The past two years have been a roller-coaster ride for Doximity (DOCS 3.65%). The company went public in mid-2021, right before equity markets started a downward spiral. And although it initially performed well, Doximity’s shares have declined and are now not that far from its initial public offering price of $26.

Doximity could be a steal at current levels, but only if a sustained rebound is on the way. Can this social networking platform for medical professionals turn things around? Let’s look into what is going on with Doximity and decide whether the company’s shares are worth investing in.

Doximity’s financial results have been slowing

There are some platforms that compete with Doximity, at least somewhat, in providing professionals with a network of like-minded people where they can advance their careers. However, Doximity focuses exclusively on doctors. Therein lies one of the company’s advantages.

Its network is dedicated only to those in the medical field who can use the platform to connect with colleagues or former classmates, seek new job opportunities, keep up with the ever-changing field with a news feed that delivers medical articles, discuss technological issues with other specialists, and more.

Unsurprisingly, more than 80% of physicians use Doximity, as do more than 90% of graduating medical students in the U.S. The platform is free for them to use, but Doximity makes revenue by charging pharmaceutical companies and health systems that use its service to communicate directly with medical professionals to post job openings and market their products (such as drugs) to physicians.

Doximity’s customers typically pay subscription fees for the services. Doximity’s platform is incredibly valuable for the parties involved. That’s why the company has found tremendous success. But it’s important to note that Doximity’s top-line growth is slowing.

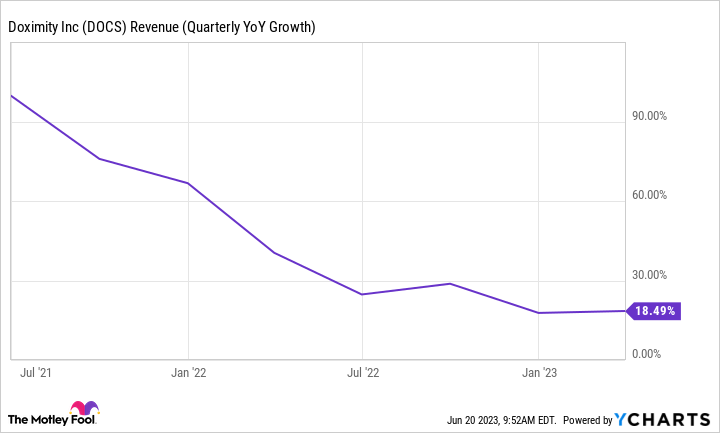

In its update for fiscal 2023’s fourth quarter (ended March 31), the company’s revenue increased 18% year over year to $111 million. Here is how that growth rate compares to the periods since its IPO.

DOCS Revenue (Quarterly YoY Growth) data by YCharts

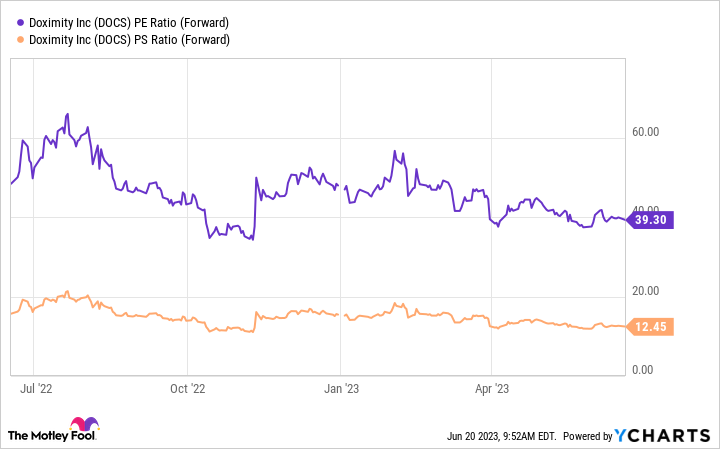

Further, Doximity’s net income of $30.7 million declined from $36.7 million in the year-ago period. Doximity’s slowing revenue growth and declining earnings are a problem, especially considering its valuation. The company’s forward price-to-earnings and forward price-to-sales ratios both look prohibitively high.

DOCS PE Ratio (Forward) data by YCharts

Unless the company can improve its financial results, its shares could remain southbound.

Looking at the company’s prospects

One of Doximity’s greatest strengths is that by making it easier for doctors to stay on top of the dynamic medical field and by facilitating communication between physicians, it makes them more effective at what they do. Doctors control the bulk of healthcare spending (more than 73% by the company’s estimates), making Doximity an ideal platform for other players in the sector.

There are some key aspects of Doximity’s business and financial results that reflect that and bode well for its future. First, there is the company’s competitive edge: the network effect, or when the value of a service increases with use. Since it is a leading platform for medical professionals and has already attracted the bulk of physicians in the U.S., that provides a powerful incentive for future doctors, or existing ones who aren’t signed up yet, to join too.

And as more of them enter Doximity’s ecosystem, the more attractive it becomes to all players involved, including pharmaceutical companies and health systems. Doximity reports that the top 20 hospitals and health systems, as well as the top 20 pharmaceutical companies by revenue, are among its clients. Second, Doximity’s retention rates, a measure of how much more or less its subscribers pay for its services compared to a previous period, are impressive.

For the trailing 12 months ended March 31, Doximity’s retention rate was 117%, signaling that its existing customers are spending more money on its services on a year-over-year basis. That’s great news for the company, especially as it still sees a huge market opportunity ahead. Doximity estimates its total addressable market (TAM) between telehealth, pharmaceutical, and health system marketing to be about $18.5 billion.

The company’s revenue for the latest 12 months is $419 million, under 3% of its TAM. Doximity’s massive untapped potential is why the company’s shares are worth buying, especially at its current price, even with its premium valuation. Its shares might remain somewhat volatile in the short run, but for investors looking at the next five years and beyond, Doximity is well-positioned to generate excellent returns.