burgeoning space has given investors plenty to cheer about this year, and as with other tech giants, Microsoft has enjoyed the spoils of 2023’s bull market (up by 38%), even if its fiscal fourth quarter of 2023 (June quarter) report failed to entirely please.

On the face of it, there was little to worry about. Revenues reached $56.2 billion, representing an 8.3% year-over-year uptick and beating the consensus estimate by $710 million. Likewise, EPS of $2.69 came in ahead of the $2.55 anticipated on Wall Street.

However, along with Cloud service Azure’s revenue showing some deceleration, for F1Q, the company guided for revenues between $53.8 billion to $54.8 billion, which is at the midpoint, lower than the $54.94 billion the Street was hoping for.

While Ives is cognizant of the worries regarding growth, all signs are that there is little need for concern, especially with the anticipated AI windfall about to take place.

“Since Microsoft reported its June quarter investors have been in a ‘wait and see’ mode on the cloud growth trajectory of Redmond and most importantly when the AI monetization opportunity will start to show up in numbers,” Ives said. “We believe while management has talked about a ‘gradual ramp’ for AI monetization in FY24 we believe so far the adoption curve is happening quicker than expected based on our recent checks. Our latest Azure checks also show a clear uptick in activity sequentially (AI driven) which gives us further confidence in Microsoft exceeding its 25%-26% Azure growth guidance in FY1Q.”

Conveying his confidence, Ives rates MSFT shares as Outperform (i.e. Buy) backed by a $400 price target, suggesting the stock will post growth of 21% over the one-year timeframe.

Overall, MSFT gets a Strong Buy consensus rating, based on a mix of 30 Buys against 4 Holds. The average target is almost identical to Ives’ objective, and at $397.19 allows for share gains of 20% over the coming months. (See Microsoft stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

U.S. stocks ended higher Monday, shaking off early losses that followed the weekend attack by Hamas on Israel, as investors focused on remarks by Federal Reserve officials

Stocks bounced Friday after a stronger-than-expected September jobs report, allowing the S&P 500 to rise 0.5% for the week and break a streak of four straight weekly declines. The Dow saw a 0.3% weekly decline, while the Nasdaq Composite rose 1.6%.

Declines for equities were pared in morning trade after remarks by Dallas Federal Reserve Bank President Lorie Logan were seen as indicating a surge in long-term Treasury yields may mean the central bank has less need to further raise interest rates. Stocks extended early afternoon gains after remarks by Fed Vice Chair Philip Jefferson that also highlighted a rise in long-term yields.

Jefferson said that a sharp rise in long-term yields could be the result of investors concluding that the underlying momentum of the economy was stronger than previously thought and the Fed would need to keep rates higher for longer. But it could also arise from changes in investor attitudes toward risk and uncertainty.

“Looking ahead, I will remain cognizant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy. I will be taking financial market developments into account along with the totality of incoming data in assessing the economic outlook and the risks surrounding the outlook and in judging the appropriate future course of policy,” Jefferson said.

Logan, in a speech, said that if interest rates “remain elevated because of higher term premiums, there may be less need to raise the fed-funds rate. However, to the extent that strength in the economy is behind the increase in long-term interest rates, the FOMC may need to do more.”

Jefferson’s call to proceed carefully in a sensitive period for risk management “conveys no urgency to hike again,” said Krishna Guha, economist at Evercore ISI, in a Monday afternoon note.

Still, it was defense stocks that led the rebound. The iShares U.S. Aerospace & Defense ETF

ITA

rose 4.5% to close at $108.72.

The attack by Hamas on Israel raised fears of a broader conflict, sending crude prices higher and spurring haven-related support for gold, the dollar and U.S. Treasury futures.

The cash Treasury market was closed on Monday for Columbus Day and Indigenous Peoples’ Day, but futures

TY00,

indicated falling benchmark yields.

See: Gold, U.S. dollar rally as investors flock to havens as Israel-Hamas war escalates

U.S. stocks saw only modest pressure, however.

“Global risks have clearly risen but in the short term, the U.S. remains the global safe haven, given the weakness in the economies of China and Europe, and should result in funds flows in our direction, though it may make things more vulnerable to earnings disappointments and subdue the rally on positive earnings surprises,” said Louis Navellier, founder of Navellier & Associates

Commodities Corner: Here’s what will drive oil prices as Israel-Hamas war continues

The price of Brent crude

BRN00,

the global energy benchmark, rose 4.2% amid concerns that oil supplies from the region may be compromised. Crude fell back significantly last week, however, after trading near $100 a barrel in September.

Read: Tom Lee points to uncomfortable upside for U.S. stocks of Israel-Hamas conflict

Meanwhile, the U.S. producer and consumer prices data for September will be published on Wednesday and Thursday, respectively, with further evidence of easing price pressure required to cement no more rate increases by the Federal Reserve this year.

