The Federal Reserve should keep credit conditions tight for now.

Source link

The Federal Reserve should keep credit conditions tight for now.

Source link

Enbridge (ENB 0.95%) has enriched investors over the years. The Canadian energy infrastructure behemoth pays a massive and steadily growing dividend (currently yielding 7.7%). The high-yielding payout, combined with its growing earnings, has given it the fuel for an 11.2% compound annual growth rate in its total shareholder return over the last 20 years. That’s outperformed the S&P 500‘s total return of 9.7%, as well as Enbridge’s peers in the utilities (8%) and midstream (7.7%) sectors.

The pipeline and utility giant should be able to continue producing double-digit annualized total returns over the next several years. Here’s a look at two factors supporting that view.

One of the great things about dividend stocks like Enbridge is that they supply investors with a tangible base return in the form of dividend income. At its current dividend payment level, Enbridge can generate an annual income return of roughly 7.7% for investors who buy around the current price.

Unlike those of some high-yield dividend stocks, that’s a very bankable return. The company generates durable and stable cash flows. It has a diversified portfolio; its low-risk utility assets include gas transmission and storage and renewable power, and its midstream businesses include liquids pipelines and gas transmission. Enbridge gets 98% of its earnings from low-risk commercial frameworks like cost-of-service agreements and long-term, fixed-rate contracts with high-quality customers (95% have investment-grade credit ratings).

The durability and predictability of its earnings have been on full display over the years. Enbridge has achieved its financial guidance in each of the last 17 years despite several significant market dislocations.

Meanwhile, the company has a reasonable dividend payout ratio — 60% to 70% of its distributable cash flow. That gives it a comfortable cushion, while allowing it to retain significant excess free cash to fund new investments and maintain its financial strength. The company also has a solid leverage ratio that’s currently below its target range of 4.5 to 5.0 (a very comfortable level for its utility-like cash flows). That conservative leverage ratio further enhances its financial flexibility.

Enbridge’s low-risk business model and conservative financial profile give it tremendous financial capacity. The company estimates that it has 8 billion to 9 billion Canadian dollars ($5.9 billion to $6.7 billion) of total annual investment capacity, between its excess free cash flow after paying dividends and balance-sheet flexibility within its current leverage target. That gives it the funds to invest in organic expansion projects, make accretive acquisitions, and opportunistically repurchase shares.

All of that supports the company’s base growth plan. It currently has a massive CA$25 billion ($18.5 billion) of commercially secured capital projects in its backlog. It expects to invest CA$6 billion to CA$7 billion ($4.4 billion to $5.2 billion) annually to build these projects, which should enter commercial service through 2028.

Enbridge’s backlog gives it lots of visibility into its earnings growth rate over the next few years. Those projects will grow its earnings by around 3% annually. Cost savings and optimizations will add another 1% to 2% to its bottom line each year. Enbridge will also get a bump from mergers and acquisitions, with its deal to buy three gas utilities from Dominion Energy, providing a meaningful near-term boost.

Add it all up, and these catalysts should grow adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) by 7% to 9% annually through at least 2026. Distributable cash flow should rise by around 3% per share each year, weighed down by some modest tax legislation headwinds and new shares issued to fund the Dominion deals. That growing cash flow will enable Enbridge to continue increasing its dividend.

There’s more growth beyond 2026. Enbridge has already secured several expansion projects that should enter service in 2027 and 2028, and it has several more under development. It also has the growing capacity to deploy additional capital into accretive acquisitions. Put it all together, and Enbridge believes it can grow its adjusted EBITDA and distributable cash flow per share by around 5% annually over the medium term. That should fuel dividend growth of as much as 5% per year.

With a dividend yield currently at 7.7%, Enbridge provides investors with a rock-solid base return. On top of that, the company expects to grow its cash flow per share by around 3% annually through 2026 (with acceleration expected beyond that year).

So the company should be able to produce an average annualized total return of more than 10% — an excellent return potential for such a low-risk stock. It makes Enbridge a great long-term investment opportunity.

Matt DiLallo has positions in Enbridge. The Motley Fool has positions in and recommends Enbridge. The Motley Fool recommends Dominion Energy. The Motley Fool has a disclosure policy.

