A new survey says consumers find e-commerce sites often fail to meet expectations. Experts say that’s because shoppers have become accustomed to how Amazon gets things done to their liking.

Source link

A new survey says consumers find e-commerce sites often fail to meet expectations. Experts say that’s because shoppers have become accustomed to how Amazon gets things done to their liking.

Source link

U.S. stocks capped off a wild 2023 with a two-month sprint that has carried the Dow to record highs and the S&P 500 index to within a whisker of a similar milestone.

But after such a powerful advance, some portfolio managers and strategists are concerned that the market could suffer its own post-New Year’s Eve hangover once the calendar turns to January 2024.

Instead of providing a tailwind for the market, several who spoke with MarketWatch worried that the “January effect” might work in reverse as investors scramble to lock in gains after the S&P 500 rose 24% in 2023, according to FactSet data.

“Any time you have a big burst like that, I think you’re vulnerable to some profit-taking,” said James St. Aubin, chief investment strategist at Sierra Investment Management, during an interview with MarketWatch. “It wouldn’t surprise anybody to see the market cool off a bit after a strong run.”

From high valuations, to bullish sentiment indicators, to economic data, to geopolitics and beyond, here are a few things that could trip up the market in January.

A technical gauge that’s widely followed by Wall Street portfolio managers and technical analysts has been screaming that U.S. stocks are overbought for a month.

The 14-day relative strength index on the S&P 500, a momentum indicator that’s supposed to help put the magnitude of the index’s latest moves into context, climbed as high as 82.4 on Dec. 19, its highest since 2020, according to FactSet data.

Although the RSI has since pulled back, it continues to hover around 70, seen by analysts as the threshold for when something can be considered “overbought.”

In the span of just two months, investors have gone from incredibly bearish to incredibly bullish, according to the American Association of Individual Investors’ weekly sentiment survey.

That should give investors pause, since the gauge is seen as a reliable counter-indicator. When sentiment becomes stretched in either direction, it can signal that the market is about to turn. Investors say that is what happened back in July, and also in October after the S&P 500 touched its 2022 bear-market nadir.

According to the AAII survey published ahead of the Christmas holiday, nearly 53% of respondents said they were bullish, the highest since April 2021. That number came down a bit this week, but it remains high relative to levels from October.

Wall Street’s favorite “fear gauge” is giving the all-clear. To some, that’s reason enough to worry.

The Cboe Volatility Index

VIX,

better known as the Vix, measures implied volatility, or how volatile traders’ expect the S&P 500 to be over the coming month based on trading activity in options contracts tied to the index.

In December, the Vix dropped below 12 for the first time since before the advent of the COVID-19 pandemic.

Nancy Tengler, CEO and CIO of Laffer Tengler Investments, said in emailed commentary that she is keeping a close eye on the Vix. Once volatility starts to climb, investors should consider taking some chips off the table.

Some investors are already anxious about the next U.S. inflation report, due Jan. 11.

The Cleveland Fed’s inflation nowcast has core CPI rising more than 0.3% in December. If this proves accurate, it would be the hottest inflation reading since May.

And even if core inflation comes in slightly cooler, stocks might not greet it with the same enthusiasm they have shown in the past.

“U.S. CPI for December will hopefully continue to show a disinflationary trend, although the question is: can we keep rallying on this same dynamic?” said Larry Adam, chief investment officer at Raymond James, in emailed comments.

For three straight quarters beginning with the final three months of 2022, the largest U.S. companies saw their earnings shrink on a year-over-year basis.

This “earnings recession” finally came to an end in the third quarter, but the conundrum that investors now face is whether companies can manage to satisfy Wall Street’s lofty expectations for 2024.

The artificial-intelligence software boom and the fact that the U.S. economy avoided a recession in 2023 has helped boost analysts’ confidence about earnings, strategists said.

According to the bottom-up consensus estimate from FactSet, analysts expect S&P 500 aggregate earnings to increase by 11.7% for the calendar year 2024.

“Markets have been baking in this 11.7% earnings growth figure for a while now. That’s a lot of optimism,” Goldman said during an interview with MarketWatch.

To be sure, this list is hardly comprehensive.

Politics and geopolitics also came up a lot in discussions with analysts. Investing professionals cited Taiwan’s upcoming presidential election, another looming federal debt-ceiling showdown in the U.S., the beginning of the 2024 Republican presidential primaries, the ongoing conflicts in Gaza and Ukraine, and more as potential threats to market calm.

Some expressed concern that the Treasury could spark a selloff in bonds and stocks with its next quarterly refunding announcement in early 2024.

