Wall Street Isn’t Sure It Can Handle All of Washington’s Bonds

Source link

Wall Street Isn’t Sure It Can Handle All of Washington’s Bonds

Source link

What will happen next to bond yields and interest rates? And how should that influence what investors do with their spare cash?

Bond yields began moving higher in earnest early last year in response to a series of interest rate hikes by the Federal Reserve. Earlier this month, the yield on the benchmark 10-year U.S. Treasury note hit its highest level in 16 years, while yields on shorter-term debt securities also rose.

That makes it a very attractive place for investors to park their money. Stocks have taken a hit as investors adjust their portfolios to take advantage of more attractive bond yields.

Yields climbed again Friday morning after the stronger than expected September jobs report. The yield on the two-year Treasury note

BX:TMUBMUSD02Y

rose to almost 5.1%, up from 5.023% Thursday afternoon and up from 4.26% a year ago.

“‘Bond yields rose primarily because the Fed pivoted to a much more hawkish position, as investors anticipated aggressive interest rate hikes to rein in inflation.’”

The yield on the ten-year Treasury note

BX:TMUBMUSD10Y

climbed to 4.86%, up from 4.715% Thursday afternoon, and up from 3.82% a year ago. The yield on the 30-year bond

BX:TMUBMUSD30Y

reached 5.01%, up from 4.88% on Thursday and up from 3.78% a year ago – heading Friday morning for the highest level since August 2007.

But will rising yields influence the Federal Reserve decision making on interest rates? Some analysts say yes.

Steen Jakobsen, Saxo Bank’s chief investment officer, said officials will began mulling rate cuts in 2024, while the spike at the long end of the yield curve will eventually nudge the Fed to take action “first through flagging a needed policy shift that keeps the ten to thirty-year yields capped at perhaps 500-525 basis points (5.0%),” he wrote in a note.

“Bond yields rose primarily because the Fed pivoted to a much more hawkish position, as investors anticipated aggressive interest rate hikes to rein in inflation,” Bill Merz, head of capital markets research at U.S. Bank Wealth Management, said this week.

On Thursday, Mary Daly, president of the San Francisco Fed, told the Economic Club of New York that the jobs market and consumer prices are two factors in the Fed’s thinking. “If we continue to see a cooling labor market and inflation heading back to our target, we can hold interest rates steady and let the effects of policy continue to work,” she said.

“‘If you need the cash for a down payment on a house in the next 18 months then placing it in a 2- or 3-year Treasury probably won’t work.’”

Usually when someone buys bonds, the interest comes in the form of a fixed, recurring “coupon” payment. Treasurys, for example, pay interest every six months until maturity. (Treasury interest income is taxed at the federal level, but exempt from state and local tax. Other interest income, like the yields on CDs, have no special tax treatment.)

In the buy-and-hold approach, “knowing when you might need access to this money is key to deciding where to put it,” said Greg Vojtanek, owner Fade In Financial, a Los Angeles-based financial planning firm. “If you need the cash for a down payment on a house in the next 18 months then placing it in a 2- or 3-year Treasury probably won’t work.”

“On the other hand, if you don’t need this money for another 20-years and you’d like a small portion of your portfolio to be safely placed in cash, then buying longer-term Treasurys is a perfectly fine option,” he said.

“Retirees drawing down their money may be in ‘statement shock’ now, amid the lower prices in the bond market where they’ve built up exposure.”

When investors buy and sell ahead of maturity the inverse relationship between prices and yield comes into play. Currently, Wall Street traders are guessing when the Fed stops raising its federal funds rate — and when it will start cutting the rate.

Treasury bills, which come due within a year, have been a yield-producing place to put cash. Yields on T-bills

BX:TMUBMUSD06M

of varying length are over 5%, up from roughly 4.5% around the start of the year.

As a result, high-yield savings accounts, certificates of deposit and money market-mutual funds have all become alluring ways to reap rewards for parking cash. It’s easy to find these products with rates in the 4% and 5% range.

Also see: Treasury yields are climbing: ‘There’s never really been such an attractive opportunity for fixed-income investments’

Suppose the Fed decides it’s done tightening and later cuts the rate. Now suppose there’s someone who bought longer-term Treasurys at today’s higher yields and then decided to sell at a time of falling interest rates.

“When that happens, the price of bonds will increase, and the investor will have the benefit of a high-yielding bond based on the purchase price and a bond that increases in price. That’s great because it gives the investor more flexibility,” said Chris Chen, CEO and a wealth strategist at Insight Financial Strategists in Newton, Mass.