Then Friday sees the start proper of the third-quarter company-earnings season, when big banks such as JPMorgan Chase

JPM,

Citigroup

C,

and Wells Fargo

WFC,

present their results.

Earnings Watch: Q3 earnings are here: S&P 500 heads toward year of profit declines as JPMorgan, and Delta report this week

The Federal Reserve will hold its penultimate FOMC meeting on October 31-November 1, and the odds that they’ll institute another interest rate hike have just jumped. The September jobs report came in, showing employment levels far above the forecast – 336,000 new jobs in the month, compared to the 170,000 expected – and that means increased inflationary pressures. Analysts now put the odds of a quarter-percent rate hike at 29%.

The messages here are mixed. The jobs numbers look good – but increased employment also risks increasing wage inflation, which increases pressure on the Fed to fire their only weapon against inflation – further interest rate hikes. The Fed has already signaled that it will hold rates ‘higher for longer,’ and bond yields are hovering near 16-year highs. This, in turn, puts pressure on stocks, as investors go seeking the highest returns.

With all of this in mind, it’s probably time to consider getting into dividend stocks. These equities offer investors the advantage of a steady passive income no matter how the markets turn.

Goldman Sachs analyst John Mackay has tapped two high-yield payers as choices for investors to buy now. According to TipRanks’ database, these are Buy-rated stocks with dividend yields of at least 8%. Let’s take a closer look.

MPLX LP (MPLX)

We’ll start with a well-known name in the hydrocarbon midstream industry, MPLX. This company spun off from Marathon Petroleum more than a decade ago, to operate the parent company’s midstream transport assets – and today MPLX is a major player in North America’s oil and natural gas midstream niche, boasting a $35 billion market cap and a continent-spanning asset network.

That asset network includes a pipeline web, terminal points, and river fleet of tugs and barges. These transportation assets link production regions and wellheads with oil and gas storage facilities, tank farms, gas refineries, and, on the coast, export terminals. Finally, in addition to moving crude oil and natural gas, MPLX also has a hand in the transport and distribution of refined fuel products.

All of this is big business, and MPLX consistently generates $2 billion-plus in quarterly revenues. In the last quarter reported, 2Q23, the company saw a top line of $2.69 billion; this total was down 8.5% from the prior year, and missed the forecast by some $18.6 million. At the bottom line, however, the company’s EPS came in at 91 cents per share by GAAP measures, or 4 cents per share better than had been anticipated. The EPS figure was also 8 cents per share better than the 2Q22 result.

MPLX will release its next set of quarterly results this coming October 31, and there is one more metric that should interest dividend investors. The company’s Q2 distributable cash flow was reported as $1.315 billion – up some 6.3% and available to support the company’s common share dividend.

That dividend was last paid out on August 14, at a rate of 77.5 cents per share, and the annualized rate, of $3.10, gives an impressive yield of 8.8%. MPLX has a dividend history stretching back some ten years, during which it has been gradually raising the payment.

Goldman Sachs’ John Mackay sees the dividend as a selling point for investors here, and also part of a comprehensive ability, on the part of MPLX, to generate returns.

“MPLX maintains a high-quality asset mix, producing stable cash flows supported by minimum-volume commitments with MPC… Since repairing the balance sheet, management has been committed to a creating a premier capital return framework which now includes annual base distribution increases coupled with opportunistic buybacks. We ultimately see MPLX as a premier capital return vehicle vs the rest of our coverage universe, as steady and growing FCF generation supports sizable dividend increases with room on the balance sheet for buybacks,” Mackay opined.

Quantifying his stance, the Goldman Sachs analyst goes on to rate MPLX shares as a Buy, and his price target of $40 implies ~14% upside in the next 12 months. Combine that with the dividend, and the return can approach 22%. (To watch Mackay’s track record, click here)

Overall, we’re looking at a stock with a Moderate Buy rating from the Street, a rating supported by 8 recent analyst reviews with a breakdown of 6 Buys, 1 Hold, and 1 Sell. Shares are currently trading for $35.13, and their average target price of $40.88 suggests a one-year gain of 16%. (See MPLX stock forecast)

Hess Midstream Partners, LP (HESM)

Next up is another oil and gas midstream company. Hess Midstream Partners, like MPLX above, got its start as a spin-off, splitting from Hess Oil and holding its IPO in 2017. As an independent operator, Hess Midstream inherited the parent company’s pipeline and midstream operations. Today, Hess Midstream owns and operates a solid network of oil and gas transport assets, with its main operational focus on the Williston Basin, one of the rich production areas in the Dakota-Montana border area and part of the larger Bakken formation that got North America’s fracking revolution started.

Hess Midstream focuses on transporting crude oil, natural gas, and various water and fluid products generated by the fracking industry. The company’s network of gathering, processing & storage, and terminal & export services fills a vital niche in one of North America’s richest oil and gas production basins and forms the base for the firm’s recent forecast-beating financial results.