But in the view of Cetera’s Goldman, a dynamic that Wall Street traders call it “buy the rumor, sell the news” could represent a bigger threat.

The thinking works like this: investors have already front-run aggressive Federal Reserve interest rate cuts. So, if the Fed delivers, the rush to take profits could drive stocks lower instead of propelling the main U.S. indexes to new highs. Put another way, many strategists believe investors have already priced in pretty aggressive Fed rate cuts.

So unless the central bank finds a way to deliver something even greater than what Wall Street is expecting, the main U.S. equity indexes could struggle to continue their advance.

“Markets are already buying the rumor that we’re going to have a better 2024, that the Fed is going to cut rates, that breadth is going to widen,” Goldman said.

“Maybe we’re already seeing that priced in.”

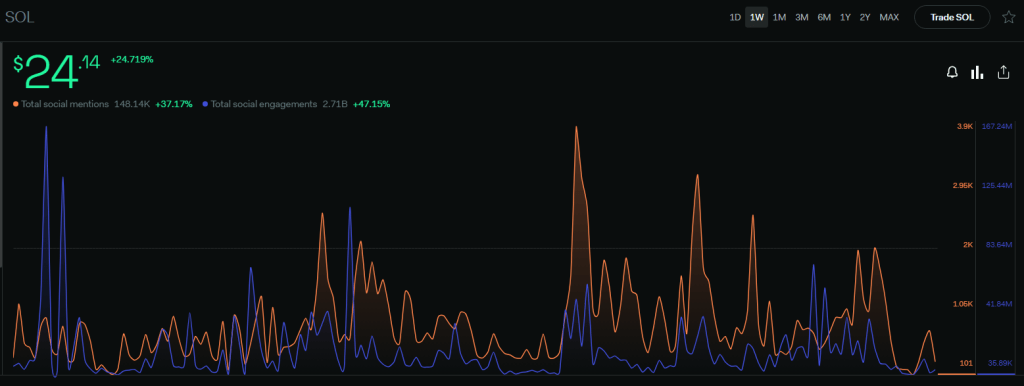

Solana (SOL) has emerged as a standout performer in the recent crypto market rally, catching the attention of investors and analysts alike. The entire cryptocurrency market has been on a bullish streak, with most digital assets turning green on the charts. However, Solana has managed to stand out by achieving an unprecedented increase in its price.

At the time of writing, SOL was trading at $23.54 on CoinGecko and boasted a market capitalization near $10 billion. While the coin did register a 1.6% loss in the past 24 hours, its seven-day surge of 22% indicated its resilience and potential for further growth.

In fact, this remarkable price uptrend enabled Solana to surpass both Dogecoin (DOGE) and Cardano (ADA), securing its position as the seventh-largest cryptocurrency by market capitalization.

BREAKING: $SOL FLIPS $DOGE AND $ADA IN MARKET CAP pic.twitter.com/RXKCBQinIJ

— DEGEN NEWS 🗞️ (@DegenerateNews) September 30, 2023

One key factor behind Solana’s surge was its impressive 100%+ increase in 24-hour trading volume, providing robust support for its price appreciation. Additionally, Solana’s performance within the decentralized finance sector also experienced notable growth during this period.

The positive sentiment surrounding Solana was further evidenced by data from LunarCrush, which indicated a nearly 47% surge in SOL’s social engagement over the last seven days. Investors and enthusiasts were increasingly drawn to the coin as its price continued to rise.

Source: LunarCrush

Pseudonymous analyst Inmortal, active on the social media platform X, expressed optimism about Solana’s potential. Inmortal believes that Solana presents a significant opportunity for long-term investors to accumulate the cryptocurrency at a point of maximum potential.

In two years you will realize that everything was as simple as buying $SOL below $20 and wait.

But you were too scared because FTX was going to dump their coins.

— Inmortal (@inmortalcrypto) September 20, 2023

According to Inmortal, those who accumulate SOL at its current price point are likely to be handsomely rewarded in the coming years. In a statement, Inmortal said, “In two years, you will realize that everything was as simple as buying SOL below $20 and waiting. But you were too scared because FTX was going to dump their coins.”

SOL market cap approaches the $10 billion level. Chart: TradingView.com

Concerns had arisen when court documents revealed that FTX owns approximately $1.16 billion worth of SOL. This led many traders to speculate that Solana’s price might face downward pressure if FTX were to liquidate its holdings.

However, notable investor Chris Burniske pointed out that only a fraction of FTX’s SOL holdings are actually liquid, stating, “Only ~13% of FTX’s SOL holdings are liquid… Keep a cool head, folks.”