The central bank is “either at or close to the peak” in its interest-rate tightening plan, said David Sekera, chief U.S. market strategist at Morningstar, the investment research firm. Rate cuts could start as early as March of next year, according to Morningstar projections.

Of course, that’s just one projection — and determining the direction of interest rates and timing is tricky.

Now suppose the Fed isn’t done with interest rates. The benchmark rate is at a two-decade high with its 5.25% to 5.50% target range, and Fed Chair Jerome Powell recently reiterated that the central bank will follow the economic data to determine its next move.

If interest rates keep increasing, the purchase of high-yielding, long-dated Treasurys doesn’t seem so enticing.

“If interest rates keep increasing, the purchase of high-yielding, long-term Treasurys does not seem so enticing.”

“The prices of long-dated bonds move much more dramatically than the prices of shorter-dated bonds,” said Mike Silane, managing partner of 21 West Wealth Management in Irvine, Calif. “First-time investors in long bonds may be shocked by how much money they could lose in a short period of time, should rates continue to rise, as some have forecasted.”

Retirees drawing down their money may be in “statement shock” now, amid the lower prices in the bond market where they’ve built up exposure, said Matt Sommer, head of specialist consulting group at Janus Henderson Investors.

Sommer said he’s advising older clients to leave their bonds alone and tap their stock gains if they need cash flow. That will give bond portfolios time to recover their value on paper, he said.

Treasurys held to maturity will return all the principal, Sommer said. The dips shown on statements are a “paper loss” based on current market valuations, not real losses.

“That’s why we can’t emphasize enough, even though you are experiencing statement shock when you are looking at your Treasurys on your screen or on your statement,” Sommer said, “now is not the time to sell.”

Quentin Fottrell contributed.

Related: Why rising Treasury yields are upsetting financial markets

Here’s the Average Social Security Benefit at Age 66

Here’s Precisely When Social Security’s Much-Anticipated Cost-of-Living Adjustment (COLA) Will Be Announced

1 Social Security Change Joe Biden Wants That You Might Like, Too

A Bull Market Is Coming: 2 Phenomenal Growth Stocks to Buy Before They Soar 93% and 127%, According to Wall Street

Investors face a growing list of risks heading into the fourth quarter that just keeps getting bigger — from rising interest rates to a possible revival of inflation and gridlock in Washington that may become a headwind for economic growth.

The Federal Reserve remains in rate-hiking mode and is unlikely to cut borrowing costs next year by as much as previously thought. The prospect of $100-a-barrel oil at a time of expanded strikes by the United Auto Workers union is reigniting inflation concerns. Meanwhile, mitigating factors that could slow economic growth — such as the possibility of a government shutdown and the resumption of student-loan payments — might not be enough to shake the Fed’s inflation-fighting resolve.

Read: Risk of government shutdown soars as House Republicans leave town in disarray amid hard-right revolt and Student-loan payments are about to resume. Defaults are expected to follow.

See also: Fed’s Collins doesn’t rule out more interest-rate hikes

It all adds up to an ever-growing wall of worry for many investors and traders, who had expected inflation to fade and the Fed to be done with raising interest rates. The phrase wall of worry is typically associated with rising stocks — given the market’s ability to often keep climbing, despite developments that might otherwise spark a selloff — but this time might be different. With the central bank’s main interest-rate target already at a 22-year high and likely to go higher by December, Treasury yields have reached levels not seen in at least a dozen years, putting a cap on how much further equity markets can climb and creating the need for investors to search for protection.

A day after the Fed’s policy update on Wednesday, which underscored a message of higher-for-longer rates, strategists Jay Barry, Jason Hunter and others at JPMorgan Chase & Co.

JPM,

the biggest U.S. bank, said their bearish equity view was “gaining material traction” and that September through mid-October “also happens to be the most bearish time of the year for risky markets from a cyclical perspective.”

Comparing the current period to 1987, the year of the “Black Monday” crash, they said they expect the U.S. stock market’s slide to accelerate into the fourth quarter, but stopped short of calling for a “crash.”

The rise in market-implied rates that followed the Fed’s announcement has created an environment of “more losers than winners” — in the words of portfolio manager Christian Hoffmann at Thornburg Investment Management — with equity prices and bond prices both falling on Thursday.

On Monday, all three major U.S. stock indexes

DJIA

SPX

COMP

managed to score their first gains in five straight sessions after struggling for momentum over much of the day. Meanwhile, 10- and 30-year Treasury yields ended at their highest levels since Oct. 17, 2007, and March 8, 2011, respectively, as fed funds futures traders priced in a 39% likelihood of further Fed tightening by year-end.