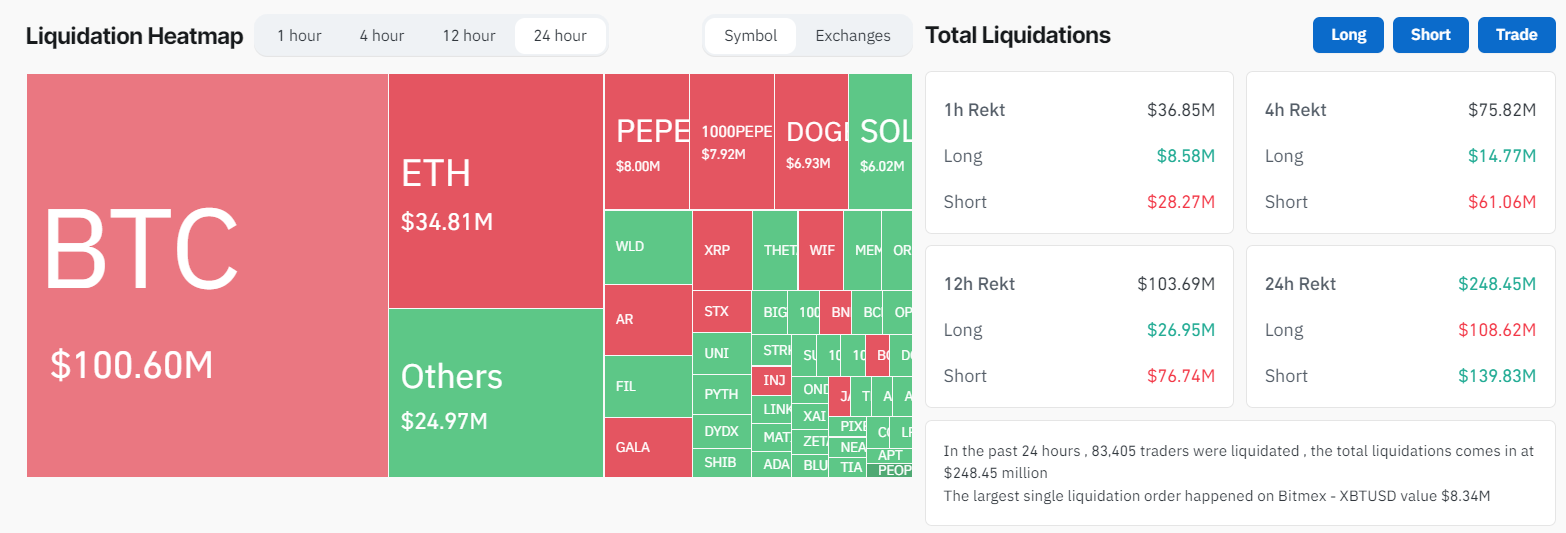

Bitcoin is currently demonstrating a robust market performance, bulldozing its way towards the $60,000 benchmark, up from its daily start of around $57,000. In the preceding 24 hours, a significant wave of liquidations hit the digital asset market, amounting to approximately $250 million. The liquidations depict a slight bias towards shorts, with an estimated worth of $140 million, according to Coinglass.

Coinglass data shows that in the same timeframe, Bitcoin experienced $100 million worth of liquidations, majorly shorts accounting for $70 million.

Simultaneously, the Exchange Traded Fund (ETF) inflows marked their third-best performance day, underlining the growing interest of institutional investors in this digital asset. A noteworthy mention is BlackRock, which recorded a record-breaking single-day performance with net inflows of $520 million.