As Solana continues to gain traction in the crypto market, investors are closely watching its performance, with many betting on the coin’s long-term potential and the possibility of significant rewards for those who enter the market now.

The recent surge in Solana’s price and its positive developments in the DeFi space have solidified its position as a cryptocurrency to watch.

(This site’s content should not be construed as investment advice. Investing involves risk. When you invest, your capital is subject to risk).

Featured image from

Crypto asset businesses in the United Kingdom could now begin withholding certain crypto transfers to comply with the new Travel Rule for crypto that came into effect on Sept. 1.

The rules targeting virtual asset service providers were first introduced by the Financial Conduct Authority on Aug. 17, requiring that VASPs based in the U.K. “collect, verify and share information” relating to crypto-asset transfers.

If an inbound payment is received from a person or entity from an overseas jurisdiction that hasn’t implemented the Travel Rule, the VASP must make a “risk-based assessment” as to “whether to make the cryptoassets available to the beneficiary.”

The Travel Rule is designed to bring greater transparency to cryptoasset transfers, making it harder for criminals to use #crypto for illegal activity.https://t.co/kmB6rgMn5e

— Financial Conduct Authority (@TheFCA) August 17, 2023

The same rule would also apply to Brits looking to send payments outside of the U.K.

The Travel Rule was created by the UN agency Financial Action Task Force in June 2019. The U.K. passed legislation to begin enforcing the Travel Rule in July 2022.

It attempts to enforce Anti-Money Laundering and Counter-Terrorist Financing rules on activities carried out on-chain.

Other countries that have adopted the Travel Rule include the U.S., Germany, Japan, Singapore, Switzerland, Canada, South Africa, the Netherlands and Estonia, according to Sygna.io.

Related: Crypto ads face stricter rules, referral bonus ban by UK FCA

On June 23, the FATF called out member states for failing to sufficiently implement the rule after a survey revealed more than half of them have failed to take any action towards implementing the rule.

A March 2022 survey by FATF found only 29 of 98 jurisdictions at the time passed the requirements needed as part of the travel rules and a small subset of these jurisdictions had started enforcement.

Ian Andrews, the chief marketing officer of blockchain forensics platform Chanalysis, explained in April 2022 that coordinating the exchange of information between VASPs cross-borders will be a “pretty hard problem” to solve — at least at the onset.

Collect this article as an NFT to preserve this moment in history and show your support for independent journalism in the crypto space.

Magazine: Deposit risk: What do crypto exchanges really do with your money?

As Jerome Powell, the Federal Reserve (Fed) Chair, prepares to return to Jackson Hole this Friday, the Bitcoin (BTC) market is experiencing a sense of anticipation due to the similarities in the current price action compared to the period leading up to last year’s speech.

Key moving averages have been tested and lost over the past two weeks, followed by a period of consolidation, reminiscent of previous events.

However, it is important to note that these similarities do not guarantee a repeat of the past, as market conditions and Powell’s stance have since evolved.

According to Keith Alan, co-founder of analysis and crypto research firm Material Indicator, last year, in the two weeks preceding Powell’s speech, BTC’s price broke through crucial technical support levels represented by the 21-day, 50-day, 100-day, and 200-week Moving Averages (MA).

Subsequently, a period of consolidation ensued, followed by a significant price drop in response to Powell’s hawkish tone during the speech. Alan stated:

Remember when Fed Chair Powell spoke from Jackson Hole last year and his hawkish tone triggered a 29% BTC dump that took 5 months to recover?

Notably, the recent price action in the Bitcoin market has displayed similarities to last year’s pattern. Over the past two weeks, Bitcoin has tested and lost these same key moving averages, and it is currently undergoing a phase of consolidation, mirroring the events leading up to Powell’s previous address.

Keith Alan emphasizes that since last year’s Jackson Hole event, there have been notable changes. Core inflation has decreased, and Powell’s approach to communication has become more “measured”.

It is uncertain whether Powell will adopt a hawkish or dovish stance in his upcoming speech, making it challenging to predict the market’s reaction with certainty. What is evident, however, is that the market is primed for a significant move.

Additionally, Alan suggests that the formation of a lower low in price increases the likelihood of an extension of the existing downtrend. Market participants should be prepared for the possibility of further testing of support levels.

As the Bitcoin market awaits Powell’s speech, market sentiment remains dynamic. Traders and investors are anticipating potential market-moving cues from the event.

As the date of Jerome Powell’s return to Jackson Hole approaches, Bitcoin has displayed a notable recovery of 2.1% within the past 24 hours, marking a positive upward movement that brings it closer to the $27,000 threshold.