In the company’s last quarterly report, for 2Q23, Hess Midstream reported a top line of $324 million, up ~3% from the $313.4 million reported in 2Q22. The company’s earnings, at 50 cents per share, were based on a net income of $25.1 million. Hess Midstream’s distributable cash flow, $202.6 million, was down slightly from the $206.2 million in the prior-year quarter – but was still sufficient, with the earnings, to cover the dividend payment.

This midstream company set its common share dividend at $0.6011 per common share, for an annualized payment of just over $2.40 per share. This payment, which last went out on August 14, yields 8.45%. Hess Midstream has been keeping up a reliable dividend payment, with frequent supplemental payments since 2017.

Checking in again with John Mackay, we find the Goldman analyst is sanguine about Hess Midstream’s ability to maintain performance from its Bakken footprint. He wrote, “We see HESM as best positioned in the Bakken among its smid-cap peers given its large exposure to, and favorable contracts with, its sponsor HES. Our GS E&P research team sees HES oil production growing faster relative to the Bakken overall, making HESM better exposed vs. peers facing softer overall Bakken growth, as HES continues to reiterate its 200 kboe/d target in 2025 and expects to hold this production going forward…”

These comments support Mackay’s Buy rating on HESM, while his $32 price target points toward a 12% upside potential – or more than 20%, when the dividend is added to it.

Zooming out to the macro view, we find that Hess Midstream has picked up 5 recent analyst reviews, and their split, 3 Buy and 2 Holds, gives the shares a Moderate Buy consensus rating. With an average price target of $34.40 and a trading price of $28.47, HESM stock has ~21% upside potential. (See HESM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Fears about rising bond yields are way overblown. This has turned investor sentiment quite dark — and created a textbook contrarian buy signal.

Here are six reasons why you can feel confident betting against the gloom and doom crowd and put money into the market — especially in economically sensitive cyclical stocks.

1. Bond yields are up because of tax-loss selling, which will end soon: Portfolio managers avoided stocks and loaded up on bonds in 2022. We know this because the sell-side suggested bond exposure was near all-time highs last year and this year as well.

Now, portfolio managers are sitting on huge losses in bonds. The iShares 20+ Year Treasury Bond exchange-traded fund

,

for example, is down almost 50% from highs in 2020, and more than 40% from the start of 2022, when investors favored bonds over stocks because of U.S. recession fears.

“ Money managers have until the end of October to finish tax-loss selling. ”

Money managers have until the end of October to finish tax-loss selling. They do not wait until the last day, which means this downward pressure on bond prices will ease sooner than that.

2. Bonds are down because of renewed concerns about Fed tightening: We know this because of how bonds react to economic data. Bonds fell on October 3 after the Bureau of Labor Statistics reported an unexpected jump in August job openings to 9.61 million. The data had investors worried that interest rates will stay higher for longer. Conversely, bonds were strong (yields fell) on October 4 in part on news that Automatic Data Processing

ADP

reported weak employment data.

“ It is pretty easy to make the case that inflation is under control. ”

This hyperfocus on inflation-related data seems misplaced, because it is pretty easy to make the case that inflation is under control. The Consumer Price Index (CPI) and the core CPI are in the low 2% range, excluding rent. Yes, rent inflation matters, but inflation in new leases is winding down, coming in at 3.4% in August. “Growing multifamily supply keeps new-lease rent growth subdued,” Goldman Sachs economist Jan Hatzuis says.

As for the wage-price spiral investors are worried about, the trendline in job openings relative to the labor supply tells the era of big wage hikes is winding down.

Goldman estimates the personal consumption expenditures (PCE), another inflation measure, will continue to fall, hitting 2.4% in December 2024.

In fact, this is arguably an ideal environment for investors, given the favorable mix of strong growth and declining inflation, says market strategist and economist Jim Paulsen. “Through the lens of another time we would be rejoicing,” he says.

3. This is the market’s “spooky season,” but it always comes to an end: The U.S. stock market normally hits annual lows in October. This is partly because institutional investor tax-loss selling has to finish by month-end. But it also has to do with the weather. People traditionally go into harvest and caution mode (raise cash) ahead of the cold season.

4. Bonds are weak because “bond vigilantes” are sending the government a message: Bond investors reacted poorly (selling bonds, driving up yields) this past Monday due to the federal budget deal announced Sunday. It contained no real budget cuts and is temporary. The bond vigilantes were telling Washington, D.C. to get the budget under control, says Ed Yardeni of Yardeni Research.

This weight on bond prices is harder to dismiss. One reason is the House of Representatives now has no leader, which increases the odds of a government shutdown on November 17 when the stopgap budget deal expires, says Goldman Sachs economist Alec Phillips.