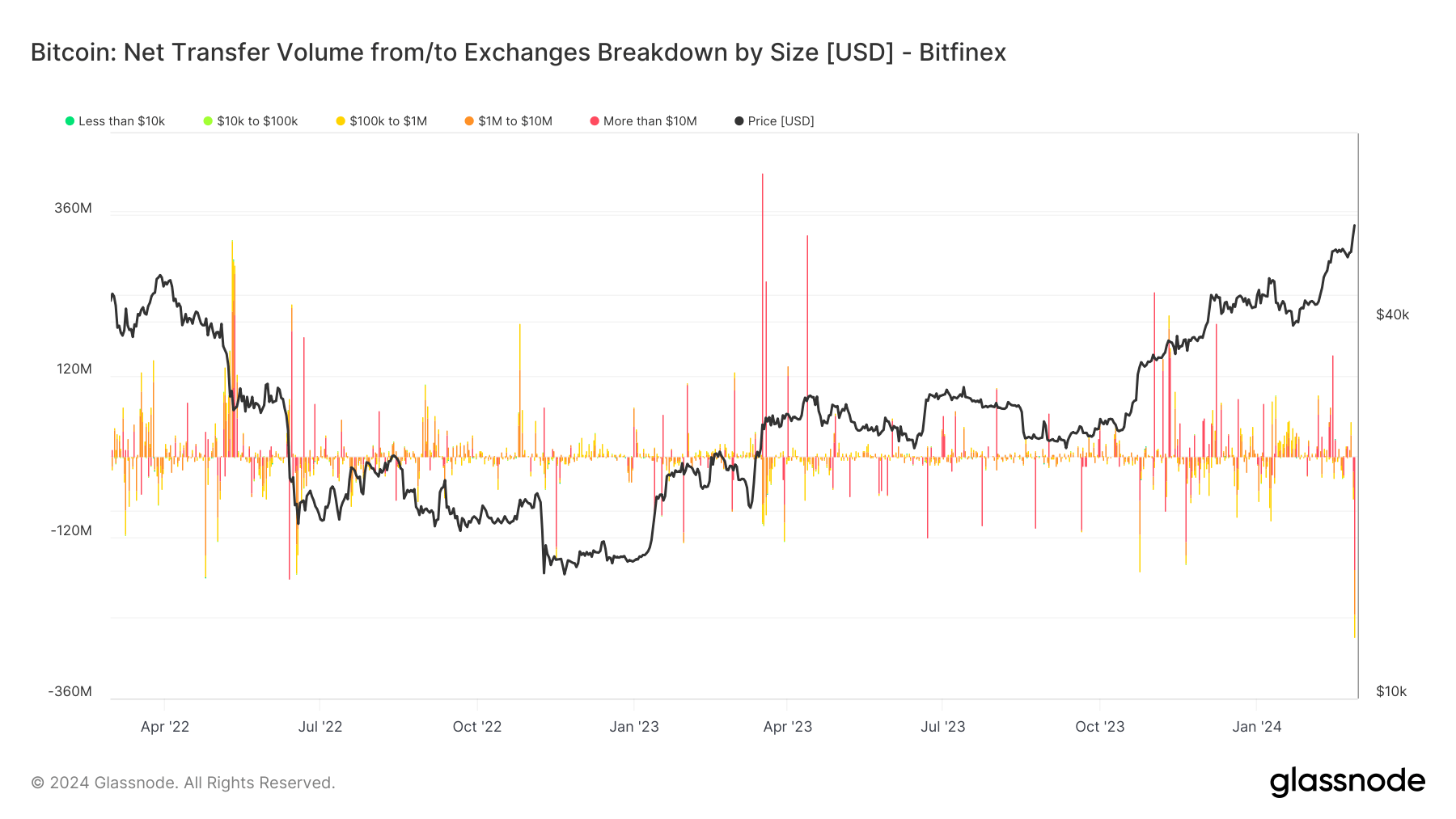

The day further witnessed the largest Bitcoin withdrawal from Bitfinex since 2021, exceeding $240 million. This substantial offloading, estimated to be the equivalent of 5,000 Bitcoins, was primarily attributed to large whale activities.

The post Whale transactions and ETF records fuel Bitcoin’s push toward $60,000 appeared first on CryptoSlate.

By most measures, investors have reason to be skeptical about vaccine specialist Novavax (NASDAQ:NVAX). Once heralded as a key player in the race to find a solution for the COVID-19 disaster, Novavax shares collapsed as fears of the virus faded sharply. Since then, the company has struggled for relevance. While very few experts will see the biotechnology firm as a robust investment opportunity, too much bad news could fuel a shocking reversal. Therefore, I am near-term bullish on NVAX stock.

Before diving into the factors that could spark a rally that few believe possible, it’s important to acknowledge the deep-seated troubles Novavax faces. For example, even with the promise of a new year, NVAX stock fell by a staggering 20% since the beginning of January. And just to reinforce the point, in the past 52 weeks, NVAX had shed about 66% of its equity value.

If stakeholders were hoping for an auspicious start, this wasn’t it. Further, management itself isn’t giving off encouraging signals. As the TipRanks Newsdesk pointed out recently, Novavax announced a strategic plan to reduce its annual spending. That’s the fancy way of saying it will lay off its global workforce. Unfortunately, the job cuts will impact approximately 12% of the firm’s full-time employees and contractors.

Moreover, it wasn’t the first time Novavax resorted to a headcount reduction. In May 2023, management made the decision to cut 25% of its workforce. While the move should theoretically help streamline its financials, the main issue has always been scientific relevancy.

According to The New York Times, Novavax was on the verge of collapse a year before the COVID-19 crisis. “One of its leading vaccine candidates — to prevent a deadly virus in infants — had failed for the second time in three years. The company’s stock was trading so low that it risked being removed from the Nasdaq,” the NYT wrote.