Read: ‘The world has changed’ as investors absorb highest Treasury yields in a dozen years or more

Some analysts remained optimistic. “Higher rates for longer is not necessarily this terrible thing if the Fed hangs out there because growth is good,” said Jeffrey Cleveland, chief economist at Payden & Rygel in Los Angeles, which manages more than $144.4 billion in assets. “Growth is coming in stronger than everyone expected, and that’s what is forcing the revisions in interest rates. That’s not necessarily bad for the riskier parts of our portfolios,” like high-yield corporate bonds.

“The economy seems to have pretty good momentum and should be able to withstand some of those worrisome issues,” Cleveland said via phone. “The momentum is sufficiently strong enough that most investors should be able to jump over the wall of worry, without running into the wall,” he said, adding that the U.S. economy should dodge a recession over the next 12 months.

However, not even Fed Chairman Jerome Powell is entirely sure the U.S. can achieve a soft landing and avoid a recession, despite the fact that’s the outcome policy makers are hoping for, judging by their projections for growth, unemployment, and inflation through 2026. The central bank’s favorite inflation gauge, the personal consumption expenditures price index, is set to be released on Friday and is the data highlight of the week ahead. July’s PCE report showed the annual rates of headline and core inflation stubbornly stuck above 2%.

At the moment, the world’s largest economy appears to be undergoing a “controlled landing,” in which the labor market is healthy but cooling, wage growth is moderating, and consumers and businesses are conservatively spending, according to chief economist Gregory Daco of EY-Parthenon, the global strategy consulting arm of Ernst & Young in New York. His firm expects real GDP growth of 2.2% in 2023 and a more muted 1.3% in 2024.

“We are not going back to a free-money era anytime soon, and the best way to approach the new paradigm of higher-for-longer interest rates is to acknowledge and adjust to it,” Daco said via phone. “Every portfolio is going to be different and have its own approach to risk objectives and returns, so it’s not about one asset class versus another. It’s about understanding what your risk tolerance is and how to maximize your returns when the cost of capital and the cost of equities is going to be higher.”

Michael Landsberg, chief investment officer of Landsberg Bennett Private Wealth Management in Punta Gorda, Fla., which manages $1 billion in assets, said that there are “big question marks about earnings season, which begins in mid-October” and “we need earnings to grow meaningfully in order to have any kind of noticeable move higher in markets.”

“With inflation, interest rates and earnings growth fears in the U.S., it’s important for investors to have exposure to non-U.S. equities, particularly countries like Japan and India, whose central banks are not aggressively raising rates like they are in the U.S.,” Landsberg wrote in an email to MarketWatch. “We have been bullish on the U.S. dollar and favor foreign ETFs in Japan that are short the yen.” His firm also likes using ETFs in India “for both large- and small-cap exposure.”

Wall Street’s so-called fear gauge has been subdued this year, in a “mysterious shrinking” pattern, that’s a bullish signal for equities, according to DataTrek Research.

Declines for the Cboe Volatility Index

VIX

fear gauge come despite continued worries over inflation and elevated interest rates.

“We’ve been saying for several months that a low VIX is a sign that U.S. stocks are in a bull market rather than being excessively delusional about the obvious challenges ahead,” said Nicholas Colas, co-founder of DataTrek, in a note emailed Monday. “We still believe the next few weeks will be choppy, however.”

The gauge, known by its ticker VIX, has dropped more than 35% so far this year and is trading below its long-term average, according to FactSet data. Its trading levels are derived from options contracts tied to the S&P 500, the U.S. stock benchmark that has rallied 16% in 2023 through Monday.

Last week the VIX made “a new post-pandemic crisis low,” finishing below 13 on Sept. 14 in a “rare occurrence” for the index that was a positive sign for stocks over the next three months, Colas’s note shows. That’s even if it suggests near-term “choppiness” will continue, he said.

On Monday the VIX closed at 14, well below its long-run average of around 20. The measure ended Sept. 14 at 12.8.

“At first glance, this makes little sense,” Colas said. “The VIX is supposed to be Wall Street’s ‘Fear Index’ and it would appear “there’s plenty to be fearful of just now.”

Colas cited several areas of concern, including uncertainty surrounding inflation, the recent jump in oil prices

CL00,

and “a cloudy picture” of how long the Fed Reserve will keep interest rates elevated, for his rationale as to why investor might feel fearful.

The Fed has been trying to slow the rise in the cost of living in the U.S. via its restrictive monetary policy, lifting its benchmark rate aggressively over the past 18 months.