However, it is crucial to note that if the outcome of Jerome Powell’s speech on Friday proves favorable for crypto investors and propels Bitcoin’s price to higher levels, the cryptocurrency may encounter a significant obstacle in the form of its 200-day moving average positioned at $27,200.

Featured image from iStock, chart from TradingView.com

Tesla (TSLA) released its second quarter production and delivery numbers on Sunday, easily beating expectations as the effects of the electric-vehicle maker’s price cuts, combined with federal EV tax credits, are boosting sales.

For the quarter, Tesla reported global production of 479,700 units with deliveries of 466,140. The delivery figure easily topped Wall Street consensus estimates of 448,599 units, as well as the prior quarter’s total of 422,875. Both production and delivery totals for the second quarter were all-time records for Tesla.

Analysts and investors focus more on delivery totals because they most closely track sales totals, which Tesla does not release. Breaking down delivery totals, Tesla delivered 446,915 Model 3 and Model Ys and 19,225 higher-priced Model S and Model X vehicles. The company also said 5% of its sales were subject to lease accounting.

Tesla’s second quarter delivery beat indicates the company’s price cuts are continuing to boost sales both in the US and abroad, though questions remain as to how deep a cut profits will take. Tesla also got another boost from the federal government in Q2 as well, as all trims of the Model 3 sedan qualified for the full $7,500 federal tax credit.

Separately, Wall Street analysts in the past two weeks have been downgrading Tesla shares after a massive run-up in the stock following big gains in the tech sector. Many analysts attributed the run-up to the big gains made by AI-related stocks, with analysts cautioning Tesla wasn’t the big AI-play many investors seemed to believe. Analysts like Mark Delaney at Goldman and Adam Jonas at Morgan Stanley see the stock as fairly valued at the moment.

Finally, Tesla announced it would be releasing second quarter earnings results after the bell on July 19th.

—

Pras Subramanian is a reporter for Yahoo Finance. You can follow him on Twitter and on Instagram.

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance

(Bloomberg) — Federal Reserve policymakers are about to take their first break from an interest-rate hiking campaign that started 15 months ago, even as they confront a resilient US economy and persistent inflation.

Most Read from Bloomberg

The Federal Open Market Committee on Wednesday is expected to maintain its benchmark lending rate at the 5%-5.25% range, marking the first skip after 10 consecutive increases going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

Investors’ focus will be on the Fed’s quarterly dot plot in its Summary of Economic Projections, which is expected to show the policy benchmark rate at 5.1% at the end of 2023.

By contrast, markets are pricing in the possibility of a quarter-point hike in July followed by a similar-sized cut by December, and some Fed policymakers have emphasized that a pause in the hiking cycle shouldn’t be seen as the final increase.

Fed Chair Jerome Powell, who’ll hold a press conference after the meeting, has suggested he favors a break from hiking to assess the impact both of past moves and of recent banking failures on credit conditions and the economy. His commentary will be scrutinized for hints of the committee’s plans at its following meeting next month.

What Bloomberg Economics Says:

“Discord on the FOMC is mounting. Those who prefer to skip a hike in June want to wait and see — given the long and variable lags of monetary policy — how 500 basis points of rate hikes to date are cooling the economy. More hawkish members are convinced rates aren’t yet restrictive enough, and the Fed shouldn’t risk falling behind the curve. We see a ‘hawkish skip’ as a way to maintain unanimity on the committee.”

—Anna Wong, Stuart Paul, Eliza Winger and Jonathan Church, economists. For full analysis, click here

Fed officials will have new consumer price index data in hand when they start their monetary policy deliberations on Tuesday. While central bankers target a separate inflation measure for their 2% goal, the closely watched CPI report is expected to show still-stout underlying price pressures.

The core gauge, which excludes volatile food and energy prices, is seen rising 0.4% from a month earlier. That would mark the sixth-straight month that core inflation has increased by that much or more, and helps to explain why interest rates may stay elevated for longer.

Monthly advances of that magnitude have made it difficult for underlying inflation to cool quickly. On a year-over-year basis, the core CPI is expected to rise 5.2%, the slowest pace since November 2021. The overall CPI is projected to recede to 4.1%. While still uncomfortably high, gradually moderating inflation provides some space for the central bank to pause.

A report on Wednesday is projected to show further disinflation at the producer level, with a core gauge seen rising at the slowest annual pace in more than two years as goods costs continue to settle back.

May retail sales round out top US economic data this coming week. The value of purchases was probably little changed during the month, consistent with softer consumer demand for merchandise.