Then, the pandemic gave NVAX stock a second lease on life. Certainly, it made the most of its opportunity. On a weekly average basis, NVAX briefly breached the $290 level. However, since December 2021, Novavax has been struggling to gain traction.

Essentially, the company is almost back to where it once was. With the COVID catalyst all but gone, management must convince its remaining shareholders to hold true. That’s a gargantuan task. However, NVAX stock may still get its lifeline.

Given the terrible print, traders may be tempted to bet against NVAX stock. That might be a bad idea. Like a sports wager, if the bookie sweetens the pot with line adjustments that increasingly favor the underdog, at some point, betting on the favorite could be a risky venture. And that may be the case with Novavax.

Unsurprisingly, an options flow screener – which exclusively filters for big block transactions likely made by institutions – shows heavy volume of short (sold) calls. Basically, these are bets that the underlying security will not rise above a specified strike price. In particular, on January 16, a trader (or traders) sold 7,355 contracts of the NVAX Apr 19 ’24 5.00 Call.

Additionally, it’s a high-conviction trade. For underwriting the risk, the call sellers received a premium of $371,000. However, at the money, the baseline totality of this trade is worth about $3.68 million (7,355 contracts multiplied by 100 shares per contract multiplied by the $5 strike). And the underlying liability is uncapped because NVAX stock could theoretically rise indefinitely.

Now, many, if not most, traders likely believe that Novavax won’t rise materially higher; hence, the high short call volume. Still, because so many traders are standing on one side, the gamma exposure for the option arena’s market makers stands at $140,000 for every 1% stock move. In a bid to be “delta neutral,” the market maker would be forced to take opposite wagers should NVAX stock move unexpectedly.

To quickly explain, in options trading, gamma exposure measures the rate of change in an option’s delta concerning the underlying stock’s price movement. To hedge against risk and maintain delta neutrality, market makers may need to adjust their options positions by taking counteractive measures.

Such an unexpected move could very well occur because NVAX simultaneously runs an extremely high short interest of 48.24% of its float. Also, the short-interest ratio stands at 9.44 days to cover, requiring about two trading weeks for the bears to fully unwind their short position based on average trading volume.

If NVAX stock swings higher for whatever reason, it could panic the shorts in the open market, which could easily cascade into panic in the options market as the sold calls get blown up.

While it’s critical to stress that NVAX stock could catch unsuspecting prospective bears off guard, such a framework centers on the nearer-term narrative. Should investors consider Novavax as a longer-term buy? In my view, no. It’s just too risky.

Perhaps most glaringly, the company posted revenue of just under $187 million in the third quarter of Fiscal 2023. In sharp contrast, Novavax generated sales of $628.3 million in the year-ago period. Adding to the misery, without a clear product candidate, the biotech’s future is very much in question.

Turning to Wall Street, NVAX stock has a Hold consensus rating based on two Buys, one Hold, and one Sell rating. The average NVAX stock price target is $14.75, implying 275.3% upside potential.

Embattled Novavax could see a short-term rally due to heavy bearish bets. Despite facing significant challenges, including declining revenue and workforce reductions, the high short interest and concentrated short call positions leave NVAX stock vulnerable to a potential squeeze if the share price unexpectedly rises. However, this is not considered a long-term investment opportunity due to the company’s uncertain future and lack of a clear product candidate.

Bristol Myers Squibb Co.

BMY,

on Friday reported fourth-quarter results that beat analysts’ expectations, helped by portfolio stalwarts like the blood thinner Eliquis as well as strong growth among newer drugs.

The drugmaker reported fourth-quarter net income of $1.762 billion, or 87 cents per share, down from $2.022 billion, or 95 cents per share, in the year-earlier period. Adjusted earnings per share came to $1.70, down 7% from a year earlier but ahead of the FactSet consensus of $1.55. Revenue totaled $11.477 billion in the quarter, up 1% from a year earlier and topping the FactSet consensus of $11.192 billion.

For the full year 2024, Bristol Myers Squibb said it expects sales growth in the low single-digits and adjusted earnings per share of $7.10 to $7.40, ahead of analysts’ estimates.

Among Bristol Myers’ top-selling products, growth in sales of blood thinner Eliquis and cancer drug Opdivo helped offset declining sales of multiple myeloma treatment Revlimid, which is facing generic competition.

Eliquis, one of 10 drugs selected for the first round of Medicare price negotiations under the Inflation Reduction Act, generated $2.87 billion in sales in the fourth quarter, up 7% from a year earlier and slightly ahead of analysts’ expectations.