That might not be a bad thing if it pressures politicians to strike a longer-lasting deal, which they typically do. Even Yardeni, who is quite concerned about the impact of the bond vigilantes pushing up yields, still sees 10-year Treasury bond yield settling at around 4.5%-5%.

5. 10-year bond yields are not that high, historically speaking: The 10-year Treasury bond yield has moved back to the 4%-5% that prevailed from 2003 to 2007, which was a good time to own stocks. For example, the SPDR S&P 500 ETF Trust

rose about 80% in that period. Indeed, rising rates have not hurt the U>S. economy this time around. “This raises the possibility that the economy can live with the bond yield back to its old normal level,” Yardeni says.

6. Investor sentiment is extremely weak — a bullish sign: The Investors Intelligence bull/bear ratio recently fell to 1.77. Historically, below 2.0 is a clear buy signal, in the contrarian sense (enough bearishness to be bullish). Meanwhile, the American Association of Individual Investors (AAII) bull/bear spread jumped to 13 percentage points at the end of September when 27.8% of respondents were bullish vs. 40.9% bearish. This historically wide spread confirms the bull-bear ratio signal.

Buy stocks. Sentiment is extremely weak. But analyst earnings estimate revisions suggest this reporting season will be strong. The fourth quarter should be solid, too. The Atlanta Fed GDP now estimates 4.2% growth. Strong economic growth normally means strong earnings growth.

Read: Here’s a roadmap for stocks to own and avoid this earnings season

Also: Let’s debunk the bears’ top arguments against further stock market gains

Also, note that the historic low for the year in stocks is just around the corner. On average, the SPDR S&P 500 ETF bottoms on October 12, notes Jason Goepfert at SentimentTrader.

Investor worries about an overly aggressive Fed hurting growth has hit cyclical stocks hard. So they look attractive. To keep things simple, go with ETFs. Consider Fidelity MSCI Consumer Discretionary ETF

,

Fidelity MSCI Industrials ETF

,

Fidelity MSCI Materials ETF

and SPDR S&P Oil & Gas Exploration & Production (XOP

).

For stocks, investment researcher Morningstar singles out Devon Energy

DVN,

which pays a 7.5% yield, and TC Energy

TRP

(8.2% yield) in energy, and Park Hotels & Resorts

PK

(5.14% yield) in consumer discretionary.

When yields rise, prices of dividend stocks decline, pushing up their yields. Utilities have been particularly hard hit. For exposure, consider the Fidelity MSCI Utilities Portfolio

(3.24% yield). For stocks, Morningstar particularly likes Duke Energy

DUK

(4.78% yield) and Entergy

ETR

(4.75% yield).

Otherwise consider bonds to lock in some decent yield, via the iShares 20+ Year Treasury Bond ETF. “We still expect that inflation will continue to moderate, making bonds look even more attractive to investors,” Yardeni says.

Michael Brush is a columnist for MarketWatch. At the time of publication, he had no positions in any stocks mentioned in this column. Brush has suggested DVN in his stock newsletter, Brush Up on Stocks. Follow him on X @mbrushstocks.

Also read: How rapidly rising Treasury yields are shaking up financial markets — in 5 charts

Plus: Banks are bracing for a recession as Treasury yields surge

Social Security’s Cost-of-Living Adjustment (COLA) Will Be Missing Its Silver Lining in 2024

3 Stocks to Hold for the Next 20 Years

The Social Security COLA Countdown Is On: Here’s How Much Your Increase Is Likely Going to Be

Should You Take Social Security at Age 62, 65, or 70? A Comprehensive Analysis Offers a Very Clear Answer

2022 was a tough year for many of the best stocks to buy and watch in part due to rising interest rates and an increasingly hawkish Federal Reserve. But a select number of stocks to buy and watch in the technology sector are acting better, even with the stock market in a correction.

X

After hitting a low of 3.3% in early May, the 10-year Treasury yield recently surged above the 4% level to a 16-year high as Wall Street weighs the prospects of another interest rate hike by the Federal Reserve before the end of the year.

At one point, fears of a recession and concerns about contagion in the financial sector after the collapse of SVB Financial and Signature Bank made it an extremely challenging environment for many of the best stocks to buy and watch. But buyers lifted the stock market off lows in August as hopes grew for a soft landing for the U.S. economy. A follow-through day on Aug. 29 didn’t have much of a chance when the Nasdaq suffered a stalling session two sessions later. Sellers came back into the stock market after that.

Stocks with high P-E ratios like Tesla (TSLA) and Nvidia (NVDA) were hit hard by institutional selling in 2022, along with security software stocks like CrowdStrike (CRWD) and Zscaler (ZS).

A rising interest rate environment isn’t good for the best stocks to buy in the tech sector with high multiples. Why? Because it makes for a more challenging operating environment. If the stock market senses any possibility of a slowdown in earnings growth from high P-E names, the selling will hit these stocks first.

