Aside from the incredible jump we are seeing from artificial intelligence technology, another big growth theme this decade will be decarbonization from the economy.

While many investors focus on electrification and electric vehicles, this effort will actually require a multipronged effort across a number of technologies, including hydrogen, liquified natural gas, biofuels, nuclear, carbon capture, and cleaning up pollutants from heavy industry.

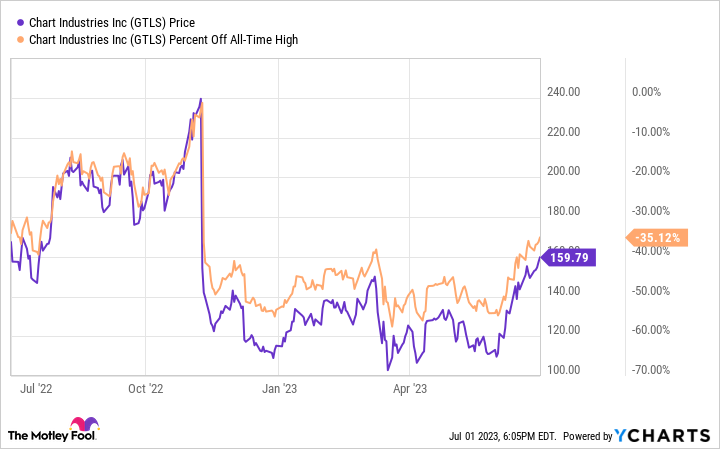

Industrial tank specialist Chart Industries (GTLS -0.76%) is exposed to all these growth trends and projects high growth for most of its end markets over the next few years. And yet, the stock is still well below its 2022 highs following a large acquisition that scared off some investors.

However, flash-forward eight months post-acquisition, and the integration looks to going according to plan — or even better. Investors should use the market’s skepticism as an entry point in this industrial growth stock.

Howdy, Howden

In November 2022, Chart announced the acquisition of industrial blower, fan, compressor, and heater specialist Howden from a private equity firm. At first, the acquisition scared off investors, as the $4.4 billion acquisition was made at an expensive-looking 12.9 enterprise value-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio, and funded with high-cost debt and equity sales.

As you can see, the reaction was swift, but Chart now seems to be beginning a recovery over the past two months:

While some investors may have balked at the price paid, Chart plans to reap ample synergies over the next three years, including at least $250 million in cost synergies and $350 million in cross-sell opportunities. Those synergies alone would amount to 13.6% of the acquisition price, or something like a 7% yield just based on synergies alone.

The cross-sell opportunities are especially tantalizing. Combining Chart’s expertise in large industrial tanks, vaporizing technology, cold boxes, liquefiers, and heat exchangers with Howden’s expertise in industrial fans and blowers, Chart is now able to offer “total solutions” to customers, rather than just products for one part of an industrial system. With both companies now able to cross-sell into each other’s large global customer base, there’s lots of potential here.

Recent developments validate the Howden thesis

A number of positive events have occurred in 2023 and even in just the past month that seem to validate the rationale behind the acquisition.

On June 14, Chart announced the expansion of its partnership with Calgary-based Kathairos for methane capture equipment in oil and gas production. The renewed partnership includes an increased number of product sales, as well as a lengthening of the contract for another two years.

Then on June 26, Chart announced that Energy Vault Holdings selected Chart’s combined solutions for its liquid clean hydrogen project, which will provide backup energy storage for Pacific Gas and Electric Co. (PG&E) to serve the city of Calistoga, California.

Cleaning up energy production, either from depolluting old industry or implementing new energy sources such as hydrogen, now makes up a huge portion of Chart’s business, especially post-Howden. Management estimates this segment, consisting of hydrogen, biofuels, liquified natural gas, carbon capture, nuclear power, electric infrastructure, and water treatment, now makes up 41% of Chart’s revenues, the company’s largest segment.

Even better: Management expects that segment to grow between 20% and 30% annually, helped along by secular trends and incentives from legislation such as the Inflation Reduction Act.

And the news gets better, as Howden also brought with it a large aftermarket services segment, which is somewhat “recurring” in that it’s tied to the installed base of equipment. The aftermarket segment, including spares, remote monitoring, software, and field service, makes up another 31% of revenue, and is expected to grow at a 20% rate.

So 72% of the “new” Chart is set to grow between 20% and 30%, and will ride the infrastructure and clean energy transition through this decade.

Paying down debt

Finally, Chart investors received yet another bit of good news in June, as the company completed a $300 million sale of a noncore Roots low-pressure compression and vacuum technologies business to Ingersoll Rand.

Management had said after the acquisition that it had identified two businesses it intended to sell for about $500 million this year, and the Roots sale made good on the first part of that promise. With enhanced credibility, Chart says the second sale of roughly another $200 million is likely to occur soon in the third quarter.

Chart stock jumped on the news, as these proceeds will help make a dent in its $4.3 billion debt load, getting the company on its way toward its deleveraging target of 2.5 to 2.9 times EBITDA by the end of 2024.

Chart is a growth stock to buy and hold

Management expects to grow EBITDA to $1.3 billion in 2024 as more synergies kick in, and at an $11 billion enterprise value today, that’s just an 8.5 times EV/EBITDA multiple. However, when one factors in another $500 million of reduced debt from divestitures, and another $300 million or so of debt paydown from cash flow this year, that would bring down the forward EV/EBITDA multiple to just 7.8.

That’s fairly cheap for a high-growth company like Chart, providing a solid entry point for buy-and-hold investors at this particular moment.