There also has been the recent climb in Treasury rates that has weighed on stocks lately, with 10-year Treasury yields looking “set on making new decade-plus highs,” said Colas.

The yield on the 10-year Treasury note

BX:TMUBMUSD10Y

finished Monday at 4.318%, according to Dow Jones Market Data. That’s around levels seen in late 2007, FactSet data show.

The VIX had kicked off 2023 trading below its long-run average, with Colas saying in January that it was looking a lot more like 2021, a year in which stocks rallied, rather than 2022, when equities tanked as the Fed rapidly hiked rates.

See: Wall Street’s ‘fear gauge’ VIX shaping up more like 2021 than 2022, as U.S. stocks rally this year, says DataTrek

Meanwhile, September and October are known for “seasonal peaks in equity market volatility,” according to Colas.

U.S. stocks have slumped so far this month, after falling in August. The S&P 500, which dropped 1.8% last month, is down 1.2% in September through Monday, FactSet data show.

The S&P 500

SPX

closed 0.1% higher on Monday while the Nasdaq Composite

COMP

and Dow Jones Industrial Average

DJIA

each finished about flat, as investors digested fresh data showing a drop in confidence among homebuilders this month amid elevated mortgage rates.

Stock-market investors also have been monitoring the U.S. Treasury market’s inverted yield curve, or when shorter-term yields climb above long-term rates, as that historically has preceded a recession.

There’s also some concern over the increased popularity of zero-day options in the stock market, as “you’d think their growing usage would push anticipated volatility higher, not lower,” Colas said.

“We doubt options desks have just walked away from trading 30-day options” on S&P 500 futures, he said. “If there is money to be made in a financial asset, someone invariably trades it.”

The Cboe Volatility Index measures 30-day expected volatility of the U.S. stock market.

“What the ultra-low VIX is telling us is that none of these concerns matter enough to offset a fundamentally strong picture for U.S. corporate earnings and the belief that the Federal Reserve is largely done hiking rates,” said Colas. “Equities are dismissing the possibility of a recession over the next 1-2 years, no matter what an inverted yield curve has historically said on that point.”

Text size

Apple

’s

long-awaited iPhone 15 launch left investors disappointed, and Wall Street doesn’t seem enthused, either.

The world’s most-valuable company unveiled its new iPhone models Tuesday, and things went pretty much as expected. The one surprise was the lack of a price increase for the iPhone Pro, largely expected by analysts, although

Apple

did hike the starting price for the Pro Max by $100.

Apple stock (ticker: AAPL), which fell 1.7% to $176.30 Tuesday, has climbed an average of 5% in the three months following an iPhone release, according to Dow Jones Market Data. In premarket trading Wednesday,

Apple

stock is down 0.5% to $175.47.

D.A. Davidson analyst Tom Forte doesn’t see Apple stock getting a boost after the latest phone launch. “Unlike years past, we believe the company may not be able to rely on strong iPhone sales to drive its share price higher,” he wrote in a note Wednesday.

Forte noted that management was guiding for revenue to decline in the September quarter despite the iPhone 15 release date of Sept. 22. He also cited the “potential for lackluster sales” in China. He reiterated a Neutral rating on Apple stock and a price target of $180.

KeyBanc analysts, led by John Vinh, also saw the product launch as being “slightly negative” for the stock, but maintained an Overweight rating and a $200 price target.

“We see the September event as a modest negative for Apple given a lack of expected price increase for the Pro model, features that lack a compelling motivation for consumers to upgrade, and modestly less aggressive promotions from carriers,” they said.

Evercore ISI analysts viewed the event as “mildly disappointing,” and said a price increase for the Pro would’ve helped mitigate the impacts of Huawei’s recently launched new smartphone.

“Investors typically go into this event with relatively low expectations given it has been a long time since we have seen a major change to the iPhone design or functionality, but investors were hoping to see a $100 bump to the cost of the Pro, which would’ve helped offset any potential headwinds from Huawei’s Mate 60 Pro Launch,” they said. They still have an Outperform rating on the stock, with a price target of $210.

Not everyone saw the launch event in a negative light. Wedbush analyst Dan Ives hiked his price target on Apple stock to $240 from $230, kept an Outperform rating, and said the upgrade cycle over the next year will surprise to the upside. He wrote that no price increase for the iPhone 15 Pro was a surprise, but that the hike for the Pro Max was a “smart strategic move.”

He expects a greater proportion of consumers to shift toward the Pro models from the basic model, in a 75% to 25% split, compared with the 60% to 40% seen in recent years—a “major tailwind” for the company’s average selling price.