The best stocks to buy and watch aren’t hard to find, as long as you’re fishing in the right pond. Top stocks like Arista Networks (ANET) and Nutanix (NTNX) don’t get a lot of attention, but both have characteristics seen in past stock market winners before big price moves.

The best stocks to buy and watch boast strong fundamentals along with leading price performance in their industry group. Many also show favorable fund ownership trends.

The best tech stocks also tend to show resilience in down markets. Use IBD Stock Checkup to quickly identify industry group leaders with the potential to be stock market leaders.

Join IBD experts as they analyze leading stocks in the stock market rally on IBD Live

Screening for the best stocks to buy and watch is as easy as looking at the MarketSmith Growth 250, a daily screen of high-quality stocks. Click on any column header to sort the screen as you wish, either by those closest to their highs, stocks with the highest Composite Rating, or stocks trading up in price with the heaviest volume.

The best stocks to buy and watch aren’t guaranteed to be huge stock market winners. But they do have qualities seen in past stock market winners before big price gains.

The best tech stocks to buy and watch now include ANET stock, NTNX, CrowdStrike, Adobe (ADBE) and Synopsys (SNPS).

The Nasdaq composite and S&P 500 flashed follow-through days on March 29, putting the stock market in a confirmed uptrend. But distribution days started to crop up in the Nasdaq and S&P 500, resulting in a strong headwind for stocks. IBD put the market trend in correction after the Aug. 17 market close. A follow-through on Aug. 29 was immediately met by distribution. The uptrend went under pressure on Sept. 7. Soon after that, on Sept. 20, IBD put the market status in correction again.

When new institutional money starts to come in from the sidelines, the best stocks to buy and watch could easily resume their market leadership, helped in part by strong fundamentals.

One of the best stocks to buy in the security software group, CrowdStrike gapped up on Aug. 31 after the company reported its second straight quarter of accelerating earnings growth.

Adjusted profit surged 106% to 74 cents a share. Revenue growth was also impressive, up 37% to $731.6 million, helped by continued strong performance of its AI-powered Falcon platform.

Subscription revenue increased 36% to $690 million. CRWD also lifted its earnings and revenue guidance for its current fiscal year 2024.

For fiscal 2024, annual earnings are expected to surge 84%, with growth slowing a bit in fiscal 2025, up 24%.

CRWD continues to hold support at its 10-week line, a rarity in the technology sector these days, while trading near a 166.99 alternate entry.

Composite Rating: 99 (on 1-99 scale with 99 tops)

Latest-quarter EPS % change: +106%

Latest-quarter sales % change: +37%

Five-year annualized EPS growth rate: 164%

Annual return on equity: 30%

Up/down volume ratio: 1.5

The provider of cloud networking software for data centers looked dead in the water when ANET stock gapped below its 50-day line on July 28. But a bullish earnings report on July 31 brought buyers back into the stock in spades. ANET has held gains and is one of the best stocks to buy as it as it trades just past the 5% buy zone from a 178.36. Trading has tightened up as the stock holds support at the 10-week moving average.

Arista Networks shows bullish earnings and revenue growth in recent quarters, fueled by strong demand for its cloud networking software and hardware for the fast-growing data center market.

Over the past eight quarters, revenue growth has ranged from 24% to 57%.

Full-year earnings are expected to rise 35% this year and 10% in 2024.

Composite Rating: 98

Latest-quarter EPS % change: +46%

Latest-quarter sales % change: +39%

Five-year EPS growth rate: 21%

Annual return on equity: 33%

Up/down volume ratio: 1.7

The company operates an enterprise cloud platform that combines server, virtualization and storage applications into one solution.

Like CrowdStrike, Nutanix also gapped up in late August after the company reversed a year-ago loss with adjusted profit of 24 cents a share. Revenue growth accelerated from the prior quarter, rising 28% to $494.2 million.

“Our fiscal year 2023 results demonstrated a good balance of growth and profitability and further strengthened our balance sheet,” said Rukmini Sivaraman, CFO of Nutanix. “In conjunction with our earnings release, we’re pleased to announce that our Board of Directors has authorized the repurchase of up to $350 million of our stock, which we see as a reflection of confidence in the company’s long-term market opportunity and financial outlook.”

During the quarter, Nutanix and Cisco Systems (CSCO) announced a partnership to accelerate hybrid multicloud adoption.

Nutanix cleared a long consolidation during the week ended Sept. 1. It’s held gains well since then and is still in the 5% buy zone from a 33.73 entry.

Composite Rating: 92

Latest-quarter EPS % change: 24 cents vs. loss of 17 cents

Latest-quarter sales % change: +28%

Five-year annualized EPS growth rate: n/a

Annual return on equity: n/a

Up/down volume ratio: 1.3

The leader in design, imaging and publishing software recently lost support at its 10-week moving average, but it’s less than 10% off its high while holding support near the 500 level.

