In today’s complicated market, it can be difficult to filter out the noise and focus on what matters most — achieving your financial goals. The best way to do that is by selecting top stocks and then building a diversified portfolio of companies that you believe can continue growing in the years to come.

Different stocks can serve different purposes in a balanced portfolio. For example, MercadoLibre (MELI 1.12%) is an underappreciated growth stock that has rebounded over the last year but is still a great value. NextEra Energy (NEE 1.91%) and Starbucks (SBUX 0.39%) are two rock-solid dividend stocks from different sectors of the economy. Axsome Therapeutics (AXSM -1.72%) is a biotech company with a healthy backlog of new products. And PayPal (PYPL 1.32%), a former growth stock turned value stock, is simply too cheap to ignore.

By selecting a basket of great stocks, you can blend growth, value, and income to create a portfolio that can weather bear market storms while also compounding gains over time. Find out why all five of these stocks are worth buying in July.

Image source: Getty Images.

E-commerce and digital payments in Latin America

Trevor Jennewine (MercadoLibre): MercadoLibre runs the largest online commerce and payments ecosystem in Latin America, a region with one of the fastest-growing digital economies in the world. The MercadoLibre marketplace receives nearly 4 times as many visitors as its closest competitor, and it’s projected to account for 21.6% of online retail sales in Latin America this year, up from 20.9% last year.

The company has reinforced its strong presence in commerce with value-added solutions for financing, payments, logistics, and digital advertising. Those products make its marketplace even more compelling for merchants, which enhances the network effect that drives its business. Value-added solutions have also given MercadoLibre a foothold in consumer finance. Its subsidiary Mercado Pago is the third-most-popular digital wallet among Latin American consumers, and Mercado Crédito has a thriving consumer credit business.

On the whole, MercadoLibre delivered solid financial results in the first quarter. Total revenue climbed 35% to $3 billion, as commerce revenue and fintech revenue increased 31% and 40%, respectively. On the bottom line, the company reported positive cash from operations of $859 million, up from a loss of $233 million in the prior year. Context makes those metrics even more impressive. MercadoLibre managed to grow quickly in spite of economic headwinds — for instance, first-quarter revenue actually rose 58% when the impact of unfavorable foreign exchange rates is excluded.

More importantly, MercadoLibre should be able to maintain that momentum in the future. It will undoubtedly benefit as online shopping and digital payments become more common given its strong presence in both markets. But the company also has a third growth engine in digital advertising. Following the Amazon blueprint, MercadoLibre has a burgeoning adtech business built on the popularity of its marketplace. Ad revenue increased 62% in the first quarter.

Despite those growth opportunities, shares trade at 5.4 times sales, a significant discount to their five-year average of 12.2 times sales. That’s why this stock is worth buying in July.

A top-quality dividend growth stock

Neha Chamaria (NextEra Energy): Heading into the earnings season, one stock I have my eyes on is NextEra Energy. Now, I can’t predict how the stock will perform before or after its earnings release, but I do believe NextEra Energy should, yet again, be able to deliver a strong set of numbers this July and support dividend growth.

With more economies transitioning away from fossil fuels to cleaner energy sources for their electricity needs, renewables is an attractive industry to invest in right now. Several things work in favor of NextEra Energy on that front.

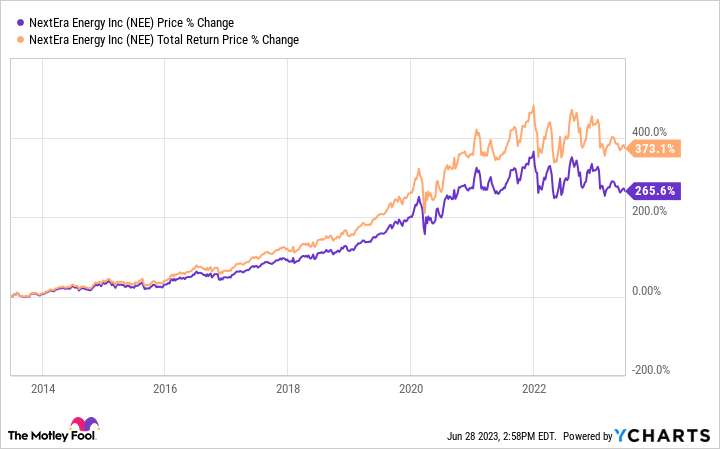

NextEra is already the world’s largest producer of electricity from wind and solar energy and has a backlog of more than 20 gigawatts (GW) of wind, solar, and battery storage contracts. That’s almost 65% of the clean energy capacity the company is currently operating. While these numbers should give you an idea about the kind of opportunity ahead of NextEra, this energy giant has also already demonstrated its capability to convert opportunities and investments into shareholder returns. Take a look at the chart below.

NextEra’s performance last quarter was so strong that although management stuck with its guidance through 2026, it said it’ll “be disappointed” if it cannot deliver numbers at the higher end of its forecast every year. NextEra expects 6% to 8% growth in adjusted earnings per share through 2026 off its 2024 estimate and sees its annual dividend per share rising by around 10% at least through 2024. Throw in a dividend yield of 2.5%, and you could earn double-digit annualized returns from NextEra Energy stock if you buy it now.

Perk up your portfolio with Starbucks

Daniel Foelber (Starbucks): There’s no denying that the stock market has had a rip-roaring 2023. A lot of quality stocks have gotten more expensive. But that doesn’t mean they aren’t decent buys. It’s just that the risk and potential reward dynamic simply isn’t what it used to be.

One stock that stands out is Starbucks. Starbucks is a well-known name, but it remains an underrated dividend stock.