Further north, Canada’s tight housing supply will be a focus after a revitalized real estate market helped prompt a resumption of rate increases. Data on Thursday will show whether housing starts kept falling in May, eroding the potential supply of homes amid record immigration, and if existing home sales kept rising too.

Elsewhere in the world, the European Central Bank is likely to keep raising rates, the Bank of Japan may remain on hold, and Chinese monetary officials could avoid adding stimulus for now.

Click here for what happened last week and below is our wrap of what’s coming up in the global economy.

Europe, Middle East, Africa

The day after the Fed decision, ECB officials are almost certain to diverge from their US counterparts and press on with rate increases. Economists expect a second consecutive quarter-point move. With another hike also widely touted for July, the focus is likely to fall on the details of new quarterly forecasts and on any hints about prospects for yet another move in September.

Further to that, a final take on euro-zone inflation in May will be published on Friday, along with the ECB’s survey of professional forecasts, illustrating the collective view of the economics community on the central bank’s outlook.

In the Nordic region, Danish inflation will be released on Monday, and later in the week, monetary officials there may follow the ECB’s rate decision with a hike of their own, as they typically do.

Meanwhile, monthly growth data in Norway and inflation and consumer expectations data in Sweden will be informative for central banks in those countries, which are still in tightening mode.

Further east, the Ukrainian central bank will announce its key rate decision at a time its war-torn economy appears to be improving faster than previously estimated.

Central banks across Africa will make decisions in the coming week as well:

On Tuesday, the Bank of Uganda’s monetary policy committee will likely hold its key rate for a third successive meeting after inflation slowed sharply in May to 6.2%.

The following day, Namibian officials will probably increase borrowing costs to safeguard their currency peg with the rand after neighboring South Africa raised rates by 50 basis points.

Central banks in Botswana and Mauritius are both expected to hold rates steady on Thursday, with inflation projected to continue slowing toward their targets.

Thursday’s also a big day for fiscal announcements. Kenya, Tanzania, Uganda, Rwanda and Burundi will unveil budgets expected to increase spending to boost recoveries from shocks such as droughts, the pandemic and Russia’s war on Ukraine.

Saudi Arabian data on Thursday is likely to show inflation steadied in May, and will probably be close to the 2.7% seen in April. The kingdom’s economy has slowed in the past three quarters, in large part because of global weakness causing a drop in oil prices.

The same day, investors will be watching whether Israeli inflation accelerated in May as the shekel weakened. The currency fell 2.7% against the dollar last month on renewed concerns over Prime Minister Benjamin Netanyahu’s plan to overhaul the judiciary.

Asia

Key Chinese economic indicators set for release on Thursday will likely show a slowdown in consumer and business activity in May as the post-pandemic boost fades.

The People’s Bank of China will have an opportunity to add more monetary stimulus, although the majority of economists surveyed by Bloomberg predict no change to rates just yet.

Hong Kong and Taiwan will also announce rate decisions on Thursday.

The Bank of Japan has its second policy meeting under Governor Kazuo Ueda at the end of the week. Most economists expect no change this time as speculation rumbles on that Prime Minister Fumio Kishida is mulling an early election.

Trade figures from Japan, India, and Indonesia on Thursday are set to show the latest state of global demand, while New Zealand also reports on its first quarter growth that day.

Latin America

Brazil’s retail sales data for April won’t likely maintain the pace seen in the strong close to the first quarter, giving President Luiz Inacio Lula da Silva more reason to hector the central bank in pursuit of lower rates.

Similarly, Brazilian GDP-proxy data for April will likely falter as Latin America’s biggest economy down-shifts from much-stronger-than-expected first-quarter output readings.

Central banks in Brazil, Colombia and Chile publish surveys of economists’ expectations, with Banco Central de Chile also posting a separate survey of traders.

Colombia posts April manufacturing, industrial output and retail sales results, which turned negative in March as the the highest borrowing costs since 1999 weighed on consumers and companies and undercut confidence.

Peru’s monthly GDP-proxy reading for April is likely to build on March’s rebound with mining operations normalizing after labor disruptions and civil unrest in the country’s south.

Argentina’s May inflation report should show a 16th straight rise in consumer prices pushing the annual rate over 116%, against the current 108.8%.

Low international reserves, an overvalued peso and presidential elections in October suggest the government lacks the tools and likely won’t have the appetite to do much about inflation before year-end.

–With assistance from Robert Jameson, Monique Vanek, Michael Winfrey and Laura Dhillon Kane.

Most Read from Bloomberg Businessweek

©2023 Bloomberg L.P.