The company on Sept. 15 reported another quarter of accelerating earnings growth, with adjusted profit up 20% to $4.09 a share. Revenue increased 10% to nearly $4.9 billion.

Revenue at the company’s Digital Media segment increased 11% to $3.59 billion; Creative revenue rose 11% to $2.91 billion and Document Cloud revenue gained 13% to $685 million.

“We are unleashing a new era of AI-enhanced creativity around the world with innovations across our product portfolio, including the recent launches of Firefly, Express, Creative Cloud and GenStudio” said Shantanu Narayen, Adobe CEO.

Several heavy-volume declines in recent days have knocked Adobe’s Accumulation/Distribution Rating down to a neutral C-.

A move above the 10-week line would strengthen ADBE’s technical picture as it works on a base. For now, it’s a potential resistance level to watch.

Composite Rating: 98

Latest-quarter EPS % change: +20%

Latest-quarter sales % change: +10%

Five-year annualized EPS growth rate: 20%

Annual return on equity: 45%

Up/down volume ratio: 0.8

The provider of electronic design software for the semiconductor industry is holding near highs as it tries to break out past a 471.15 entry. But that could be a tough task with the stock market in a correction.

It’s one of best stocks to buy in the design software group, helped by one of the most consistent track record of earnings growth around. Annual earnings have increased every year since at least 2016.

SNPS soared above its 50-day moving average on Aug. 17 as investors cheered the company’s second straight quarter of accelerating revenue growth.

Revenue increased 19% to $1.49 billion. Adjusted profit jumped 37% to $2.88 a share.

Annual earnings estimate are strong, with fiscal 2023 profit expected to rise 26%, with 23% growth forecast for fiscal 2024.

Composite Rating: 98

Latest-quarter EPS % change: +37%

Latest-quarter sales % change: +19%

Five-year EPS growth rate: 24%

Annual return on equity: 26%

Up/down volume ratio: 1.1

Follow Ken Shreve on Twitter @IBD_KShreve for more stock market analysis and insight.

YOU MIGHT ALSO LIKE:

Join IBD Live For Stock Ideas Each Morning Before The Open

Best Growth Stocks To Buy And Watch: See Updates To IBD Stock Lists

Stay In Sync With The Market With IBD’s ETF Market Strategy

Get Free IBD Newsletters: Market Prep | Tech Report | How To Invest

What should we make of today’s market conditions? Investors are digesting how the Federal Reserve’s ‘higher for longer’ interest rate policy will impact the economy, and they’re not pleased with the prospect. Other challenges on the horizon include the ongoing Congressional budget battles, lingering inflation, the evaporation of consumer savings and purchasing power, and concerns over China’s incendiary combination of slowing growth, geopolitical ambition, and approaching demographic collapse.

That’s a lot to digest, but covering the situation from banking giant J.P. Morgan, global investment strategist Madison Faller believes there is some reason for optimism through the autumn.

“When it comes to stocks, the recent selloff means valuations are more reasonable today than they were before… Focusing on valuations alone also ignores the actual experience of companies. The S&P 500 has already suffered through three quarters of earnings declines, and expectations for future earnings have been rising steadily over the last six months. Despite all the worry, that backdrop could spur stocks to new highs over the next year… Staying invested through the uncertainty has typically served investors best,” Faller opined.

So, given this optimistic perspective, the question is, which equities should investors consider adding to their portfolios? J.P. Morgan analysts have pinpointed two names they believe would be valuable additions.

And they are not alone; according to TipRanks’ database, both stocks are also rated as ‘Strong Buys’ by the analyst consensus. Let’s see why they are drawing plaudits across the board.

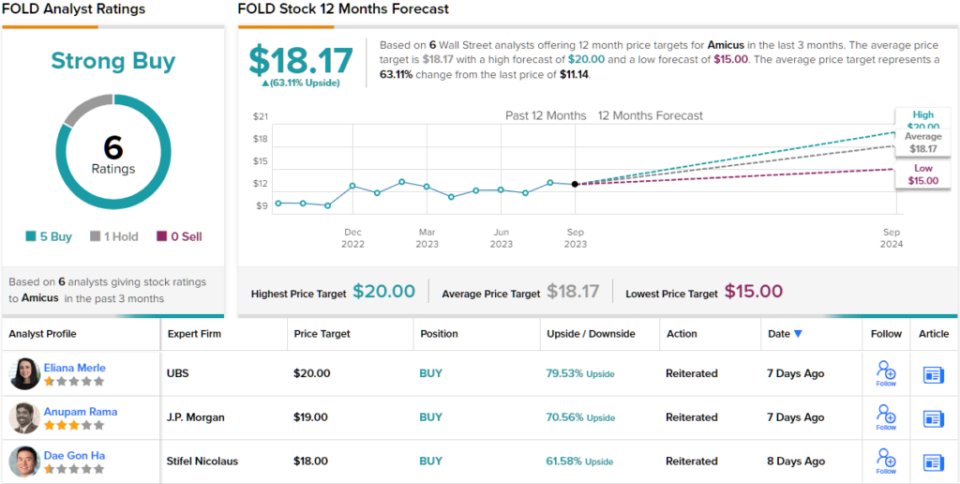

Amicus Therapeutics (FOLD)

