Sometimes it can pay to own early-stage stocks with extremely high growth potential. Being early into stocks like Tesla or Amazon can create life-changing wealth for your portfolio, turning $1,000 into hundreds of thousands of dollars within a few decades.

But buying these types of stocks doesn’t come without risk and shouldn’t make up 100% of anyone’s portfolio. That’s where blue-chip businesses with strong competitive advantages come in.

Visa (V 0.51%) is one of those tried-and-true stocks that can produce steady price appreciation year after year. Here’s why the payment network has crushed the market and why it will be extremely hard for any competitor to disrupt in the years to come.

Visa: Industry dominance and market outperformance

Visa — as many readers know — is the leading credit card and digital payments network worldwide. It is estimated to have 40% market share globally among credit card payments and a whopping 60% market share in the United States.

However, you may not know that Visa doesn’t issue credit cards, but is simply the payments facilitator connecting bank accounts to retailers whenever someone makes a purchase. Financial institutions like Bank of America manage credit cards on the Visa network, taking all the credit risk and dishing out a small percentage of every transaction paid on the card back to Visa.

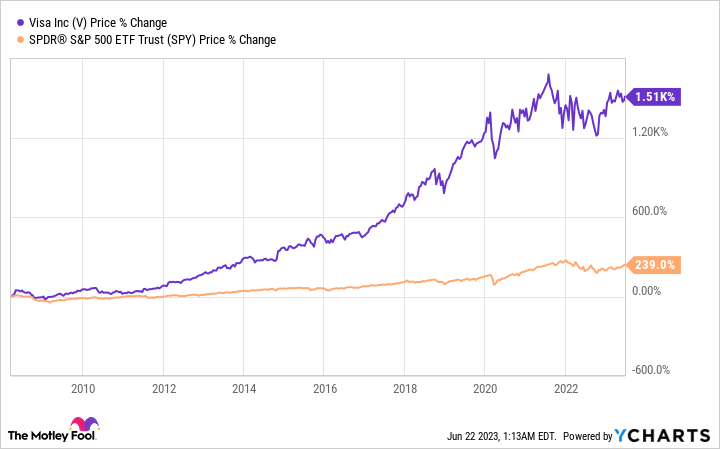

The stock has crushed the market since going public, up over 1,500% versus the S&P 500‘s 239% return. Why did this happen? A few reasons.

First is the general transition from people using cash/checks for payments to digital methods like credit cards. The majority of this transition happened in the last two decades or so — at least in the United States — and there’s no reason to think it won’t continue for the next decade around the globe.

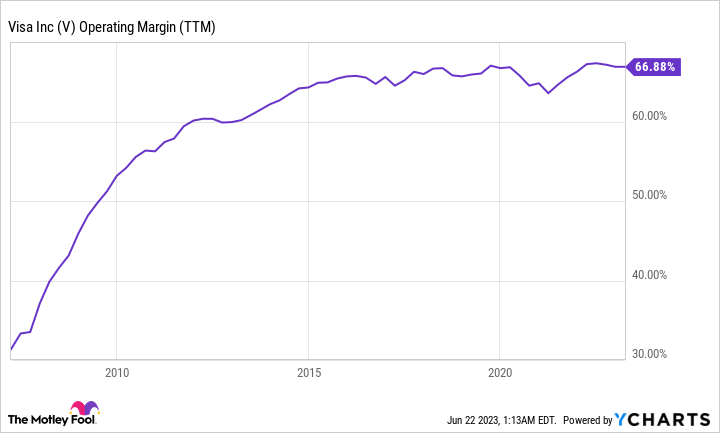

Second, Visa has close to zero variable costs, giving it incredible operating leverage as its annual payments volume has climbed higher. Over the last 12 months, its operating margin was an eye-popping 67%.

Third, and perhaps most important, is Visa’s extremely strong network effect that keeps it insulated from other card network competition. You can pay with a Visa card at over 100 million merchants around the globe, and merchants can accept payments from over 4.2 billion Visa cards in circulation.

The more cards in circulation, the more valuable it is for a merchant to use Visa for accepting payments, and vice versa for people deciding what credit card to use. As the number of merchants that accept Visa climbs higher, the more valuable it is for a person to have a Visa-backed payment solution. This dynamic makes it incredibly difficult for other card networks to compete with and this is why the industry has only a few other players like Mastercard and American Express.

V Operating Margin (TTM) data by YCharts

Is disruption coming?

A lot of companies have tried to disrupt Visa over the years. From PayPal 15 years ago to cryptocurrencies to buy-now-pay-later (BNPL) solutions, many people have poured billions of dollars into disrupting the credit card networks and have (so far) failed. We’ve even seen the proliferation of government-sponsored payment solutions in places like India and China. And yet, Visa’s revenue just keeps climbing higher.

Counterintuitively, a lot of these perceived “threats” to Visa are actually helping it grow. BNPL solutions have adopted the Visa network and now offer Visa-linked payment cards. Many perceive payment wallets like Apple Pay and Google Pay (part of Alphabet) to be threats to Visa, but most of the time these wallets are funded through payment cards linked to the Visa network.

In India, where the government invested heavily in its own payment solutions, Visa actually grew incredibly quickly. According to management, payment volumes in India are up 80% since 2019.

Investors should never ignore disruptive risks. But Visa shows time and again that it has so many advantages that it is almost impossible for upstarts to compete with.

The valuation isn’t crazy

Since Visa is such a good business, it typically trades at a premium valuation. Today, its price-to-earnings ratio (P/E) sits at 30, which is above the market average but below where it typically traded for the past five years.

V PE Ratio data by YCharts

Last quarter, Visa’s net revenue grew 11% year over year and steadily compounded over the last 10 years. With the continued growth of digital payments around the globe, this 10%-plus growth should continue for the next few years, if not longer.

Durable growth makes a premium P/E ratio much more palatable. If you hold Visa stock for the long term, it will likely put up solid returns for your portfolio.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Bank of America is an advertising partner of The Ascent, a Motley Fool company. American Express is an advertising partner of The Ascent, a Motley Fool company. Brett Schafer has positions in Alphabet and Amazon.com. The Motley Fool has positions in and recommends Alphabet, Amazon.com, Apple, Bank of America, Mastercard, PayPal, Tesla, and Visa. The Motley Fool recommends the following options: long January 2025 $370 calls on Mastercard, short January 2025 $380 calls on Mastercard, and short June 2023 $67.50 puts on PayPal. The Motley Fool has a disclosure policy.