According to Ricardo Da Ros, CEO of the crypto platform Patex, many crypto users in Latin America (LATAM) seem to prefer using centralized exchanges (CEXs) over decentralized ones. He attributes this preference to a culture in the region that “has been built on trust in authority.” Da Ros suggests that this culture, combined with the […]

According to Ricardo Da Ros, CEO of the crypto platform Patex, many crypto users in Latin America (LATAM) seem to prefer using centralized exchanges (CEXs) over decentralized ones. He attributes this preference to a culture in the region that “has been built on trust in authority.” Da Ros suggests that this culture, combined with the […]

Source link

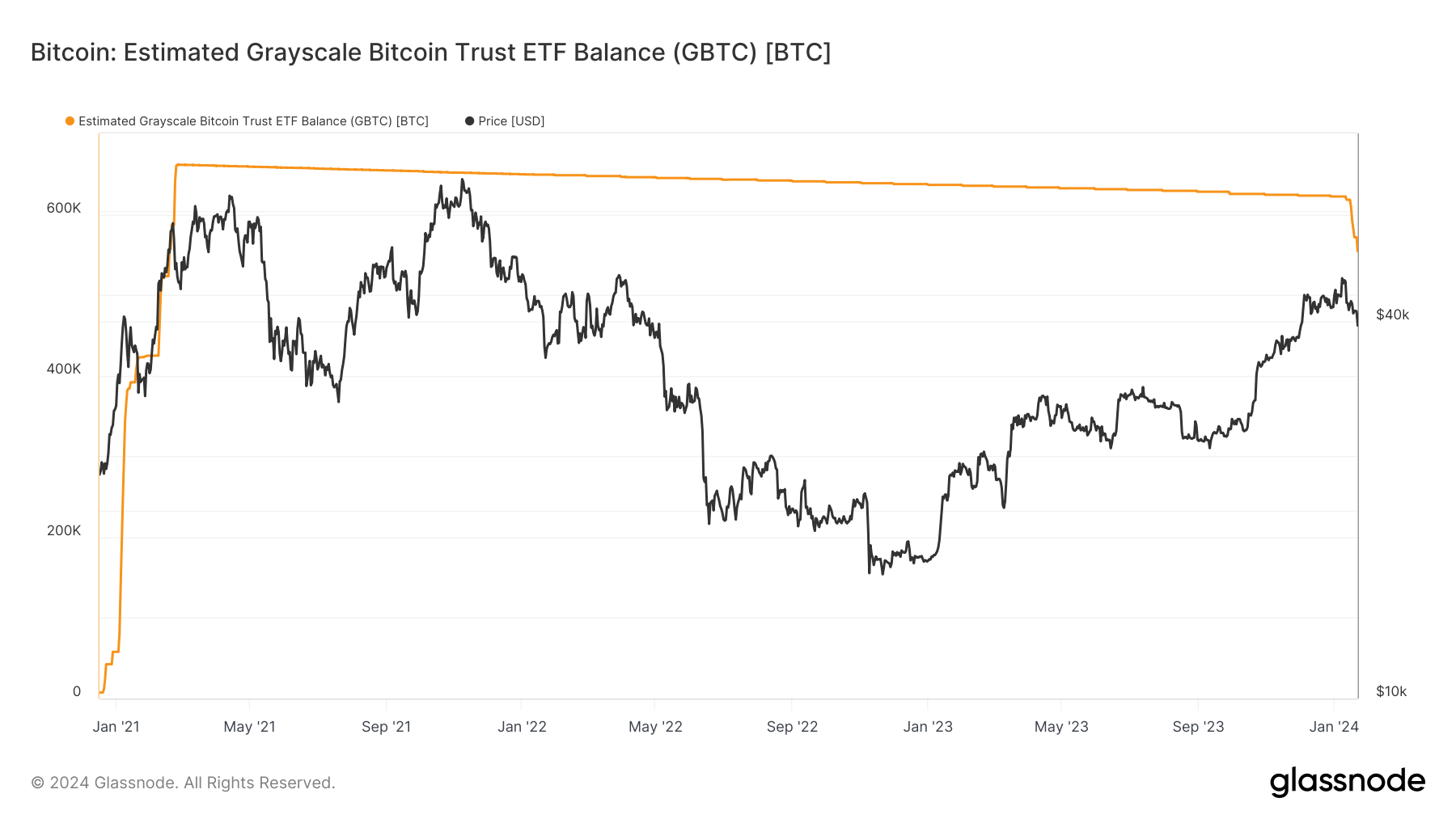

Grayscale has revealed the submission of an S-1 form to the U.S. Securities and Exchange Commission (SEC) for the launch of a new, smaller version of its popular Grayscale Bitcoin Trust (GBTC). This initiative is designed to provide shareholders with exposure to bitcoin, reduced fees and potential tax benefits. Grayscale Unveils Bitcoin Mini Trust With […]

Grayscale has revealed the submission of an S-1 form to the U.S. Securities and Exchange Commission (SEC) for the launch of a new, smaller version of its popular Grayscale Bitcoin Trust (GBTC). This initiative is designed to provide shareholders with exposure to bitcoin, reduced fees and potential tax benefits. Grayscale Unveils Bitcoin Mini Trust With […]

According to a recent Form N-1A, Grayscale has approached the U.S. Securities and Exchange Commission (SEC) with a proposal for a unique exchange-traded fund (ETF) dedicated to the privacy and cybersecurity realm. The Grayscale Privacy ETF aims to be the first to encapsulate the burgeoning sector of privacy technology and cybersecurity. Privacy Takes Center Stage […]

According to a recent Form N-1A, Grayscale has approached the U.S. Securities and Exchange Commission (SEC) with a proposal for a unique exchange-traded fund (ETF) dedicated to the privacy and cybersecurity realm. The Grayscale Privacy ETF aims to be the first to encapsulate the burgeoning sector of privacy technology and cybersecurity. Privacy Takes Center Stage […]