We’ll start in the biotech sector, where Amicus is a biopharmaceutical company with a focus on the treatment of rare diseases. These are typically disease conditions with small patient bases and devastating effects. Amicus is working on new therapeutic agents with novel actions to deliver advanced treatments with a patient-centered focus.

This company has achieved its goal and reached the brass ring – it now has two approved drugs on the market. The first of these, Galafold, is a treatment for adults suffering from Fabry disease; the second is a combination therapy, Pombiliti and Opfolda, used in the treatment of late-onset Pompe disease.

These approved drugs have given Amicus a steady revenue stream. The company reported $94.5 million in global revenue for 2Q23, the last quarter reported, beating the forecast by ~$4.6 million. The revenue was also up 17% year-over-year.

Looking ahead, Amicus is predicting that sales of Galafold will show revenue growth in the 14% to 18% range for the full year 2023. The company credits this outlook to high demand and commercial expansion in the US, UK, EU, and Japanese markets. Also of note, Amicus has received regulatory approval from the EU in Q2 for the commercial launch of the Pombility+Opfolda combination therapy.

JPMorgan analyst Anupam Rama is impressed by the full commercialization potential of Amicus, writing of the company, “With peak sales of ~$600M+ for Galafold and ~$750M+ for Pombiliti + Opfolda, we believe that FOLD shares are undervalued. As Pombiliti + Opfolda was approved in Pompe disease in 3Q23, we believe that the therapy shows best-in-class potential and it has been noted that the therapy is preferred by KOLs we have spoken with…”

“Net-net, at current valuation levels, we continue to think that solid execution on the Galafold and Pombiliti + Opfolda should drive value into the mid- to high-teens / share level,” Rama summed up.

Looking ahead, Rama rates FOLD an Overweight (i.e. Buy), and sees it hitting a share price of $19 for ~71% one-year upside potential. (To watch Rama’s track record, click here)

Overall, the Strong Buy consensus rating on this stock is supported by 6 recent analyst reviews, including 5 Buys and 1 Hold. The shares are priced at $11.14 and their $18.17 average price target implies a 12-month gain of 63%. (See FOLD stock forecast)

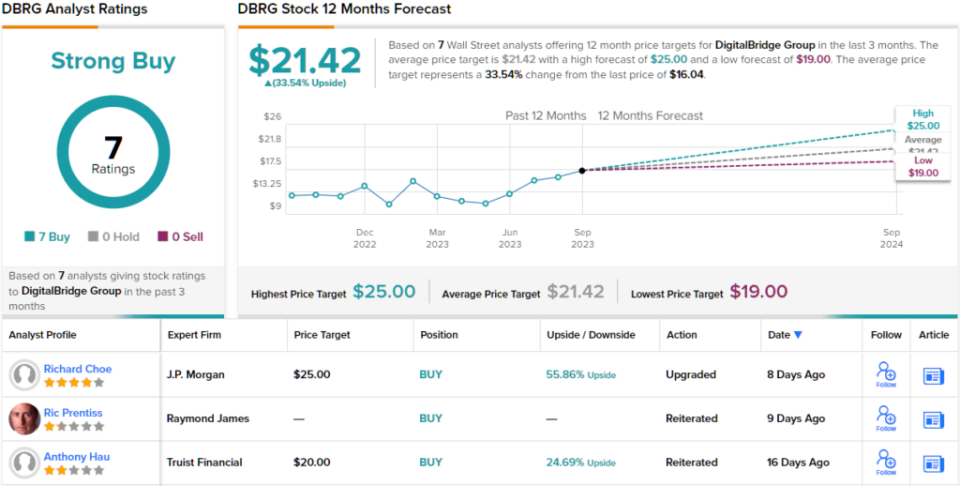

DigitalBridge Group (DBRG)

Next up is DigitalBridge, a digital investing firm with a global footprint. The company has 25 years’ experience working with businesses across the digital ecosystem, and has a network of investments in cell towers, small cells, data centers, fiber networks, and edge infrastructure. DigitalBridge buys, builds, owns, and operates these assets; it forms a vital link connecting digital providers with customers.

As of the end of 2Q23, the last reported, DigitalBridge had invested some $4 billion in portfolio growth this year. The greatest expansion took place in the data center and tower segments of the portfolio, which each grew in Q2 by more than 21% year-over-year; the company’s fiber portfolio was up more than 15%.