Revlimid sales fell 36% from a year earlier, to $1.45 billion in the fourth quarter.

Bristol Myers’ new product portfolio accounted for $1.072 billion in sales in the quarter, up 66% from a year earlier. Melanoma treatment Opdualog and anemia drug Reblozyl helped fuel that growth, but sales of the CAR-T cell therapy Abecma fell 20%, to $100 million.

The company’s partner on Abecma, 2seventy bio Inc.

TSVT,

said earlier this week that it is pivoting to focus exclusively on the development and commercialization of the cell therapy and is selling its research-and-development pipeline to Regeneron Pharmaceuticals Inc.

REGN,

With analysts watching for a reset after a rough 12 months, as the shares have dropped more than 30%, Bristol Myers has been on a shopping spree lately. In December, the company struck deals to buy radiopharmaceuticals company RayzeBio Inc.

RYZB,

as well as Karuna Therapeutics Inc.

KRTX,

which has a key experimental schizophrenia treatment, KarXT. A regulatory decision on KarXT is expected in September.

Last month, the company closed its acquisition of cancer drugmaker Mirati Therapeutics Inc.

Bristol Myers Squibb shares are down 5.2% year to date, while the S&P 500

SPX

has gained 2.9%.

Prices at a Chevron Corp. gas station in Fontana, California, on Thursday, July 8, 2021.

Kyle Grillot | Bloomberg | Getty Images

On Monday, Chevron announced plans to acquire oil and gas company Hess for $53 billion in stock.

Less than two weeks prior, Exxon Mobil announced it is acquiring oil company Pioneer Natural Resources for $59.5 billion in stock.

On Tuesday, the International Energy Agency released its annual world energy outlook report that projects global demand for coal, oil and natural gas will hit an all-time high by 2030, a prediction the IEA’s executive director Fatih Birol had telegraphed in September.

“The transition to clean energy is happening worldwide and it’s unstoppable. It’s not a question of ‘if,’ it’s just a matter of ‘how soon’ — and the sooner the better for all of us,” Birol said in a written statement published alongside his agency’s world outlook. “Taking into account the ongoing strains and volatility in traditional energy markets today, claims that oil and gas represent safe or secure choices for the world’s energy and climate future look weaker than ever.”

But based on their acquisitions, Chevron and Exxon are seemingly preparing for a different world than the IEA is portending.

“The large companies — nongovernment companies — do not see an end to oil demand any time in the near future. That’s one of the messages you have to take from this. They are committed to the industry, to production, to reserves and to spending,” Larry J. Goldstein, a former president of the Petroleum Industry Research Foundation and a trustee with the not-for-profit Energy Policy Research Foundation, told CNBC in a phone conversation Monday.

“They’re in this in the long haul. They don’t see oil demand declining anytime in the near term. And they see oil demand in fairly large volumes existing for at least the next 20, 25 years,” Goldstein told CNBC. “There’s a major difference between what the big oil companies believe the future of oil is and the governments around the world.”

So, too, says Ben Cahill, a senior fellow in the energy security and climate change program at the bipartisan, nonprofit policy research organization, Center for Strategic and International Studies.

“There are endless debates about when ‘peak demand’ will occur, but at the moment, global oil consumption is near an all-time high. The largest oil and gas producers in the United States see a long pathway for oil demand,” Cahill told CNBC.

Pioneer Natural Resources crude oil storage tanks near Midland, Texas, on Oct. 11, 2023.

Bloomberg | Bloomberg | Getty Images

Globally, momentum behind and investment in clean energy is increasing. In 2023, there will be $2.8 trillion invested in the global energy markets, according to a prediction from the IEA in May, and $1.7 trillion of that is expected to be in clean technologies, the IEA said.

The remainder, a bit more than $1 trillion, will go into fossil fuels, such as coal, gas and oil, the IEA said.

Continued demand for oil and gas despite growing momentum in clean energy is due to population growth around the globe and in particular, growth of populations “ascending the socioeconomic ladder” in Africa, Asia and to some extent Latin America, according to Shon Hiatt, director of the Business of Energy Transition Initiative at the USC Marshall School of Business.

Oil and gas are relatively cheap and easy to move around, particularly in comparison with building new clean energy infrastructure.

“These companies believe in the long-term viability of the oil and gas industry because hydrocarbons remain the most cost-effective and easily transportable and storable energy source,” Hiatt told CNBC. “Their strategy suggests that in emerging economies marked by population and economic expansion, the adoption of low-carbon energy sources may be prohibitively expensive, while hydrocarbon demand in European and North American markets, although potentially reduced, will remain a significant factor.”