In the past, Starbucks took the market by storm for its growth potential. Today, Starbucks is a mature industry-leading brand. The investment thesis has shifted from all-out growth to a balance of slow and steady growth that supports the company’s dividend.

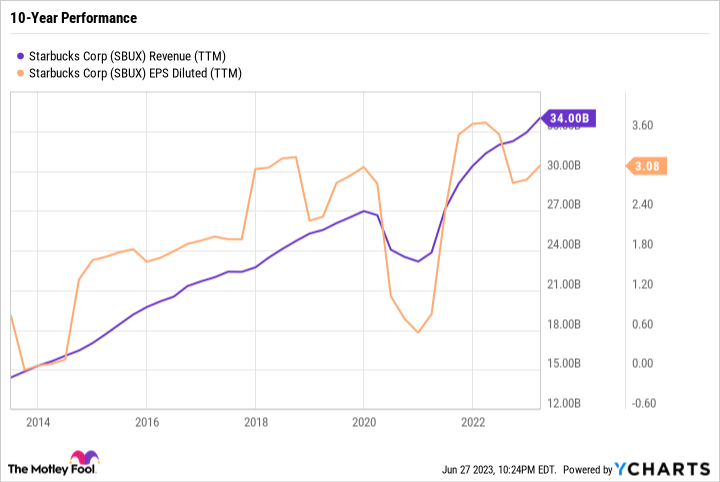

The reliability of Starbucks’ business model has been put on display over the last few years. The company’s performance nose-dived during the COVID-19 pandemic but has since recovered — and then some.

SBUX Revenue (TTM) data by YCharts

In the above chart, you can see that Starbucks is currently generating all-time-high revenue. This was no easy task, as Starbucks is heavily dependent on people commuting to work, being out and about, shopping, taking vacations, and other overall healthy consumer spending that leaves room for discretionary purchases.

As for the value portion of the equation, Starbucks isn’t all that expensive. Especially for the caliber of company we are talking about. Analyst consensus estimates for 2024 earnings per share are $4.11 — giving Starbucks a forward yield of 24, which is reasonable for Starbucks.

As for the income, Starbucks doesn’t offer the highest yield — at just 2.2%. But since it began paying a dividend in 2010, Starbucks has increased its dividend every single year. It also has a uniquely affordable dividend. Starbucks generates more free cash flow and earnings than it uses to pay its dividend — a sign the company has plenty of cushion to not only raise the dividend, but also buy back stock and reinvest in the business.

Overall, Starbucks is one of those quality stocks that is worth buying and holding forever. It just comes down to the price. Its current price isn’t dirt cheap, but it’s definitely reasonable. And that’s good enough for investors looking to put capital to work even after this recent rally.

A star-spangled biotech stock

Keith Speights (Axsome Therapeutics): Want to really add some fireworks to your investment portfolio? Consider buying shares of Axsome Therapeutics.

Sure, biotech stocks can be risky. Axsome is no exception. However, the company already has two products on the market. Auvelity won U.S. Food and Drug Administration (FDA) approval in treating major depressive disorder in 2022. Axsome picked up sleep-disorder drug Sunosi from Jazz Pharmaceuticals last year as well.

Some analysts predict that Auvelity could achieve peak annual sales of close to $1.7 billion. Sunosi won’t make that much money but could still rake in several hundred millions of dollars per year.

There’s even more to get excited about with Axsome’s pipeline. The company plans to resubmit for FDA approval of AXS-07 in treating migraine in the second half of 2023. It expects to file for FDA approval of AXS-14 in treating fibromyalgia later this year.

Axsome is evaluating Auvelity (AXS-05) in a late-stage study targeting Alzheimer’s disease agitation. It hopes to advance the drug into a pivotal phase 2/3 study for smoking cessation in the fourth quarter of 2023.

The company is also moving forward with a late-stage study of Sunosi (solriamfetol) in treating attention deficit hyperactivity disorder (ADHD). In addition, Axsome’s pipeline features AXS-12, which is being evaluated in a late-stage study for treating narcolepsy.

Despite all of this potential, Axsome’s market cap stands at only $3.7 billion. I think this is a star-spangled biotech stock that could become much bigger over time.

There’s investor value in PayPal’s steady top-line growth

Anders Bylund (PayPal): Digital payments expert PayPal may not be a high-octane growth rocket anymore, but that’s OK. There are other reasons to get excited about the company’s future profits, and the stock looks like a downright bargain these days.

Consider this: PayPal crushed Wall Street’s expectations in the first quarter, topping the performance off with bullish guidance for the rest of 2023. Yet the report inspired a sharp sell-off as management talked about an unpredictable global economy.

I think the PayPal bears overreacted to an honest and sober assessment of the volatile times we live in. Also, they took CEO Dan Schulman’s statement out of context.

“Both the macroeconomic and geopolitical environments are complex and difficult to predict,” Schulman said on the earnings call. “We know that job number one is to invest and innovate to improve our value proposition to our merchants and consumers.”

So the company is leaning into long-term growth opportunities such as unbranded checkout services and digital wallets. The product mix is evolving in a lower-margin direction, but it also adds a lot of muscle to PayPal’s top-line revenue — and the higher-growth services are still profitable.

At the end of the day, PayPal keeps delivering robust top-line growth and rock-solid free cash flows. Meanwhile, the stock price has fallen more than 75% from the all-time highs of 2021, before the inflation crunch put a heavy lid on market darlings like PayPal. Today, the stock trades at the bargain-bin valuation of 12 times forward earnings or 14 times free cash flow.

I can’t promise that PayPal’s shares will soar anytime soon, but it’s a great long-term investment at these modest prices and you should consider picking up a few shares while the markdown lasts.