In global revenues, the second quarter was a good one for DigitalBridge. The company’s $425 million top line was up a modest 2% y/y, but it beat the forecast by more than $125 million. The company also reported $0.06 per share in distributable earnings, a result that easily covers the 1-cent dividend paid out to common shareholders.

Among the bulls is JPMorgan analyst Richard Choe who sees DigitalBridge in a sound position to continue growing. The company is directly involved in the expanding digital industry, and offers investors an indirect route of exposure to networking tech, according to Choe.

“The transformed DigitalBridge is a direct way for investors to benefit from digital infrastructure investment management on a global basis without being fully invested to one vertical and region. Investors are looking for focused alternative asset managers and digital infrastructure is highly attractive given long-term growth prospects, scale and return potential. We believe DBRG will be able to raise capital in a more stable financial environment as rates level off and digital infrastructure gains broader appeal to pension, sovereign wealth and other infrastructure funds,” Choe opined.

Taking this view forward, Choe rates DBRG shares an Overweight (i.e. Buy), with a $25 price target to imply a solid 57% upside potential on the one-year horizon. (To watch Choe’s track record, click here)

All in all, DigitalBridge gets a unanimous Strong Buy consensus rating, based on 7 positive analyst reviews. The shares are currently trading for $16.04, and their $21.42 average price target indicates room for a one-year gain of 33.5%. (See DBRG stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

U.S. stocks saw their losses accelerate on Thursday, reversing most of the S&P 500’s gains from its best session in three weeks a day earlier, as Treasury yields whipsawed, keeping investors on edge ahead of Friday’s monthly jobs report from the Labor Department.

On Wednesday, the Dow Jones Industrial Average rose 127 points, or 0.39%, to 33,130, snapping a three-day losing streak, while the S&P 500 gained 34 points, or 0.81%, to 4,264 for its biggest percentage-point gain in three weeks, FactSet data show.

Treasury yields were volatile in early trade on Thursday, which added to pressure on U.S. stocks as investors digested a batch of fresh economic data ahead of Friday’s all-important September jobs report.

The yield on the 10-year Treasury note

BX:TMUBMUSD10Y

was last pegged at 4.73%, near a 16-year high reached earlier this week. Bond yields move inversely to prices.

“I think the momentum is still on the down side,” said Liz Ann Sonders, chief investment strategist at Charles Schwab, in a phone interview with MarketWatch. “There’s nothing specific that you could point to today.”

A weekly report on jobless-claims data showed no sign that layoffs have been increasing. Rising layoffs are seen as a necessary prerequisite for the Federal Reserve to start easing its monetary policy, which has weighed on both stocks and bonds since early 2022. Government data showed the number of Americans who applied for unemployment benefits last week rose slightly to 207,000, but remained near pandemic-era lows.

See: U.S. jobs report forecast: 170,000 new workers and 3.7% unemployment

Investors also received data on the U.S. international trade deficit which suggested some weakness in consumer spending, but analysts chiefly blamed the jobless claims numbers for the impact on yields and stocks.

Rising Treasury yields, particularly on the long end of the yield curve, have been widely blamed for driving the selloff in stocks that has taken place since early August. But as stocks continued to fall on Thursday with no obvious driver in sight, equity strategists see signs of investors simply following the latest trend.

“Financial markets have been rattled in the last few days,” said Bill Adams, Chief Economist for Comerica Bank. “The yield on the 10-year Treasury note has jumped about 0.6 percentage points since the beginning of September, extending a steady march higher since the early summer.”

“There are competing explanations for the surge in interest rates and they have very different implications. Treasury issuance is way up this year with a higher deficit, and the Fed is no longer a buyer; rising interest rates would be the classic warning that the deficit is starting to crowd out private-sector access to capital. But Treasury yields rose in August, too, even though the Federal government ran a monthly surplus in the month.”

“On net the increase in long Treasury yields makes the Fed more likely to choose an earlier peak in short-term interest rates and an earlier pivot to rate cuts in 2024.”

Several senior Fed officials are set to speak on Thursday, including Cleveland Fed President Loretta Mester, who spoke at the Chicago Payments Symposium at 9 a.m., and San Francisco Fed President Mary Daly, who is set to speak in New York at noon. Richmond Fed President Thomas Barkin is set to speak in North Carolina at 11:30 a.m. Eastern.

Choppy trading in recent days sent the Cboe VIX index

VIX,

a gauge of expected equity-market volatility, to 20 for the first time in four months as stocks tumbled. Some analysts see a near-term rebound ahead, but many argue the direction of bond yields remains critical for stocks.

Looking ahead to Friday, economists polled by The Wall Street Journal expect 170,000 jobs were created last month, which would be lower than the 187,000 created during the month prior.