“We believe the robust consumer product cycle continues globally for Cook & Co. despite the noise, with the iPhone 15 giving Apple additional momentum heading into the all-important holiday season,” Ives wrote.

Citi analysts also saw the positives, noting that “flat pricing on the three models could help lift units in a tough macro environment.” They said Apple is more focused on maximizing gross profit per unit from consumers migrating to premium phones, adding that the iPhone 15 would drive higher premiumization than the iPhone 14 range. They maintained a Buy rating on Apple stock with a $240 price target.

Write to Callum Keown at callum.keown@barrons.com

U.S real estate investment trusts today manage $4.5 trillion in real estate worldwide. Many groups on Wall Street offer these tax-friendly funds to retail investors.

KKR’s real estate business is one of the big players in the REIT game. The private equity firm manages multiple REIT funds. The KKR Real Estate Select Trust, which currently manages $1.5 billion in assets, paid a dividend of 5.4% to its investors in July 2023.

But the benefits extend beyond returns.

“When you look at the after tax equivalent of that yield, it is very compelling.” said Billy Butcher, CEO of KKR’s global real estate business. “The depreciation from our properties has covered 100% of the income generated by our properties, and there’s no tax on that dividend,” he said in an interview with CNBC.

Larger funds sometimes contain a diversified pool of assets. Categories may include office, student housing, casino, timberlands, radio and cell towers, server farms, self-storage properties, billboards, and much more.

“Back in the 1960s, there were three or four different types [of REITs], said Sher Hafeez, a managing director at Jones Lang LaSalle, a real estate services firm. “Now, I can count at least 20 different types.”

Top performing REIT sub-sectors in recent years include data centers, self-storage properties, residential housing and tower REITs. Residential housing delivered a return of 16% from 2010 to 2020, according to a S&P Global Investments report.

The investor-friendly tax rules can also increase the pace of large-scale development.

“Having REITs there as a potential exit helps the market, and helps the availability of financing,” said Michael Pestronk, CEO and co-founder of Post Brothers, a Philadelphia-based housing developer.

Some funds like Invitation Homes and American Homes 4 Rent were founded in the yearslong slowdown in U.S. home construction. At the time, REITs bought and managed commercial-scale properties, which could include products like master-planned communities or traditional apartment complexes.

In recent years, publicly traded trusts have targeted single-family rental market, and today, these REITs have grown tremendously — enough to build new neighborhoods in their entirety.

Watch the video above to learn the fundamentals of real estate investment trusts.

XRP, the cryptocurrency tied to Ripple, found itself entangled in a familiar tussle with the $0.55 resistance level as bearish forces thwarted its early attempts at a rebound.

While last month’s pivotal summary judgment offered a glimmer of regulatory clarity for XRP, the ongoing specter of the SEC appeal and an impending trial slated for the first half of 2024 are fostering an air of skepticism among the investor community.

Despite the much-needed legal clarity provided by the recent summary judgment, a cloud of uncertainty still hangs over XRP’s trajectory. The forthcoming SEC appeal and the looming trial timeline have combined to cast doubt on the cryptocurrency’s immediate future. The ripple effect of these uncertainties is palpable as investors remain cautious about diving back into the XRP market.

Price analysis indicates that the prevailing bearish sentiment pervading the broader cryptocurrency market is acting as a significant impediment to XRP’s upward breakout.

Santiment’s Network Value to Transaction Volume (NVT) ratio, which gauges the relationship between a blockchain network’s transactional activity and its recent price performance, reveals the extent to which bearish undercurrents are hampering XRP’s ascent.

As of now, XRP’s price hovers around $0.513, marking a decline of 2.8% over the last 24 hours. The past week has seen the cryptocurrency grappling with losses amounting to 1.6%, CoinGecko data shows.

The struggle to break through the $0.55 resistance level seems to mirror the broader market sentiment, reflecting the challenges that lie ahead.

Coinalyze’s data presents a somewhat brighter aspect. XRP’s funding rates turned green on August 25, signifying an improved stance.

Moreover, the Open Interest (OI) rates, which indicate the total number of outstanding derivative contracts, have risen from approximately $340 million to surpass $360 million.

This increase could signal growing interest among traders and investors, adding a dash of optimism to the otherwise cautious outlook.

In addition, seasoned crypto investor Austin Hilton offers a contrarian view, suggesting that XRP is poised for a significant 20% breakout in the short term. Hilton points to various indicators and fundamental factors underpinning his projection.