Also, while electric vehicles are growing in popularity, they are just one section of the transportation pie, and many of the other sections of the transportation sector will continue to use fossil fuels, said Marianne Kah, senior research scholar and board member at Columbia University’s Center on Global Energy Policy. Kah was previously the chief economist of ConocoPhillips for 25 years.

“While there is a lot of media attention given to the increasing penetration of electric passenger vehicles, global oil demand is still expected to grow in the petrochemical, aviation and heavy-duty trucking sectors,” Kah told CNBC.

Geopolitical pressures also play a role.

Exxon and Chevron are expanding their holdings as European oil and gas majors are more likely to be subject to strict emissions regulations. The U.S. is unlikely to have the political will to force the same kind of stringent regulations on oil and gas companies here.

“One might speculate that Exxon and Chevron are anticipating the European oil majors divesting their global reserves over the next decade due to European policy changes,” Hiatt told CNBC.

“They are also betting domestic politics will not allow the U.S. to take significant new climate policies directed specifically to restrain or limit or ban the level of U.S. oil and gas domestic production,” Amy Myers Jaffe, a research professor at New York University and director of the Energy, Climate Justice and Sustainability Lab at NYU’s School of Professional Studies, told CNBC.

Goldstein expects the ever-expanding U.S. national debt will eventually put all kinds of government subsidies on the chopping block, which he says will also benefit companies such as Exxon and Chevron.

“All subsidies will be under enormous pressure,” Goldstein said, the intensity of that pressure dependent on which party is in the White House at any given time. “By the way, that means the large financial oil companies will be able to weather that environment better than the smaller companies.”

Also, sanctions of state-controlled oil and gas companies in countries like those in Russia, Venezuela and Iran are providing Exxon and Chevron a geopolitical opening, Jaffe said.

“They likely hope that any geopolitically driven market shortfalls to come can be filled by their own production, even if demand for oil overall is reduced through decarbonization policies around the world,” Jaffe told CNBC. “If you imagine oil like the game of musical chairs, Exxon Mobil and Chevron are betting that other countries will fall out of the game regardless of the number of chairs and that there will be enough chairs left for the American firms to sit down, each time the music stops.”

An oil pumpjack pulls oil from the Permian Basin oil field in Odessa, Texas, on March 14, 2022.

Joe Raedle | Getty Images News | Getty Images

Known oil reserves are increasingly valuable as European and American governments look to limit the exploration for new oil and gas reserves, according to Hiatt.

“Notably, both Pioneer and Hess possess attractive, well-established oil and gas reserves that offer the potential for significant expansion and diversification for Exxon and Chevron,” Hiatt told CNBC.

Oil and gas reserves that can be brought to market relatively quickly “are the ideal candidates for production when there is uncertainty about the pace of the energy transition,” Kah told CNBC, which explains Exxon’s acquisition of Pioneer, which gave Exxon more access to “tight oil,” or oil found in shale rock, in the Permian basin.

Shale is a kind of porous rock that can hold natural gas and oil. It’s accessed with hydraulic fracking, which involves shooting water mixed with sand into the ground to release the fossil fuel reserves held therein. Hydrocarbon reserves found in shale can be brought to market between six months and a year, where exploring for new reserves in offshore deep water can take five to seven years to tap, Jaffe told CNBC.

“Chevron and Exxon Mobil are looking to reduce their costs and lower execution risk through increasing the share of short cycle U.S. shale reserves in their portfolio,” Jaffe said. Having reserves that are easier to bring to market gives oil and gas companies increased ability to be responsive to swings in the price of oil and gas. “That flexibility is attractive in today’s volatile price climate,” Jaffe told CNBC.

Chevron’s purchase of Hess also gives Chevron access in Guyana, a country in South America, which Jaffe also says is desirable because it is “a low cost, close to home prolific production region.”

Don’t miss these CNBC PRO stories:

Just a few months ago, investors appeared relatively sanguine about the dreaded prospect of stagnant economic activity and rising inflation.

Oil prices surging to the brink of $100 per barrel and the specter of higher-for-longer inflation have renewed concern about stagflation risks, however.

“I think that the big bogeyman out there is stagflation, that we get into this spirit of high inflation and low growth,” Mel Lagomasino, CEO of WE Family Offices, told CNBC’s “Squawk Box” on Wednesday.

Lagomasino cited comments from Minneapolis Fed President Neel Kashkari, who said in an essay earlier this week that U.S. interest rates may have to go “meaningfully higher” to bring down stubbornly sticky inflation.

Kashkari reaffirmed this message when speaking to CNBC on Wednesday, saying that he was not sure if interest rates have been raised enough to successfully fight price growth.

“It looks like they might not just be higher for longer, they might be quite a bit higher for longer,” Lagomasino said, before adding that she believes a recession is “definitely” on the horizon.

Federal Reserve Board Chairman Jerome Powell speaks during a news conference after a Federal Open Market Committee meeting on September 20, 2023 at the Federal Reserve in Washington, DC.

Chip Somodevilla | Getty Images News | Getty Images

Stagflation was first recognized in the 1970s, when an oil shock prompted an extended period of higher prices but sharply falling economic growth.

The phenomenon is characterized by slow growth, high unemployment and soaring inflation. The one ingredient currently missing is the high unemployment, still relatively low at 3.8% — although there are fears that mounting layoffs may mean this could soon change.

Market participants are worried that surging oil prices could keep inflation higher for longer, amplifying the risk of stagflation.

Brent crude futures have jumped more than $20 a barrel in the three months to late September, a rally that has put a return to $100 sharply into focus. The international benchmark was last seen trading at $96.12 on Friday, up 0.8% for the session. U.S. West Texas Intermediate futures, meanwhile, rose 1.4% to trade at $92.96.

The price rally comes amid growing expectations of tighter supply, after Saudi Arabia, leader of OPEC, and non-OPEC heavyweight Russia moved to draw down global inventories and extend some of their voluntary oil supply cuts through to the end of the year. Together, OPEC and non-OPEC producers are known as OPEC+.

“By early summer, investors looked increasingly confident that the global economy was escaping the plague of stagflation,” analysts at Generali Investments said in a research note published Thursday.

“They are having a second thought – rightly so.”

Looking ahead to the fourth quarter, analysts at Generali Investments said the oil price surge was “most unwelcome” because this would likely keep headline U.S. inflation higher and hurt economic growth.

“The price pressure reflects a shortage of supply, after OPEC+ cut production targets, under the leadership of Saudi Arabia and Russia. This must be seen in the context of a moving geopolitical environment, with Saudi Arabia recently joining the BRICS group,” they added.

The BRICS economic coalition of emerging markets last month invited six countries to become members.

The alliance — which is currently composed of Brazil, Russia, India, China and South Africa — asked Argentina, Egypt, Iran, Ethiopia, Saudi Arabia and the United Arab Emirates to become new members of the bloc, with membership to take effect from Jan. 1, 2024.

Paul Gambles, co-founder and managing partner at MBMG Family Office Group, said Friday that rising oil prices could keep inflation higher for longer. He also suggested that policymakers appeared determined to bring the risk of stagflation back into the picture.

“The oil price is still really a wild card. And what we are seeing now is we can get into a situation where we do end up with softer demand for oil and yet the prices can still keep going higher because of the fact that there is this ability to constrain supply,” Gambles told CNBC’s “Squawk Box Europe.”

He cited Germany, Europe’s traditional growth engine, as one notable example where the mix of high inflation and low growth seems to have taken hold.

“Germany looks like it is on the precipice of a really significant slowdown combined with a potential inflation spike because of energy prices,” Gambles said.

“If you look at the premiums that are being charged on U.S. oil that is being shipped to Europe right now because of the low inventories in the states then it suggests that policymakers — aided by OPEC and the other oil suppliers — are doing everything they can to create the potential for stagflation. And that’s a real worry.”

SALEM, Ore. (AP) — For the first time in 72 years, Oregon motorists can grab a fuel nozzle and pump gas into their cars on their own, since a decades-old ban on self-serve gas stations has been revoked.

Gov. Tina Kotek signed a bill on Friday allowing people across the state to choose between having an attendant pump gas or doing it themselves. The law takes immediate effect.

That leaves New Jersey as the only state that prohibits motorists from pumping their own gas. A few countries also ban it, including South Africa, where attendants offer to check fluid levels and clean the windshield, with tipping expected.

“It’s about time. It’s long overdue,” said Karen Cooper, who lives in Salem, said shortly before the bill was signed.

“I’ve spent a lot of time in California,” Cooper said. “I know how to pump my own. Everybody should know how to pump their own gas.”

Kacy Willson, 32, who has lived in Oregon her whole life, said she doesn’t have much interest in pumping her own gas. She’s only tried it a few times in her life.

“It’s kind of nice to have someone do that,” she said at a Portland gas station Friday. “I don’t really leave Oregon very much, and when I do, I have to ask someone how to pump gas, and I feel weird.”