Notably, his argument centers around a Tradingview indicator that tracks momentum shifts on the daily timeframe, helping traders determine optimal entry and exit points.

XRP’s journey forward remains intricate, marked by legal battles, market sentiment, and technical indicators. As the cryptocurrency navigates these multifaceted challenges, investors and enthusiasts alike eagerly await the next chapter in XRP’s tumultuous saga.

(This site’s content should not be construed as investment advice. Investing involves risk. When you invest, your capital is subject to risk).

Featured image from LinkedIn

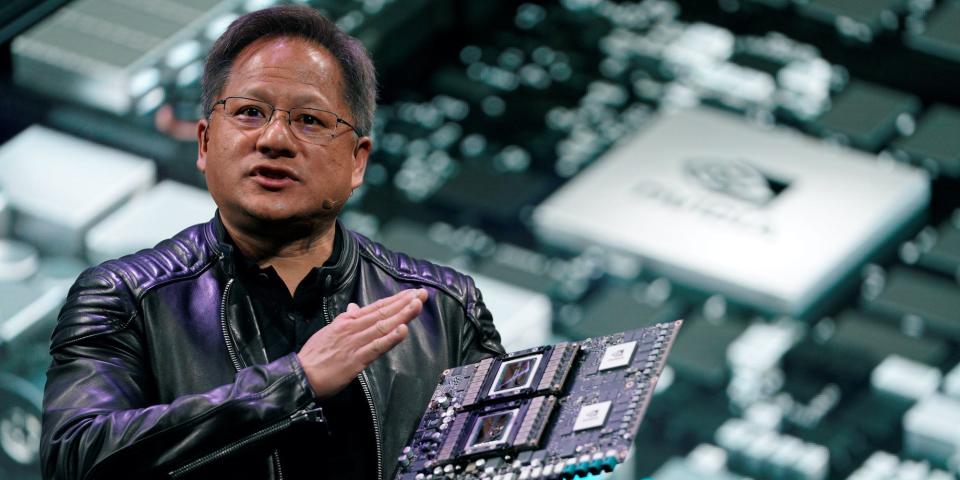

Investors are awaiting Nvidia’s second-quarter earnings report after the market close on Wednesday.

The AI chip company has set high expectations after its May revenue guidance exceeded Wall Street estimates.

Here’s what Wall Street expects from Nvidia’s upcoming earnings report.

Nvidia will be closely watched by investors this week as the company gets ready to release its second-quarter earnings report after the market close on Wednesday.

The chipmaker blew away analyst expectations in May when it issued second-quarter revenue guidance of $11 billion, which exceeded Wall Street estimates by a massive $4 billion.

The company, which manufactures and sells GPUs that help power AI chatbots like ChatGPT, has seen soaring demand for its products over the past few months, and it commands a decisive lead in the AI chip market.

“We’re using a lot of Nvidia hardware. We’ll actually take it as fast as they’ll deliver it to us. Frankly, if they could deliver us enough GPUs, we might not need Dojo. But they can’t. They’ve got so many customers,” Tesla CEO Elon Musk said during Tesla’s second-quarter earnings call in July.

The boom in Nvidia’s AI-focused business has sent its stock price soaring more than 200% year to date, giving it a $1.1 trillion market valuation.

Most of Wall Street expects Nvidia to continue impressing investors with solid second-quarter results, and even better-than-expected guidance for the second half of the year. The average EPS estimate for the quarter is $2.07, and the average revenue estimate is $11.2 billion, according to data from YahooFinance.

Here’s what the Wall Street analysts are saying about Nvidia’s upcoming earnings report.

“Our backend Asia checks show Nvidia backend can support up to $15 billion in H100/A100 revenue in Q3 and more in Q4, leaving potential for more substantial beats and raises over the next few quarters,” Barclays said in a note late last month, referring to Nvidia’s GPUs

“The consensus total Data Center estimate (including Mellanox) for Q3 is just $8.5 billion… AMD looks positioned within the market as the potential first viable competitor, but we likely won’t even see initial signs of success until next year. In the meantime, Nvidia will continue to take the lion’s share of the economics from the AI boom.”

Barclays rates Nvidia “Overweight” with a $600 price target.

Nvidia is a “top sector pick ahead of its F2Q earnings call given its dominant position and multi-year runway in transforming the $1+ trillion in traditional global data centers to AI/accelerated compute. After last quarter’s shock-and-awe report, we expect the sentiment to be bit more measured. Demand isn’t the issue, its supply (packaging, memory) and importantly the pace with which US cloud service providers are able to set up genAI compute instances,” Bank of America said in a note earlier this month.