When Oregon prohibited self-service in 1951, lawmakers cited safety concerns, including motorists slipping on the slick surfaces at filling stations subject to Oregon’s notoriously rainy weather. In recent years legislators relaxed the rule and allowed rural counties to have self-serve gas available at night. Then they extended it to all hours in eastern Oregon’s sparsely populated areas, where motorists low on gas could be stranded when there’s no attendant on duty.

The COVID-19 pandemic labor shortage helped drive a renewed push to allow self-serve across the state.

“We live in a small town in a large county and can’t find employees to pump fuel,” Steve Rodgers, whose community is at the base of the snow-capped Cascade Mountains, complained to lawmakers. “We are paying top dollar and also offering insurance, paid time off and retirement benefits, and still cannot fully staff.”

Haseeb Shojai, who immigrated from Afghanistan in 2004 and owns gas stations in central Oregon’s high desert, also lamented the labor shortage and described how wildfires, with increased intensity and frequency due to climate change, are having a major effect. The state fire marshal lifted the self-serve ban during dangerous heat waves the past couple of summers.

“Wildfires have been a factor in operating our business in the summer months, when it is hard for our gas attendants to stay for long periods outside in smoke and in heat,” Shojai said. “We don’t know if we can stay open tomorrow or the next day or even next week due to the labor shortage.”

A union representing workers at grocery store fuel stations in Oregon predicted job losses and called the the law a “blatant cash grab for large corporations.”

“With over 2,000 gas stations in Oregon, laying off just one employee per location represents millions of dollars a year that giant corporations are not paying in wages, benefits and public payroll taxes,” said Sandy Humphrey, the secretary-treasurer of UFCW Local 555.

Under the new law, there can’t be more self-service pumps at a gas station than full-service ones. And prices for motorists must be the same at both types.

Still, opponents of the measure worry that it could lead to the demise of full-service pumps, depriving older adults and people with disabilities of that option.

“I have some real concerns that we are progressively getting closer and closer to eliminating Oregon’s fuel service law entirely,” Democratic state Sen. Lew Frederick said on the Senate floor in June before voting against the bill.

Brandon Venable, a service station manager, had urged lawmakers to reject the bill, saying some customers are careless and that attendants keep people safe.

“I deal with many dangerous situations daily created by people smoking, leaving their engines running, getting in and out of their vehicles creating static electricity, trying to fill up random bottles and jugs, and driving off with the pump still in the vehicle,” Venable said.

Others wonder if motorists who are now clamoring to pump their own gas might be less keen on doing so when they have to stand out in the rain, cold and snow instead of remaining in their warm, dry cars.

Republican state Sen. Tim Knopp, who leads the minority GOP caucus, downplayed safety concerns as he described being allowed to pump his own gas because he belongs to a commercial fueling cooperative.

“I have yet to light myself on fire. I have yet to cause any problems whatsoever as it relates to self-serve gas,” Knopp said during debate on the bill. “So, colleagues, let’s make New Jersey the only state in the country that has a law against self-serve gas.”

The state Senate then approved the bill on a 16-9 vote. The House earlier passed it 47-10.

New Jersey’s 1949 ban on self-service pumps remains a source of pride for some in a state where bumper stickers declare “Jersey Girls Don’t Pump Gas.”

Since New Jersey has lower gas prices than New York and Pennsylvania, many drivers from neighboring states cross the state line to fuel up.

In 2015, lawmakers proposed ending the New Jersey ban, but the measure died because of opposition from the powerful state Senate president.

___

Associated Press reporters Michael Catalini in Trenton, New Jersey, and Claire Rush in Portland, Oregon, contributed to this report.

Don’t miss these top money and investing features:

Sign up here to get MarketWatch’s best mutual funds and ETF stories emailed to you weekly!

Mutual-fund and ETF flows suggest that stock-market investors now are more fearful than greedy. Read More

U.S. stocks give no sell signals yet, but the market is now in a negative seasonal period. Read More

After rallying in the wake of the Fed’s recent meeting, the U.S. stock market is losing ground. Read More

The monthly review of recent Wall Street research. Read More

The lowdown on small-caps: They’re cheap and set up for a rebound. Read More

Nvidia will be the only chip maker positioned to exceed Wall Street expectations in the near term when it comes to AI, one analyst believes. Read More

Above-average real U.S. interest rates are bullish for bond investors Read More

A positive second-half return for the Dow is likely in any given year, regardless of market valuation. Read More

Vanguard’s latest retirement yearbook has a sobering message—and some hope. Read More

The path to increasing adults’ financial literacy may be through their children. Read More