“Nvidia is unlikely to guide beyond a quarter, but listen for management commentary around continued sales acceleration/early in ramp etc. Post-earnings reaction could see some near-term stock consolidation following the 200%+ move up YTD (vs SOX up 46%),” BofA said.

Bank of America rates Nvidia at “Buy” with a $550 price target.

“We continue to see significant runway ahead for the company based on its robust competitive position in what is a rapidly growing (yet nascent) AI semiconductor market. With our forward estimates sitting above Street consensus, we envision positive EPS revisions supporting sustained stock price outperformance through the balance of the calendar year,” Goldman Sachs said in a note last month.

Goldman Sachs rates Nvidia at “Buy” with a $495 price target.

Read the original article on Business Insider

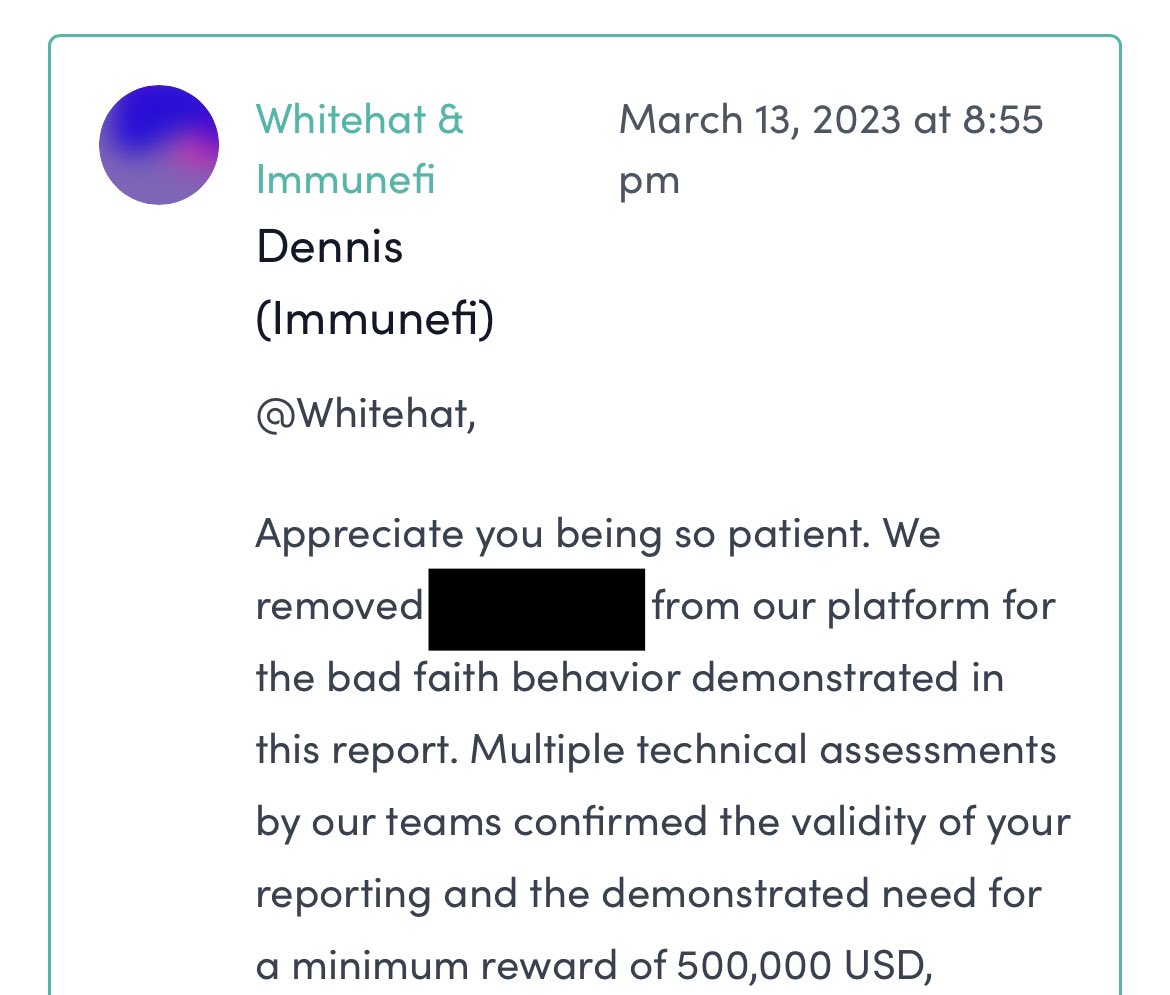

The crypto community is grappling with issues surrounding bug bounty programs, a crucial mechanism for discovering and addressing system vulnerabilities.

Usmann Khan, a web3 security auditor, posted on Aug. 17, “Remember that projects can simply not pay, whitehat,” with a screenshot of a message from Immunefi indicating a project had been removed from its bug bounty problem for failure to pay a minimum of $500,000 in bounties.

In response, security researcher Marc Weiss shared the ‘Bug Bounty Wall of Shame’ (BBWoS), a list documenting unpaid rewards allegedly owed to white hat hackers in web3. The data from BBWoS appears to signal a significant lack of accountability and trust within the crypto ecosystem that cannot be ignored.

The BBWoS indicates that a bug bounty for the Arbitrum exploit of Sep. 2022 had a $2 million reward. Yet, the white hate was awarded just $780,000 for identifying an exploit that exposed over $680 million.

Further, BBWoS states the CRV borrowing/lending exploit on Aave from Nov. 2022 led to the loss of $1.5 million, with $40 million at risk, and no bounty was paid to the white hat who identified the attack path “days before.”

Lastly, in April this year, just $500 was paid to a white hat who reportedly identified a way for managers to steal up to $14 million worth of “tokens from users using malicious swap paths” after being told by dHEDGE that the issue was “well-known.”

The list was created by whitehat hackers “tired of spending sleepless nights finding bugs in protocols only to have a payout of $500 when the economic damage totals in the millions,” with the creator stating,

“I created this leaderboard to help inform the security community as to the projects that don’t take security seriously so we can avoid them and spend time on the projects that do.”

In his presentation at the DeFi Security Summit in July, Weiss highlighted auditors’ critical role at various stages of protocol development. By integrating auditors and researchers in-house, he stressed their potential to make insightful architectural decisions, design effective codebases, and adopt a security-focused approach to protocol development.

Consequently, it is concerning when platforms fail to acknowledge and adequately reward the efforts of these security professionals when working on a contract basis.

Auditors Gogo and MiloTruck highlighted that non-payment for identified vulnerabilities is a widespread issue. Their posts underscore the urgent need for these platforms to enhance their accountability and trustworthiness and ensure due recognition for white hat hackers.

More transparency is required in handling vulnerabilities. High-profile cases listed on BBWoS, like the compromised deposit contract of Arbitrum, the economic exploit of Aave, and the malicious swap paths in dHEDGE, amplify this need.

In response to Weiss’s issues about trust, Danny Ki from Super Protocol emphasized the potential of “decentralized confidential computing” to bolster trust in Web3 projects and mitigate vulnerabilities. Ki is referencing the option to run DeFi in Trusted Execution Environments (TEE), something inherent in Super Protocol.

A TEE is a secure area of a processor that guarantees code and data loaded inside be protected for confidentiality and integrity. However, one disadvantage of using TEEs within DeFi dApps is relying on proprietary architecture from centralized companies such as Intel, AMD, and ARM. There are efforts in the open-source community to develop open standards and implementations for TEE, such as Open-TEE and OP-TEE projects.

Ki argues that should “Web3 projects operate within confidential enclaves, there may be no need to pay out for vulnerabilities, as the security will be inherently fortified.”

While a fusion of blockchain and confidential computing could provide a formidable security layer for future projects, the move to replace bug bounties and security auditors with TEEs seems complex, to say the least.

Still, there are additional concerns for white hat hackers, such as improper bug disclosures from security firms on social media. A post from Peckshield identifying a bug in July simply said, “Hi @JPEGd_69, you may want to take a look,” with a link to an Ethereum transaction.

Gogo lambasted the post stating, “If this vulnerability were responsibly disclosed instead of exploited, PEGd’s users wouldn’t have lost $11 million, No reputational damage would have been caused, The guy would have gotten a solid bug bounty instead of been front-run by an MEV bot.”

Gogo shared their bug bounty experience with Immunefi, a company they described as ‘beyond fantastic,’ where the payout required a mediation process, eventually leading to a satisfactory payout of $5k for a critical bug.

These insights from the web3 security community underscore the critical role of auditors and the importance of effective bug bounty programs to the crypto ecosystem’s security, trust, and growth.

As some have identified, hacks are covered extensively in the news and on X, but what for those who discover the exploits and are never adequately compensated? Nearly $2.5 million in allegedly unpaid bounties is listed on BBWoS alone, yet, as Ki highlighted, could the future include a web3 that is innately secure with no need for bounties?